There are a variety of loans available to students to help cover the costs of their education. These include federal loans, which are provided by the government, and private loans, which are provided by banks or other financial institutions. Both types of loans are legal agreements and must be paid back with interest. However, federal loans generally offer more flexibility in terms of repayment options and don't require a credit check, while private loans may offer lower interest rates and the ability to borrow up to 100% of certified school costs. It's important for students to carefully consider their future earning potential and borrow responsibly, as they will need to pay back the full amount borrowed plus interest.

| Characteristics | Values |

|---|---|

| Loan types | Federal and private student loans |

| Loan provider | Federal loans are provided by the government; private loans are provided by banks, credit unions, and other financial institutions |

| Application process | Both federal and private student loans require a legal agreement to be signed; private student loans require a credit check |

| Grace period | Federal loans have a six-month grace period before principal and interest payments begin; private loans have a similar grace period, but interest payments may be required during this time depending on the loan type |

| Repayment | Both federal and private student loans must be paid back with interest; repayment plans and interest rates vary |

| Borrowing amount | Borrow only what you can afford to pay back; consider future income potential |

| Other funding options | Grants, scholarships, work-study programs, and personal savings can also help cover education costs |

Explore related products

What You'll Learn

![]()

Federal vs private student loans

Federal student loans are provided by the government, while private student loans are issued by banks, credit unions, and other financial institutions. Both types of loans have their own eligibility criteria, application process, and terms and conditions. It is recommended to consider federal loans first due to their lower interest rates and valuable borrower protections, such as income-driven repayment plans and loan forgiveness programs. Federal loans also do not consider an applicant's credit score.

Private student loans usually offer the choice of a fixed or variable interest rate, which may be lower than federal loans. They can be more flexible, as they can be taken out by a wider range of people, including students with a cosigner, parents, or creditworthy individuals. However, they often lack the borrower protections that come with federal loans, and there may be fewer safety nets in place. Private loans also require a credit check, and the interest rate offered depends on the applicant's credit score.

To apply for federal student loans, applicants need to complete the Free Application for Federal Student Aid (FAFSA). This also determines eligibility for other federal student aid, such as grants and work-study. Private student loans can be applied for directly from the chosen lender, but enough time must be allowed for the lender to process the loan and send the money to the school.

Federal student loans have loan caps, and graduate students can borrow up to $138,500 in total in direct federal loans, including undergraduate borrowing. Private loan borrowing limits vary by lender but are usually up to the school's cost of attendance. Federal loans also require the payment of an origination fee, which can be high for graduate students, professional students, and parents.

In summary, federal student loans are generally the first choice for most borrowers due to their lower interest rates, income-driven repayment plans, and loan forgiveness options. Private student loans may offer lower interest rates for those with a good credit score but lack the same borrower protections as federal loans. Private loans can be useful for those who have maxed out their federal aid or do not meet the eligibility requirements for federal loans.

How to Strategically Pay Off Student Loans

You may want to see also

Explore related products

![]()

Borrowing only what you can afford

When it comes to student loans, it is important to remember that you should only borrow what you can afford to pay back. This means considering your future earnings and borrowing responsibly. Here are some things to keep in mind:

Firstly, start with financial aid that doesn't need to be repaid, such as scholarships, grants, and savings. Then, explore federal loans before considering private student loans. Federal loans often have lower interest rates and more favourable terms, such as loan forgiveness opportunities and income-driven repayment plans. Private student loans typically have higher interest rates and may require a cosigner if you don't have a strong credit history.

Secondly, keep track of how much you are borrowing. Maintain your own records of all documents and transactions related to your student loans. This will help you understand your total student debt and future repayment obligations. You can access information about your federal student loans through the US Department of Education's Federal Student Aid website, and your college financial aid office or lender can provide information about your private student loan balances.

Thirdly, only borrow what you truly need. To determine this, calculate your total costs for tuition, housing, and living expenses. Then, subtract any financial aid or other funds you have available for these expenses. The remaining amount is what you may need to borrow. Remember that you don't have to accept the full amount offered in a loan; borrow only what is necessary to cover your costs.

Additionally, consider your future earnings and try not to accumulate more student debt than you expect to earn. Visit the US Department of Labor website to estimate your future income potential based on your chosen career path. This can help you make informed decisions about how much to borrow.

