The Supreme Court's decision on student loan forgiveness has been a highly anticipated and contentious issue, as it directly impacts millions of borrowers across the United States. In June 2023, the Court ruled on the Biden administration's student loan forgiveness program, which aimed to cancel up to $20,000 in debt for eligible borrowers. The Court’s 6-3 decision struck down the program, determining that the administration overstepped its authority under the HEROES Act of 2003, which allows the Secretary of Education to waive or modify federal student loan regulations during national emergencies. The ruling cited a lack of clear congressional authorization for such broad debt relief, leaving borrowers and policymakers to grapple with the implications for the future of student loan policy and the ongoing student debt crisis.

| Characteristics | Values |

|---|---|

| Decision Date | June 30, 2023 |

| Case Name | Biden v. Nebraska and Department of Education v. Brown |

| Outcome | The Supreme Court struck down President Biden's student loan forgiveness plan. |

| Ruling Basis | The Court ruled that the Biden administration exceeded its authority under the HEROES Act. |

| Majority Opinion | Written by Chief Justice John Roberts, joined by 5 other conservative justices. |

| Dissenting Opinion | Justices Sonia Sotomayor, Elena Kagan, and Ketanji Brown Jackson dissented. |

| Loan Forgiveness Plan | The plan aimed to forgive up to $20,000 in federal student loan debt for eligible borrowers. |

| Impact on Borrowers | Approximately 43 million borrowers were affected, with 20 million expected to have their debt fully canceled. |

| Legal Authority Cited | The HEROES Act of 2003, which allows the Education Secretary to modify student loans during national emergencies. |

| Key Argument Against | The Court held that the plan constituted major policy change requiring clear congressional authorization. |

| Current Status of Loan Payments | Student loan payments resumed in October 2023 after a pandemic-related pause. |

| Alternative Relief Measures | The Biden administration announced targeted relief programs, such as income-driven repayment plan reforms. |

Explore related products

What You'll Learn

- Eligibility criteria for loan forgiveness under the Supreme Court's ruling

- Impact of the decision on Biden's student debt relief plan

- Legal arguments presented by both sides in the case

- Implications for future federal student loan forgiveness programs

- Reactions from borrowers, lawmakers, and advocacy groups post-decision

![]()

Eligibility criteria for loan forgiveness under the Supreme Court's ruling

The Supreme Court's decision on student loan forgiveness, specifically in the case of *Biden v. Nebraska* (2023), struck down the Biden administration's broad student loan forgiveness plan, which aimed to cancel up to $20,000 in debt for eligible borrowers. This ruling significantly narrowed the scope of loan forgiveness, leaving many borrowers uncertain about their eligibility. To understand who may still qualify for relief, it’s essential to examine the remaining pathways for loan forgiveness that align with the Court’s decision.

One key eligibility criterion for loan forgiveness post-ruling is participation in income-driven repayment (IDR) plans. These plans, such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE), cap monthly payments at a percentage of the borrower’s discretionary income and offer forgiveness after 20–25 years of consistent payments. Borrowers enrolled in these plans must meet specific income thresholds and recertify their income annually to remain eligible. For example, a single borrower earning $50,000 annually with $30,000 in loans could see monthly payments reduced to as low as $150 under REPAYE, with forgiveness possible after 240 payments.

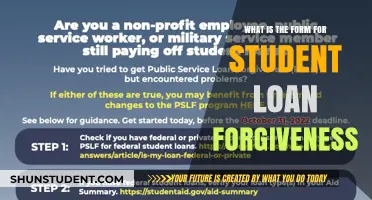

Another pathway is the Public Service Loan Forgiveness (PSLF) program, which remains unaffected by the Supreme Court’s ruling. This program forgives the remaining balance on federal Direct Loans after 120 qualifying payments for borrowers working full-time in eligible public service jobs, such as government or nonprofit organizations. To qualify, borrowers must submit a PSLF form to certify their employment and ensure their payments count toward forgiveness. For instance, a teacher with $40,000 in loans could have their debt forgiven after 10 years of service, provided they meet all program requirements.

