The issue of student debt has become a pressing concern in the realm of higher education, with a significant percentage of college students finding themselves burdened by financial obligations upon graduation. As the cost of tuition continues to rise, many students are forced to rely on loans to fund their education, leading to a growing crisis that affects not only individual students but also the broader economy. Understanding the percentage of college students who will be in debt is crucial in addressing this issue, as it highlights the need for more affordable education options, improved financial aid, and better debt management strategies to alleviate the strain on students and their families.

Explore related products

$8.34 $17.99

What You'll Learn

- Average student loan debt amounts for graduates across different degree types and institutions

- Impact of federal vs. private loans on overall debt accumulation and repayment terms

- Role of socioeconomic status in determining likelihood and severity of student debt

- Effect of scholarships, grants, and work-study programs on reducing debt dependency

- Long-term financial consequences of student debt on career choices and lifestyle post-graduation

![]()

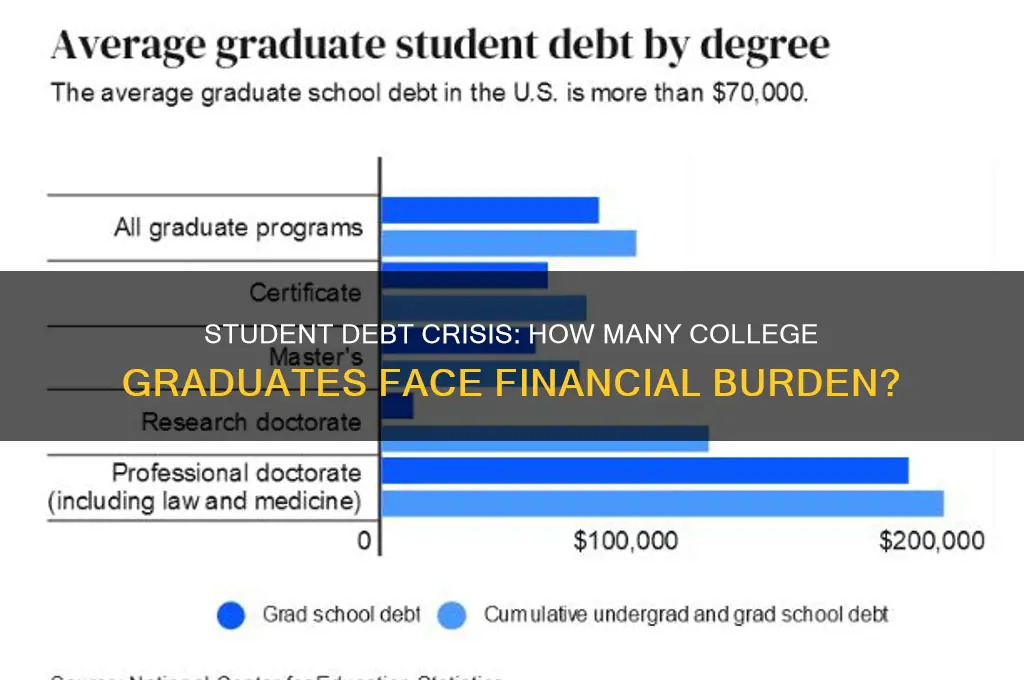

Average student loan debt amounts for graduates across different degree types and institutions

Student loan debt is not a one-size-fits-all burden. Graduates emerge from college with vastly different debt loads depending on their chosen field of study and the type of institution they attended. Understanding these disparities is crucial for students and families navigating the financial realities of higher education.

A 2023 report by the Institute for College Access & Success reveals a stark contrast: graduates with bachelor’s degrees in health professions and related programs averaged $41,944 in debt, while those in education and teaching programs carried an average of $29,320. This disparity highlights the impact of degree type on borrowing needs. Fields requiring specialized equipment, extensive clinical hours, or additional certifications often necessitate higher levels of borrowing.

Community colleges offer a more affordable pathway, with graduates typically accumulating significantly less debt than their four-year university counterparts. The same report found that graduates from public two-year colleges held an average debt of $12,990, compared to $28,800 for graduates of public four-year institutions. This difference underscores the financial advantage of starting at a community college and transferring to a four-year school for degree completion.

Privately funded institutions, unsurprisingly, often come with a heftier price tag. Graduates from private non-profit four-year colleges averaged $33,500 in debt, while those from for-profit institutions faced an average debt burden of $39,900. The higher cost of attendance at private institutions, coupled with potentially lower graduation rates at for-profit schools, contributes to these elevated debt levels.

Understanding these averages is a starting point, not a definitive predictor. Individual circumstances, scholarship opportunities, and financial aid packages play a significant role in determining a student's ultimate debt load. Prospective students should carefully research the average debt burden associated with their desired degree and institution. Utilizing tools like the College Scorecard, which provides data on graduation rates, average debt, and post-graduation earnings for specific programs, can empower students to make informed financial decisions.

Grade Forgiveness: A Student Favorite or Unnecessary Academic Policy?