Finally, if you need to borrow more than the federal loan limit, consider other options before turning to private student loans. For example, you could work a part-time job to help cover some expenses or enrol in a community college or online program to save on tuition and housing costs. By borrowing responsibly and only what you can afford, you can minimise your future financial burden and ensure a smoother repayment process.

Strategies to Eradicate Six-Figure Student Debt

You may want to see also

Explore related products

$8.34 $17.99

![]()

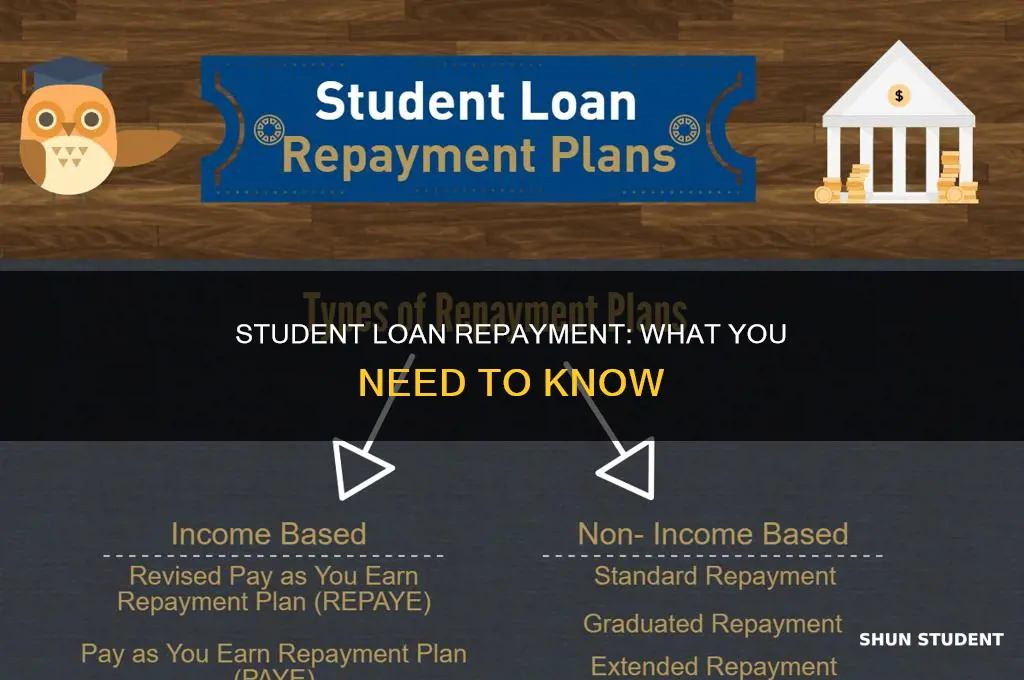

Interest rates and repayments

When taking out a student loan, you will have the option to choose between a variable interest rate and a fixed interest rate. A variable interest rate can fluctuate over time, depending on market conditions. This means your student loan payments may also change. For example, if interest rates rise, you will have higher monthly payments, whereas a drop in interest rates will result in lower monthly payments. On the other hand, a fixed interest rate remains the same throughout the life of the loan, providing more predictability and stability in your repayment plan.

When it comes to repayments, it is important to understand the different options available. Some loans may require you to start making in-school payments immediately after the funds are disbursed, usually once per semester. This means your monthly payments will begin early, and you will need to manage your finances accordingly. Other repayment plans might offer a grace period after graduation before regular repayments commence. This period typically ranges from six months to a year and can provide some financial breathing room as you transition into the workforce.

Additionally, you can choose between various repayment term lengths. A shorter repayment term, such as five or ten years, will result in higher monthly payments but less overall interest paid. On the other hand, a longer repayment term of 15 years or more will reduce your monthly payment amount but result in paying more interest over the life of the loan. It is important to carefully consider your expected future income and financial situation when selecting a repayment term that best suits your needs and abilities.

Finally, some lenders may offer interest-only repayment options during your time in school. This means that you will only be responsible for paying off the interest that accrues during your studies and the subsequent grace period. This can help reduce the overall cost of the loan by lowering the amount of interest that compounds over time. However, it is important to keep in mind that this option may not be available for all loan types and lenders, and it could result in higher monthly payments once the principal amount repayment begins.

