Navigating the path to securing $10,000 in student loan forgiveness requires a clear understanding of available programs and eligibility criteria. One of the most prominent options is the Public Service Loan Forgiveness (PSLF) program, which forgives remaining loan balances after 120 qualifying payments for those working full-time in eligible public service jobs. Additionally, the recent one-time student loan forgiveness initiative, tied to the COVID-19 pandemic, offers up to $10,000 in relief for eligible borrowers. Other avenues include income-driven repayment (IDR) plans, which can lead to forgiveness after 20–25 years of payments, and state-specific or employer-based forgiveness programs. To maximize your chances, ensure your loans are in the correct repayment plan, verify your employment for PSLF, and stay updated on federal and state policy changes.

| Characteristics | Values |

|---|---|

| Eligibility Criteria | Must have federal student loans and meet income requirements. |

| Income Threshold | Single filers: <$125,000; Married/Head of Household: <$250,000 (2020/2021). |

| Loan Types Covered | Federal student loans held by the U.S. Department of Education. |

| Private Loans Eligibility | Not eligible for forgiveness. |

| Forgiveness Amount | Up to $10,000 (or $20,000 for Pell Grant recipients). |

| Application Process | Automatic for borrowers with income info on file; others must apply online. |

| Tax Implications | Forgiveness is tax-free under the American Rescue Plan Act. |

| Deadline to Apply | December 31, 2023 (subject to change). |

| Impact on Credit Score | No negative impact on credit score. |

| Repayment Restart Date | October 1, 2023 (payments resume after forgiveness). |

| Additional Requirements | No additional requirements beyond income and loan type. |

| Status Updates | Check updates via the Federal Student Aid website or loan servicer. |

Explore related products

What You'll Learn

- Income-Driven Repayment Plans: Enroll in IDR plans to lower payments and qualify for forgiveness after 20-25 years

- Public Service Loan Forgiveness (PSLF): Work full-time in public service and make 120 qualifying payments for forgiveness

- Teacher Loan Forgiveness: Teach full-time in low-income schools for 5 consecutive years to get up to $17,500

- Loan Forgiveness for Nurses: Participate in nurse corps or NHSC programs for partial or full loan forgiveness

- Disability Discharge: Apply for Total and Permanent Disability (TPD) discharge to have federal loans forgiven

![]()

Income-Driven Repayment Plans: Enroll in IDR plans to lower payments and qualify for forgiveness after 20-25 years

Income-driven repayment (IDR) plans are a lifeline for borrowers seeking manageable student loan payments and eventual forgiveness. These plans cap your monthly payment at a percentage of your discretionary income, typically 10-20%, making them ideal for those with high debt relative to their earnings. For instance, a borrower earning $40,000 annually with $50,000 in loans might see payments drop from $500 to $200 per month under an IDR plan. This reduction not only eases financial strain but also sets the stage for forgiveness after 20-25 years of consistent payments.

Enrolling in an IDR plan requires selecting the right option from four available plans: Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR). Each plan has unique eligibility criteria and payment calculations. For example, REPAYE is open to all borrowers but includes spousal income in the payment calculation, while PAYE is limited to those with loans from specific years. Understanding these nuances is crucial to maximizing benefits. Annual recertification of income is mandatory, as payments adjust based on your earnings and family size.

While IDR plans offer significant advantages, they’re not without trade-offs. Lower monthly payments mean more interest accrues over time, potentially increasing the total amount forgiven. Additionally, forgiven amounts may be taxed as income, though current laws exempt borrowers from taxes on forgiven balances through 2025. To mitigate these drawbacks, consider making extra payments when financially feasible to reduce principal faster. Pairing IDR with Public Service Loan Forgiveness (PSLF) can also accelerate forgiveness for those in qualifying public service roles.

The path to $10k in student loan forgiveness through IDR requires patience and strategy. Start by consolidating loans into a Direct Loan if necessary, as only this type qualifies for IDR. Next, apply for an IDR plan via the Federal Student Aid website, providing accurate income documentation. Monitor your progress annually, ensuring payments are counted toward forgiveness. For borrowers nearing the 20-25 year mark, stay vigilant about policy changes and maintain records of all payments. With persistence, IDR can transform overwhelming debt into a manageable—and eventually forgivable—obligation.

Can Refinanced Student Loans Qualify for Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Work full-time in public service and make 120 qualifying payments for forgiveness

