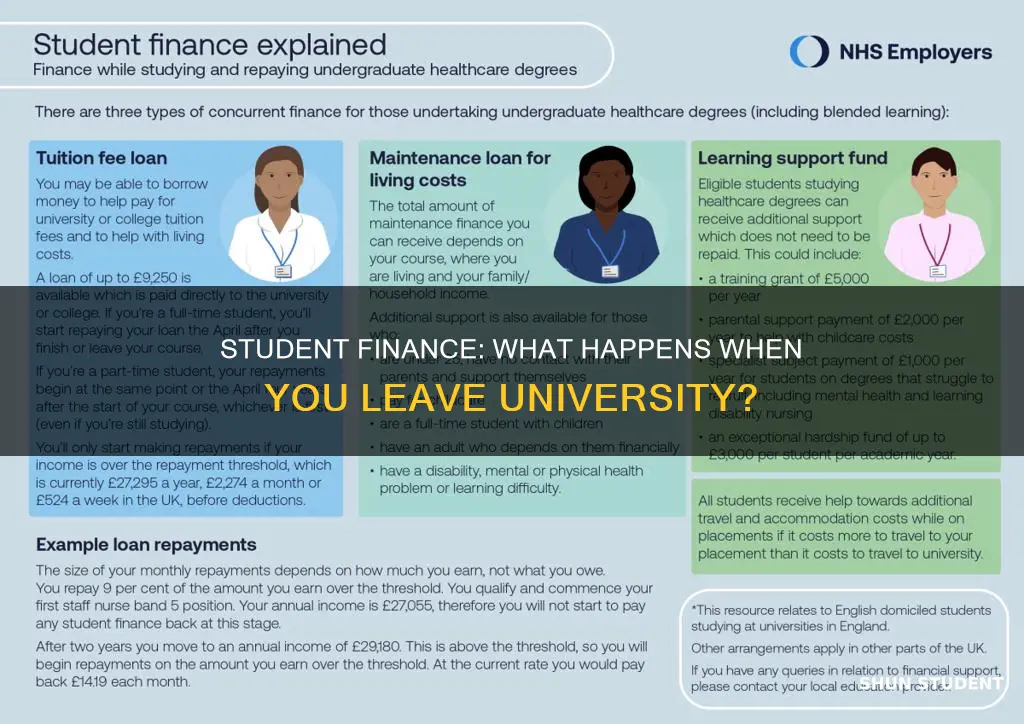

If you're considering leaving university, it's important to understand the financial implications of your decision. The consequences for your student finance depend on a number of factors, including the type of funding you have, the reason for leaving, and whether you plan to return to your studies. You may still be entitled to some student finance during a suspension period, for example, if you're experiencing financial hardship or illness. However, if you withdraw completely, you will usually be required to repay any Tuition Fee Loan and Maintenance Loan that you have received. The amount you need to repay will depend on the number of days you attended your course, and you may be able to set up a repayment plan if you cannot afford to pay the full amount immediately.

| Characteristics | Values |

|---|---|

| If you suspend your studies | You might still be able to get student finance while you’re away, for example, if you’re experiencing financial hardship, or you suspended due to a caring responsibility or illness. |

| If you withdraw from your studies | You will be responsible for repaying any Tuition Fee Loan and Maintenance Loan. If you have been overpaid, you may need to repay this early. |

| If you have been overpaid | The amount you were overpaid will usually be taken off your student finance payments when you return, so you do not have to repay straight away. |

| If you have a federal student loan | You may be eligible for a grace period of six months before you have to start making payments. |

| If you have a private student loan | Refinancing could lower your interest rate, especially if your credit and income have improved. |

Explore related products

What You'll Learn

![]()

Notify Student Finance England and your university

If you decide to suspend or withdraw from your studies, you must notify Student Finance England and your university as soon as possible. This is to minimise the risk of being overpaid by Student Finance. Your university or college will inform Student Finance England of the date you finished your course, and they will reassess your Maintenance Loan based on the number of days you attended. If your loan covers any period after you left your course, this will be treated as an overpayment, and you will need to repay it immediately.

If you suspend your studies due to illness or another serious personal reason, you may still be eligible for student finance during this period. You will usually need to send Student Finance England evidence, such as bank statements or a letter from your university. If you suspended your studies on health grounds, you will receive full student finance for 60 days after you suspend.

If you decide to withdraw from your course, you will be responsible for repaying any Tuition Fee Loan and Maintenance Loan. The amount of the Tuition Fee Loan you will need to repay will depend on the date you withdrew from your course. Student Finance England will contact you to discuss affordable repayment options.

If you have federal student loans, you may be eligible for a grace period before you need to start making payments. Most federal student loans allow a six-month grace period to give you time to get your finances in order. You may also be eligible for an income-driven repayment plan, which calculates your monthly payment as a percentage of your income.

Exploring Lee University's Student Population

You may want to see also

Explore related products

![]()

Repayment of Tuition Fee Loan and Maintenance Loan

If you decide to suspend or withdraw from your studies, it is important to understand how you will repay any money you have borrowed. You will be responsible for repaying your Tuition Fee Loan and Maintenance Loan, unless you were overpaid. Your university or college will inform your student finance provider of the date you finished your studies, and they will reassess your Maintenance Loan based on the number of days you attended your course. Any loan covering the period after you left your course will be considered an overpayment, which you will need to repay immediately. If you cannot repay the full amount, you can request a repayment plan. The rest of your Maintenance Loan is repaid as usual once you start earning over the threshold amount.

