The average student loan graduated interest rate is a critical financial metric that recent graduates and current students must understand. It represents the typical interest rate applied to student loans after graduation, which can significantly impact the total amount repaid over the life of the loan. This rate can vary based on several factors, including the type of loan (federal or private), the borrower's credit score, and the repayment plan chosen. Understanding this rate helps graduates plan their finances effectively and make informed decisions about managing their student debt.

Explore related products

![NMLS Study Guide: SAFE Mortgage Loan Originator Test Prep Secrets Book, Full-Length MLO Practice Exam, Detailed Answer Explanations: [2nd Edition]](https://m.media-amazon.com/images/I/71wuD4SQlSL._AC_UY218_.jpg)

What You'll Learn

- Definition: Explanation of what an average student loan graduated interest rate entails

- Current Rates: Overview of the present interest rates for graduated student loans

- Historical Trends: Analysis of how interest rates have changed over time

- Impact on Borrowers: Discussion of how these rates affect student loan borrowers financially

- Comparison Options: Exploration of different lenders and their offered interest rates

![]()

Definition: Explanation of what an average student loan graduated interest rate entails

The average student loan graduated interest rate refers to the typical interest rate that borrowers pay on their student loans after they have completed their education. This rate is often higher than the interest rate during the in-school period, reflecting the borrower's increased earning potential post-graduation. Lenders calculate this rate based on various factors, including the borrower's credit history, the amount of the loan, and the repayment term.

One key aspect of the average student loan graduated interest rate is that it can vary significantly depending on the type of loan. For instance, federal student loans typically have fixed interest rates, which means the rate remains the same throughout the life of the loan. In contrast, private student loans often have variable interest rates, which can fluctuate based on market conditions. This variability can make it challenging for borrowers to predict their future monthly payments.

Another important consideration is the impact of interest rates on the total cost of borrowing. Even a small difference in interest rates can result in significant savings or additional costs over the repayment period. For example, a 1% difference in interest rates on a $30,000 loan with a 10-year repayment term can result in over $3,000 in additional interest paid. Therefore, understanding and managing the average student loan graduated interest rate is crucial for borrowers seeking to minimize their overall debt burden.

To better manage their student loan debt, borrowers should consider strategies such as making extra payments, refinancing their loans, or exploring income-driven repayment plans. These options can help reduce the total interest paid and potentially lower the average student loan graduated interest rate. Additionally, borrowers should stay informed about changes in interest rates and economic conditions that may affect their loan payments.

In conclusion, the average student loan graduated interest rate is a critical factor for borrowers to consider when managing their student loan debt. By understanding how this rate is calculated, the differences between fixed and variable rates, and the impact of interest rates on the total cost of borrowing, borrowers can make informed decisions to minimize their debt burden and achieve financial stability.

Understanding Graduate Student Stipends: A Comprehensive Guide

You may want to see also

Explore related products

![NMLS Study Cards: NMLS MLO Test Prep 2026-2027 for the SAFE Mortgage Loan Originator Exam with Practice Test Questions [Full Color Cards]](https://m.media-amazon.com/images/I/61f1NUOp4iL._AC_UY218_.jpg)

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UY218_.jpg)

![]()

Current Rates: Overview of the present interest rates for graduated student loans

As of June 2024, the interest rates for graduated student loans have seen a slight increase compared to the previous year. For federal Direct Unsubsidized Loans, the current rate stands at 6.5%, while Direct Subsidized Loans and Direct PLUS Loans are at 5.5% and 8.5%, respectively. These rates are fixed for the life of the loan, providing borrowers with predictability in their repayment plans.

Private student loan rates, on the other hand, vary widely depending on the lender and the borrower's creditworthiness. As of the latest data available, the average private student loan interest rate ranges from 5% to 14%. Borrowers with excellent credit may qualify for rates on the lower end of this spectrum, while those with fair or poor credit may face higher rates.

When considering these rates, it's essential for borrowers to understand the difference between fixed and variable interest rates. Fixed rates remain constant throughout the loan term, while variable rates can fluctuate based on market conditions. This can impact the total amount paid over the life of the loan, as variable rates may increase or decrease over time.

Additionally, borrowers should be aware of any fees associated with their loans, as these can add to the overall cost. Origination fees, late payment fees, and prepayment penalties are common charges that can increase the expense of borrowing.

To manage these costs effectively, borrowers should consider strategies such as making extra payments when possible, refinancing to a lower rate if their credit improves, and taking advantage of any available tax deductions or repayment assistance programs. By staying informed about current rates and loan terms, borrowers can make more informed decisions about their student loan management.