Borrowers who were defrauded by their colleges may still seek relief through the Borrower Defense to Repayment program. This pathway allows individuals to apply for loan discharge if their school misled them or violated certain laws. The Supreme Court’s ruling did not impact this program, making it a viable option for those who attended predatory institutions. Applicants must provide evidence of the school’s misconduct, such as false job placement rates or accreditation claims, to qualify for forgiveness.

Finally, borrowers with total and permanent disabilities (TPD) can apply for loan discharge through the TPD program. This pathway requires medical documentation proving the borrower’s inability to work due to a disability. The Supreme Court’s decision did not affect this program, ensuring that disabled borrowers can still access relief. For example, a borrower with a severe medical condition could submit a physician’s certification to have their loans discharged without further repayment obligations.

In summary, while the Supreme Court’s ruling limited broad student loan forgiveness, specific eligibility criteria remain for targeted programs like IDR, PSLF, Borrower Defense, and TPD discharge. Borrowers must carefully review these pathways, meet the requirements, and take proactive steps to apply for the relief they qualify for.

Disability Student Loan Forgiveness: Tax Implications Explained

You may want to see also

Explore related products

![]()

Impact of the decision on Biden's student debt relief plan

The Supreme Court’s June 2023 decision in *Biden v. Nebraska* struck down President Biden’s student debt relief plan, which aimed to cancel up to $20,000 in federal student loans for eligible borrowers. The Court ruled 6-3 that the administration overstepped its authority under the HEROES Act, which allows the Secretary of Education to waive or modify student loan terms during national emergencies. This decision immediately halted a program that had already been approved for nearly 26 million borrowers, leaving millions in financial limbo. The ruling not only invalidated the plan but also set a precedent limiting executive power in broad policy actions without explicit congressional approval.

Analyzing the impact, the decision dealt a significant blow to Biden’s signature economic relief initiative, which was framed as a lifeline for low- and middle-income borrowers. For those with Pell Grants, the plan offered up to $20,000 in forgiveness, while others qualified for $10,000. The Court’s ruling forced the administration to pivot, shifting focus to alternative strategies like income-driven repayment plans and targeted loan forgiveness for public service workers. However, these measures lack the sweeping scale of the original plan, leaving a gap in addressing the $1.7 trillion student debt crisis. Borrowers who had already received approval or were planning their finances around forgiveness faced renewed uncertainty, with payments resuming in October 2023 after a three-year pause.

From a comparative perspective, the decision highlighted the stark divide between judicial and executive interpretations of emergency powers. While the Biden administration argued the HEROES Act granted broad discretion during the COVID-19 pandemic, the Court’s majority opinion emphasized the need for clear congressional authorization for such expansive actions. This contrasts with past instances where executive actions during emergencies, such as pandemic-related eviction moratoriums, were allowed to proceed. The ruling underscores a growing trend of judicial scrutiny of executive overreach, potentially limiting future administrations’ ability to act unilaterally on contentious policy issues.

For borrowers, the practical takeaway is clear: explore alternative relief options immediately. Income-driven repayment plans, such as SAVE (Saving on a Valuable Education), cap monthly payments at 5% of discretionary income and offer forgiveness after 20–25 years. Public Service Loan Forgiveness (PSLF) remains an option for eligible workers, though it requires 10 years of qualifying payments. Borrowers should also monitor legislative efforts, as Congress could still pass targeted relief measures. Meanwhile, advocates argue the decision necessitates a broader rethinking of higher education financing, including lowering college costs and increasing institutional accountability.

Instructively, borrowers should take proactive steps to manage their debt post-decision. First, reassess your budget to accommodate resumed payments, which began in October 2023. Second, enroll in an income-driven plan to lower monthly obligations and track progress toward forgiveness. Third, stay informed about potential legislative or administrative changes that could offer relief. Finally, consider refinancing private loans if interest rates are favorable, though federal loans offer more protections. The Supreme Court’s decision closed one door but opened others for advocacy and reform, making this a critical moment for borrowers to engage with their financial futures.

