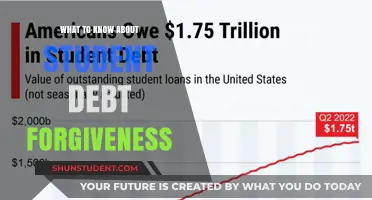

Yesterday, significant developments in student loan forgiveness captured national attention as the U.S. Department of Education announced the cancellation of billions of dollars in student debt for thousands of borrowers. The move comes as part of ongoing efforts to address the growing student loan crisis and provide relief to those burdened by educational debt. The forgiveness primarily targeted borrowers under specific programs, including those who attended predatory for-profit institutions and individuals eligible under the Public Service Loan Forgiveness (PSLF) program. This decision marks a pivotal moment for many, offering financial freedom and renewed hope, while also sparking debates about the broader implications for the future of student loan policy and economic equity.

Explore related products

What You'll Learn

![]()

Biden Administration's Loan Forgiveness Update

The Biden Administration recently announced a significant update to its student loan forgiveness program, targeting specific groups of borrowers and addressing long-standing issues within the system. This latest development comes as a relief to many, as it expands eligibility and streamlines the application process, ensuring that more individuals can benefit from debt cancellation.

Who Qualifies for Forgiveness?

In a strategic move, the administration has identified several categories of borrowers for immediate relief. Firstly, individuals with federal student loans who have been in repayment for at least 20 years and earn less than $125,000 annually (or $250,000 for married couples) will have their remaining debt forgiven. This measure aims to alleviate the burden on long-term borrowers struggling with persistent debt. Additionally, public servants, including teachers, nurses, and government employees, are now eligible for loan forgiveness after 10 years of service, regardless of their income level. This expansion recognizes the value of public service and encourages more professionals to pursue careers in these sectors.

A Simplified Application Process

One of the most notable changes is the introduction of a simplified application system. Borrowers no longer need to navigate complex paperwork and can now apply for forgiveness through a streamlined online platform. This digital transformation is expected to reduce processing times significantly, providing quicker relief to eligible individuals. The new system also automatically identifies and notifies borrowers who qualify for forgiveness, ensuring that those entitled to relief are not left behind due to administrative hurdles.

Impact and Future Prospects

This update is a strategic step towards addressing the growing student debt crisis, which has burdened millions of Americans. By targeting specific groups and simplifying the application process, the Biden Administration aims to provide tangible relief to those most in need. However, critics argue that more comprehensive reforms are necessary to tackle the root causes of rising tuition fees and increasing debt levels. As the debate continues, borrowers can now take advantage of these new provisions, potentially transforming their financial trajectories and opening doors to new opportunities.

For those eager to explore their eligibility, the official government websites provide detailed guidelines and application portals, ensuring a transparent and accessible process. This update serves as a reminder that student loan forgiveness is an evolving landscape, requiring borrowers to stay informed and proactive in managing their debt.

Understanding the Student Loan Forgiveness Plan: How It Worked

You may want to see also

Explore related products

![]()

