Physician student loan forgiveness is a critical topic for medical professionals burdened by substantial educational debt. Many physicians graduate with hundreds of thousands of dollars in student loans, making repayment a significant financial challenge. To alleviate this burden, various loan forgiveness programs have been established, offering relief in exchange for service commitments in underserved areas, public health roles, or specific specialties. The rate of forgiveness varies widely depending on the program, with some offering partial forgiveness over time and others providing full loan forgiveness after a set number of years. Understanding the eligibility criteria, application processes, and repayment structures of these programs is essential for physicians seeking to manage their debt effectively while contributing to healthcare needs in high-demand areas.

Explore related products

What You'll Learn

![]()

Eligibility criteria for physician loan forgiveness programs

Physician student loan forgiveness programs offer a lifeline to medical professionals burdened by debt, but not all doctors qualify. Eligibility criteria vary widely across programs, often hinging on factors like specialty, practice setting, and commitment duration. For instance, the National Health Service Corps (NHSC) Loan Repayment Program requires physicians to serve in Health Professional Shortage Areas (HPSAs) for at least two years, with repayment amounts capped at $50,000 annually. Understanding these specifics is crucial for physicians seeking financial relief.

To qualify for most loan forgiveness programs, physicians must meet stringent service requirements. Programs like the Public Service Loan Forgiveness (PSLF) mandate 10 years of full-time employment in a qualifying nonprofit or government organization, with 120 eligible monthly payments. In contrast, state-specific programs may offer faster forgiveness but require practice in underserved areas, such as rural clinics or community health centers. For example, California’s Steven M. Thompson Loan Forgiveness Program forgives up to $105,000 in loans for physicians serving in federally designated HPSAs for three years.

Specialty plays a pivotal role in eligibility, with primary care physicians often prioritized over specialists. Programs like the NHSC and the Indian Health Service Loan Repayment Program favor family medicine, internal medicine, pediatrics, and obstetrics/gynecology practitioners. Specialists, however, are not entirely excluded; some programs, like the NIH Loan Repayment Programs, target physicians conducting research in areas like cancer or pediatric medicine, offering up to $50,000 annually in loan repayment.

Beyond service and specialty, administrative details can make or break eligibility. Physicians must ensure their loans qualify—federal Direct Loans are typically required for PSLF, while private loans are ineligible. Additionally, maintaining full-time status (usually 32+ hours per week) and submitting timely applications are non-negotiable. For instance, the NHSC requires applications to be submitted during specific cycles, with awards contingent on funding availability.

Practical tips can streamline the application process. Physicians should document all service hours and payments meticulously, as inconsistencies can delay or disqualify applications. Networking with program alumni or attending informational webinars can provide insider insights. Finally, exploring multiple programs simultaneously increases the chances of securing forgiveness. For example, a physician could apply to both the NHSC and a state-based program, leveraging overlapping eligibility criteria to maximize benefits.

In summary, eligibility for physician loan forgiveness programs demands careful planning and adherence to specific criteria. By focusing on service requirements, specialty alignment, administrative details, and strategic application, physicians can navigate these programs effectively, turning overwhelming debt into manageable—or even forgivable—obligations.

Government Student Loan Forgiveness Programs: What’s Available Now?

You may want to see also

Explore related products

$7.99 $14.99

$7.99

$22.96 $29.95

![]()

Maximum loan forgiveness amounts available for physicians

Physicians burdened by student loan debt often seek relief through forgiveness programs, but the maximum amounts available vary widely based on the program and eligibility criteria. For instance, the Public Service Loan Forgiveness (PSLF) program offers complete tax-free forgiveness after 120 qualifying payments, potentially wiping out six-figure debt for those working full-time in eligible nonprofit or government roles. However, this program requires meticulous documentation and adherence to strict guidelines, making it a high-reward but high-effort option.

In contrast, the National Health Service Corps (NHSC) Loan Repayment Program provides up to $50,000 in loan forgiveness for a two-year commitment to serve in a Health Professional Shortage Area (HPSA). Physicians can renew their commitment for additional years, potentially reaching $250,000 in total forgiveness. This program is particularly attractive for primary care physicians, but it requires working in underserved areas, which may not align with everyone’s career goals or personal circumstances.

