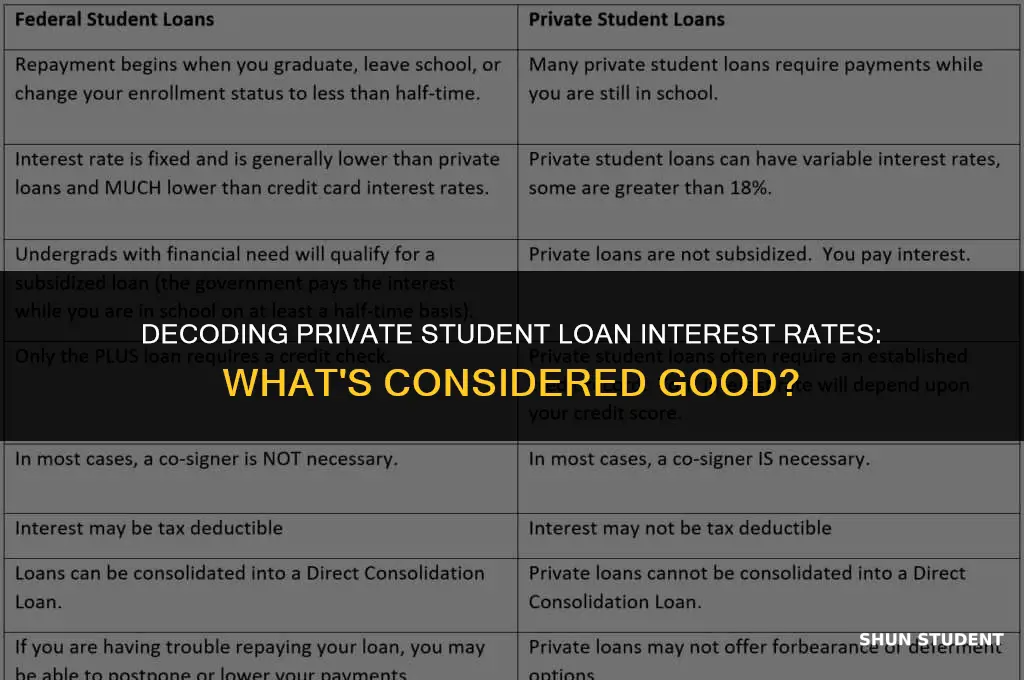

When considering private student loans, one of the most critical factors to evaluate is the interest rate. A good interest rate can significantly impact the overall cost of the loan and the borrower's ability to repay it. In general, a lower interest rate is preferable, as it reduces the amount of money paid over the life of the loan. However, interest rates for private student loans can vary widely depending on the lender, the borrower's creditworthiness, and the current market conditions. As of June 2024, interest rates for private student loans typically range from around 5% to 15% or more. Borrowers with excellent credit scores and a strong financial history may qualify for lower rates, while those with less-than-stellar credit may face higher rates. It's essential to shop around and compare rates from different lenders to find the best option for your individual circumstances. Additionally, consider other factors such as repayment terms, fees, and borrower protections when choosing a private student loan.

Explore related products

$15.99 $20

What You'll Learn

- Understanding Interest Rates: Learn about fixed vs. variable rates and how they impact loan repayment

- Current Market Rates: Research the latest interest rates offered by top private student loan lenders

- Factors Affecting Rates: Discover how credit score, income, and cosigner status influence interest rates

- Comparing Loan Options: Evaluate different lenders and loan terms to find the best interest rate for your needs

- Strategies for Lower Rates: Explore tips and strategies to secure a lower interest rate on private student loans

![]()

Understanding Interest Rates: Learn about fixed vs. variable rates and how they impact loan repayment

Understanding interest rates is crucial when navigating the landscape of private student loans. Fixed interest rates remain constant throughout the loan term, providing predictability in repayment amounts. This stability can be beneficial for budgeting purposes, as borrowers know exactly how much they'll owe each month. On the other hand, variable interest rates fluctuate based on market conditions, which can lead to changes in monthly payments. While variable rates may start lower than fixed rates, they carry the risk of increasing over time, potentially making repayment more challenging.