Exploring the Journey: What Is a Prospective Graduate Student?

You may want to see also

Explore related products

![]()

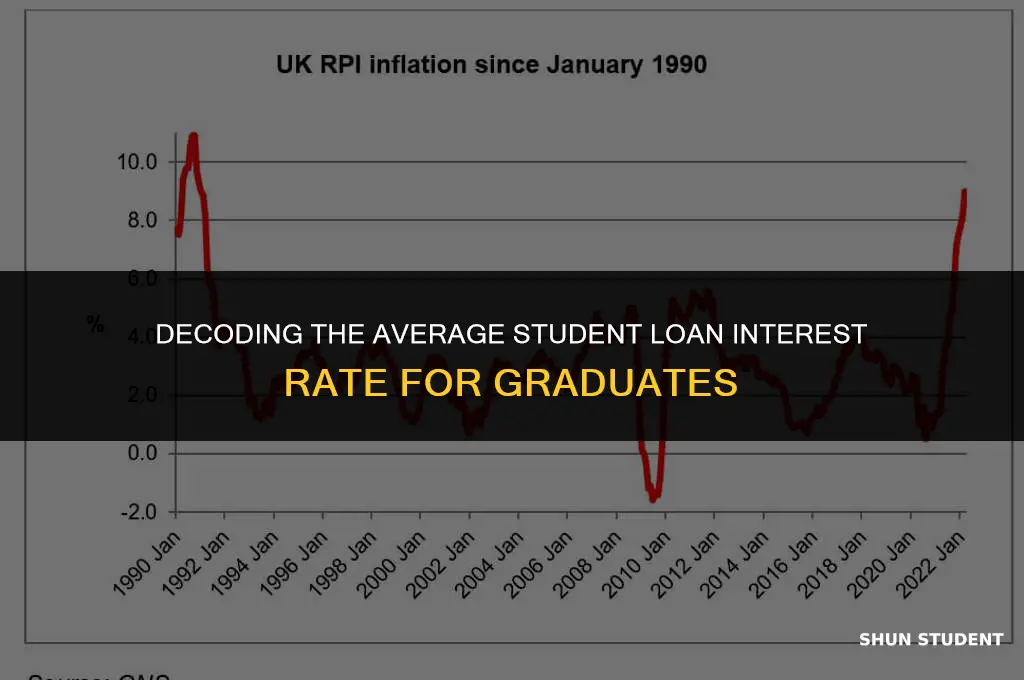

Historical Trends: Analysis of how interest rates have changed over time

Interest rates on student loans have undergone significant changes over the past several decades. In the 1980s, interest rates were relatively high, often exceeding 10%. This was due to a combination of factors, including high inflation rates and a tight monetary policy implemented by the Federal Reserve to combat inflation. As a result, students who took out loans during this period faced substantial financial burdens upon graduation.

In the 1990s and early 2000s, interest rates on student loans began to decline. This was partly due to a decrease in inflation rates and a more accommodative monetary policy. Additionally, the introduction of the Direct Loan Program in 1993, which allowed the government to lend directly to students, helped to lower interest rates. During this period, variable-rate loans became more popular, as they offered lower initial interest rates compared to fixed-rate loans.

However, the mid-2000s saw a reversal of this trend, as interest rates on student loans began to rise again. This was largely due to a series of rate hikes by the Federal Reserve in response to concerns about inflation and economic growth. The increase in interest rates made it more difficult for students to afford their loan payments, leading to a rise in defaults and delinquencies.

The financial crisis of 2008 had a significant impact on the student loan market. In response to the crisis, the Federal Reserve implemented a series of measures to lower interest rates and increase liquidity in the financial system. This led to a decrease in interest rates on student loans, making it more affordable for students to borrow. Additionally, the government introduced new programs, such as the Pay As You Earn (PAYE) repayment plan, which helped to reduce the financial burden on student loan borrowers.

In recent years, interest rates on student loans have remained relatively low, hovering around 5%. This is due to a combination of factors, including low inflation rates, a slow economic recovery, and continued government intervention in the student loan market. However, there are concerns that interest rates may rise in the future, as the Federal Reserve has indicated that it may begin to tighten monetary policy in response to improving economic conditions.

Overall, the historical trends in student loan interest rates have been shaped by a complex interplay of economic factors, government policies, and market conditions. Understanding these trends is essential for students and policymakers alike, as they can help to inform decisions about borrowing and repayment strategies.

