The topic of student loan forgiveness has been a significant point of discussion, particularly regarding the specific periods during which borrowers could apply for relief. Understanding the timeline for student loan forgiveness applications is crucial, as it directly impacts eligibility and the potential for debt relief. Different programs, such as the Public Service Loan Forgiveness (PSLF) or the recent one-time adjustment period for federal student loans, have had distinct application windows. For instance, the PSLF program allows borrowers to apply after making 120 qualifying payments, while the one-time adjustment period, which ended on December 31, 2023, offered a limited window for borrowers to consolidate or correct payment counts. Missing these deadlines can result in ineligibility, making it essential for borrowers to stay informed about the specific periods and requirements for each forgiveness program.

| Characteristics | Values |

|---|---|

| Application Period Start | October 2022 |

| Application Period End | December 31, 2023 (extended due to legal challenges) |

| Eligibility Criteria | Federal student loan borrowers under income-driven repayment plans |

| Income Limit | $125,000 for individuals, $250,000 for married couples (2020/2021 tax year) |

| Loan Types Covered | Federal Direct Loans, FFELP Loans (if consolidated into Direct Loans) |

| Forgiveness Amount | Up to $20,000 (Pell Grant recipients) or $10,000 (non-Pell Grant recipients) |

| Application Method | Online via Federal Student Aid website (studentaid.gov) |

| Documentation Required | FAFSA or tax return to verify income |

| Current Status | On hold due to legal challenges (as of November 2023) |

| Updates | Borrowers encouraged to apply before deadline for potential future relief |

Explore related products

What You'll Learn

- Application Window Dates: Specific start and end dates for submitting student loan forgiveness applications

- Eligibility Criteria: Requirements borrowers must meet to qualify for loan forgiveness programs

- Documentation Needed: List of documents required to complete the forgiveness application process

- Program Deadlines: Cutoff dates for different forgiveness programs (e.g., PSLF, IDR)

- Retroactive Forgiveness: Details on whether past payments count toward forgiveness eligibility

![]()

Application Window Dates: Specific start and end dates for submitting student loan forgiveness applications