The amount you were overpaid will typically be deducted from your student finance payments when you return to your studies, so you do not have to repay it right away. However, if you have been overpaid a Childcare Grant, your future payments will not be reduced. Student Finance England will contact you after you have left your course to discuss affordable repayment options. The amount of Tuition Fee Loan you will need to repay depends on when you suspended or withdrew from your course.

It is important to note that dropping a class does not always impact your student loans. Usually, early repayment is only triggered if your enrolment drops below half-time status. However, each school has its own policies regarding financial aid eligibility. Withdrawing from a class could impact your academic progress, which may affect your graduation eligibility. If you switch from full-time to part-time status, your federal aid amount will be adjusted accordingly.

If you are considering suspending or withdrawing from your studies due to financial concerns, it is recommended to explore repayment options with your lender. Federal student loan borrowers may be eligible for income-driven repayment plans or forbearance during periods of financial hardship. Private student loans may offer refinancing options to lower your interest rate.

Ball State University's Undergraduate Population

You may want to see also

Explore related products

![]()

Overpayment and repayment plans

If you leave university, your university or college will inform your student finance provider of your last day of attendance. Your student finance provider will then reassess your loan and grant amounts based on the number of days you attended your course. Any amount that covers the period after you left your course is considered an overpayment and must be repaid separately from your regular loan repayments. You must repay overpayments as soon as possible, regardless of your earnings. If you are unable to repay the full amount immediately, you can contact your student finance provider to set up a repayment plan.

Overpayments can occur for various reasons, such as changes in your personal circumstances, course changes, or incorrect income assessments. It is important to regularly review your student finance entitlement and notify your student finance provider of any changes to avoid overpayments.

If you accidentally overpay your student loan, you may be able to reclaim the overpaid amount. This can be done by contacting your student finance provider and requesting a refund. Additionally, if you are in the last two years of your loan repayments, you can set up monthly Direct Debit payments directly to the Student Loans Company (SLC) to avoid overpaying due to communication breakdowns between SLC and the tax office.

It is important to note that overpaying smaller amounts may not reduce your future payments, and it may be more beneficial to reclaim the overpaid amount, especially if you are in a low-earning profession. However, for very high earners who will clear their loans, overpaying can be advantageous.

If you are unsure about your repayment options or require financial assistance, you can contact your university or college for advice or seek support from organisations like Student Finance England.

Jewish Students at University of Virginia: How Many?

You may want to see also

Explore related products

$17.49 $27.33

$19.95 $19.95

$28.99

![]()

Impact on other financial aid

Leaving university early can impact other financial aid you are receiving beyond student loans. The repercussions differ depending on the type of grant or scholarship you are receiving and the timing of when you drop out. If you have received a federal student grant in the US and you withdraw after completing 60% of the semester, you will not need to repay it. However, if you drop out before this threshold, you will likely be required to repay some or all of the grant. Similarly, you may need to repay a scholarship depending on the award's stipulations, so it is important to check the terms of the award.

Withdrawing from a class could impact your satisfactory academic progress, which institutions use to determine eligibility for graduation and financial aid. If you go from full-time to part-time status, your federal aid amount will be adjusted accordingly. Dropping below half-time enrolment often makes you ineligible for federal financial aid, including federal student loans, as most schools have requirements for minimum enrolment to qualify for aid. Private lenders may also have similar enrolment requirements that can impact your eligibility for their financial aid.

If you are receiving financial aid from the UK government, you may still be able to get student finance during your suspension period if you are experiencing financial hardship, have caring responsibilities, or are ill. You will need to provide evidence, such as bank statements or a letter from your university or college, and each case is assessed individually. If you suspend your studies due to illness, you will receive full student finance for 60 days after you suspend, and your university or college should automatically notify the Student Finance England office.

It is important to understand the financial implications of leaving university early to make an informed decision. Contacting your university's financial aid office or a relevant government body, such as Student Finance England, can provide you with specific advice and guidance on managing your financial aid and loans.

UMES Student Population: How Many Terrapins?

You may want to see also

Explore related products

![]()

Grace periods and refinancing

If you decide to suspend or withdraw from your studies, it is important to understand the financial implications. You will be responsible for repaying any Tuition Fee Loan and Maintenance Loan from Student Finance England. The amount you repay will depend on the number of days you attended your course, and whether you were overpaid after suspending or withdrawing. In the case of an overpayment, you may need to repay this amount early, and Student Finance England will advise you on how to do so.

When you leave university, your loan status changes, and you will need to start making payments. Most federal student loans allow a six-month grace period before you must start repaying, giving you time to get your finances in order and find employment. During this grace period, you can also look into refinancing options to lower your interest rate, especially if your credit score and income have improved.

If you are experiencing financial hardship, you may be able to request forbearance on your loan, which pauses payments for 12 months, although interest will continue to accrue. Alternatively, federal student loan borrowers may be eligible for an income-driven repayment plan (IDR), which calculates monthly payments as a percentage of your income. While these plans lower your monthly payment, they extend the repayment period, potentially resulting in higher interest over time.

It is important to understand your loan type and contact your lender to discuss repayment options as soon as possible. This will help you navigate the financial implications of leaving university and ensure you are aware of any grace periods or refinancing options available to you.

Confronting Students: A Christian University Instructor's Dilemma

You may want to see also

Frequently asked questions

You need to contact Student Finance England and let your university or college know as soon as possible. They will then reassess your student finance based on the number of days you attended your course.

Your loan status changes, and you will need to start making payments. However, with certain types of loans, you may be eligible for a grace period. For example, most federal student loans allow a six-month grace period before you have to start making payments.

If any of your grant or bursary covers the period after you’ve left your course, this counts as an overpayment and you’ll need to repay it straight away. However, you don’t have to pay back overpayments on these grants until you’ve finished your course.