When considering private student loans, it's essential to weigh the pros and cons of each interest rate type. Fixed rates offer peace of mind, but they may not be the most cost-effective option if market rates decrease. Variable rates, while initially appealing due to lower starting rates, can become more expensive if interest rates rise. Borrowers should assess their financial situation, risk tolerance, and repayment strategy to determine which type of interest rate aligns best with their needs.

To illustrate the impact of interest rates on loan repayment, let's consider an example. Suppose a student takes out a $20,000 private loan with a 5% fixed interest rate and a 10-year repayment term. Their monthly payment would be approximately $227. In contrast, if they opt for a variable interest rate that starts at 3% but increases to 6% over the loan term, their initial monthly payment would be around $183, but it could rise to $248 as the rate adjusts. This demonstrates how interest rate choices can significantly affect the total cost of borrowing and the borrower's financial burden over time.

In conclusion, understanding the nuances of fixed and variable interest rates is vital for making informed decisions about private student loans. Borrowers should carefully evaluate their financial circumstances and future expectations to choose the interest rate type that best suits their repayment goals and risk appetite. By doing so, they can better manage their loan obligations and achieve financial stability.

Finding the Right Speaking Pace for ESL Students: A Guide

You may want to see also

Explore related products

$10.45 $22.95

$14.45 $27.5

![]()

Current Market Rates: Research the latest interest rates offered by top private student loan lenders

As of June 2024, the private student loan market is highly competitive, with lenders offering a range of interest rates to attract borrowers. To determine a good interest rate for private student loans, it's essential to research the latest offerings from top lenders. This can be done by visiting lender websites, comparing rates on financial aggregator platforms, or consulting with financial advisors.

Currently, the best private student loan lenders are offering fixed interest rates as low as 3.99% APR and variable rates starting at 1.99% APR. These rates are subject to change and may vary based on the borrower's creditworthiness, loan term, and other factors. It's important to note that these are the lowest rates available and may not be representative of the rates offered to all borrowers.

When evaluating interest rates, borrowers should consider the overall cost of the loan, including any fees or penalties. They should also compare the rates offered by different lenders to find the best deal for their specific needs. Additionally, borrowers should be aware of the potential risks associated with variable interest rates, which can fluctuate over time and increase the cost of the loan.

To secure the best interest rate, borrowers should have a strong credit history and a stable income. They may also benefit from having a cosigner with good credit. Furthermore, borrowers should be prepared to provide documentation of their income and credit history when applying for a loan.

In conclusion, a good interest rate for private student loans is one that is competitive with the current market rates and aligns with the borrower's financial goals and circumstances. By researching the latest offerings from top lenders and considering the overall cost of the loan, borrowers can make informed decisions and secure the best possible rate for their needs.

Exploring the Qualities of an Exemplary Student: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Factors Affecting Rates: Discover how credit score, income, and cosigner status influence interest rates

Credit score plays a pivotal role in determining the interest rate for private student loans. Lenders use credit scores to assess the borrower's creditworthiness and predict the likelihood of repayment. A higher credit score typically results in a lower interest rate, as it indicates a lower risk for the lender. For instance, a borrower with a credit score of 750 or above may qualify for interest rates as low as 3.5%, while someone with a score below 600 might face rates exceeding 10%.

Income is another critical factor influencing interest rates. Lenders consider the borrower's income to ensure they have the financial capacity to repay the loan. A higher income can lead to a lower interest rate, as it demonstrates the borrower's ability to manage their debt obligations. For example, a borrower earning $50,000 per year may be offered a rate of 4.5%, whereas someone earning $20,000 might receive a rate of 7% or higher.

Cosigner status can also significantly impact interest rates. A cosigner with a strong credit score and stable income can help a borrower qualify for a lower rate, especially if the primary borrower has a limited credit history or lower income. This is because the cosigner's financial strength provides additional security for the lender. In some cases, having a cosigner can reduce the interest rate by as much as 2-3 percentage points.

It's essential for borrowers to understand these factors and take steps to improve their credit score and income before applying for a private student loan. Additionally, finding a cosigner with a strong financial profile can be a strategic move to secure a more favorable interest rate. By doing so, borrowers can potentially save thousands of dollars in interest over the life of their loan.