NJ Unemployment Overpayment Forgiveness for College Students: What You Need to Know

You may want to see also

Explore related products

![]()

Legal arguments presented by both sides in the case

The Supreme Court's decision in *Biden v. Nebraska* (2023) hinged on competing interpretations of federal authority and statutory limits, with both sides marshaling intricate legal arguments to support their positions. At the heart of the case was the Biden administration’s student loan forgiveness program, which sought to cancel up to $20,000 in debt for eligible borrowers under the HEROES Act of 2003. Proponents argued that the Act granted the Secretary of Education broad discretion to modify student loan terms during national emergencies, such as the COVID-19 pandemic. They emphasized the economic hardship faced by millions of borrowers and the Secretary’s historical use of the Act to provide relief in smaller-scale crises. This argument framed the program as a lawful exercise of executive authority to address a pressing national issue.

Opponents, including several Republican-led states, countered that the HEROES Act did not authorize such sweeping debt cancellation. They argued that the program exceeded statutory limits by effectively waiving debt rather than merely modifying loan terms, as the Act permits. Critics also invoked the Major Questions Doctrine, asserting that Congress, not the executive branch, must explicitly authorize actions with significant economic and political consequences. This doctrine, rooted in separation of powers principles, was central to their claim that the administration overstepped its bounds. Additionally, they highlighted the lack of clear congressional intent to delegate such broad authority, framing the program as an unconstitutional usurpation of legislative power.

A key point of contention was the interpretation of the phrase "waive or modify" in the HEROES Act. The administration argued that "modify" encompassed the power to cancel debt, citing dictionary definitions and legislative history. Opponents, however, distinguished between modification—such as adjusting interest rates or payment schedules—and outright cancellation, which they deemed beyond the Act’s scope. This linguistic debate underscored the case’s reliance on statutory interpretation and the role of judicial scrutiny in resolving ambiguities in federal law.

Practical implications of these arguments were stark. For borrowers, the program promised financial relief, but its legality remained uncertain. For the administration, the case tested the limits of executive action in addressing systemic issues. The Supreme Court’s 6-3 decision ultimately sided with the opponents, ruling that the program exceeded the authority granted by the HEROES Act and violated the Major Questions Doctrine. This outcome highlighted the judiciary’s role in checking executive power and reinforced the principle that significant policy changes require explicit congressional approval.

To navigate such legal disputes, stakeholders must carefully examine statutory language, legislative intent, and constitutional principles. For instance, when drafting or interpreting laws, clarity in wording—such as explicitly defining terms like "modify"—can prevent future litigation. Similarly, policymakers should consider the Major Questions Doctrine when proposing actions with far-reaching consequences, ensuring they have a clear legal basis. For borrowers and advocates, understanding these legal nuances can inform strategies for pursuing debt relief through legislative channels rather than relying on executive action. This case serves as a reminder that even well-intentioned policies must align with established legal frameworks to withstand judicial scrutiny.

Can Teachers Get Student Loan Forgiveness? Exploring Eligibility and Programs

You may want to see also

Explore related products

![]()

Implications for future federal student loan forgiveness programs

The Supreme Court’s 2023 decision in *Biden v. Nebraska* struck down the Biden administration’s sweeping student loan forgiveness plan, citing a lack of explicit congressional authorization under the HEROES Act. This ruling sets a precedent that limits executive authority to implement large-scale debt relief without clear legislative backing. For future federal student loan forgiveness programs, this means policymakers must prioritize bipartisan legislation rather than relying on executive action. Without such collaboration, any future attempts at broad forgiveness will face immediate legal challenges, delaying relief for millions of borrowers.

One immediate implication is the need for targeted, rather than universal, forgiveness programs. The Court’s decision suggests that initiatives with specific eligibility criteria—such as income thresholds, public service requirements, or focus on predatory lending victims—may fare better legally. For example, expanding the Public Service Loan Forgiveness (PSLF) program or creating relief for borrowers defrauded by for-profit institutions could align with existing statutory frameworks. Policymakers should focus on crafting programs that address inequities without overstepping executive authority, ensuring they are defensible in court.

Another critical takeaway is the importance of transparency and public engagement. The Biden administration’s plan faced criticism for its abrupt rollout and lack of stakeholder input. Future programs must involve borrowers, educators, and financial experts in the design process to build credibility and reduce legal vulnerabilities. Additionally, clear communication about eligibility, application processes, and timelines will be essential to avoid confusion and ensure equitable access. Borrowers need practical guidance, such as step-by-step instructions for applying and documentation requirements, to navigate these programs effectively.

