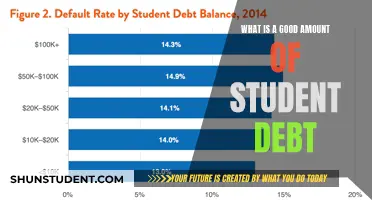

Determining a good amount of student loans is a complex and highly individualized decision that depends on various factors, including the cost of tuition, living expenses, potential income after graduation, and personal financial goals. While some argue that any amount of debt is undesirable, others view student loans as an investment in one's future earning potential. It's essential to consider the long-term implications of taking on student debt, such as the impact on credit scores, loan repayment terms, and the potential for loan forgiveness or refinancing. Ultimately, the ideal amount of student loans will vary significantly from person to person, and it's crucial to carefully weigh the benefits and risks before committing to any level of borrowing.

Explore related products

What You'll Learn

![]()

Understanding loan limits

Federal student loan limits vary based on your year in school, dependency status, and the type of loan you're applying for. For instance, if you're an undergraduate student, you can borrow up to $5,500 in subsidized loans and $20,500 in unsubsidized loans for your first year. These limits increase for each subsequent year of study. Graduate and professional students have higher loan limits, with the maximum amount depending on their specific program and financial need. Understanding these limits is crucial to avoid overborrowing and to ensure you're making informed decisions about your educational financing.

It's also important to note that private student loans have their own set of limits and terms, which can vary significantly from one lender to another. Some private lenders may offer loans that cover up to the full cost of attendance, while others may have lower maximum loan amounts. When considering private loans, it's essential to shop around and compare offers from different lenders to find the best terms and interest rates.

In addition to understanding the numerical limits of student loans, it's equally important to consider the long-term implications of borrowing. Student loan debt can have a significant impact on your financial future, affecting everything from your credit score to your ability to purchase a home or start a business. Before taking out any loans, it's crucial to have a clear understanding of your repayment options and the potential consequences of defaulting on your loans.

One strategy for managing student loan debt is to borrow only what you absolutely need. This may involve creating a detailed budget for your educational expenses and exploring other sources of funding, such as scholarships, grants, and work-study programs. By minimizing the amount you borrow, you can reduce the financial burden of repayment and increase your chances of achieving long-term financial stability.

Another important consideration when it comes to student loans is the interest rate. Federal student loans typically have fixed interest rates, which means the rate you receive when you take out the loan will remain the same throughout the repayment period. Private student loans, on the other hand, may have variable interest rates, which can fluctuate based on market conditions. Understanding the difference between fixed and variable interest rates can help you make more informed decisions about which type of loan is right for you.

In conclusion, understanding loan limits is a critical component of managing student loan debt. By familiarizing yourself with the specific limits and terms of both federal and private student loans, you can make more informed decisions about your educational financing and set yourself up for long-term financial success.

Exploring Good Citizenship: A Student's Perspective

You may want to see also

Explore related products

![]()

Assessing repayment capacity

To assess repayment capacity, start by calculating your debt-to-income ratio. This is done by dividing your total monthly debt payments by your gross monthly income. Ideally, your debt-to-income ratio should be below 36% to ensure you have enough income to cover your loan repayments comfortably. Next, consider your credit score, as it can impact your ability to secure favorable loan terms. A higher credit score may qualify you for lower interest rates, reducing the overall cost of your student loans.

Evaluate your employment prospects and job stability. Lenders often look at your employment history and current job situation to gauge your ability to repay loans. If you have a stable job with a steady income, you're in a better position to manage your loan repayments. Conversely, if you're in a field with uncertain job prospects or are currently unemployed, you may need to be more cautious about taking on additional debt.

Create a detailed budget to understand your monthly expenses and how much you can realistically allocate towards loan repayments. Consider using the 50/30/20 budgeting rule, where 50% of your income goes towards necessary expenses, 30% towards discretionary spending, and 20% towards savings and debt repayment. This can help you prioritize your financial obligations and ensure you're not overextending yourself.

Finally, research and compare different repayment plans. There are various options available, such as income-driven repayment plans, which adjust your monthly payments based on your income and family size. Understanding the different repayment plans can help you choose the one that best fits your financial situation and minimizes the strain on your budget.

