Student loan debt is a significant issue in the United States, with rising tuition costs and increasing student debt balances. As of 2025, the average federal student loan debt is $38,375, while the total student debt balance, including private loans, stands at $1.77 trillion. More than half of college students graduate with debt, and the share of students with debt has increased over time. The burden of student debt varies across demographic groups, with Black students being the most likely to borrow federal loans and Black adults being more likely to hold student debt compared to other racial groups. Additionally, students with graduate degrees contribute significantly to the total debt balance, as they pursue careers in higher-paying fields. Understanding the prevalence and impact of student debt is crucial for evaluating the accessibility and affordability of higher education.

Explore related products

What You'll Learn

![]()

Racial disparities in student debt

Student debt is a significant issue in the United States, with Americans collectively owing over $1.6 trillion in student loans. This debt disproportionately affects people of colour, exacerbating existing racial wealth disparities.

Black students and graduates are more likely to take on student debt and struggle with repayment compared to their white peers. They are also more likely to report higher levels of stress related to their educational debt. Black students finance their education through debt, contributing to the fragility of the Black middle class. The disproportionate debt they take on to finance their education reinforces the racial wealth gap. The average white family has about ten times the wealth of the average Black family, while white college graduates have over seven times more wealth than Black college graduates.

Several factors contribute to these disparities. Firstly, Black families have historically been disadvantaged by generational wealth disparities, leaving them with fewer resources to pay for college. As a result, Black students rely more heavily on student loans to pursue higher education. Additionally, Black graduates face a larger Black-white wage gap, making it more challenging for them to repay their loans. The income gap persists even with a college degree, as Black workers continue to earn significantly less than their white counterparts.

Furthermore, predominantly white institutions receive more funding through federal, state, and local contracts and grants than Historically Black Colleges and Universities (HBCUs). This disparity in resources affects the endowments and opportunities available to Black students.

The issue of student debt extends beyond Black and white communities. For example, Asian college graduates are the fastest to repay their loans and the most likely to earn higher salaries to facilitate repayment. However, multiracial degree holders are more likely to report high stress levels related to their student debt.

While student debt cancellation has been proposed as a solution, it is essential to recognize that it is not a panacea for addressing racial wealth disparities. Even with debt cancellation, systemic racism and anti-Black policies across multiple sectors continue to hinder wealth-building opportunities for Black communities.

Exploring Drury University's Student Population

You may want to see also

Explore related products

![]()

Undergraduate vs graduate debt

Student loan debt is the second-highest consumer debt category after mortgages. The average federal student loan debt balance is $38,375, while the total average balance may be as high as $41,618. The average public university student borrows $31,960 to attain a bachelor’s degree. About half of students at four-year public universities finish their bachelor’s degree without any debt, and 78% graduated with less than $30,000 in debt. Only 4% of public university graduates left with more than $60,000, and those with over $100,000 in debt are rare, representing 0.5% of graduates.

Among federal student loan borrowers who completed a bachelor’s degree in 2015–16, the average amount owed as a percentage of the amount borrowed as of four years later was 78%. This average percentage varied by race/ethnicity, with Asian graduates owing the least at 63% and Black graduates owing the most at 105% of their original loan.

Graduate students are those who have completed a bachelor’s program and are pursuing an additional degree, such as an MBA, master’s, PhD, or doctorate. Graduate students may be eligible for different types of federal loans and financial aid than they received as an undergraduate. However, federal student loans for graduate students typically have a higher interest rate and fees than options for undergraduate students. Graduate students are also no longer eligible for subsidized student loans, which are loans for which the ED covers all the interest during periods of deferment. This includes in-school deferment, economic hardship deferment, and military deferment. Direct loans for graduate borrowers begin accruing interest the moment the government disburses the funds, even while the student is still in school.

Graduate student debt is consistently higher than undergraduate debt. In 2020, most master’s degree holders carried a cumulative student loan debt balance of over $80,000 adjusted for inflation. For graduate school alone, the average debt among master’s degree holders exceeds $60,000. The average debt for a Master of Business Administration (MBA) graduate is $81,218, while the average debt for a Master of Arts (MA) graduate is $98,087. The average debt for a Master of Science (MS) graduate is $78,893, and the average debt for a Master of Education graduate is $69,857.

Although graduate students have more flexibility in how much they can borrow, it can be challenging to pay back those higher amounts of debt. Graduate students can borrow $20,500 per year, which is significantly higher than undergraduates’ access to between $5,500 and $12,500, with an aggregate limit of $31,000.

