The topic of student loan forgiveness has gained significant attention, particularly regarding the criteria for eligibility and the sources of income that will be considered for relief. As discussions continue, many borrowers are eager to understand what income will be used to determine their eligibility for loan forgiveness programs. This includes whether adjusted gross income (AGI), taxable income, or other financial metrics will be the primary factor in assessing qualification. Clarifying these details is crucial for millions of borrowers who are hoping to benefit from potential forgiveness initiatives, as it directly impacts their financial planning and long-term debt management strategies.

| Characteristics | Values |

|---|---|

| Income Threshold for Forgiveness | Borrowers earning less than $12,885 (single) or $26,500 (married/head of household) annually may qualify for full loan forgiveness under the Saving on a Valuable Education (SAVE) Plan. |

| Income Calculation Method | Adjusted Gross Income (AGI) or an alternative measure if AGI is not available. |

| Discretionary Income Definition | Income above the poverty line, adjusted for family size, used to determine repayment amounts. |

| Poverty Line Reference | Based on federal poverty guidelines, which vary by state and family size. |

| Income-Driven Repayment (IDR) Plans | Payments capped at 5-10% of discretionary income, depending on the plan. |

| Public Service Loan Forgiveness (PSLF) | Requires 10 years of qualifying payments under an IDR plan while working full-time for a qualifying employer. |

| Tax Treatment of Forgiven Amounts | Forgiven amounts are generally tax-free through 2025 under the American Rescue Plan Act. |

| Income Recertification | Borrowers must recertify income annually for IDR plans to maintain eligibility. |

| Spousal Income Consideration | Married borrowers filing jointly must include spousal income in calculations. |

| Income Limits for Full Forgiveness | Borrowers below the poverty line may qualify for $0 monthly payments and eventual forgiveness. |

Explore related products

What You'll Learn

- Federal vs. Private Loans: Only federal student loans qualify for forgiveness programs like PSLF or IDR

- Income-Driven Repayment Plans: Forgiveness after 20-25 years of payments based on adjusted gross income

- Public Service Loan Forgiveness (PSLF): Requires 10 years of qualifying payments while working full-time in public service

- Tax Implications: Forgiven amounts may be taxable unless under specific programs like PSLF

- Eligibility Criteria: Income, employment, and repayment plan determine qualification for loan forgiveness programs

![]()

Federal vs. Private Loans: Only federal student loans qualify for forgiveness programs like PSLF or IDR

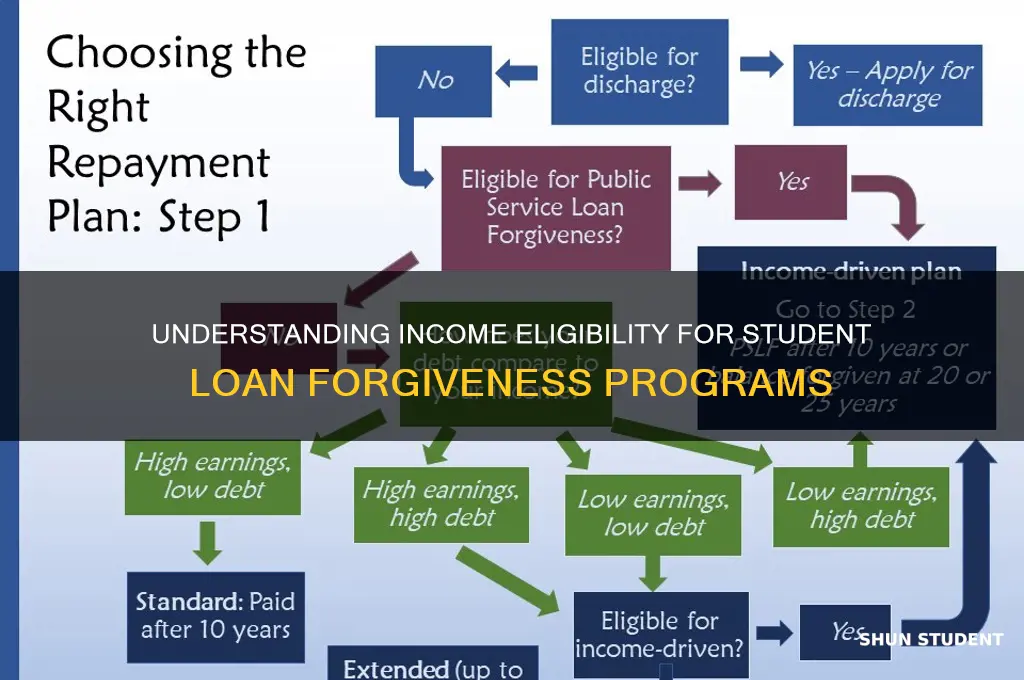

Federal student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and Income-Driven Repayment (IDR) plans, hinge on a critical distinction: only federal loans qualify. Private loans, despite often carrying higher interest rates and fewer protections, are ineligible for these programs. This means borrowers with private loans must rely on standard repayment terms or seek refinancing, which may or may not offer better conditions. Understanding this difference is the first step in strategizing how to manage your student debt effectively.