For those in academic medicine, the NIH Loan Repayment Programs offer up to $50,000 annually in loan repayment for researchers committing to biomedical or clinical research careers. While this program doesn’t cap total forgiveness, it requires a minimum two-year commitment and competitive renewal. It’s ideal for physicians passionate about research but less appealing for those seeking clinical practice-focused relief.

State-specific loan forgiveness programs further expand options, though maximum amounts vary significantly. For example, California’s Steven M. Thompson Loan Forgiveness Program offers up to $105,000 for physicians working in federally designated underserved areas, while New York’s Doctors Across New York program provides up to $20,000 annually for a five-year commitment. These programs often have fewer applicants than federal options, increasing the likelihood of approval but requiring careful research to match eligibility criteria.

When evaluating maximum forgiveness amounts, physicians must weigh commitment length, practice location, and career alignment. While PSLF offers the highest potential forgiveness, its rigid requirements may not suit everyone. Alternatively, targeted programs like NHSC or state-specific options provide substantial relief with shorter commitments but may limit practice flexibility. Ultimately, maximizing loan forgiveness requires strategic planning, early program enrollment, and a clear understanding of personal and professional priorities.

Student Loan Forgiveness for First Responders: What You Need to Know

You may want to see also

Explore related products

![]()

Repayment terms and conditions for forgiveness

Physicians burdened by student loan debt often seek relief through forgiveness programs, but the path to forgiveness is paved with specific repayment terms and conditions. Understanding these requirements is crucial to maximizing the benefits and avoiding pitfalls.

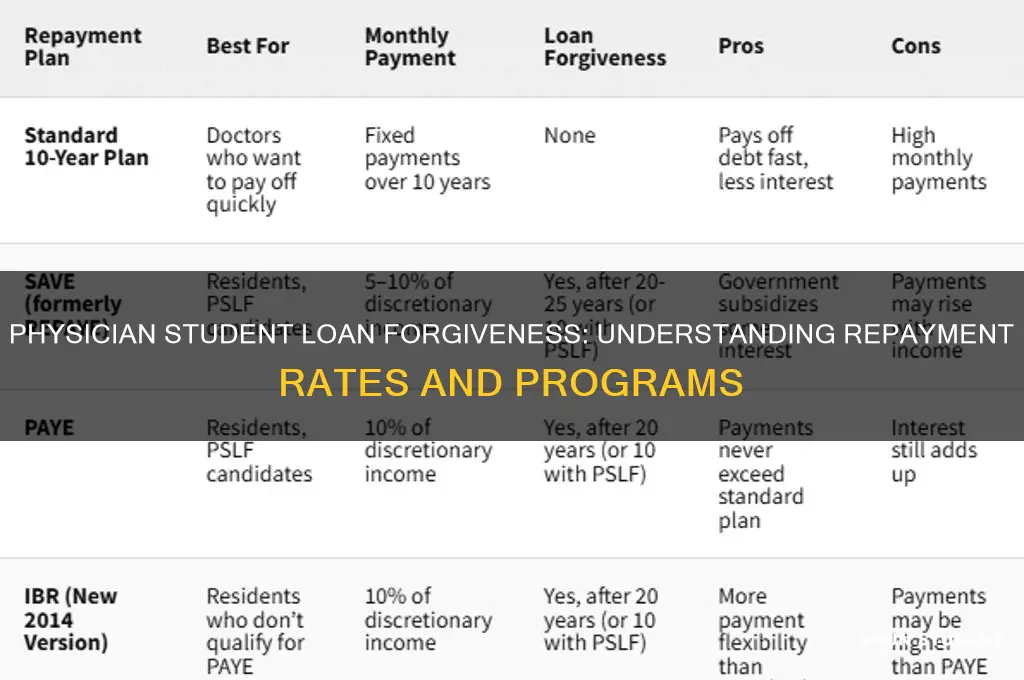

Qualifying Repayment Plans: The Foundation of Forgiveness

Most physician loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, mandate enrollment in specific repayment plans. PSLF requires borrowers to make 120 qualifying payments while employed full-time by a qualifying employer, such as a 501(c)(3) nonprofit or government organization. IDR plans, including Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE), calculate monthly payments based on income and family size, typically ranging from 10-20% of discretionary income.

