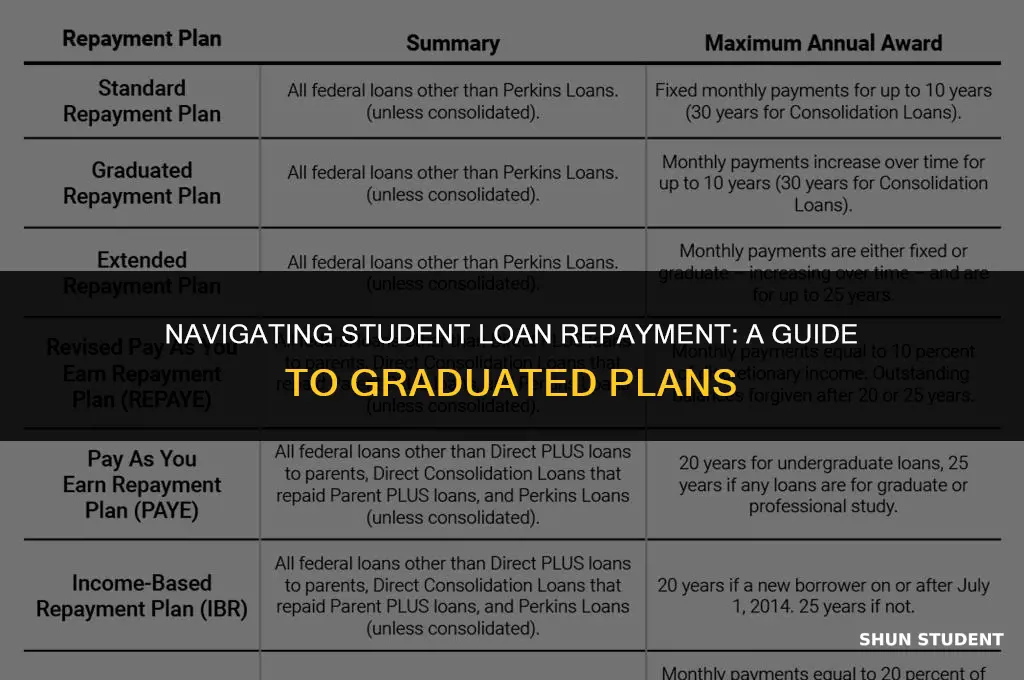

A graduated repayment plan for student loans is a repayment strategy designed to help borrowers manage their loan payments more effectively over time. This plan typically starts with lower monthly payments that gradually increase every two years, aligning with the assumption that the borrower's income will rise as they advance in their career. The graduated repayment plan can be particularly beneficial for individuals who expect to see a steady increase in their earnings and want to avoid the burden of high initial loan payments. By structuring repayments in this way, borrowers can better align their loan obligations with their financial capabilities, potentially reducing the risk of default and improving their overall financial health.

| Characteristics | Values |

|---|---|

| Definition | A graduated repayment plan is a type of repayment plan for student loans that allows borrowers to make lower payments initially, with payments increasing over time. |

| Payment Structure | Payments start low and increase gradually, typically every two years. |

| Interest Rates | Interest rates are typically fixed, but may vary depending on the lender. |

| Repayment Term | The repayment term is usually longer than with other repayment plans, often 20-30 years. |

| Eligibility | Borrowers must meet certain eligibility criteria, such as having a steady income and a good credit score. |

| Benefits | Graduated repayment plans can help borrowers who expect their income to increase over time, as they can make lower payments initially and then increase their payments as their income grows. |

| Drawbacks | Graduated repayment plans can result in higher total interest paid over the life of the loan, as the payments are lower initially but increase over time. |

Explore related products

What You'll Learn

- Definition: A graduated repayment plan is an option for student loans that allows borrowers to make lower payments initially

- Eligibility: Borrowers with federal student loans, such as Direct Loans or FFEL Loans, may qualify for graduated repayment

- Payment Structure: Payments start low and increase every two years, typically over a 10-year repayment period

- Interest Accrual: Interest continues to accrue on the unpaid balance, potentially increasing the total cost of the loan

- Application Process: Borrowers must apply for graduated repayment through their loan servicer, providing income verification and other required documents

![]()

Definition: A graduated repayment plan is an option for student loans that allows borrowers to make lower payments initially

A graduated repayment plan for student loans is a strategic financial approach designed to ease the burden of loan repayment for recent graduates. This plan acknowledges the reality that many new graduates may not have the financial stability to make substantial loan payments immediately after completing their education. By allowing borrowers to make lower payments initially, the graduated repayment plan provides a more manageable transition into the workforce.