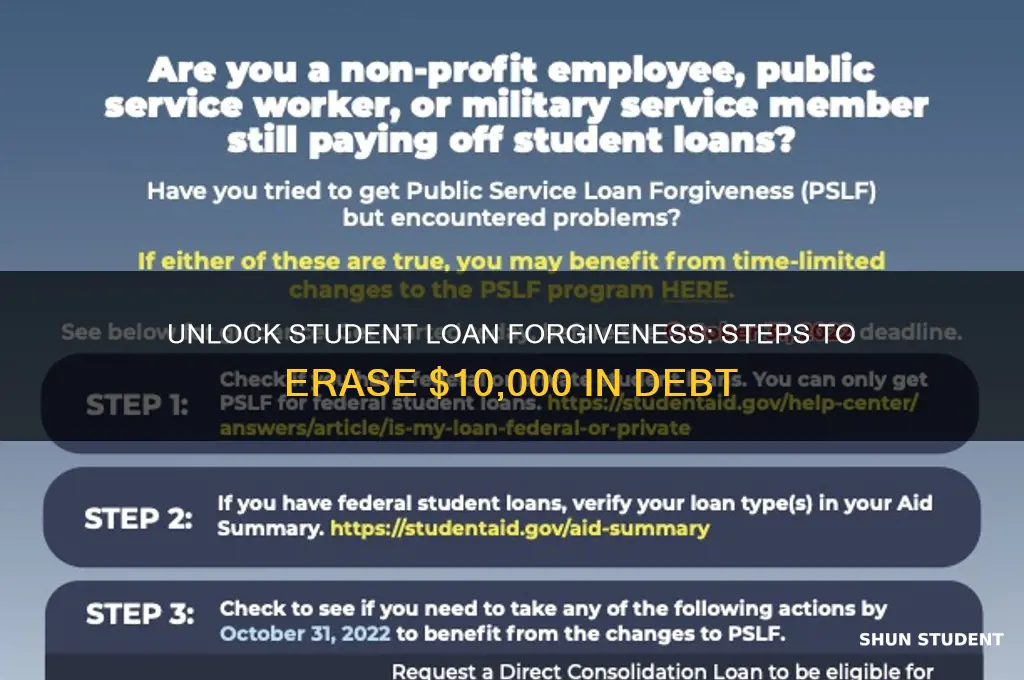

Public Service Loan Forgiveness (PSLF) offers a clear path to erasing federal student debt for those committed to a career in public service. Unlike broad forgiveness programs, PSLF requires a specific commitment: 120 qualifying monthly payments while working full-time for an eligible employer. This isn’t a quick fix—it’s a 10-year journey demanding consistent employment in sectors like government, education, healthcare, or nonprofits. The payoff? Tax-free forgiveness of your remaining loan balance after meeting the criteria.

To qualify, your employer must be a government organization at any level (federal, state, local, or tribal), a 501(c)(3) nonprofit, or a private nonprofit providing specific public services. Full-time employment typically means working at least 30 hours per week, though exceptions exist for certain roles. Payments must be made under an income-driven repayment plan to count toward the 120 required. This ensures your payments are manageable relative to your income, a critical detail often overlooked by borrowers.

One common pitfall is assuming all payments made while working in public service qualify. Only payments made after October 1, 2007, on Direct Loans while employed full-time in public service and enrolled in an income-driven plan count. Consolidating loans into a Direct Consolidation Loan can restart the payment count, so timing matters. Use the PSLF Help Tool on the Federal Student Aid website to confirm employer eligibility and track progress—a proactive step that prevents costly mistakes.

PSLF isn’t just about forgiveness; it’s a strategic choice aligning career goals with financial relief. For example, a teacher earning $45,000 annually with $50,000 in loans could pay as little as $200 monthly under an income-driven plan, making the 10-year commitment feasible. Compare this to standard repayment, where payments might exceed $500 monthly, and the advantage becomes clear. PSLF rewards long-term dedication to public service with a debt-free future, making it a powerful tool for those willing to commit.

Finally, stay vigilant about documentation. Submit the PSLF Employment Certification Form annually or when switching employers to ensure payments are correctly tracked. Missing this step can lead to disqualified payments, derailing progress. While PSLF demands patience and precision, its structured approach offers a guaranteed path to forgiveness for those who qualify. It’s not just a program—it’s a partnership between borrowers and public service, rewarding dedication with financial freedom.

Exploring the Financial Strategies Behind Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness: Teach full-time in low-income schools for 5 consecutive years to get up to $17,500

Teachers burdened by student debt have a powerful, if demanding, path to forgiveness: commit to five consecutive years of full-time teaching in a low-income school. This isn't a quick fix, but a strategic investment of time and energy that can erase up to $17,500 in federal student loans.

The program, known as Teacher Loan Forgiveness, is designed to incentivize educators to serve in communities with the greatest need. To qualify, you must teach full-time (as defined by your state) in a Title I school, where a significant percentage of students come from low-income families. This means long hours, potentially challenging classrooms, and a deep commitment to student success. But for those passionate about education and social impact, it's a chance to make a difference while addressing personal debt.

The forgiveness amount varies based on your subject area. Secondary school teachers in math, science, or special education can receive the maximum $17,500. Other eligible teachers, regardless of subject, can receive up to $5,000. This tiered system acknowledges the critical need for specialized educators in high-demand fields.

Before diving in, carefully research the program's requirements. Ensure your school qualifies as a Title I school and that your teaching position meets the full-time criteria. Keep meticulous records of your employment and loan payments throughout the five-year period. After completing your service, submit a Teacher Loan Forgiveness Application to your loan servicer. This process requires documentation from your school verifying your employment and the school's Title I status.

While demanding, Teacher Loan Forgiveness offers a substantial reward for those dedicated to both education and financial stability. It's a testament to the power of public service, allowing teachers to invest in the future of their students while securing their own.