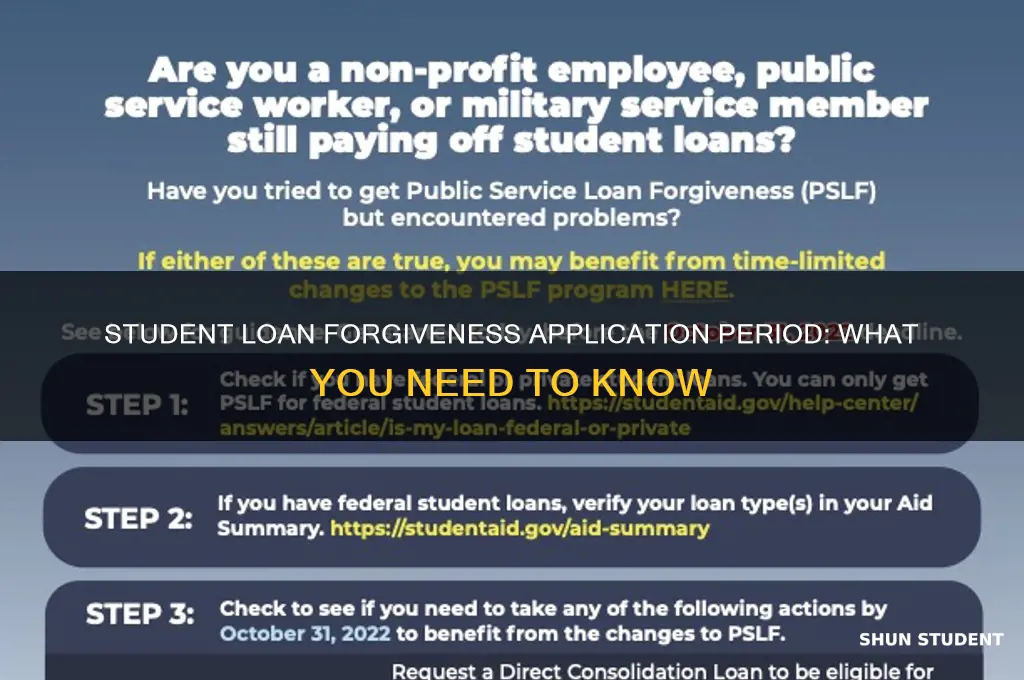

The application window for student loan forgiveness is a critical period that borrowers must navigate with precision. Missing this window can result in delays or even disqualification from relief programs. Historically, these windows have varied by program, with some lasting only a few months and others extending over several years. For instance, the Public Service Loan Forgiveness (PSLF) program has no fixed end date, but limited-time waivers—like the one offered in 2021—had strict deadlines, such as October 31, 2022, for certain actions. Understanding these timelines is essential for maximizing eligibility.

To illustrate, the Biden administration’s one-time student debt relief program in 2022 had a clear application window: October 17, 2022, to November 14, 2022, before legal challenges halted it. Borrowers who missed this window faced uncertainty, as extensions were not guaranteed. Similarly, income-driven repayment (IDR) forgiveness applications often require borrowers to track their qualifying payments, with forgiveness typically available after 20–25 years of payments. However, temporary adjustments, like the IDR Account Adjustment in 2023, allowed borrowers to retroactively count certain months toward forgiveness, but only if they acted by December 31, 2023.

When preparing to apply, borrowers should first verify their program’s specific window. For example, the Fresh Start initiative for defaulted loans had a deadline of December 31, 2023, to rehabilitate loans and regain eligibility for forgiveness. Practical tips include setting calendar reminders, gathering required documents early, and confirming eligibility criteria before the window opens. Additionally, monitoring official government websites or subscribing to updates from the Department of Education can provide real-time alerts on deadlines.

Comparatively, state-based forgiveness programs often have distinct timelines. For instance, California’s Teacher Loan Forgiveness Program accepts applications annually from March 1 to June 30, while New York’s GETAP program has rolling deadlines but prioritizes early submissions. Borrowers should also be cautious of scams that exploit application windows, offering expedited services for a fee. Always use official government portals and avoid sharing personal information with unverified sources.

In conclusion, application window dates are non-negotiable in the student loan forgiveness process. Borrowers must stay informed, act promptly, and leverage available resources to meet deadlines. Whether it’s a federal program with a fixed end date or a state initiative with recurring windows, understanding and adhering to these timelines is the linchpin of securing debt relief. Procrastination or misinformation can derail years of effort, making timely action the ultimate key to success.

Are Argosy Student Loans Forgiven? Understanding Your Options and Relief

You may want to see also

Explore related products

![]()

Eligibility Criteria: Requirements borrowers must meet to qualify for loan forgiveness programs

To qualify for student loan forgiveness programs, borrowers must navigate a complex web of eligibility criteria that vary by program. For instance, the Public Service Loan Forgiveness (PSLF) program requires 120 qualifying payments while working full-time for a government or nonprofit organization. Each payment must be made under an income-driven repayment plan, and the loan type must be a Direct Loan. This specificity underscores the importance of understanding program requirements before applying.

Consider the income-driven repayment (IDR) plans, which offer forgiveness after 20 or 25 years of qualifying payments, depending on the plan. Eligibility hinges on demonstrating partial financial hardship, calculated as the difference between your discretionary income and the federal poverty guideline for your family size. For example, a single borrower in 2023 with an adjusted gross income (AGI) of $40,000 would have a discretionary income of approximately $14,730 (AGI minus 150% of the poverty line). If their monthly payment under an IDR plan is lower than what they’d pay on a 10-year Standard Repayment Plan, they may qualify. This example highlights how income and family size directly impact eligibility.

Borrowers seeking forgiveness under the Temporary Expanded Public Service Loan Forgiveness (TEPSLF) must act swiftly, as this program has a limited application window. Introduced to address PSLF processing errors, TEPSLF allows previously ineligible payments (e.g., those made under graduated or extended repayment plans) to count toward forgiveness. However, borrowers must submit a PSLF form by October 31, 2023, to take advantage of this temporary expansion. This time-sensitive requirement emphasizes the need for proactive planning and documentation.