The key feature of a graduated repayment plan is the structured increase in monthly payments over time. Typically, payments start at a lower amount and gradually rise every two years, aligning with the assumption that the borrower's income will increase as they gain more work experience. This incremental approach helps borrowers avoid defaulting on their loans during the early stages of their careers when their earning potential is still developing.

To qualify for a graduated repayment plan, borrowers usually need to demonstrate financial need and meet specific eligibility criteria set by the lender or loan servicer. These criteria may include factors such as income level, debt-to-income ratio, and credit history. Once approved, the borrower enters into a repayment schedule that outlines the payment amounts and due dates over the life of the loan.

One of the primary benefits of a graduated repayment plan is the reduced financial strain it places on borrowers in the initial years of repayment. This can be particularly advantageous for those entering fields with lower starting salaries or those who have multiple loans to manage. Additionally, by making timely payments under this plan, borrowers can build a positive credit history, which can be beneficial for future financial endeavors.

However, it is important for borrowers to carefully consider the long-term implications of a graduated repayment plan. While the lower initial payments can be attractive, they may result in paying more interest over the life of the loan compared to a standard repayment plan. Borrowers should also be aware that if they do not meet the eligibility criteria or fail to make payments as scheduled, they may face penalties or be required to switch to a different repayment plan.

In conclusion, a graduated repayment plan can be a valuable tool for managing student loan debt, especially for recent graduates who are just starting their careers. By understanding the specifics of this repayment option and its potential benefits and drawbacks, borrowers can make informed decisions about their financial future.

Understanding Graduate Student Stipends: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Eligibility: Borrowers with federal student loans, such as Direct Loans or FFEL Loans, may qualify for graduated repayment

Eligibility for a graduated repayment plan is contingent upon the type of student loan a borrower has. Specifically, borrowers with federal student loans, such as Direct Loans or Federal Family Education Loans (FFEL), may qualify for this repayment option. This plan is designed to accommodate borrowers who expect their income to increase over time, allowing them to start with lower payments that gradually increase every two years.

To qualify for a graduated repayment plan, borrowers must meet certain criteria. For instance, they must have a high enough income to cover their monthly expenses and still have some disposable income left over. Additionally, they must demonstrate a good credit history and have a stable employment record. The lender will also consider the borrower's debt-to-income ratio, which is the percentage of their monthly income that goes towards paying off debts.

The application process for a graduated repayment plan typically involves submitting a formal request to the lender, along with supporting documentation such as proof of income, employment, and credit history. Borrowers may also need to provide information about their educational background and the loans they wish to include in the repayment plan. Once approved, the borrower will be required to make regular payments according to the agreed-upon schedule.

One of the key benefits of a graduated repayment plan is that it allows borrowers to manage their finances more effectively. By starting with lower payments, they can allocate more funds towards other essential expenses, such as rent, utilities, and groceries. As their income increases, they can gradually increase their loan payments without feeling overwhelmed. This plan also helps borrowers avoid defaulting on their loans, which can have serious consequences for their credit score and financial future.

However, it's important to note that a graduated repayment plan may not be suitable for all borrowers. Those who do not expect their income to increase significantly over time may find it difficult to keep up with the rising payments. Additionally, borrowers who have a high amount of debt or a poor credit history may not qualify for this repayment option. It's essential for borrowers to carefully consider their financial situation and long-term goals before deciding whether a graduated repayment plan is right for them.

Exploring the Life and Times of a Graduate Student

You may want to see also

Explore related products

![]()

Payment Structure: Payments start low and increase every two years, typically over a 10-year repayment period

Under a graduated repayment plan, your initial payments are lower and gradually increase over time. This structure is designed to align with the typical career progression of recent graduates, who may start with lower salaries that increase as they gain experience. The payments rise every two years, which helps manage the financial burden as your income grows.

The total repayment period for a graduated plan is usually 10 years, which is longer than the standard repayment term for federal student loans. This extended timeline allows for smaller monthly payments initially, providing immediate financial relief. However, it also means you'll pay more in interest over the life of the loan compared to a shorter repayment term.

To qualify for a graduated repayment plan, you typically need to demonstrate financial need and have a stable income. Lenders will review your current earnings and employment history to ensure you're likely to benefit from the graduated structure. If approved, you'll start with payments that are lower than those required under a standard plan, with the understanding that they will increase biennially.

One advantage of a graduated repayment plan is that it can help you manage your cash flow more effectively in the early years of your career. This can be particularly beneficial if you're working in a field where salaries are initially low but increase rapidly with experience. Additionally, the predictability of the payment increases allows you to budget and plan your finances more accurately over the long term.

However, it's important to consider the long-term implications of a graduated repayment plan. While the lower initial payments can be attractive, the increasing payments every two years may become a financial strain if your income doesn't rise as expected. Furthermore, the extended repayment term means you'll be in debt for a longer period, which can impact your ability to achieve other financial goals, such as buying a home or saving for retirement.