For those with federal loans, the income used for forgiveness calculations under IDR plans is typically based on your Adjusted Gross Income (AGI) from your most recent tax return. These plans cap your monthly payments at a percentage of your discretionary income, usually 10-20%, depending on the plan. For example, if your AGI is $40,000 and you’re on the Revised Pay As You Earn (REPAYE) plan, your payments would be 10% of the difference between your income and 150% of the federal poverty guideline for your family size. After 20-25 years of qualifying payments, any remaining balance is forgiven, though it may be taxed as income.

PSLF, on the other hand, requires 120 qualifying payments while working full-time for a government or nonprofit employer. The income level itself is less relevant here, as forgiveness is tied to employment and consistent payments, not a percentage of earnings. However, borrowers often pair PSLF with an IDR plan to minimize payments during the 10-year qualification period. For instance, a teacher earning $50,000 annually could reduce monthly payments significantly under an IDR plan while working toward PSLF, making the program more manageable.

Private loan borrowers have fewer options but can explore refinancing to lower interest rates or extend repayment terms. Some employers also offer student loan repayment assistance as a benefit, which can help offset the burden. However, these strategies do not provide the same level of relief as federal forgiveness programs. For example, refinancing a $30,000 private loan from 8% to 5% interest could save thousands over the life of the loan, but it won’t eliminate the debt entirely.

In summary, federal loans offer pathways to forgiveness through programs like PSLF and IDR, with income playing a central role in determining repayment amounts. Private loans, however, require a different approach, focusing on refinancing or employer assistance. Borrowers should carefully assess their loan types and explore all available options to make informed decisions about managing their student debt.

Forgiving Sallie Mae Student Loans: A Step-by-Step Guide to Relief

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans: Forgiveness after 20-25 years of payments based on adjusted gross income

For borrowers enrolled in Income-Driven Repayment (IDR) plans, the promise of student loan forgiveness after 20–25 years hinges on one critical factor: adjusted gross income (AGI). This metric, derived from your federal tax return, determines your monthly payment amount and, ultimately, your eligibility for forgiveness. Unlike discretionary income, which varies by plan, AGI is a standardized figure that reflects your total income minus specific deductions, such as retirement contributions and student loan interest. Understanding how AGI influences your repayment journey is essential for maximizing forgiveness benefits.

Consider this scenario: A borrower earning $50,000 annually with a family size of two might have an AGI of $48,000 after deductions. Under the Revised Pay As You Earn (REPAYE) plan, their monthly payment would be 10% of their discretionary income, calculated as the difference between AGI and 150% of the poverty guideline for their family size. If their AGI remains relatively stable, they could qualify for forgiveness after 20 years of consistent payments. However, if their income increases significantly, their AGI would rise, potentially raising their monthly payments and delaying forgiveness. This underscores the importance of monitoring AGI annually, especially during tax season, to ensure your repayment strategy aligns with your financial goals.

A common misconception is that AGI must remain low to secure forgiveness. While lower AGI results in smaller payments, it’s not a requirement for forgiveness—it’s the *consistency* of payments over 20–25 years that matters. For instance, a borrower with fluctuating income might have years with higher AGI, leading to larger payments, but as long as they remain in an IDR plan and make timely payments, they’ll still qualify for forgiveness. Practical tips include maximizing deductions to lower AGI (e.g., contributing to retirement accounts) and annually recertifying your income to ensure your payment amount reflects your current financial situation.

Comparatively, IDR plans offer a more forgiving structure than standard repayment plans, which don’t consider AGI and have no forgiveness option. For example, a borrower with $100,000 in loans on a standard 10-year plan would pay approximately $1,150 monthly, regardless of income. In contrast, an IDR plan might reduce their payment to $200–$300 monthly based on their AGI, with the remaining balance forgiven after 20–25 years. This makes IDR plans particularly advantageous for borrowers with high debt-to-income ratios, as forgiveness provides a clear endpoint to their repayment journey.

In conclusion, AGI is the linchpin of Income-Driven Repayment plans, dictating both monthly payments and the timeline for forgiveness. By strategically managing your AGI through deductions and annual recertification, you can optimize your repayment strategy and position yourself for forgiveness after 20–25 years. While income fluctuations are inevitable, staying in an IDR plan and making consistent payments ensures you remain on track to eliminate your student debt. For borrowers overwhelmed by student loans, understanding and leveraging AGI within IDR plans can transform a seemingly endless repayment journey into a manageable path toward financial freedom.