Will Federal Student Loan Forgiveness Survive Legal Challenges and Political Debates?

You may want to see also

Explore related products

![]()

Loan Forgiveness for Nurses: Participate in nurse corps or NHSC programs for partial or full loan forgiveness

Nurses burdened by student loan debt have a powerful ally in the Nurse Corps Loan Repayment Program and the National Health Service Corps (NHSC) Loan Repayment Program. These federal initiatives offer substantial financial relief in exchange for service in underserved communities, providing a clear path to partial or full loan forgiveness.

Unlike generic loan forgiveness programs, these are specifically tailored to address the critical shortage of healthcare professionals in areas with limited access to care.

The Nurse Corps program, administered by the Health Resources and Services Administration (HRS), provides up to 85% loan repayment for registered nurses and advanced practice registered nurses who commit to working full-time for two years at an eligible Critical Shortage Facility (CSF). These facilities include hospitals, clinics, and community health centers located in Health Professional Shortage Areas (HPSAs) or Medically Underserved Areas (MUAs). Nurses can receive up to 60% of their qualifying loans repaid for the first two years of service, with an additional 25% for a third year.

The NHSC program operates similarly, offering loan repayment assistance to primary care providers, including nurse practitioners and certified nurse midwives, who serve in NHSC-approved sites located in HPSAs. Repayment amounts vary based on the HPSA score and the length of service commitment, ranging from $30,000 to $50,000 for two years of full-time service.

While both programs offer significant financial benefits, careful consideration is crucial. Applicants must be prepared to relocate to underserved areas, which may involve adjusting to a new community and potentially facing challenges associated with limited resources. Additionally, both programs have competitive application processes, requiring strong academic credentials, relevant clinical experience, and a demonstrated commitment to serving underserved populations.

A strategic approach is essential. Nurses should research eligible facilities in their desired geographic area, understand the specific needs of the community, and tailor their application to highlight their skills and experience relevant to addressing those needs.

Beyond the financial relief, participating in these programs offers nurses a unique opportunity to make a tangible impact on the health and well-being of underserved communities. By providing essential healthcare services in areas with limited access, nurses can experience the profound satisfaction of directly improving lives while simultaneously alleviating their student loan burden.

Am I Eligible for Federal Student Loan Forgiveness? A Guide

You may want to see also

Explore related products

![]()

Disability Discharge: Apply for Total and Permanent Disability (TPD) discharge to have federal loans forgiven

For borrowers facing the insurmountable challenge of repaying student loans due to severe health conditions, the Total and Permanent Disability (TPD) discharge offers a lifeline. This federal program forgives all eligible loans for individuals who can prove they are completely and permanently unable to work. Unlike other forgiveness options, TPD doesn’t require a minimum number of payments or years in service—it’s a direct path to relief for those whose disabilities have upended their financial futures.

To qualify, applicants must meet strict criteria. The Department of Education accepts disability documentation from three sources: the Social Security Administration (SSA), a physician’s certification, or the U.S. Department of Veterans Affairs (VA). If using SSA records, ensure you’ve received a notice of award for SSDI or SSI benefits with a review date at least five to seven years in the future. For physician certification, your doctor must complete a form confirming your inability to engage in substantial gainful activity due to a physical or mental impairment expected to last continuously, result in death, or has lasted for at least 60 months. Veterans must submit VA documentation of a 100% disability rating.

Once approved, TPD discharge initiates a three-year monitoring period during which borrowers must meet annual income requirements and avoid certain actions, such as taking out new federal loans or receiving new federal benefits based on earned income. Failure to comply can result in loan reinstatement. However, if borrowers navigate this period successfully, their loans are permanently forgiven, freeing them from the burden of debt.

Practical tips for a smooth application include keeping detailed medical records, ensuring all documentation is current, and double-checking that forms are completed accurately. Borrowers should also be aware of potential tax implications, as forgiven amounts may be considered taxable income unless they qualify for an exemption under the American Rescue Plan Act of 2021. For those whose disabilities have made loan repayment impossible, TPD discharge isn’t just a program—it’s a chance to reclaim financial stability and focus on health without the shadow of debt.

When Will Student Loan Forgiveness Checks Arrive? Key Dates Explained

You may want to see also

Frequently asked questions

The $10,000 student loan forgiveness is typically associated with the Public Service Loan Forgiveness (PSLF) program or targeted relief initiatives. Eligibility often requires working full-time for a qualifying public service employer (e.g., government, non-profit) and making 120 qualifying payments under an income-driven repayment plan. For targeted relief, income limits may apply (e.g., $125,000 for individuals or $250,000 for married couples).

For PSLF, submit the PSLF Form to certify your employment and payments. For targeted relief (e.g., one-time forgiveness initiatives), check the Department of Education’s website for application instructions, as these may be automatic or require a simple form. Ensure your loans are federal Direct Loans, as FFEL or Perkins Loans may need consolidation first.

No, federal student loan forgiveness programs, including the $10,000 relief, apply only to federal student loans (e.g., Direct Loans). Private loans are not eligible. If you have private loans, explore refinancing or repayment assistance programs offered by your lender or employer.