The once-promising concept of student loan forgiveness has become a contentious and elusive topic in recent years, leaving millions of borrowers in limbo. Initially touted as a lifeline for those burdened by skyrocketing educational debt, programs like Public Service Loan Forgiveness (PSLF) and income-driven repayment plans were designed to offer relief after years of consistent payments. However, bureaucratic hurdles, stringent eligibility requirements, and inconsistent implementation have left many borrowers frustrated and disillusioned. As political debates continue and legal challenges mount, the fate of student loan forgiveness remains uncertain, leaving borrowers to question whether the relief they were promised will ever materialize.

| Characteristics | Values |

|---|---|

| Current Status | As of October 2023, most student loan forgiveness programs remain active but face legal and political challenges. The Biden administration's broad forgiveness plan was blocked by the Supreme Court in June 2023. |

| Supreme Court Ruling | The Supreme Court ruled 6-3 against the Biden administration's $400 billion student loan forgiveness plan, deeming it unconstitutional. |

| Active Programs | - Public Service Loan Forgiveness (PSLF): Available for qualifying public servants after 120 payments. - Income-Driven Repayment (IDR) Forgiveness: Forgiveness after 20-25 years of payments, depending on the plan. - Teacher Loan Forgiveness: Up to $17,500 for eligible teachers in low-income schools. - Borrower Defense to Repayment: Forgiveness for borrowers defrauded by their college. |

| One-Time Adjustment | The Biden administration implemented a one-time account adjustment in 2023, crediting borrowers with additional payments toward IDR and PSLF forgiveness. |

| SAVE Plan | The new Saving on a Valuable Education (SAVE) repayment plan launched in 2023, offering lower monthly payments and faster forgiveness for smaller balances. |

| Outstanding Student Debt | Approximately $1.77 trillion in federal and private student loan debt as of 2023. |

| Political Landscape | Student loan forgiveness remains a divisive issue, with Republicans generally opposing broad forgiveness and Democrats advocating for targeted relief. |

| Payment Restart | Student loan payments resumed in October 2023 after a three-year pause due to the COVID-19 pandemic. |

| Interest Rates | Federal student loan interest rates for 2023-2024 range from 5.5% to 8.05%, depending on the loan type. |

| Future Outlook | The Biden administration continues to explore alternative pathways for targeted debt relief, but broad forgiveness remains uncertain without legislative or legal changes. |

Explore related products

What You'll Learn

![]()

Biden’s forgiveness plan blocked by Supreme Court

In a pivotal ruling, the U.S. Supreme Court blocked President Biden’s student loan forgiveness plan in June 2023, dealing a significant blow to millions of borrowers. The Court’s 6-3 decision, rooted in the HEROES Act, determined that the administration overstepped its authority by forgiving up to $20,000 in debt per borrower without explicit congressional approval. This plan, which aimed to alleviate the $1.7 trillion student debt crisis, was halted before it could provide relief to an estimated 43 million Americans. The ruling underscored the limits of executive power and reignited debates about the role of Congress in addressing systemic financial burdens.

To understand the Court’s decision, consider the legal framework at play. The HEROES Act, invoked by the Biden administration, allows the Secretary of Education to modify student loan programs during national emergencies. However, the Court argued that the forgiveness plan went beyond mere "waiver or modification" of existing terms, effectively creating new policy. This distinction is critical: while the administration framed forgiveness as a response to the COVID-19 pandemic, the Court viewed it as an overreach, lacking the necessary legislative foundation. Borrowers, many of whom had already applied for relief, were left in limbo, their financial futures uncertain.

The fallout from this ruling extends beyond legal technicalities. For borrowers earning under $125,000 annually (or $250,000 for married couples), the promise of up to $10,000 in forgiveness—and $20,000 for Pell Grant recipients—was a lifeline. Now, they face the reinstatement of payments, which resumed in October 2023 after a three-year pause. Practical steps for affected borrowers include enrolling in income-driven repayment plans, exploring Public Service Loan Forgiveness, and contacting loan servicers to discuss options. The Court’s decision also highlights the need for legislative action, as executive solutions remain vulnerable to judicial scrutiny.

Comparatively, this setback contrasts with other countries’ approaches to student debt. In England, for instance, student loans are automatically forgiven after 30 years, regardless of repayment status. Canada offers repayment assistance based on income, while Germany provides tuition-free higher education. These examples suggest that systemic reform, rather than piecemeal forgiveness, may be necessary to address the root causes of student debt. The Supreme Court’s ruling serves as a reminder that temporary fixes, while well-intentioned, often fall short without comprehensive policy changes.

