A PLUS loan for graduate students is a type of federal student loan offered in the United States. It is designed to help cover the costs of graduate education, including tuition, fees, room, and board. Unlike undergraduate PLUS loans, which are taken out by parents on behalf of their dependent students, graduate PLUS loans are taken out directly by the graduate student. To be eligible for a graduate PLUS loan, students must be enrolled at least half-time in a graduate program and meet certain credit requirements. The loan offers a fixed interest rate and flexible repayment options, making it a valuable resource for students pursuing advanced degrees.

| Characteristics | Values |

|---|---|

| Loan Type | Federal student loan |

| Borrower | Graduate students |

| Loan Limits | Higher limits compared to undergraduate loans |

| Interest Rates | Fixed interest rates, typically higher than undergraduate loans |

| Repayment Terms | Longer repayment terms, often up to 30 years |

| Grace Period | 6-month grace period after graduation |

| Credit Check | No credit check required |

| Collateral | No collateral required |

| Loan Fees | Origination fees apply |

| Loan Forgiveness | Eligible for Public Service Loan Forgiveness (PSLF) |

| Loan Consolidation | Can be consolidated with other federal student loans |

| Loan Servicer | Serviced by federal loan servicers |

| Loan Application | Apply through the Free Application for Federal Student Aid (FAFSA) |

| Loan Disbursement | Funds disbursed directly to the school |

| Loan Repayment | Borrower responsible for repaying the loan, not the school |

| Loan Default | Default occurs if payments are not made according to the repayment plan |

| Loan Rehabilitation | Options available to rehabilitate a defaulted loan |

Explore related products

What You'll Learn

- Eligibility Criteria: Requirements for graduate students to qualify for a PLUS loan, including credit history and enrollment status

- Application Process: Steps to apply for a PLUS loan, such as completing the FAFSA and obtaining an endorser if necessary

- Interest Rates and Fees: Current interest rates, origination fees, and any additional costs associated with PLUS loans for graduate students

- Repayment Options: Various repayment plans available, including deferment and forbearance options, and how they impact loan management

- Loan Limits: Maximum amount a graduate student can borrow through PLUS loans, considering other financial aid received

![]()

Eligibility Criteria: Requirements for graduate students to qualify for a PLUS loan, including credit history and enrollment status

To qualify for a PLUS loan as a graduate student, you must meet specific eligibility criteria set by the U.S. Department of Education. One of the primary requirements is that you must be enrolled at least half-time in a graduate or professional program. This ensures that you are actively pursuing your advanced degree and that the loan funds will be used for educational purposes.

In addition to enrollment status, your credit history plays a crucial role in determining your eligibility for a PLUS loan. Unlike undergraduate students, graduate students are required to have a creditworthy history to qualify for this type of loan. This means that you must have a positive credit record with no adverse credit history, such as bankruptcies, foreclosures, or accounts in default. If you have a limited credit history, you may still be eligible if you can demonstrate other indicators of creditworthiness.

Furthermore, you must be a U.S. citizen or a permanent resident to apply for a PLUS loan. International students, even if they are studying in the United States, are not eligible for this type of federal loan. Additionally, you must not have reached the maximum borrowing limit for PLUS loans, which is determined by your cost of attendance and other financial aid you have received.

It's important to note that the eligibility criteria for a PLUS loan can vary slightly depending on the specific program and institution you are attending. Some schools may have additional requirements or restrictions, so it's essential to check with your financial aid office for the most up-to-date information. By understanding and meeting these eligibility criteria, you can increase your chances of securing a PLUS loan to help fund your graduate education.

Exploring Berkeley Housing: What It Means to Be a Partnered Graduate Student

You may want to see also

Explore related products

![]()

Application Process: Steps to apply for a PLUS loan, such as completing the FAFSA and obtaining an endorser if necessary

To apply for a PLUS loan as a graduate student, you must first complete the Free Application for Federal Student Aid (FAFSA). This form is used to determine your eligibility for federal student aid, including the PLUS loan. You can submit the FAFSA online at the Federal Student Aid website. Be sure to include your graduate school's code on the form to ensure that your application is sent to the correct institution.

Once you have submitted the FAFSA, your graduate school will review your application and determine your eligibility for the PLUS loan. If you are eligible, the school will send you an award letter outlining the terms of your loan. If you are not eligible, you may need to obtain an endorser to guarantee the loan. An endorser is someone who agrees to repay the loan if you default. To find an endorser, you can ask a parent, grandparent, or other creditworthy individual.