Employment and Payment Requirements: Staying on Track

Forgiveness programs have stringent employment and payment requirements. For PSLF, borrowers must submit an Employment Certification Form annually or when changing employers to ensure continued eligibility. Missing payments or making late payments can disrupt the 120-payment count, delaying forgiveness. IDR plans require annual recertification of income and family size to maintain adjusted payment amounts. Failure to recertify can result in a return to the standard repayment plan, potentially increasing monthly payments.

Tax Implications and Strategic Planning: A Double-Edged Sword

While loan forgiveness can provide significant financial relief, it may also trigger tax consequences. Under current law, forgiven amounts through PSLF are tax-free, but forgiven amounts through IDR plans after 20-25 years of repayment are considered taxable income. Physicians should consult tax professionals to develop strategies, such as setting aside funds in a tax-advantaged account or timing forgiveness to coincide with lower-income years, to minimize tax liabilities.

Navigating Program Nuances: Avoiding Common Pitfalls

Each forgiveness program has unique nuances that can impact eligibility and repayment terms. For instance, Federal Family Education Loan (FFEL) Program loans are not eligible for PSLF unless consolidated into a Direct Consolidation Loan. Parent PLUS loans can only be forgiven through the Income-Contingent Repayment (ICR) plan or PSLF if consolidated into a Direct Consolidation Loan and repaid under an IDR plan. Physicians should carefully review program guidelines, maintain meticulous records, and seek guidance from loan servicers or financial advisors to ensure compliance with repayment terms and conditions. By understanding and adhering to these requirements, physicians can optimize their chances of achieving loan forgiveness and alleviating the burden of student debt.

Minnesota's Tax Rules: Will Forgiven Student Loans Be Taxable?

You may want to see also

Explore related products

![]()

Tax implications of physician loan forgiveness

Physician student loan forgiveness programs, such as the Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, offer significant relief for medical professionals burdened by educational debt. However, the tax implications of these programs can complicate their benefits. For instance, under current federal law, forgiven loan amounts are generally treated as taxable income, potentially resulting in a substantial tax liability for physicians. This means that while the principal and interest on the loan may be forgiven after meeting program requirements, the IRS considers the forgiven amount as income, subjecting it to federal and, in some cases, state income tax.

Consider a physician who has $250,000 in student loans forgiven after 10 years of qualifying payments under PSLF. Without proper planning, this forgiven amount could push them into a higher tax bracket, resulting in a tax bill of $60,000 or more, depending on their marginal tax rate. To mitigate this, physicians should explore strategies such as setting aside a portion of their income annually in a tax-deferred account or consulting a tax professional to estimate their future liability. Additionally, understanding the nuances of state tax laws is crucial, as some states, like Pennsylvania and Virginia, follow federal guidelines and tax forgiven loans, while others, like California, exempt PSLF forgiveness from state taxation.

A comparative analysis reveals that income-driven repayment plans, such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE), also have tax implications, but they differ from PSLF. Under these plans, any remaining loan balance forgiven after 20–25 years of payments is taxed as income. However, physicians in these programs often have lower annual incomes during repayment, potentially placing them in a lower tax bracket when forgiveness occurs. For example, a physician earning $150,000 annually under REPAYE may face a smaller tax burden compared to a colleague earning $300,000 when their loans are forgiven. This underscores the importance of aligning repayment strategies with long-term financial goals and tax planning.

To navigate these complexities, physicians should adopt a proactive approach. First, calculate the estimated taxable amount of potential loan forgiveness and incorporate it into a broader financial plan. Second, consider relocating to a state with favorable tax treatment of loan forgiveness, if feasible. Third, explore tax-advantaged retirement accounts, such as 401(k)s or Health Savings Accounts (HSAs), to reduce taxable income in years leading up to forgiveness. Finally, physicians should stay informed about legislative changes, as proposals to eliminate the taxability of student loan forgiveness have been introduced in Congress, though none have passed as of 2023.