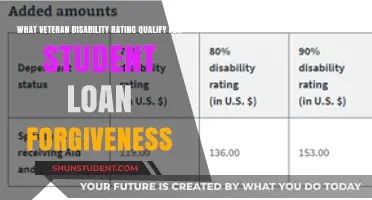

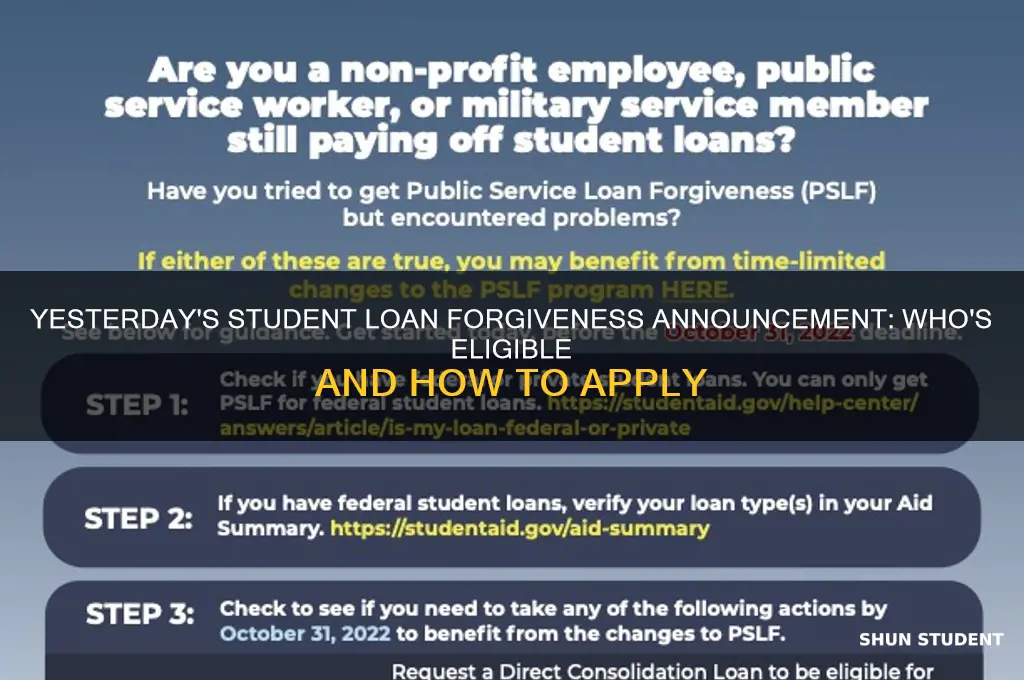

Eligibility Criteria for Recent Forgiveness

Recent student loan forgiveness initiatives have targeted specific groups, each with distinct eligibility criteria. For instance, the Public Service Loan Forgiveness (PSLF) program has seen updates that allow more borrowers to qualify, including those with previously ineligible repayment plans. To benefit, borrowers must have made 120 qualifying payments while working full-time for a government or nonprofit organization. A critical detail: payments made under the Federal Family Education Loan (FFEL) program now count if consolidated into a Direct Loan before October 31, 2022. This change alone has opened doors for thousands who were previously excluded.

Another key initiative is the forgiveness for borrowers who attended predatory for-profit institutions. The U.S. Department of Education has approved group discharges for students defrauded by schools like ITT Tech and Corinthian Colleges. Eligibility here hinges on proof of institutional misconduct, such as misleading job placement rates or accreditation claims. Borrowers need not apply individually; the Department identifies eligible groups based on investigations. However, those who attended closed schools may need to submit a borrower defense to repayment application if their institution isn’t on the approved list.

Income-driven repayment (IDR) plan adjustments have also led to unexpected forgiveness for some. The Department of Education conducted a one-time account adjustment in 2023, counting time spent in forbearance or economic hardship deferment toward IDR forgiveness. This means borrowers nearing the 20- or 25-year repayment mark could see balances wiped clean without further payments. For example, a borrower in repayment for 20 years under an IDR plan, with 3 years in forbearance, would now qualify for forgiveness as if they’d made 23 years of payments.

Lastly, the Fresh Start initiative targets defaulted borrowers, offering a pathway to forgiveness through rehabilitation. To qualify, borrowers must make nine on-time, voluntary payments within a 10-month window. These payments can be as low as $0 if the borrower’s income qualifies for a reduced payment under an IDR plan. Once rehabilitated, the default is removed from the borrower’s credit report, and they regain access to forgiveness programs like PSLF. This approach not only clears debt but also restores financial standing, making it a dual-benefit opportunity.

Understanding these criteria requires attention to detail and proactive steps. Borrowers should review their repayment histories, consolidate loans if necessary, and monitor Department of Education announcements for updates. For those unsure of eligibility, consulting a loan servicer or using the Federal Student Aid website’s tools can clarify next steps. Each program’s nuances mean that what works for one borrower may not apply to another, underscoring the importance of personalized assessment.

Hope Walz's Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

![]()

Impact on Borrower Balances

The recent wave of student loan forgiveness has left many borrowers wondering about the tangible effects on their financial lives. For those whose loans were discharged, the impact is immediate and profound: balances reduced to zero, monthly payments eliminated, and credit reports updated to reflect debt-free status. This isn’t just a theoretical win—it’s a life-altering shift that frees up income for savings, investments, or other expenses. For example, a borrower with $30,000 in forgiven debt could redirect $300–$400 monthly (the average payment) toward emergency funds, retirement accounts, or even homeownership.

However, the impact varies depending on the type of forgiveness granted. Public Service Loan Forgiveness (PSLF) recipients, for instance, often see their entire remaining balance wiped out after 10 years of qualifying payments. In contrast, income-driven repayment (IDR) forgiveness typically occurs after 20–25 years, but only a portion of the balance may be forgiven, with the remainder taxed as income. Borrowers must understand these nuances to plan effectively. For instance, someone expecting IDR forgiveness in 2024 should set aside funds to cover potential tax liabilities, which could reach thousands of dollars depending on their balance.

Another critical aspect is the psychological impact of reduced balances. Studies show that high student debt correlates with increased stress, delayed milestones, and reduced financial confidence. Forgiveness can reverse these effects, empowering borrowers to take control of their finances. A 30-year-old with $50,000 in forgiven debt might now feel comfortable starting a family or pursuing a career change without the burden of loan payments. Practical steps include updating budgets, recalculating net worth, and exploring new financial goals post-forgiveness.

Lastly, the ripple effects extend beyond individual borrowers. Communities benefit when residents have more disposable income, stimulating local economies through increased spending and investment. For example, a forgiven borrower might now afford a down payment on a home, boosting the housing market. Employers also benefit from a more financially stable workforce, potentially reducing turnover and increasing productivity. While the direct impact on borrower balances is clear, the broader economic and social implications underscore the transformative power of student loan forgiveness.

Future Student Loans: Will Forgiveness Programs Still Apply?