If you need an endorser, you will need to complete an additional form, the PLUS Loan Endorser Addendum. This form is available on the Federal Student Aid website. Once you have completed the form, you will need to submit it to your graduate school along with the endorser's signature.

After you have submitted all of the required forms, your graduate school will review your application and determine the final terms of your loan. If your loan is approved, the funds will be disbursed directly to your school to cover your tuition and fees. Any remaining funds will be sent to you in the form of a refund.

It is important to note that the PLUS loan has a fixed interest rate and a 10-year repayment term. You will need to make payments on the loan while you are in school, but you may be able to defer payments if you are enrolled in a graduate program. Be sure to review the terms of your loan carefully before accepting the funds.

Unlocking Opportunities: The Graduate Student Tuition Waiver Explained

You may want to see also

Explore related products

$13.29 $17.91

$7.99 $19.99

![]()

Interest Rates and Fees: Current interest rates, origination fees, and any additional costs associated with PLUS loans for graduate students

As of my last update in June 2024, the current interest rate for PLUS loans for graduate students is 7.99%. This rate is fixed for the life of the loan, which means it will not change over time, providing borrowers with predictable monthly payments. However, it's important to note that interest rates can fluctuate based on market conditions and may be different at the time of your application.

In addition to the interest rate, PLUS loans for graduate students also come with an origination fee. This fee is currently 4.99% of the total loan amount. Origination fees are typically deducted from the loan disbursement, reducing the net amount you receive. It's crucial to factor in this fee when calculating the total cost of borrowing.

Beyond the interest rate and origination fee, there are no additional costs associated with PLUS loans for graduate students. There are no prepayment penalties, which means you can pay off your loan early without incurring any extra charges. However, it's essential to be aware of any potential late payment fees or penalties that may apply if you fail to make your monthly payments on time.

When considering a PLUS loan for graduate studies, it's important to carefully review the terms and conditions, including the interest rate, origination fee, and any other potential costs. This will help you make an informed decision about whether a PLUS loan is the right choice for financing your education.

To further illustrate the impact of interest rates and fees on your loan, let's consider an example. Suppose you borrow $20,000 at the current interest rate of 7.99% with an origination fee of 4.99%. Your monthly payment would be approximately $233.33, and over the life of the loan, you would pay a total of $27,999.60, including the origination fee. This example highlights the importance of understanding the true cost of borrowing when taking out a PLUS loan for graduate studies.

Exploring the Path Less Traveled: Non-Matriculated Graduate Studies

You may want to see also

Explore related products

$9.99 $14.99

$9.99

![]()

Repayment Options: Various repayment plans available, including deferment and forbearance options, and how they impact loan management

Graduate students often face significant financial burdens, and managing repayment of loans can be a daunting task. Understanding the various repayment options available, including deferment and forbearance, is crucial for effective loan management. Deferment allows borrowers to temporarily postpone payments, while forbearance permits reduced or paused payments for a specified period. These options can provide much-needed relief, but it's essential to comprehend their implications fully.

Deferment options typically include in-school deferment, where payments are postponed while the borrower is enrolled in school, and post-graduation deferment, which allows for a grace period after completing studies. Forbearance, on the other hand, may be granted due to financial hardship, medical expenses, or other qualifying circumstances. It's important to note that interest may continue to accrue during deferment and forbearance periods, potentially increasing the overall cost of the loan.

To navigate these options effectively, graduate students should familiarize themselves with the specific terms and conditions of their loans. This includes understanding the duration of deferment or forbearance periods, the impact on interest accrual, and any potential fees associated with these options. Additionally, borrowers should consider their long-term financial goals and how these repayment plans align with their overall financial strategy.

In conclusion, repayment options such as deferment and forbearance can be valuable tools for graduate students managing their loan obligations. However, it's crucial to approach these options with a clear understanding of their implications and to integrate them into a comprehensive financial plan. By doing so, borrowers can make informed decisions that support their financial well-being both during and after their graduate studies.