Exploring the Journey of a PhD Graduate Student

You may want to see also

Explore related products

![]()

Impact on Borrowers: Discussion of how these rates affect student loan borrowers financially

The impact of average student loan graduated interest rates on borrowers is multifaceted and profound. As borrowers transition from the grace period to the repayment phase, the realization of these rates can lead to significant financial strain. For many, the graduated interest rate structure, which typically increases over time, can result in a substantial rise in the total amount owed, making it challenging to manage monthly payments. This financial burden can affect borrowers' ability to achieve other financial milestones, such as saving for a home, starting a family, or investing in their careers.

Moreover, the psychological impact of these rates should not be underestimated. The stress of accruing interest and the pressure to make timely payments can lead to anxiety and financial insecurity. Borrowers may feel trapped in a cycle of debt, with the graduated rates perpetuating a sense of never-ending financial obligation. This can have long-term effects on mental health and overall well-being.

To mitigate these impacts, borrowers should consider strategies such as refinancing their loans to secure lower interest rates or exploring income-driven repayment plans that adjust monthly payments based on income and family size. Additionally, understanding the terms of their loans and staying informed about changes in interest rates can empower borrowers to make proactive financial decisions.

In conclusion, the average student loan graduated interest rate has far-reaching implications for borrowers, affecting not only their financial stability but also their mental health and life choices. By being aware of these impacts and taking informed actions, borrowers can better navigate the complexities of student loan repayment and work towards achieving their financial goals.

Unlocking Opportunities: A Guide to Graduate Student Externships

You may want to see also

Explore related products

![]()

Comparison Options: Exploration of different lenders and their offered interest rates

To effectively explore different lenders and their offered interest rates for student loans, it's crucial to understand the various types of lenders available. Broadly, student loan lenders can be categorized into federal lenders, private lenders, and credit unions. Federal lenders, such as the U.S. Department of Education, offer loans with fixed interest rates that are typically lower than those offered by private lenders. Private lenders, on the other hand, may offer variable interest rates that can fluctuate based on market conditions. Credit unions often provide competitive interest rates and may have more flexible repayment terms.

When comparing lenders, it's important to consider not only the interest rates but also other factors such as loan terms, repayment options, and any additional fees. For instance, some lenders may offer interest rate discounts for automatic payments or for having a cosigner. Others may have origination fees or prepayment penalties. By carefully evaluating these factors, borrowers can make informed decisions about which lender best suits their needs.

One effective strategy for comparing lenders is to use online comparison tools or platforms that aggregate information from multiple lenders. These tools can help borrowers quickly and easily compare interest rates, loan terms, and other key details. Additionally, borrowers can reach out directly to lenders to request quotes and ask questions about their loan offerings. This proactive approach can help borrowers gain a better understanding of their options and make more confident decisions.

Another important consideration when exploring different lenders is the borrower's own creditworthiness. Lenders typically use credit scores and other financial information to determine eligibility and interest rates. Borrowers with higher credit scores may be eligible for lower interest rates, while those with lower scores may face higher rates or be required to have a cosigner. Understanding one's credit profile and taking steps to improve it, if necessary, can help borrowers secure more favorable loan terms.

In conclusion, exploring different lenders and their offered interest rates requires a thoughtful and comprehensive approach. By considering various types of lenders, evaluating key factors such as loan terms and fees, utilizing online comparison tools, and understanding one's own creditworthiness, borrowers can make informed decisions that best align with their financial goals and needs.

Exploring the Path of a Non-Degree Graduate Student

You may want to see also

Frequently asked questions

As of my last update in June 2024, the average student loan interest rate for graduates in the United States is around 7%. However, this rate can vary depending on the type of loan and the lender.

The interest rate on a student loan significantly impacts the total amount paid back. A higher interest rate means more money will be paid in interest over the life of the loan, increasing the total cost. For example, on a $30,000 loan with a 7% interest rate over a 10-year term, the total amount paid back would be approximately $42,200, with about $12,200 of that being interest.

Yes, there are several ways to potentially reduce the interest rate on a student loan after graduation. These include refinancing the loan with a private lender, consolidating multiple loans into one with a lower interest rate, or applying for an income-driven repayment plan which may offer lower interest rates or interest subsidies.

A fixed interest rate on a student loan remains the same throughout the life of the loan, providing predictable monthly payments. A variable interest rate, on the other hand, can change periodically based on market conditions, which means the monthly payment amount can fluctuate. Fixed rates are often preferred for their stability, while variable rates may start lower but can increase over time.

To find out the specific interest rate on your student loan, you can check your loan agreement or contact your loan servicer directly. The interest rate should be clearly stated in the terms and conditions of your loan contract. Additionally, you can often find this information through your online loan account or by reviewing your monthly billing statement.