Moving forward, advocates and policymakers must pivot to sustainable solutions. Congress could pass legislation capping interest rates, expanding Pell Grants, or creating a universal forgiveness program with clear eligibility criteria. Borrowers, meanwhile, should stay informed about updates from the Department of Education and explore state-level relief programs. While Biden’s plan was blocked, the conversation it sparked about the affordability of higher education remains vital. The Court’s decision is not the end of the road but a call to action for more robust, permanent reforms.

Hope Waltz's Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

![]()

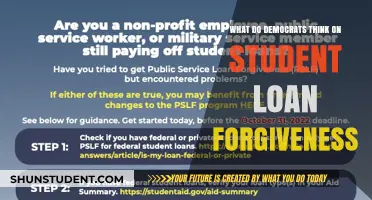

Public Service Loan Forgiveness (PSLF) updates

The Public Service Loan Forgiveness (PSLF) program has undergone significant changes in recent years, leaving many borrowers both hopeful and confused. One of the most notable updates came in October 2021 with the introduction of the Limited PSLF (TEPSLF) Waiver, which temporarily relaxed the program’s stringent eligibility rules. This waiver allowed borrowers to receive credit for past payments made under any federal loan plan, not just income-driven repayment plans, and it recognized payments made on consolidated loans that were previously disqualified. For example, a teacher who had been paying under a standard repayment plan for a decade could suddenly qualify for forgiveness, provided they met the public service employment criteria. This waiver expired in October 2022, but its impact highlighted the program’s potential when barriers are removed.

Another critical update is the PSLF Processing Improvements implemented by the Department of Education. Historically, PSLF applications were plagued by bureaucratic inefficiencies, with many borrowers denied due to technicalities like incorrect payment counts or loan servicer errors. In response, the department introduced a more streamlined application process and partnered with the U.S. Digital Service to modernize its systems. Borrowers can now track their progress through the PSLF Help Tool, which provides real-time updates on qualifying payments and employment certification. While these changes have reduced frustration, they also underscore the need for borrowers to proactively monitor their accounts and submit employment certifications annually to avoid setbacks.

Despite these advancements, challenges remain. The income-driven repayment (IDR) account adjustment, announced in 2022, aimed to correct historical errors in payment counting, particularly for borrowers pursuing PSLF. This adjustment retroactively credited borrowers for months spent in forbearance or certain repayment plans, bringing many closer to forgiveness. However, the rollout has been slow, and some borrowers report discrepancies in their payment counts. For instance, a social worker who had been in forbearance for two years during graduate school might now see those months counted toward PSLF, but only if they actively review their account and dispute inaccuracies. This highlights the importance of vigilance and advocacy in navigating the program.

Looking ahead, the PSLF On-Ramp initiative, launched in 2023, offers a final opportunity for borrowers to receive credit for past payments that were previously disqualified. This temporary measure, ending in October 2024, is designed to bridge gaps caused by administrative errors or servicer mismanagement. For example, a nonprofit employee who made 10 years of payments but was denied due to a loan consolidation error can now have those payments counted. To take advantage, borrowers must ensure their employment certification forms are up to date and their loans are in good standing. While these updates represent progress, they also reveal the program’s ongoing complexity, emphasizing the need for clear communication and borrower education.

In conclusion, the PSLF program is evolving, with updates aimed at making forgiveness more accessible and less frustrating. However, borrowers must remain proactive, leveraging tools like the PSLF Help Tool and staying informed about policy changes. For those in public service, the potential for debt relief is real, but it requires persistence and attention to detail. As the program continues to improve, its success will depend on both administrative reforms and borrowers’ willingness to engage with the process.