Finally, the decision underscores the need for long-term reforms to the student loan system. Rather than relying on piecemeal forgiveness initiatives, policymakers should address root causes of debt, such as rising tuition costs and inadequate funding for public institutions. Proposals like increasing Pell Grants, capping interest rates, or implementing income-driven repayment plans as the default option could prevent future debt crises. While these measures may take time to implement, they offer a more sustainable solution than recurring forgiveness debates. Borrowers, especially those under 30 or earning below $50,000 annually, would benefit most from systemic changes that reduce reliance on loans altogether.

Will Biden Deliver on Student Debt Forgiveness? Analyzing the Promises

You may want to see also

Explore related products

![]()

Reactions from borrowers, lawmakers, and advocacy groups post-decision

The Supreme Court’s June 2023 decision striking down President Biden’s student loan forgiveness plan sent shockwaves through millions of borrowers, igniting a spectrum of reactions that mirrored the complexity of the issue itself. For borrowers, the ruling was a gut punch. Many had already factored the promised $10,000 to $20,000 in relief into their financial plans, only to see it vanish overnight. Social media platforms erupted with stories of dashed hopes: a single mother in Texas who had planned to use the savings to cover childcare, a recent graduate in Ohio who had delayed buying a car, and a teacher in New Mexico who had hoped to pay off high-interest credit card debt. The emotional toll was palpable, with hashtags like #BrokenPromises trending alongside expressions of frustration and despair.

Lawmakers, predictably, split along partisan lines. Democrats decried the decision as a blow to economic justice, with Senate Majority Leader Chuck Schumer calling it “a gut-wrenching day for millions of Americans.” Progressives like Senator Elizabeth Warren and Representative Ayanna Pressley doubled down on calls for legislative solutions, urging Congress to act where the executive branch had been blocked. Republicans, meanwhile, hailed the ruling as a victory for fiscal responsibility and the rule of law. Senator Mitch McConnell praised the Court for “reining in executive overreach,” while others argued that widespread loan forgiveness would unfairly burden taxpayers who had not attended college. The divide underscored the deep ideological chasm that continues to stymie bipartisan solutions to the student debt crisis.

Advocacy groups mobilized swiftly, though their strategies diverged sharply. Organizations like the Student Borrower Protection Center and the Debt Collective framed the decision as a call to arms, organizing protests and petition drives to pressure Congress and the Biden administration to explore alternative avenues for relief. They also ramped up efforts to educate borrowers about existing programs, such as income-driven repayment plans and public service loan forgiveness, which remain underutilized due to complexity and lack of awareness. On the other side, groups like the Job Creators Network celebrated the ruling as a win for fairness, arguing that blanket forgiveness would disproportionately benefit higher-earning professionals while doing little to address the root causes of rising tuition costs.

Amid the chaos, practical advice emerged as a lifeline for borrowers. Financial experts urged individuals to reassess their budgets and explore options like refinancing (though cautioning that this would forfeit federal protections), consolidating loans, or applying for hardship forbearance. Mental health advocates also stepped in, offering resources for managing the stress and anxiety triggered by the decision. For many, the takeaway was clear: while the Supreme Court had closed one door, others remained ajar—but navigating them would require vigilance, persistence, and a healthy dose of skepticism about quick fixes. The fight for student debt relief, it seemed, was far from over.

Student Loan Forgiveness and Taxes: Will You Receive a 1099-C?

You may want to see also

Frequently asked questions

In June 2023, the Supreme Court ruled against the Biden administration's student loan forgiveness program in a 6-3 decision. The Court determined that the administration lacked the authority under the HEROES Act to cancel up to $20,000 in student debt per borrower without explicit congressional approval.

No, the decision specifically struck down the Biden administration’s broad loan forgiveness plan. Other forms of loan forgiveness, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) forgiveness, remain available to eligible borrowers.

The administration has limited options but is exploring alternative pathways. One possibility is using the Higher Education Act to provide targeted relief, though this would likely face legal challenges. Additionally, Congress could pass legislation to authorize loan forgiveness, but bipartisan support would be required.