Exploring the Journey of Nontraditional Graduate Students

You may want to see also

Explore related products

$9.99 $18.74

![]()

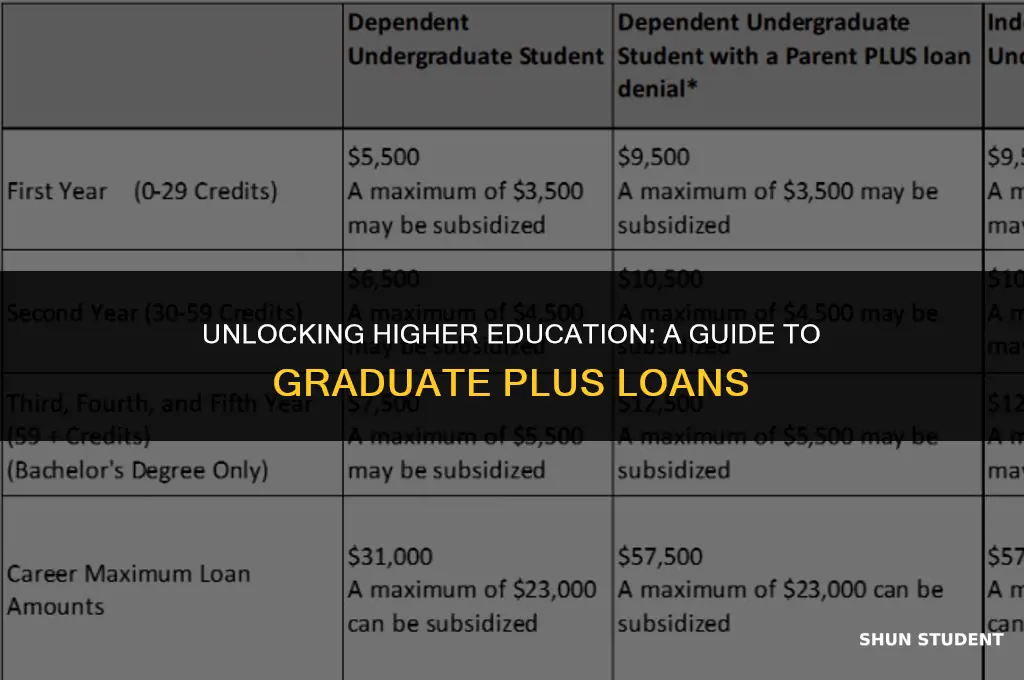

Loan Limits: Maximum amount a graduate student can borrow through PLUS loans, considering other financial aid received

Graduate students seeking financial assistance through PLUS loans must be aware of the loan limits imposed by the federal government. These limits are designed to ensure that students do not take on more debt than they can reasonably manage. The maximum amount a graduate student can borrow through PLUS loans is determined by several factors, including the cost of attendance at their institution and the amount of other financial aid they have received.

To calculate the maximum PLUS loan amount, students must first determine their institution's cost of attendance (COA). This figure typically includes tuition, fees, room and board, books, supplies, and other miscellaneous expenses. Once the COA is established, students must subtract the amount of other financial aid they have received, such as grants, scholarships, and fellowships. The remaining amount is the maximum PLUS loan amount for which they are eligible.

It is important to note that PLUS loans are intended to cover educational expenses only. Students should not borrow more than they need to cover their COA, as this can lead to unnecessary debt and financial strain. Additionally, students should be aware that PLUS loans are subject to interest rates and repayment terms, which can impact their long-term financial health.

In some cases, students may be able to borrow additional funds through private student loans or other sources. However, it is generally advisable to exhaust all federal aid options, including PLUS loans, before turning to private lenders. This is because federal loans often offer more favorable terms and protections for borrowers.

To summarize, graduate students can borrow up to the difference between their institution's COA and the amount of other financial aid they have received through PLUS loans. It is crucial for students to carefully consider their financial needs and the terms of the loan before borrowing to ensure they are making a responsible decision.

Exploring the Path Less Traveled: A Guide for Non-Traditional Graduate Students

You may want to see also

Frequently asked questions

A PLUS Loan is a federal student loan available to graduate students who need additional funding beyond what is offered through other federal loan programs. It is designed to cover the cost of education expenses not covered by other forms of financial aid.

To be eligible for a PLUS Loan, a graduate student must be enrolled at least half-time in a graduate program and meet the general eligibility requirements for federal student aid. Additionally, the student must not have an adverse credit history.

The maximum amount a graduate student can borrow with a PLUS Loan is the cost of attendance minus any other financial aid received. The cost of attendance includes tuition, fees, room and board, and other education-related expenses.

The interest rate for a PLUS Loan is a fixed rate that is set annually by the U.S. Department of Education. Repayment terms typically require the borrower to begin making payments six months after the loan is fully disbursed. The standard repayment plan is 10 years, but other repayment options may be available.