Crafting the Perfect Student Recommendation: A Comprehensive Guide

You may want to see also

Explore related products

$20.99 $25.99

$24.55 $30.99

![]()

Evaluating interest rates

Understanding the interest rates associated with student loans is crucial in determining what constitutes a 'good' amount of debt. Interest rates can significantly impact the total cost of your loan over time. For instance, a 1% difference in interest rates can result in thousands of dollars more paid over the life of the loan. Therefore, it's essential to evaluate interest rates carefully before taking on student debt.

One approach to evaluating interest rates is to compare them to the expected return on investment (ROI) of your education. If the interest rate on your loan is lower than the potential ROI of your degree, it may be considered a worthwhile investment. However, if the interest rate is higher, it could indicate that you're paying more for your education than it's likely to yield in the long run.

Another factor to consider is the type of interest rate: fixed or variable. Fixed interest rates remain the same throughout the life of the loan, providing predictability in your monthly payments. Variable interest rates, on the other hand, can fluctuate based on market conditions, which can lead to changes in your payment amounts. When evaluating interest rates, it's important to consider your personal financial situation and risk tolerance to determine which type of rate is more suitable for you.

Additionally, it's crucial to consider any fees associated with the loan, as these can also impact the overall cost. Origination fees, late payment fees, and prepayment penalties are all factors that should be taken into account when evaluating the true cost of borrowing.

In conclusion, evaluating interest rates is a critical step in determining a good amount of student loans to have. By comparing interest rates to the expected ROI of your education, considering the type of rate, and factoring in associated fees, you can make a more informed decision about how much student debt is manageable for you.

Exemplifying Integrity: The Essence of Being a Good Student

You may want to see also

Explore related products

![]()

Exploring forgiveness programs

Navigating the complex landscape of student loans can be daunting, but exploring forgiveness programs offers a potential lifeline for many borrowers. These programs, designed to alleviate the burden of educational debt, come in various forms and cater to different professional and financial circumstances. Understanding the intricacies of these programs is crucial for anyone seeking to manage their student loans effectively.

One prominent forgiveness program is the Public Service Loan Forgiveness (PSLF) program, which targets individuals working in public service roles. To qualify, borrowers must make 120 qualifying monthly payments while employed full-time by a government or non-profit organization. This program can forgive the remaining balance of Direct Loans after meeting these criteria. However, it's essential to note that not all loans are eligible, and borrowers must carefully review the program's requirements to ensure they qualify.

Another option is the Teacher Loan Forgiveness program, which aims to support educators working in low-income schools. This program offers forgiveness of up to $17,500 for Direct Loans and Federal Stafford Loans after five consecutive years of teaching. To qualify, teachers must meet specific criteria, including teaching in a school that serves students from low-income families and holding a valid teaching certificate.

For those in the medical field, the National Health Service Corps (NHSC) Loan Repayment Program provides an opportunity to have up to $50,000 of student loans forgiven. This program requires a two-year commitment to work in a health center or clinic that serves underserved communities. Borrowers must be licensed primary medical care providers to qualify.

When exploring forgiveness programs, it's crucial to consider the fine print. Each program has its own set of eligibility requirements, application processes, and potential tax implications. Borrowers should consult with a financial advisor or student loan expert to determine the best approach for their individual situation. Additionally, staying informed about changes to these programs is essential, as policy shifts can impact eligibility and benefits.

In conclusion, forgiveness programs offer a valuable avenue for managing student loan debt, but they require careful consideration and planning. By understanding the specific requirements and benefits of each program, borrowers can make informed decisions and potentially alleviate a significant portion of their educational debt.

Exploring the Qualities of an Exemplary Student: A Comprehensive Guide

You may want to see also

Explore related products

![]()