Lastly, the Borrower Defense to Repayment program offers forgiveness to borrowers who were misled by their college or university. Eligibility requires submitting evidence of the school’s misconduct, such as false job placement rates or accreditation claims. For instance, students defrauded by for-profit institutions like ITT Tech or Corinthian Colleges have successfully applied under this program. Practical tips include gathering enrollment agreements, marketing materials, and communication with the school to strengthen your case. This program’s eligibility hinges on proving institutional wrongdoing, not financial hardship, making it a distinct pathway to forgiveness.

In summary, eligibility for loan forgiveness programs demands meticulous attention to detail, from payment history and employment status to income calculations and documentation. Each program’s unique criteria require borrowers to tailor their approach, ensuring compliance with specific rules to maximize their chances of approval.

Discover Student Loans: Are They Eligible for Forgiveness?

You may want to see also

Explore related products

![]()

Documentation Needed: List of documents required to complete the forgiveness application process

The student loan forgiveness application process demands meticulous documentation to ensure eligibility and streamline approval. Missing or incomplete paperwork can delay or derail your application, so understanding the required documents is crucial. This guide outlines the essential documentation you'll need, categorized for clarity and ease of reference.

Proof of Employment and Service:

The cornerstone of most forgiveness programs is demonstrating qualifying employment. This typically involves providing documentation from your employer(s) verifying your job title, employment dates, and the nature of your work. For Public Service Loan Forgiveness (PSLF), this includes Form 120, the Employer Certification Form, submitted annually or when changing employers. Other programs, like Teacher Loan Forgiveness, may require specific forms or letters detailing your teaching assignment and school demographics.

Loan and Payment History:

A comprehensive record of your student loans is essential. This includes loan disbursement dates, loan types, and payment history. You can access this information through your loan servicer's website or by requesting a loan history statement. For income-driven repayment plans tied to forgiveness, documentation of your income and family size for each year of repayment may be required.

Tax Returns and Income Verification:

Tax returns are often used to verify income for income-driven repayment plans and certain forgiveness programs. Be prepared to submit copies of your federal tax returns, including all schedules and forms, for the relevant years. If you're self-employed or have complex income sources, additional documentation like profit and loss statements or 1099 forms may be necessary.

Additional Documentation:

Depending on the specific forgiveness program and your individual circumstances, you may need to provide additional documents. This could include:

- Disability Documentation: For Total and Permanent Disability Discharge, medical documentation from a qualified physician is required.

- School Closure Documentation: If your school closed while you were enrolled or shortly after, you'll need official documentation from the school or the Department of Education.

- Military Service Records: For military-related forgiveness programs, discharge papers and service records are typically required.

Organizing Your Documentation:

Gathering and organizing your documents beforehand is key to a smooth application process. Create a dedicated folder, either physical or digital, to store all relevant paperwork. Label documents clearly and keep copies for your records. Consider creating a spreadsheet to track submission deadlines and required documents for each program you're applying to.

Unemployed and Overwhelmed: A Guide to Student Loan Forgiveness

You may want to see also

Explore related products

![]()

Program Deadlines: Cutoff dates for different forgiveness programs (e.g., PSLF, IDR)

Navigating the labyrinth of student loan forgiveness programs requires a keen eye for deadlines, as each program operates on its own timeline. For instance, the Public Service Loan Forgiveness (PSLF) program mandates that borrowers make 120 qualifying payments while working full-time for an eligible employer. However, the clock doesn’t start ticking until your first qualifying payment is made. If you began repayments in January 2015, your earliest forgiveness eligibility would be January 2025, assuming no pauses or disqualifying changes. Missing this cutoff by even one payment could delay forgiveness by months or years.

In contrast, Income-Driven Repayment (IDR) plans like REPAYE or IBR offer forgiveness after 20 or 25 years of qualifying payments, depending on the plan and loan type. Here, the cutoff isn’t a single date but a cumulative period. For example, if you enrolled in an IDR plan in 2009, you could qualify for forgiveness as early as 2029 or 2034. However, switching plans or missing payments can reset this timeline. Borrowers must track their payment counts meticulously, as servicers don’t always do so accurately.