Placement Students and Taxes: What You Need to Know

You may want to see also

Explore related products

![]()

Eligibility criteria

When it comes to eligibility criteria for student loans, there are a few key factors to consider. These criteria can vary depending on the type of loan, such as federal or private, and the specific loan programme or provider. Here are some detailed points about eligibility:

- Federal Student Loans: In the US, federal student loans are provided by the government through the Federal Direct Loan Program. One of the advantages of federal loans is that they do not require a credit check for most borrowers. However, there may be specific eligibility criteria based on factors like citizenship or eligible non-citizen status, enrolment in an eligible school, maintaining satisfactory academic progress, and not having defaulted on previous federal student loans. Federal loans often offer more flexibility in repayment plans, including income-driven options where repayments are based on the borrower's post-college salary.

- Private Student Loans: Private student loans are offered by banks, credit unions, and other financial institutions. Unlike federal loans, private loans typically require a credit check as part of the eligibility criteria. If the borrower does not have an established credit history, they may need a creditworthy cosigner who shares responsibility for repaying the loan. Lenders will evaluate the borrower's (and cosigner's) creditworthiness, financial situation, and ability to repay the loan. Private loans may also have specific eligibility requirements regarding enrolment status, academic progress, and loan amounts relative to the cost of attendance.

- General Eligibility: Beyond the specific loan types, there are some general considerations for eligibility. Firstly, age and level of education may be factors, as student loans are typically targeted at undergraduate and graduate students enrolled in accredited institutions. Additionally, factors such as a stable income, proof of employment or financial resources, and a positive credit history (or the presence of a creditworthy cosigner) can significantly influence eligibility for student loans.

- Responsible Borrowing: While not always a formal part of eligibility criteria, responsible borrowing practices are essential when considering student loans. It is recommended that borrowers evaluate their future income potential, borrow only what they need, and start with alternative sources of funding, such as scholarships, grants, savings, or work-study programmes, before turning to loans. Understanding the repayment terms, interest rates, and potential loan burdens is crucial for making informed decisions about eligibility and loan amounts.

Biden's Student Debt Forgiveness: Who Pays and How?

You may want to see also

Explore related products

![]()

Other financial aid options

While student loans are a common way to fund your education, they are not the only option. Here are some alternative financial aid options for students:

Grants

Grants are a significant source of financial aid that generally does not have to be repaid. One of the most common grant options is the Federal Pell Grant. To be eligible for grants, you must meet specific criteria, which may include your educational or financial situation. It is worth noting that some grants may require repayment if your circumstances change.

Scholarships

Scholarships are another form of financial aid that does not require repayment. These are often offered by nonprofit and private organizations and can be based on various factors such as academic merit, talent, financial need, or your chosen area of study. Scholarships are a great way to secure funding for your education without accumulating debt.

Work-Study Programs

The Federal Work-Study Program allows you to earn money while attending school. This program provides part-time job opportunities that can help you pay for your education. Work-study programs are an excellent option if you prefer to earn your education funds rather than borrow them.

Federal Student Loans

Before considering private student loans, it is advisable to explore federal student loan options. Federal loans often have more favourable terms and conditions, including fixed interest rates and income-driven repayment plans. Additionally, federal student loans may offer deferment or forbearance options if you face financial difficulties during repayment.

Savings

Using your savings to fund your education is another option to consider. This approach allows you to avoid debt altogether and maintain financial freedom. However, it is important to weigh this option carefully and ensure that you have sufficient funds to cover your educational expenses.

Remember to research and compare the different financial aid options available to make an informed decision. Each option has its own set of eligibility requirements, application processes, and benefits, so it is essential to understand which ones align best with your financial situation and educational goals.

How Parents Can Repay Student Loans

You may want to see also

Frequently asked questions

There are federal and private student loans. Federal loans are provided by the government, while private loans are provided by banks, credit unions, and other financial institutions.

Federal loans generally offer more flexibility than private loans. Borrowers of federal loans do not need a credit check to be considered (except for Federal PLUS Loans), and they can change their repayment options after the loan has been disbursed. Some federal loans also offer income-driven repayment plans. Private loans, on the other hand, are credit-based and require a credit check. They may offer different repayment plans, such as making interest-only or fixed payments while in school.

If you are entering college and do not have a credit history, you may need a creditworthy cosigner for a private student loan. A cosigner shares the responsibility for paying back the loan with you.

You should borrow only what you can afford to pay back. Consider your future salary and use a responsible borrowing approach. Start with scholarships, grants, and work-study options before exploring federal and private loans.