You may want to see also

Explore related products

![]()

Impact of federal vs. private loans on overall debt accumulation and repayment terms

Federal and private student loans diverge sharply in their impact on debt accumulation and repayment terms, creating vastly different financial trajectories for borrowers. Federal loans, backed by the government, offer fixed interest rates that are typically lower than private alternatives. For instance, as of 2023, undergraduate federal loans carry a rate of 4.99%, compared to private loans, which can range from 3.5% to 14.5% depending on creditworthiness. This disparity alone can add thousands of dollars to a student’s debt over time. For example, a $30,000 federal loan accrues approximately $7,500 in interest over 10 years, while a private loan at 10% would accrue nearly $17,000—a difference of $9,500.

Repayment terms further highlight the advantages of federal loans. Federal borrowers have access to income-driven repayment (IDR) plans, which cap monthly payments at 10-20% of discretionary income and forgive remaining balances after 20-25 years. Private loans rarely offer such flexibility, often requiring fixed payments that can strain recent graduates. For instance, a borrower earning $40,000 annually with $50,000 in federal debt might pay $250/month under an IDR plan, whereas a private loan could demand $500/month or more, depending on the term length. This rigidity can lead to default, which has severe consequences, including damaged credit and wage garnishment.

The accumulation of debt also differs due to borrowing limits and eligibility criteria. Federal loans have annual caps—$5,500 for first-year undergraduates and up to $12,500 for graduate students—which can curb excessive borrowing. Private lenders, however, often approve larger amounts, tempting students to take on more debt than they can manage. A student borrowing the maximum federal amount over four years would graduate with $27,000 in debt, while a private loan borrower might easily exceed $50,000 if not careful. This disparity underscores the importance of exhausting federal options before turning to private lenders.

Practical tips for navigating these differences include prioritizing federal loans through the FAFSA, comparing private loan offers meticulously, and avoiding borrowing more than your expected first-year salary. For example, if you anticipate earning $50,000 annually, limit total borrowing to that amount to ensure manageable payments. Additionally, explore federal forgiveness programs like Public Service Loan Forgiveness (PSLF) if you plan to work in eligible sectors. By understanding these distinctions, students can minimize debt accumulation and leverage favorable repayment terms to achieve financial stability post-graduation.

Can You Get a Student Loan from a Bank? Key Insights

You may want to see also

Explore related products

![]()

Role of socioeconomic status in determining likelihood and severity of student debt

Socioeconomic status (SES) plays a pivotal role in shaping the likelihood and severity of student debt, often determining whether higher education becomes a stepping stone to opportunity or a financial burden. Students from lower-SES backgrounds are disproportionately more likely to take on debt to finance their education. According to a 2020 report by the Institute for Higher Education Policy, 84% of students from families earning less than $30,000 annually borrowed for college, compared to only 54% of students from families earning over $100,000. This disparity highlights how financial constraints force lower-SES students to rely heavily on loans, while higher-SES families can often cover costs through savings or income.

The severity of debt also varies significantly by SES. Lower-SES students not only borrow more frequently but also tend to borrow larger amounts relative to their family resources. For instance, a student from a low-income family attending a public four-year institution might graduate with an average debt of $32,800, whereas a peer from a higher-income family might graduate with $20,000 less, even when attending the same school. This gap is exacerbated by limited access to financial literacy resources and fewer opportunities for high-paying internships or part-time jobs that could offset borrowing.

To mitigate these disparities, targeted interventions are essential. One practical step is expanding need-based financial aid programs, such as Pell Grants, which provide up to $7,395 annually for eligible low-income students. Institutions should also offer financial literacy workshops tailored to lower-SES students, covering topics like loan repayment strategies and budgeting. Additionally, creating work-study programs that align with students’ career goals can help them earn income while gaining relevant experience, reducing reliance on loans.

A comparative analysis reveals that countries with robust public funding for higher education, such as Germany and Norway, have significantly lower student debt rates across all SES levels. In contrast, the U.S. system, which relies heavily on tuition fees and loans, perpetuates inequality. Policymakers can draw lessons from these models by investing in tuition-free or subsidized higher education, particularly for lower-SES students. Such reforms would not only reduce debt but also level the playing field for socioeconomic mobility.

Ultimately, addressing the role of SES in student debt requires a multifaceted approach. By combining expanded financial aid, financial education, and systemic reforms, we can ensure that higher education remains accessible without saddling vulnerable students with crippling debt. The goal should be to create a system where a student’s financial future is determined by their potential, not their family’s bank account.

Biden's Student Loan Forgiveness: Will Parent PLUS Loans Qualify?

You may want to see also

Explore related products

$19.99 $19.99

![]()

Effect of scholarships, grants, and work-study programs on reducing debt dependency

Student debt is a looming specter for many college students, with recent data indicating that over 55% of college graduates carry some form of student loan debt. The average debt burden hovers around $30,000, a figure that can stifle financial independence for years after graduation. However, scholarships, grants, and work-study programs offer a lifeline, significantly reducing the need for loans and mitigating long-term financial strain. These resources, when strategically utilized, can transform the college experience from a debt-ridden journey into a more manageable investment in the future.