The Temporary Expanded Public Service Loan Forgiveness (TEPSLF) initiative, introduced in 2018, added complexity by offering a second chance to borrowers who previously made payments under non-qualifying plans. This program had a limited application window, which closed in October 2023. Borrowers who missed this cutoff lost the opportunity to have previously ineligible payments counted toward forgiveness, underscoring the importance of staying informed about program updates.

Practical tips for managing these deadlines include setting calendar reminders for key milestones, such as when you’ll reach 120 PSLF payments or your 20-year IDR mark. Annually submit the PSLF Employment Certification Form to ensure your employer and payments remain eligible. For IDR plans, recertify your income on time each year to avoid being kicked out of the program and losing progress. Finally, keep detailed records of all payments and correspondence with loan servicers—this documentation can be a lifeline if deadlines are disputed.

In summary, each forgiveness program’s cutoff dates demand proactive planning and vigilance. Whether it’s the 120-payment threshold for PSLF, the 20- or 25-year horizon for IDR, or limited-time initiatives like TEPSLF, missing a deadline can derail years of effort. By understanding these timelines and implementing practical strategies, borrowers can maximize their chances of achieving loan forgiveness.

Teacher Loan Forgiveness: A Step-by-Step Guide to Debt Relief

You may want to see also

Explore related products

![]()

Retroactive Forgiveness: Details on whether past payments count toward forgiveness eligibility

One critical question for borrowers seeking student loan forgiveness is whether their past payments, made before the introduction of new forgiveness programs, can be retroactively applied toward eligibility. This issue is particularly relevant for programs like Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, where the clock on qualifying payments is crucial. For instance, under PSLF, borrowers must make 120 qualifying payments while working full-time for an eligible employer. If past payments count, borrowers could significantly shorten their path to forgiveness.

To understand retroactive forgiveness, consider the IDR Account Adjustment, a temporary initiative launched in 2022. This measure allowed the Department of Education to retroactively count certain months of repayment history, including periods of deferment or forbearance, toward IDR and PSLF forgiveness. For example, if a borrower had been in forbearance for 12 months, those months could now count as qualifying payments. This adjustment was a game-changer for many, as it addressed historical servicing errors and provided a second chance for borrowers who had been misled or placed in the wrong repayment plans.

However, retroactive forgiveness is not automatic and often requires proactive steps from borrowers. For PSLF, borrowers must submit a PSLF Help Tool form to have their payment count updated, even if they believe their past payments should qualify. Similarly, for IDR plans, borrowers should ensure their loan servicers have accurate records of their repayment history. A practical tip: log into your Federal Student Aid account regularly to review your payment history and dispute any inaccuracies. This step is essential, as errors in payment counting can delay forgiveness by years.

Comparing PSLF and IDR, the treatment of past payments differs slightly. PSLF focuses on employment and payment type, while IDR emphasizes the total number of qualifying payments, regardless of employment. For example, a borrower who switched from a private sector job to a public service role could have their pre-employment payments counted under IDR but not PSLF. This distinction highlights the importance of understanding program-specific rules when pursuing retroactive forgiveness.

In conclusion, retroactive forgiveness can accelerate the path to student loan relief, but it requires vigilance and action from borrowers. By leveraging initiatives like the IDR Account Adjustment and ensuring accurate payment records, borrowers can maximize their eligibility for forgiveness. For those nearing the 120-payment threshold for PSLF or the 20- to 25-year mark for IDR, every past payment counts—literally. Take the time to review your history, submit necessary forms, and stay informed about policy updates to make the most of these opportunities.

Unlock $6 Billion Student Loan Forgiveness: Eligibility Guide

You may want to see also

Frequently asked questions

The PSLF program does not have a specific application deadline, but borrowers must make 120 qualifying payments while working full-time for an eligible employer. However, the limited PSLF waiver, which allowed past payments to count toward forgiveness regardless of loan type, ended on October 31, 2022.

The application period for the Biden administration’s one-time student debt relief plan (up to $20,000 in forgiveness) opened in October 2022 but was halted due to legal challenges. As of now, the program remains paused, and no new applications are being accepted.

The IDR account adjustment, which allows past periods of repayment to count toward forgiveness, is ongoing. Borrowers do not need to apply separately; adjustments are automatic. However, the deadline for any manual updates or corrections was April 30, 2023.