Forgiving Student Loans for Teachers: A Comprehensive Guide to Debt Relief

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Requires 10 years of qualifying payments while working full-time in public service

Public Service Loan Forgiveness (PSLF) offers a clear path to debt relief for those committed to a decade of service in the public sector. However, understanding which income qualifies for this program is crucial to maximizing its benefits. The PSLF program uses your Adjusted Gross Income (AGI) as the basis for determining your monthly payments under an income-driven repayment (IDR) plan, which is a prerequisite for PSLF eligibility. Your AGI includes wages, salaries, tips, and other taxable income, minus certain deductions like student loan interest and contributions to retirement accounts. For example, if you earn $60,000 annually but contribute $5,000 to a 401(k) and pay $1,000 in student loan interest, your AGI would be $54,000, potentially lowering your monthly payment under an IDR plan.

To qualify for PSLF, you must make 120 qualifying payments while working full-time for a qualifying employer. These payments are based on your income under an IDR plan, which adjusts your monthly payment to a percentage of your discretionary income. For instance, under the Revised Pay As You Earn (REPAYE) plan, your payment is 10% of your discretionary income, defined as the difference between your AGI and 150% of the poverty guideline for your family size. If your AGI is $54,000 and you’re single, your discretionary income would be approximately $40,000 (assuming a poverty guideline of $14,580 in 2023). Your monthly payment would then be roughly $333, making it easier to manage while working in a lower-paying public service role.

One critical aspect of PSLF is that your income level directly impacts the amount forgiven after 10 years. Since IDR plans cap your payments based on income, borrowers with lower AGIs will pay less over the 10-year period, resulting in a larger balance forgiven tax-free. For example, a borrower earning $40,000 annually might pay around $25,000 over 10 years under an IDR plan, while someone earning $80,000 might pay closer to $70,000. The remaining balances—potentially $50,000 or more—are forgiven, making PSLF particularly advantageous for those with modest incomes in public service roles.

To ensure your income is optimally used for PSLF, consider strategies like maximizing pre-tax deductions to lower your AGI. Contributions to retirement accounts, health savings accounts (HSAs), and dependent care flexible spending accounts (FSAs) can reduce your taxable income, thereby lowering your IDR payments. Additionally, annually recertifying your income for your IDR plan is essential, as changes in income or family size can adjust your monthly payment. For instance, if you receive a raise, recertifying ensures your payment remains affordable and continues to qualify for PSLF.

In summary, PSLF hinges on your AGI and its role in determining your IDR payments. By understanding how income is calculated and strategically managing deductions, you can minimize payments and maximize forgiveness. For public service workers, this program offers a lifeline, but it requires careful planning and adherence to its specific rules. Whether you’re a teacher, social worker, or nonprofit employee, leveraging your income effectively can make the difference between a decade of manageable payments and a life-changing debt discharge.

Is Student Loan Debt Forgiveness Automatic? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Tax Implications: Forgiven amounts may be taxable unless under specific programs like PSLF

Forgiven student loan amounts can feel like a financial windfall, but the taxman may still come knocking. The IRS generally considers forgiven debt as taxable income, meaning you could owe taxes on the amount wiped away. This unexpected liability can sting borrowers who haven’t planned for it, turning relief into a financial headache. However, not all forgiveness programs are created equal. Understanding the tax treatment of forgiven student loans is crucial to avoiding surprises come tax season.

Take the Public Service Loan Forgiveness (PSLF) program, for instance. Under PSLF, borrowers who make 120 qualifying payments while working full-time for a government or nonprofit organization can have their remaining balance forgiven tax-free. This exception is a significant benefit, as it allows borrowers to avoid the tax burden that often accompanies other forgiveness programs. For example, if you have $50,000 forgiven under PSLF, you won’t owe a dime in taxes on that amount. In contrast, forgiveness through income-driven repayment plans like Income-Based Repayment (IBR) or Pay As You Earn (PAYE) typically results in taxable income, unless the forgiveness occurs under the limited-time provisions of the American Rescue Plan Act of 2021, which temporarily excludes such forgiveness from taxation through 2025.

To navigate these complexities, borrowers should proactively plan for potential tax liabilities. If you’re pursuing forgiveness outside of PSLF, estimate the taxable amount and set aside funds to cover the tax bill. For example, if $30,000 is forgiven under an income-driven plan, you might owe $7,500 in taxes (assuming a 25% tax bracket). Using tax software or consulting a financial advisor can help you calculate this accurately. Additionally, consider adjusting your tax withholdings or making quarterly estimated tax payments to avoid penalties for underpayment.