Stony Brook University: Student Event Bookings Explained

You may want to see also

Explore related products

![]()

Average student loan debt

The average student loan debt in the United States has been steadily increasing over the years. As of 2025, the average federal student loan debt balance is $38,375, while the total average balance, including private loan debt, may be as high as $41,618. This represents a slight increase from 2024, when the average federal student loan debt was $37,853, and the total average loan debt, including private loans, was estimated to be as high as $40,681. The average federal student loan debt has doubled since 2007, increasing by 108% or 6.0% each year.

In 2023, the average student loan debt for a bachelor's degree was $38,290, with 58% of millennials and 57% of Gen Z-ers with a bachelor's degree taking on student loan debt. The average amount of debt varies across different demographic groups. For example, Black adults were more likely to have student loan debt, with an average federal student loan debt of $33,960 upon graduation with a bachelor's degree, while white student borrowers owed $30,720 on average. Additionally, 64% of student loan debt belongs to women, with Black women having the highest average amount of debt.

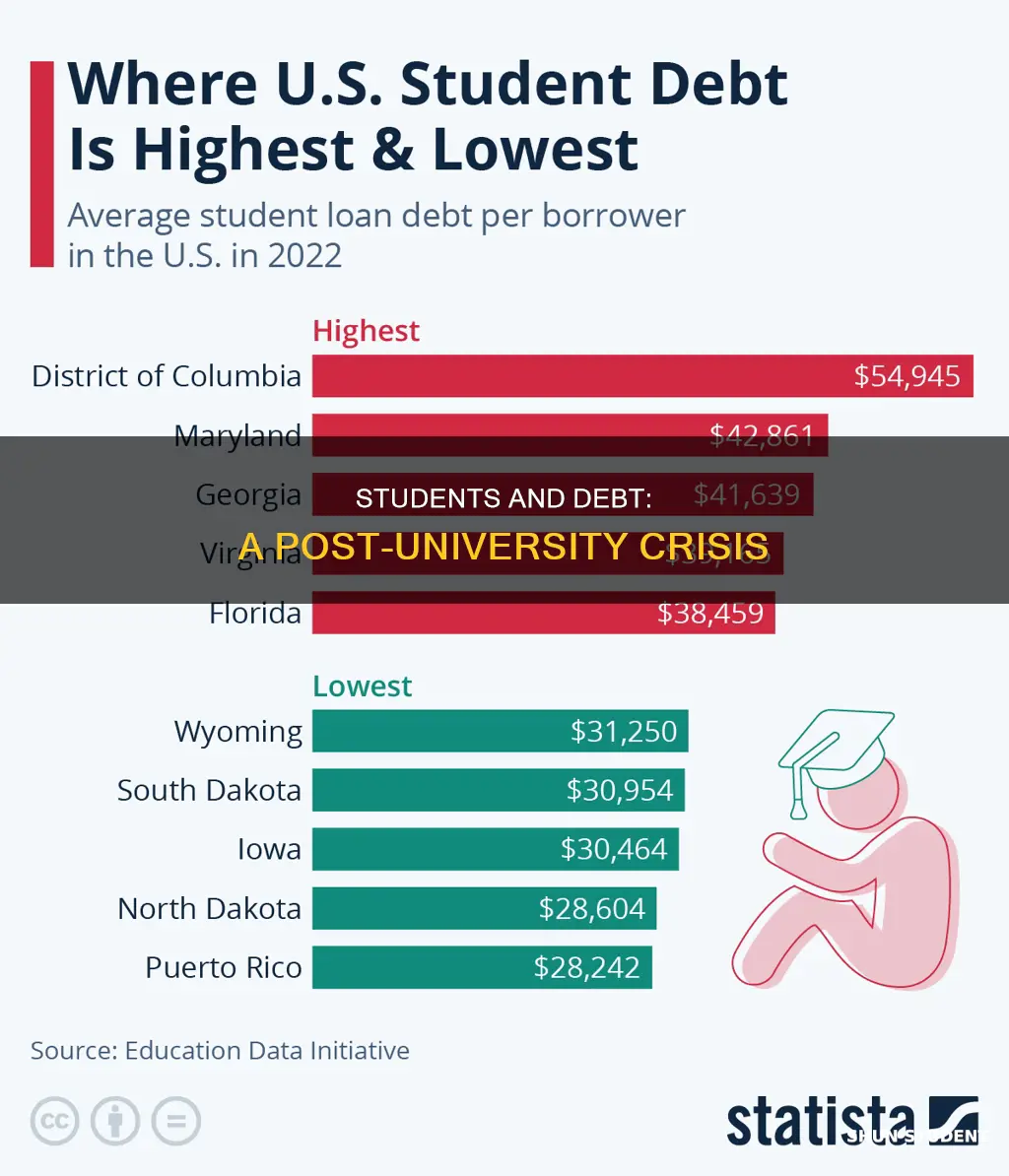

The average student loan debt also differs across states, with Georgia, Maryland, and Mississippi having the highest average student loan debt per capita. In 2024, South Dakota saw the greatest increase in average federal student loan debt per borrower, with an additional $1,381, while Wyoming had the smallest increase of $218.