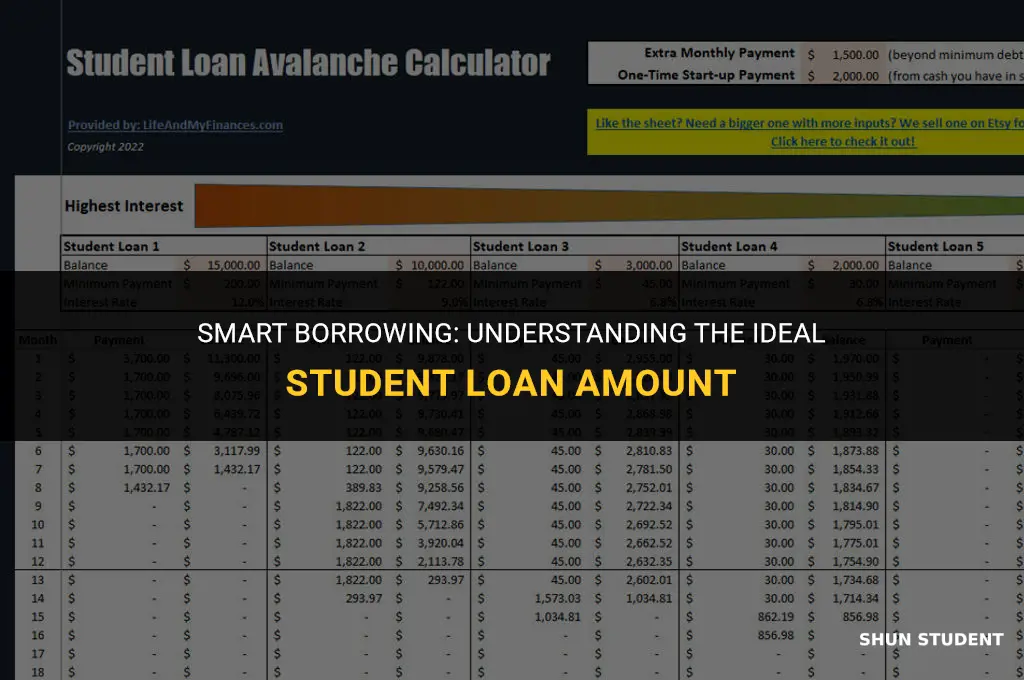

Managing loan repayment strategies

One effective strategy for managing student loan repayment is to prioritize high-interest loans first. This approach, known as the avalanche method, involves making minimum payments on all loans while directing any extra funds towards the loan with the highest interest rate. By tackling the most expensive debt first, borrowers can reduce the overall cost of their loans and pay off their balances more quickly.

Another strategy to consider is the snowball method, which focuses on paying off the smallest loan balance first. This approach can provide a psychological boost as borrowers experience the satisfaction of eliminating an entire loan. As each loan is paid off, the borrower can then apply the funds that were previously going towards that loan to the next smallest balance, gradually working their way up to the larger loans.

For those struggling to make their monthly payments, income-driven repayment plans can be a valuable option. These plans adjust the monthly payment amount based on the borrower's income and family size, potentially reducing the monthly burden. However, it's important to note that these plans may extend the repayment period and result in more interest paid over the life of the loan.

Refinancing student loans can also be a viable strategy for managing repayment. By refinancing, borrowers may be able to secure a lower interest rate or a longer repayment term, which can help reduce monthly payments. However, refinancing federal student loans can result in the loss of certain benefits, such as income-driven repayment options and loan forgiveness programs, so it's crucial to weigh the pros and cons carefully.

Lastly, borrowers should be aware of the importance of maintaining a good credit score while managing their student loan repayment. A strong credit score can open up opportunities for refinancing at better rates or qualifying for other financial products. To maintain a good credit score, borrowers should make their loan payments on time, keep their credit utilization low, and monitor their credit reports for any errors.

Active Listening: The Key to Academic Success in Class

You may want to see also

Frequently asked questions

A good amount of student loans depends on various factors such as your income, career prospects, and personal financial goals. Generally, it's advisable to keep your total student loan debt below your expected starting salary after graduation.

To determine if you're taking on too much student loan debt, calculate your debt-to-income ratio. This ratio should ideally be below 36%. You can also use online student loan calculators to estimate your monthly payments and ensure they fit within your budget.

Having a high amount of student loans can impact your long-term financial stability. It may delay major life milestones such as buying a home, starting a family, or saving for retirement. High student loan debt can also affect your credit score and limit your ability to take on additional debt in the future.

Yes, there are several strategies to manage and pay off student loans effectively. These include making consistent on-time payments, considering loan consolidation or refinancing, utilizing income-driven repayment plans, and exploring loan forgiveness programs if you qualify. Additionally, creating a budget and prioritizing your loan payments can help you pay off your debt faster.