A comparative analysis reveals the stark difference in tax treatment between programs. While PSLF offers a clear path to tax-free forgiveness, other programs leave borrowers vulnerable to unexpected tax bills. This disparity underscores the importance of choosing the right repayment strategy based on your long-term financial goals. For instance, a borrower with a high debt-to-income ratio might prioritize PSLF for its dual benefits of tax-free forgiveness and public service alignment, whereas someone with a shorter repayment timeline might opt for standard repayment to avoid tax complications altogether.

In conclusion, forgiven student loan amounts are not always a free pass. Borrowers must carefully consider the tax implications of their chosen forgiveness program to avoid financial surprises. By understanding the rules, planning ahead, and seeking professional guidance when needed, you can maximize the benefits of loan forgiveness while minimizing its tax impact. After all, the goal is to achieve financial freedom, not trade one debt for another.

Which Student Loans Deserve Forgiveness? A Comprehensive Guide to Eligibility

You may want to see also

![]()

Eligibility Criteria: Income, employment, and repayment plan determine qualification for loan forgiveness programs

Student loan forgiveness programs often hinge on a borrower's income, employment, and repayment plan, creating a complex eligibility matrix. For instance, the Public Service Loan Forgiveness (PSLF) program requires 120 qualifying payments while working full-time for a government or nonprofit organization. However, the income used to determine eligibility isn’t just your annual salary—it’s the Adjusted Gross Income (AGI) reported on your federal tax return. This distinction is critical because deductions, credits, and exemptions can significantly lower your AGI, potentially making you eligible for income-driven repayment (IDR) plans like REPAYE or PAYE, which cap monthly payments at 10-15% of discretionary income. Understanding this interplay between income and repayment plans is the first step in navigating forgiveness eligibility.

Employment plays a dual role in determining eligibility, particularly for programs like PSLF or Teacher Loan Forgiveness. For PSLF, the employer must qualify as a government or 501(c)(3) nonprofit organization, and the borrower must be employed full-time (at least 30 hours per week). Part-time workers in public service may still qualify if their combined hours meet the full-time threshold. For Teacher Loan Forgiveness, eligibility requires five consecutive years of teaching in a low-income school, with income indirectly factored in through the school’s designation. Borrowers should verify their employer’s eligibility using the PSLF Help Tool or consult their HR department to ensure their employment meets program requirements.

Repayment plans act as the bridge between income and forgiveness, with IDR plans being the most common pathway. For example, the Income-Based Repayment (IBR) plan caps payments at 10-15% of discretionary income, depending on when the loan was taken out. After 20-25 years of qualifying payments, the remaining balance is forgiven, though the forgiven amount may be taxed as income. Borrowers must recertify their income annually to remain on an IDR plan, which can be done through the StudentAid.gov website. Failure to recertify can result in a switch to a standard repayment plan, potentially disqualifying the borrower from forgiveness.

A practical tip for maximizing eligibility is to strategically time income-driven payments. For instance, if a borrower anticipates a significant income increase, they might recertify their income earlier in the year to lock in lower payments for the remaining months. Conversely, borrowers nearing the end of their repayment term might delay recertification to ensure their income remains low enough to qualify for forgiveness. Additionally, married borrowers should consider filing taxes separately to exclude their spouse’s income from the AGI calculation, though this may reduce eligibility for certain tax credits.

In conclusion, eligibility for student loan forgiveness is a dynamic interplay of income, employment, and repayment plan choices. Borrowers must proactively manage their AGI, verify employer eligibility, and select the most advantageous repayment plan to qualify. Tools like the PSLF Help Tool and annual income recertification are essential for staying on track. By understanding these criteria and leveraging strategic financial planning, borrowers can position themselves to benefit from loan forgiveness programs effectively.

Nebraska's Tax Implications for Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

The PSLF program does not consider income for loan forgiveness eligibility. Instead, it requires 120 qualifying payments while working full-time for a qualifying public service employer.

IDR plan forgiveness uses the income reported on your most recent tax return or through the annual recertification process to determine eligibility for forgiveness after 20–25 years of qualifying payments.

Yes, if you file taxes jointly, your spouse’s income is included in the calculation of your adjusted gross income (AGI), which determines your monthly payment and forgiveness eligibility.

Student loan forgiveness programs, such as IDR plans, typically use your adjusted gross income (AGI) from your federal tax return, which is your gross income minus certain deductions.

Yes, all taxable income, including overtime and bonuses, is included in your AGI, which is used to calculate your monthly payments under IDR plans and determine forgiveness eligibility.