Qualifying for New Student Loan Forgiveness: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Income-Driven Repayment (IDR) account adjustments

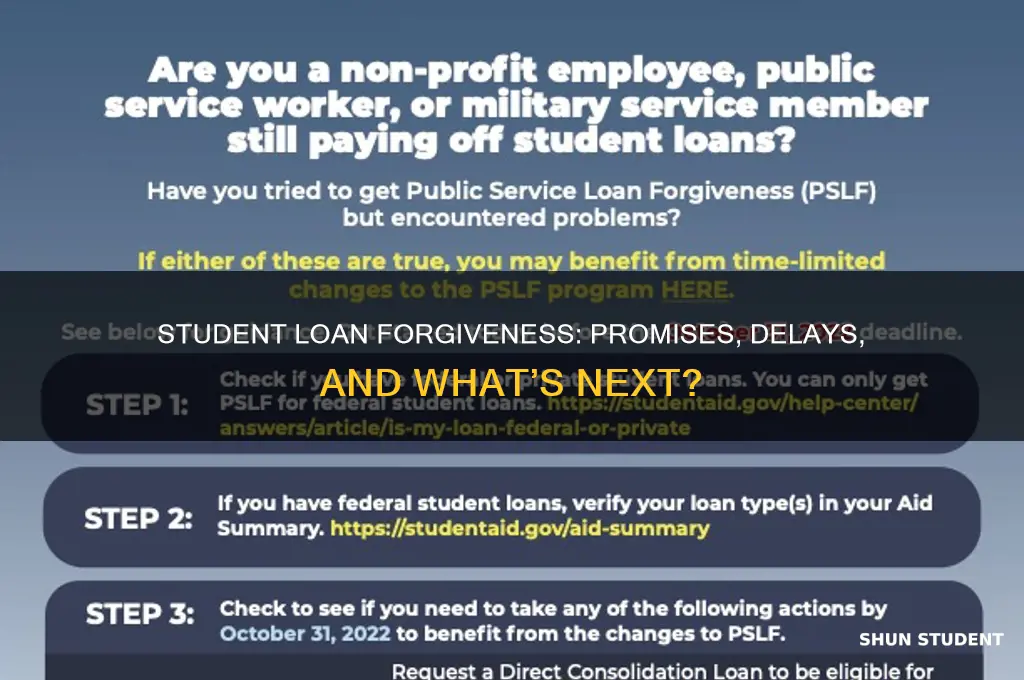

The U.S. Department of Education recently announced a one-time account adjustment for Income-Driven Repayment (IDR) plans, addressing longstanding issues with payment counting. This adjustment, part of broader student loan forgiveness efforts, aims to correct errors in tracking qualifying payments, ensuring borrowers receive credit toward forgiveness milestones. For example, months in deferment or forbearance due to economic hardship may now count toward the required 240 or 300 payments for forgiveness, potentially shaving years off repayment timelines.

To benefit from this adjustment, borrowers must consolidate loans into a Direct Consolidation Loan by December 31, 2023, if their loans are not already in the Direct Loan program. This step is crucial for Federal Family Education Loan (FFEL) or Perkins Loan holders, as only Direct Loans qualify for IDR adjustments. After consolidation, the Department will automatically review accounts, applying forgone payments retroactively. Borrowers nearing forgiveness thresholds may see immediate loan discharge without further action.

However, this adjustment is not without caveats. Payments made under now-discontinued plans, like the original Income-Contingent Repayment (ICR) plan, may not qualify unless borrowers switch to an eligible IDR plan. Additionally, time spent in certain statuses, such as administrative forbearance during loan transfers, may still be excluded. Borrowers should log into their Federal Student Aid account to verify payment counts post-adjustment and dispute inaccuracies if necessary.

The IDR account adjustment underscores a shift toward rectifying systemic flaws in student loan servicing. By recalibrating payment counts, the Department aims to restore trust and accelerate forgiveness for millions. For instance, a borrower with 10 years of payments under an ineligible plan could see those years applied toward the 20- or 25-year forgiveness timeline after switching to a qualifying IDR plan. This move complements other initiatives, like Public Service Loan Forgiveness (PSLF) waivers, in addressing the $1.7 trillion student debt crisis.

Practical steps for borrowers include monitoring updates from loan servicers, ensuring contact information is current, and avoiding unnecessary forbearance or deferment. Those with mixed loan types should prioritize consolidation to streamline eligibility. While the adjustment offers relief, it is not a blanket solution; borrowers must remain proactive in navigating the complexities of IDR plans. As the Department continues to refine policies, staying informed and engaged remains key to maximizing forgiveness opportunities.

Block Unwanted Calls: Stop Student Loan Forgiveness Scams Now

You may want to see also

Explore related products

![]()

State-level forgiveness programs emerging

As federal student loan forgiveness programs face legal challenges and bureaucratic delays, states are stepping in to fill the void with their own initiatives. These state-level programs, though smaller in scale, offer targeted relief to borrowers in specific professions or facing particular financial hardships. For instance, New York’s “Get on Your Feet” loan forgiveness program provides up to $17,500 in relief for recent college graduates earning less than $50,000 annually, addressing the unique challenges of early-career professionals burdened by debt.