Consider the case of merit-based scholarships, which can cover anywhere from a few hundred dollars to the full cost of tuition. For instance, a student awarded a $10,000 annual scholarship over four years could reduce their potential debt by $40,000. This not only lowers the principal amount borrowed but also minimizes the accrual of interest, which compounds over time. Similarly, need-based grants, such as the Federal Pell Grant, provide up to $7,395 per year for eligible students, directly reducing out-of-pocket expenses. By combining scholarships and grants, students can drastically cut their reliance on loans, often graduating debt-free or with a significantly lower balance.

Work-study programs, another underutilized resource, offer a dual benefit: earning money while gaining relevant work experience. These programs typically allow students to work part-time on or off campus, earning up to $5,000 annually, depending on financial need and availability. For example, a student working 10 hours a week at $15 per hour could earn approximately $7,500 over the academic year, funds that can be used to cover textbooks, housing, or other expenses. This reduces the need to take out additional loans for living costs, a common pitfall for many students. Moreover, work-study positions often align with a student’s field of study, providing valuable resume-building opportunities.

However, maximizing the impact of these resources requires proactive planning and strategic application. Students should start by completing the FAFSA (Free Application for Federal Student Aid) as early as possible to determine eligibility for grants and work-study. Additionally, they should research and apply for scholarships aggressively, targeting both institutional and external opportunities. For instance, local community organizations, corporations, and nonprofits often offer scholarships ranging from $500 to $5,000, which can add up quickly. A well-crafted essay and strong academic record can significantly increase the chances of securing these awards.

In conclusion, scholarships, grants, and work-study programs are powerful tools for reducing debt dependency among college students. By covering tuition, providing stipends, and offering work opportunities, these resources can substantially lower the financial burden of higher education. Students who leverage these options effectively can graduate with minimal debt, setting themselves up for greater financial stability and flexibility in their post-college lives. The key lies in early planning, thorough research, and a proactive approach to securing these funds.

Is Mentor a Legitimate Student Loan Forgiveness Program? Unveiling the Truth

You may want to see also

Explore related products

![]()

Long-term financial consequences of student debt on career choices and lifestyle post-graduation

Student debt is a reality for the majority of college graduates, with recent statistics indicating that approximately 65% of students in the United States leave higher education with some form of debt. This financial burden, often amounting to tens of thousands of dollars, has far-reaching implications that extend well beyond the graduation ceremony. The weight of repayment shapes career trajectories and daily life in profound ways, influencing everything from job selection to long-term financial stability.

Consider the immediate post-graduation period, where the average debt holder faces monthly payments that can rival rent or even a mortgage. This financial strain often forces graduates into a survival mindset, prioritizing high-paying jobs over those aligned with their passions or long-term career goals. For instance, a recent art history graduate might shelve their dream of working in a museum to pursue a corporate role with a higher salary, simply to keep up with loan repayments. This compromise can lead to job dissatisfaction and a sense of being trapped in a career path that doesn't fulfill personal or professional aspirations.

The impact of student debt on lifestyle choices is equally significant. Young adults, typically in their 20s and 30s, find themselves delaying major life milestones. Homeownership, often a cornerstone of financial stability, becomes a distant dream for many. The Federal Reserve reports that student debt holders are less likely to own a home by their early 30s compared to their debt-free peers. Similarly, starting a family or even getting married can be postponed due to financial constraints. The pressure to maintain a certain income level to service debt can also lead to a more frugal lifestyle, limiting travel, leisure activities, and overall quality of life.

Furthermore, the long-term financial health of individuals with student debt is at risk. High debt-to-income ratios can negatively impact credit scores, making it harder to secure loans for future investments, such as starting a business or purchasing a car. The compounding effect of interest on unpaid debt can also lead to a cycle of financial stress, where individuals struggle to build wealth or save for retirement. For example, a graduate with $30,000 in debt at a 6% interest rate could end up paying over $10,000 in interest alone if they only make minimum payments over 10 years.

To mitigate these consequences, graduates should consider proactive strategies. Refinancing loans to secure lower interest rates, exploring income-driven repayment plans, and taking advantage of employer-based loan assistance programs can provide much-needed relief. Additionally, creating a detailed budget that prioritizes debt repayment while allowing for some lifestyle flexibility can help strike a balance between financial responsibility and personal well-being. By understanding the long-term implications and taking control of their financial situation, graduates can navigate the challenges of student debt and work towards a more secure future.

Exploring the Possibility of Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

Approximately 65% of college students in the United States graduate with student loan debt.

The average student loan debt for college graduates is around $28,000, though this varies by institution type and degree level.

Students from private colleges tend to have higher debt levels, with an average of $32,000, compared to $25,000 for public college graduates.