Decoding Academic Excellence: What Does 'Student in Good Standing' Mean?

You may want to see also

Explore related products

![]()

Comparing Loan Options: Evaluate different lenders and loan terms to find the best interest rate for your needs

To find the best interest rate for private student loans, it's crucial to compare loan options from different lenders. Start by researching various lenders, including banks, credit unions, and online lenders. Each type of lender may offer different interest rates and loan terms. For instance, credit unions often provide more competitive rates due to their non-profit nature, while online lenders might offer more flexible repayment terms.

Once you have a list of potential lenders, evaluate their loan terms. Look for information on fixed versus variable interest rates, repayment periods, and any fees associated with the loan. Fixed interest rates remain the same throughout the loan term, providing predictability in your monthly payments. Variable interest rates, on the other hand, can fluctuate based on market conditions, which might result in changes to your payment amounts.

Consider using online comparison tools to facilitate the evaluation process. These tools allow you to input your loan details and receive a side-by-side comparison of different loan options. This can help you visualize the differences in interest rates and terms more clearly.

Additionally, pay attention to any special offers or discounts that lenders may provide. Some lenders offer interest rate reductions for borrowers who set up automatic payments or have a co-signer with a strong credit history. These discounts can significantly impact the overall cost of your loan.

Finally, before making a decision, read reviews and check the lender's reputation. Look for feedback from current or past borrowers to get an idea of their experiences with the lender. This can provide valuable insights into the lender's customer service and overall reliability.

By thoroughly comparing loan options and evaluating different lenders and loan terms, you can find the best interest rate for your private student loan needs. This process requires time and effort, but it can save you money and ensure that you're making an informed decision about your financial future.

Best Credit Cards for Students: Building Credit and Managing Finances

You may want to see also

Explore related products

![]()

Strategies for Lower Rates: Explore tips and strategies to secure a lower interest rate on private student loans

To secure a lower interest rate on private student loans, it's essential to understand the factors that lenders consider when determining your rate. Credit score plays a significant role, as lenders typically offer lower rates to borrowers with a strong credit history. If your credit score is less than ideal, consider applying with a cosigner who has a higher score. This can significantly improve your chances of securing a lower rate. Additionally, some lenders offer discounts for setting up automatic payments or for having a specific type of bank account with them. Be sure to inquire about these potential discounts when applying.

Another strategy is to shop around and compare rates from multiple lenders. This allows you to find the best offer for your specific situation. Online marketplaces can be a great resource for comparing rates and terms from various lenders. When comparing, look not only at the interest rate but also at the loan terms, fees, and any additional benefits offered.

If you're currently in school, you may be able to take advantage of in-school interest rate reductions. Some private lenders offer lower rates to students who are enrolled in school, as they recognize that students may not have a steady income yet. Additionally, some lenders offer a grace period after graduation, during which you can defer payments without accruing interest. This can be a valuable feature if you're unsure about your immediate post-graduation financial situation.

Finally, consider the loan amount you're borrowing. Lenders may offer lower rates for smaller loan amounts, as these are typically seen as less risky. If possible, try to borrow only what you need to cover your educational expenses. This not only increases your chances of securing a lower rate but also helps you avoid unnecessary debt.

By understanding these strategies and taking the time to research and compare your options, you can increase your chances of securing a lower interest rate on your private student loan. This can save you money over the life of the loan and help you achieve your financial goals more quickly.

Nourishing Minds: Wholesome Food Ideas for Students

You may want to see also

Frequently asked questions

Several factors can influence the interest rate on a private student loan, including your credit score, income, debt-to-income ratio, and the lender's policies. Borrowers with higher credit scores and lower debt-to-income ratios typically qualify for lower interest rates.

A fixed interest rate remains the same throughout the life of the loan, providing predictable monthly payments. In contrast, a variable interest rate can fluctuate based on market conditions, potentially leading to changes in your monthly payment amount.

As of 2024, a good interest rate for a private student loan is generally considered to be around 5% to 7% APR for fixed rates and 4% to 6% APR for variable rates. However, the best rate for you will depend on your individual financial situation and creditworthiness.