In conclusion, while physician loan forgiveness programs provide a pathway to debt relief, their tax implications demand careful consideration. By understanding the rules, planning ahead, and leveraging available strategies, physicians can minimize their tax liability and maximize the benefits of these programs. Ignoring these implications could transform a financial windfall into an unexpected burden, underscoring the need for informed decision-making in managing student loan debt.

Unlock Retroactive Student Loan Forgiveness: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Comparison of federal vs. state forgiveness programs

Physicians burdened by student loan debt often turn to forgiveness programs for relief, but the landscape is complex. A critical distinction lies in understanding the differences between federal and state-level initiatives. While both aim to alleviate financial strain, their structures, eligibility criteria, and benefits vary significantly.

Federal programs, administered by the Department of Education, offer broader accessibility but often require longer commitment periods. For instance, the Public Service Loan Forgiveness (PSLF) program forgives remaining debt after 120 qualifying payments (10 years) for those working full-time in eligible public service jobs, including many healthcare roles. However, stringent requirements regarding loan type, repayment plan, and employer certification demand meticulous attention to detail. Conversely, state-level programs, though more localized, can provide faster relief and target specific specialties or underserved areas. For example, the California State Loan Repayment Program offers up to $50,000 annually for two years to primary care physicians serving in Health Professional Shortage Areas (HPSAs). Such programs often prioritize immediate community needs, making them attractive for those seeking shorter-term solutions.

Analyzing these programs reveals a trade-off between scope and specificity. Federal programs cast a wider net, benefiting a larger pool of physicians but requiring sustained commitment. State programs, while more niche, offer tailored incentives that align with regional healthcare priorities. For instance, rural states like Kansas or Nebraska may provide substantial loan repayment for physicians practicing in remote areas, addressing critical shortages. This localized focus can be particularly advantageous for physicians willing to commit to underserved communities. However, state programs often have limited funding and competitive selection processes, making federal options a more reliable fallback for some.

A practical approach involves assessing individual circumstances and long-term career goals. Physicians in urban areas with diverse job opportunities might lean toward federal programs for flexibility, while those passionate about rural or underserved medicine could benefit more from state-specific incentives. Additionally, combining programs—such as using PSLF while simultaneously applying for state repayment assistance—can maximize benefits. For example, a physician working in a rural HPSA could qualify for both PSLF and state repayment, effectively accelerating debt relief.

In conclusion, the choice between federal and state forgiveness programs hinges on aligning program requirements with personal and professional objectives. Federal programs offer stability and broad eligibility, while state programs provide targeted, often more lucrative, opportunities. By carefully evaluating eligibility, commitment timelines, and regional needs, physicians can strategically navigate these options to minimize debt and maximize career satisfaction.

SAVE Program: Unlocking Student Loan Forgiveness Opportunities Explained

You may want to see also

Frequently asked questions

The rate of physician student loan forgiveness varies depending on the program. For example, the Public Service Loan Forgiveness (PSLF) program forgives the remaining balance after 120 qualifying payments, which is 100% of the remaining debt. Other programs like the National Health Service Corps (NHSC) offer up to $50,000 in loan repayment for two years of service, with additional amounts for extended service.

The PSLF program forgives the remaining balance of federal student loans after 120 qualifying payments (10 years) for physicians working full-time in eligible public service jobs, such as government, non-profit, or certain healthcare organizations. The forgiveness amount is tax-free.

Yes, primary care physicians can benefit from programs like the NHSC Loan Repayment Program, which offers up to $50,000 in loan repayment for two years of service in a Health Professional Shortage Area (HPSA). Additional years of service can increase the repayment amount.

No, most physician student loan forgiveness programs, such as PSLF and NHSC, only apply to federal student loans. Private loans are generally not eligible for these programs, though some state-based or employer-sponsored programs may offer assistance for private loans.