Consider the structure of these programs as a patchwork of solutions rather than a one-size-fits-all approach. States like California and Minnesota have launched forgiveness initiatives for public servants, including teachers, nurses, and social workers, with California’s program offering up to $50,000 in relief for those working in underserved communities. Meanwhile, Maryland’s “SmartBuy” program takes a creative turn by forgiving up to $30,000 in student loans for homebuyers purchasing their first home in the state, linking debt relief to economic development goals.

While these programs offer hope, they come with caveats. Eligibility criteria can be stringent, often requiring borrowers to commit to multi-year service obligations or meet specific income thresholds. For example, Texas’ Loan Repayment Assistance Program for mental health professionals requires a two-year commitment to serve in a Health Professional Shortage Area. Borrowers must carefully review program terms to ensure they qualify and can fulfill the requirements, as failing to do so may result in clawbacks or penalties.

The emergence of state-level forgiveness programs underscores a shift toward localized solutions in the absence of comprehensive federal action. However, their impact is limited by funding constraints and varying political priorities across states. Advocates argue that these initiatives, while valuable, are no substitute for federal reform, as they leave many borrowers in states without such programs behind. Still, for those who qualify, these programs provide a lifeline, offering tangible relief from the crushing weight of student debt.

To maximize the benefits of these programs, borrowers should proactively research opportunities in their state, often available through higher education or workforce development agencies. Additionally, tracking legislative developments can uncover new programs as states continue to innovate in response to the student debt crisis. While state-level forgiveness may not solve the problem entirely, it represents a critical step toward addressing the financial burdens faced by millions of Americans.

Steps to Apply for Student Loan Forgiveness: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Loan cancellation scams targeting borrowers

As the student loan forgiveness landscape continues to shift, borrowers are increasingly vulnerable to scams promising debt cancellation. Fraudsters exploit confusion surrounding government programs, preying on those desperate for financial relief. Understanding their tactics is crucial to avoiding becoming a victim.

Scammers often impersonate government agencies or legitimate debt relief companies, using official-sounding language and logos to appear credible. They may claim exclusive access to "limited-time" forgiveness programs or guarantee loan cancellation for an upfront fee. Red flags include aggressive sales tactics, requests for sensitive information like Social Security numbers or bank account details, and pressure to act immediately.

One common scam involves companies charging exorbitant fees for services borrowers can access for free through their loan servicers. These companies may promise to negotiate lower payments or even complete forgiveness, but often deliver little to no results. Another tactic is phishing emails or text messages claiming your loans have been forgiven, requiring you to click a link or provide personal information to "confirm" the cancellation. These links often lead to malicious websites designed to steal your data.

Remember, legitimate student loan forgiveness programs are administered through the U.S. Department of Education and your loan servicer. There are no shortcuts or secret programs requiring upfront payments.

To protect yourself, never share personal information with unsolicited callers or respond to suspicious emails or texts. Verify any company's legitimacy by checking with the Better Business Bureau and the Consumer Financial Protection Bureau. If you're unsure about a program or offer, contact your loan servicer directly. They can provide accurate information about your repayment options and any available forgiveness programs. Staying informed and vigilant is your best defense against falling victim to these predatory scams.

When Will Student Loan Forgiveness Finally Become a Reality?

You may want to see also

Frequently asked questions

Student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) forgiveness, still exist but have faced challenges. The Biden administration has made efforts to improve these programs, including temporary waivers and reforms to address issues like improper payment counts and servicing errors.

Widespread student loan forgiveness has been stalled due to legal challenges, political opposition, and concerns about its cost and fairness. The Supreme Court struck down President Biden’s plan for broad debt cancellation in 2023, limiting forgiveness to targeted programs like PSLF and IDR.

While no new broad forgiveness programs have been introduced, the Biden administration has expanded existing ones. For example, the SAVE Plan (Saving on a Valuable Education) offers faster forgiveness for smaller balances and lowers monthly payments for many borrowers.

Borrowers should ensure their loans are enrolled in eligible programs like PSLF or IDR, keep track of qualifying payments, and stay updated on policy changes. They can also explore temporary relief measures, such as the payment pause extensions or waivers, to manage their debt while waiting for forgiveness.