While the number of federal student loan borrowers has remained relatively stable over the past decade, hovering between 41 and 43 million, the increasing debt balance is attributed to factors such as compounding interest on old student debt and the rising cost of college. Federal student loans account for approximately 92% of all student debt in the United States, with the rest held in private student loans, which often carry higher interest rates.

Manchester Metropolitan University: Student Population Size

You may want to see also

Explore related products

![]()

Student debt repayment plans

Student loan debt is a significant issue in the US, with federal student loan debt representing 92.2% of all student loan debt. The average federal student loan debt balance is $38,375, while the total average balance, including private loan debt, may be as high as $41,618. As of 2024, nearly 43 million Americans had student loan debt, and about a quarter of college graduates between the ages of 25 and 39 reported having trouble making ends meet due to their student loans.

To address this issue, the federal government has created several income-driven student loan repayment plans to make repaying student debt more manageable. These plans take into account factors such as income and family size to determine monthly payments. Here are some of the available repayment plans:

- Standard Repayment Plan: This is the default plan that borrowers are automatically enrolled in unless they sign up for an income-driven plan. The monthly payment is a fixed amount that ensures the loan is paid off within 10 years.

- Income-Driven Repayment (IDR) Plans: These plans base the monthly payment on a percentage of the borrower's discretionary income and family size. Examples include the Income-Based Repayment (IBR) plan, the Pay As You Earn (PAYE) plan, and the Revised Pay As You Earn (REPAYE) plan. The type of IDR plan a borrower qualifies for depends on their financial situation.

- SAVE Plan: This plan is designed for extremely low-income borrowers, with a monthly payment of 10% of discretionary income after meeting the 225% DHHS poverty guideline. The SAVE plan has a time frame of 20 years for undergraduate loans and 25 years for graduate or professional education loans. Possible balance forgiveness is available after 10 years for those who borrowed $12,000 or less.

- Direct Consolidation Loans: These loans are for borrowers with multiple student loans who want to combine them into a single loan with a fixed interest rate based on the average of the interest rates on the consolidated loans. This can simplify repayment by having only one monthly payment and may extend the repayment period, resulting in lower monthly payments.

It's important to note that the availability and specifics of repayment plans may vary depending on the loan type, the borrower's financial situation, and the governing body overseeing the loans. It is always advisable to carefully review the terms and conditions of any loan agreement and seek financial advice if needed.

Utah Students: Free Football Tickets?

You may want to see also

Explore related products

![]()

Student debt relief companies

In the US, student loan debt is the second-highest consumer debt category after mortgages. 20% of American adults with undergraduate degrees have outstanding student debt, and this figure rises to 24% for postgraduate degree holders. Among federal student loan borrowers who completed a bachelor's degree in 2015–16, the average amount owed as a percentage of the amount borrowed as of four years later was 78%. This figure varies by race, with Black bachelor's degree holders owing more than they initially borrowed on average, and Asian graduates owing the least on average.

Some student debt relief companies offer private student loans for undergraduate, graduate, and professional school students, with a minimum loan amount of $5,000 and a maximum of up to $500,000. They may also offer federal and/or private student loan refinancing options for degree-holders, with competitive rates and flexible repayment terms. Consolidation of both federal and private student loans is another service provided by these companies, allowing borrowers to combine multiple debts into one new payoff plan with a single lender and monthly payment.

It is essential for borrowers to carefully review the terms and conditions of any loan or refinancing options offered by student debt relief companies. While these companies can provide assistance and resources, borrowers should be aware of potential fees, pre-payment penalties, origination fees, and other criteria that may apply according to the lender. Additionally, borrowers should be cautious of scams and fraud when dealing with student debt relief companies, and official government programs should always be considered first.

California State University: Student Population Insights

You may want to see also

Frequently asked questions

About half of students have debt after university.

78% of students graduated with less than $30,000 in debt. Only 4% of public university graduates left with more than $60,000.

36% of Black, non-Hispanic adults held student loan debt compared to 20% of white, non-Hispanic adults; 15% of Hispanic adults; and 24% of adults of other races. Black bachelor's degree completers were the only racial/ethnic group whose average amount owed four years after graduation was greater than 100% of the amount borrowed.

Generally, millennials with degrees are more likely than Gen Z-ers with degrees to have acquired student loan debt.

71% of borrowers with a graduate degree, 48% of borrowers with a bachelor’s degree, and 31% of borrowers with an associate degree had student debt balances of over $25,000.