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness Changes

Recent updates to the Public Service Loan Forgiveness (PSLF) program have expanded eligibility, offering a lifeline to thousands of borrowers. One significant change allows payments made under any federal loan repayment plan to qualify, not just those under income-driven plans. This shift means borrowers who previously thought they were ineligible may now have a path to forgiveness. For instance, if you’ve been paying under a standard 10-year plan while working full-time in public service, those payments could now count toward the 120 required for forgiveness. This change alone could fast-track forgiveness for many, reducing the burden of long-term debt.

Another critical update is the temporary waiver extension, which expired on October 31, 2023, but still offers a grace period for borrowers to consolidate loans or certify employment. If you missed the deadline, don’t panic—the Department of Education has processed millions of waiver applications, and some borrowers are still being notified of adjustments. To maximize this opportunity, log into your Federal Student Aid account, consolidate any FFEL or Perkins Loans into a Direct Loan, and submit the PSLF form to certify your employment. Even if you’re unsure of eligibility, applying now ensures you’re considered for future changes.

The PSLF program now also includes a more flexible definition of "public service," benefiting borrowers in non-traditional roles. For example, contractors working full-time for a government agency or nonprofit may now qualify, provided they meet the hourly equivalent of full-time employment. This expansion is particularly impactful for sectors like healthcare and education, where contract work is common. To verify eligibility, use the PSLF Help Tool on the Federal Student Aid website, which guides you through employment certification and loan consolidation steps.

Lastly, the program has introduced an appeals process for denied applications, giving borrowers a second chance to prove eligibility. If your application was denied, review the reason carefully—common issues include incomplete employment certification or ineligible loan types. You can now file an appeal through the Federal Student Aid website, providing additional documentation to support your case. This process underscores the program’s commitment to fairness and accessibility, ensuring borrowers aren’t left behind due to technicalities. For those in public service, these changes represent a significant step toward financial freedom.

Discover If You Qualify for Student Loan Forgiveness: A Guide

You may want to see also

Explore related products

![]()

Reactions from Borrowers and Critics

The announcement of student loan forgiveness yesterday sparked a wave of emotions, from elation to skepticism, among borrowers and critics alike. For many, the news meant a significant reduction in financial burden, with some loans being entirely wiped clean. Borrowers in fields like education and nonprofit work, who qualified for Public Service Loan Forgiveness (PSLF), celebrated the immediate relief. One teacher, Sarah, shared, “After 10 years of payments, my $40,000 balance is gone. It feels like a new beginning.” This sentiment was echoed across social media, where hashtags like #DebtFree trended alongside stories of newfound financial freedom.

Critics, however, raised concerns about the long-term implications of such broad forgiveness. Economists argued that while targeted relief could stimulate the economy, widespread forgiveness might inflate costs in higher education. “If colleges know students will have debts forgiven, tuition could skyrocket,” warned financial analyst Mark Thompson. Others questioned the fairness of the policy, pointing out that taxpayers, many of whom never attended college, would indirectly fund the forgiveness. A common critique was the lack of safeguards to prevent future borrowing crises, such as capping interest rates or reforming loan servicing practices.

For borrowers, the practical steps post-forgiveness varied. Those with federal loans under $12,000 received automatic forgiveness, while others had to apply for PSLF or income-driven repayment plans. Financial advisors urged recipients to reinvest savings into emergency funds or retirement accounts. “This is a chance to break the cycle of debt,” said planner Emily Rodriguez. She recommended using forgiven amounts, say $200 monthly, to build a 6-month emergency fund or contribute to a Roth IRA. Critics countered that such advice assumes borrowers have disposable income, overlooking systemic issues like wage stagnation.

The generational divide in reactions was striking. Younger borrowers, often burdened with six-figure debts, hailed the move as transformative. “I can finally think about buying a house,” said 32-year-old engineer Alex. Older generations, however, were more divided. Some praised the relief as overdue, while others viewed it as an unfair advantage. “We paid our loans without help,” remarked retiree Linda, reflecting a sentiment of generational inequity. This tension highlights the broader debate over collective responsibility versus individual accountability in addressing student debt.

In the end, the reactions underscored the complexity of student loan forgiveness. While borrowers celebrated tangible relief, critics called for structural reforms to prevent future crises. The challenge now lies in balancing immediate aid with long-term solutions. Policymakers must address root causes, such as rising tuition costs and predatory lending practices, to ensure yesterday’s forgiveness isn’t tomorrow’s problem. For now, the impact remains deeply personal, a mix of hope, gratitude, and caution as borrowers navigate their newfound financial landscapes.

Can the Government Forgive Student Loans? Exploring the Possibilities and Challenges

You may want to see also

Frequently asked questions

As of yesterday, there was no widespread student loan forgiveness announcement. However, specific groups like borrowers under the Public Service Loan Forgiveness (PSLF) program or those with approved borrower defense claims may have received forgiveness.

No, federal student loans were not forgiven for all borrowers yesterday. Forgiveness is typically limited to specific programs or targeted relief efforts, not a blanket cancellation.

Private student loans are not eligible for federal forgiveness programs. Any forgiveness for private loans would be rare and dependent on individual lender policies or settlements, not a widespread event.