In summary, a graduated repayment plan can be a valuable tool for managing student loan debt, particularly for those in fields with lower starting salaries and high growth potential. By understanding the structure and implications of this repayment option, you can make an informed decision about whether it's the right choice for your financial situation.

Exploring the Key Differences: Graduate vs Undergraduate Studies

You may want to see also

Explore related products

![]()

Interest Accrual: Interest continues to accrue on the unpaid balance, potentially increasing the total cost of the loan

Interest accrual is a critical aspect of student loans that can significantly impact the total cost of borrowing. When a borrower fails to make timely payments on their student loan, interest continues to accumulate on the unpaid balance. This can lead to a snowball effect, where the amount owed grows larger over time, making it increasingly difficult for the borrower to repay the loan in full.

For example, let's consider a borrower who takes out a $30,000 student loan with a fixed interest rate of 6%. If the borrower makes no payments for two years, the interest accrued would be approximately $3,600, bringing the total balance to $33,600. This increase in the loan balance not only makes it more challenging for the borrower to repay the loan but also extends the repayment period, potentially leading to additional interest accrual.

One of the key benefits of a graduated repayment plan is that it can help borrowers manage interest accrual more effectively. By starting with lower payments that gradually increase over time, borrowers can reduce the amount of interest that accumulates on their unpaid balance. This can result in significant savings over the life of the loan and help borrowers repay their debt more quickly.

However, it's essential for borrowers to understand that interest accrual can still occur even with a graduated repayment plan. If a borrower's payments are not sufficient to cover the accruing interest, the loan balance may continue to grow. Therefore, it's crucial for borrowers to make timely payments and consider making additional payments whenever possible to minimize interest accrual.

In conclusion, interest accrual can have a significant impact on the total cost of a student loan. Borrowers should be aware of this potential issue and take steps to manage it effectively, such as enrolling in a graduated repayment plan and making timely payments. By doing so, borrowers can reduce the amount of interest that accumulates on their unpaid balance and repay their loan more quickly and efficiently.

Unlocking Opportunities: The Graduate Student Tuition Waiver Explained

You may want to see also

Explore related products

![]()

Application Process: Borrowers must apply for graduated repayment through their loan servicer, providing income verification and other required documents

To initiate the application process for a graduated repayment plan, borrowers must reach out to their loan servicer. This is the entity responsible for managing the loan and ensuring payments are processed correctly. Borrowers can typically find their loan servicer's contact information on their monthly billing statement or by logging into their online account.

Once contact is made, the loan servicer will provide the necessary forms and documentation required to apply for a graduated repayment plan. This usually includes income verification documents, such as pay stubs or tax returns, as well as other supporting materials like proof of employment or enrollment in a degree program. Borrowers should be prepared to provide detailed information about their financial situation, including their income, expenses, and any other debts they may have.

The application process can vary depending on the loan servicer and the specific requirements of the graduated repayment plan. Some servicers may allow borrowers to apply online, while others may require a paper application. Borrowers should carefully review the instructions provided by their loan servicer to ensure they submit all required documents and information accurately and on time.

After submitting the application, borrowers should expect a response from their loan servicer within a few weeks. If approved, the servicer will provide details on the new repayment plan, including the monthly payment amount and the expected payoff date. Borrowers should carefully review these details to ensure they understand the terms of the new plan and how it will impact their finances.

It's important to note that not all borrowers may be eligible for a graduated repayment plan. Eligibility criteria can vary depending on the loan servicer and the specific plan being offered. Borrowers should consult with their loan servicer to determine if they meet the necessary criteria and to discuss any other repayment options that may be available.

Exploring the Life and Opportunities of a UK Graduate Student

You may want to see also

Frequently asked questions

A graduated repayment plan is a type of repayment plan for student loans that starts with lower monthly payments and gradually increases them over time. This plan is designed to help borrowers who expect their income to increase in the future.

With a graduated repayment plan, the monthly payments are lower at the beginning and increase every two years. The plan is based on the borrower's current income and the expected increase in income over time. The goal is to make the loan payments more manageable in the early years of repayment when the borrower's income is lower.

To be eligible for a graduated repayment plan, the borrower must have a Direct Loan or a Federal Family Education Loan (FFEL). Additionally, the borrower must not have an income that is more than 1.5 times the poverty guideline for their family size.

The main benefit of a graduated repayment plan is that it allows borrowers to make lower monthly payments in the early years of repayment when their income is lower. This can help borrowers avoid defaulting on their loans and make it easier to manage their finances.

One drawback of a graduated repayment plan is that the total amount of interest paid over the life of the loan may be higher than with other repayment plans. Additionally, if the borrower's income does not increase as expected, they may struggle to make the higher monthly payments in the later years of repayment.