The interest rate on federal student loans is a critical factor for millions of borrowers, as it directly impacts the total cost of repayment over the life of the loan. Each year, these rates are set by the federal government based on the yield of the 10-year Treasury note auctioned in May, plus a fixed margin determined by the type of loan and the borrower’s education level. For the 2023-2024 academic year, rates were notably higher than in previous years due to rising inflation and Federal Reserve interest rate hikes, prompting concerns about affordability for current and future students. Understanding these rates and their annual adjustments is essential for borrowers to make informed decisions about financing their education and managing their debt effectively.

Explore related products

What You'll Learn

![]()

Historical Trends in Federal Student Loan Interest Rates

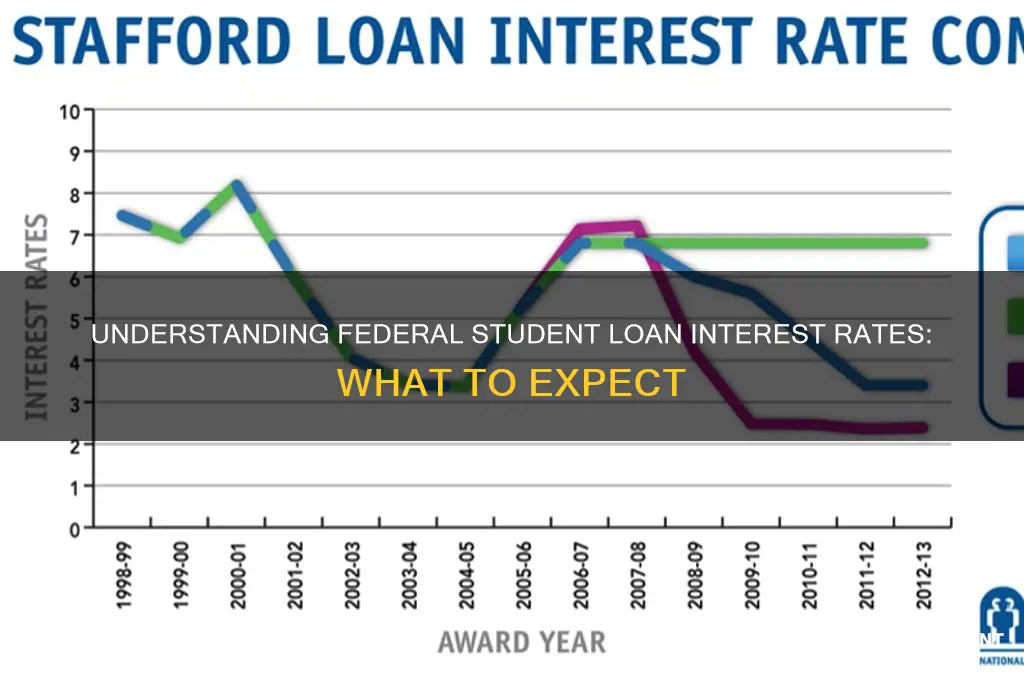

Federal student loan interest rates have fluctuated significantly over the past few decades, reflecting broader economic conditions and policy shifts. In the 1980s, rates soared to double digits, peaking at 18.5% in 1987, as the Federal Reserve combated inflation. These high rates placed immense financial strain on borrowers, often resulting in loan balances growing faster than they could be repaid. By contrast, the 2010s saw historically low rates, dipping to 3.4% for subsidized undergraduate loans in 2011-2012, due to recessionary pressures and legislative efforts to ease student debt burdens. This stark contrast highlights how macroeconomic forces and political decisions directly shape the cost of borrowing for education.

Analyzing the shift from fixed to variable rates provides further insight into historical trends. Prior to 1998, federal student loan rates were fixed but adjusted annually for new borrowers, creating uncertainty. The switch to long-term fixed rates in 1998 offered stability, but rates remained tied to market conditions. For instance, the 2007-2008 financial crisis prompted Congress to temporarily lower rates and cap them at 6.8% for certain loans. However, the Bipartisan Student Loan Certainty Act of 2013 introduced a new formula linking rates to 10-year Treasury notes, plus a margin, making them more responsive to economic fluctuations. This change underscores the trade-off between predictability and affordability in federal loan policy.

A comparative analysis of undergraduate and graduate loan rates reveals distinct trends. Since 2013, undergraduate loans have consistently carried lower rates than graduate and parent PLUS loans, reflecting a policy emphasis on supporting lower-income students. For example, in 2023, undergraduate rates were set at 5.5%, while graduate loans were at 7.05%, and PLUS loans at 8.05%. This tiered structure aims to balance accessibility with fiscal sustainability, though critics argue higher rates for advanced degrees disproportionately burden professionals in lower-paying fields, such as social work or education.

Practical takeaways from these trends can guide borrowers in navigating future rate changes. First, understanding the link between Treasury yields and loan rates allows students to anticipate increases during economic expansions. Second, locking in fixed rates through consolidation can provide long-term savings, especially when rates are low. Finally, staying informed about legislative proposals, such as interest rate caps or subsidies, can help borrowers advocate for policies that reduce their financial burden. By studying historical patterns, students can make more strategic decisions about when and how to borrow for their education.

Can My Daughter Get Student Loan Forgiveness? A Parent's Guide

You may want to see also

Explore related products

$6.99 $12.99

![]()

Factors Influencing Interest Rate Changes

Federal student loan interest rates are not set in stone; they fluctuate based on a complex interplay of economic and legislative factors. Understanding these influences can help borrowers anticipate changes and plan their finances accordingly. One of the primary drivers is the yield on the 10-year Treasury note, which serves as a benchmark for federal student loan rates. When the Treasury yield rises, student loan rates typically follow suit, and vice versa. For instance, in 2022, the 10-year Treasury yield increased significantly due to inflationary pressures, leading to higher interest rates on federal student loans for the 2022-2023 academic year.

Another critical factor is congressional legislation, which sets the formula for calculating federal student loan interest rates. The Bipartisan Student Loan Certainty Act of 2013 tied these rates to financial markets, adding a fixed margin based on the type of loan and the borrower’s education level. For example, undergraduate loans have a lower margin than graduate or parent PLUS loans. This legislative framework ensures that rates remain market-driven but also introduces a degree of predictability. Borrowers should monitor legislative proposals, as changes to this formula could directly impact future interest rates.

Economic conditions, particularly inflation and Federal Reserve policies, also play a significant role. When inflation rises, the Federal Reserve often increases interest rates to curb spending and stabilize the economy. This ripple effect extends to student loans, as higher borrowing costs reflect the broader financial environment. For instance, during periods of high inflation, such as in the early 2020s, student loan rates climbed to levels not seen in over a decade. Borrowers can mitigate the impact by locking in fixed rates when refinancing or consolidating loans during periods of lower rates.

Lastly, political priorities and public sentiment can influence interest rate changes. During election years or times of economic hardship, policymakers may propose temporary rate reductions or freezes to alleviate financial strain on borrowers. For example, in response to the COVID-19 pandemic, federal student loan interest rates were set to 0% for a prolonged period. Staying informed about policy debates and advocacy efforts can provide insights into potential rate adjustments, allowing borrowers to make strategic decisions about repayment and refinancing.

In summary, federal student loan interest rates are shaped by a combination of market forces, legislative decisions, economic conditions, and political priorities. By understanding these factors, borrowers can better navigate the complexities of student loan financing and prepare for future changes. Regularly reviewing Treasury yields, tracking legislative updates, and monitoring economic indicators can empower borrowers to make informed choices in managing their educational debt.

Understanding the Student Loan Forgiveness Plan: How It Worked

You may want to see also

Explore related products

![]()

Comparison with Private Loan Rates

Federal student loan interest rates are set by Congress and typically remain fixed for the life of the loan, offering borrowers predictability. As of the latest updates, undergraduate loans carry rates around 5.5%, while graduate and parent PLUS loans hover near 7%. These rates are often lower than private alternatives, which can fluctuate based on market conditions and individual creditworthiness. For instance, private loans may start at 4% for highly qualified borrowers but can soar above 12% for those with limited credit history. This disparity underscores the importance of comparing options before committing.

Consider a borrower with a $30,000 loan over 10 years. At a federal rate of 5.5%, monthly payments would be approximately $315, totaling $37,800 over the loan term. In contrast, a private loan at 8% would increase monthly payments to $338, totaling $40,560—a difference of nearly $2,800. Beyond cost, federal loans offer benefits like income-driven repayment plans, deferment, and forgiveness programs, which private lenders rarely match. These advantages make federal loans a safer bet for borrowers uncertain about their future financial stability.

However, private loans can be advantageous in specific scenarios. Borrowers with excellent credit or a cosigner might secure rates below federal levels, particularly for short-term loans. For example, a private loan at 4% would reduce the $30,000 loan’s total repayment to $34,200, saving over $3,600 compared to federal rates. Additionally, private lenders often provide variable-rate options, which can be lower initially but carry the risk of increasing over time. Borrowers should weigh these trade-offs carefully, considering both immediate savings and long-term flexibility.

To navigate this decision, start by checking your credit score and exploring private lender offers. Use online calculators to compare total repayment amounts under different scenarios. If your credit score is below 670, federal loans are likely the better choice due to their lower rates and borrower protections. Conversely, if you have a score above 750 and a stable income, private loans might offer significant savings. Always read the fine print—private loans often lack federal benefits like forbearance or forgiveness, which can be critical in financial hardship.

Ultimately, the choice between federal and private loans hinges on your financial profile and risk tolerance. Federal loans provide stability and safety nets, making them ideal for most borrowers. Private loans, while potentially cheaper for well-qualified individuals, require careful consideration of both immediate and future financial circumstances. By analyzing rates, terms, and benefits side by side, you can make an informed decision that aligns with your long-term goals.

When Will Student Loan Forgiveness Checks Arrive? Key Dates Explained

You may want to see also

Explore related products

![]()

Impact of Economic Conditions on Rates

Federal student loan interest rates are not set in stone; they fluctuate with the economic tides, much like a ship navigating stormy seas. The federal government, acting as the captain, adjusts these rates annually based on the 10-year Treasury note auction in May. This auction serves as a barometer for the broader economic climate, reflecting investor confidence, inflation expectations, and overall market sentiment. When the economy is booming, interest rates tend to rise as investors demand higher returns. Conversely, during economic downturns, rates often fall as investors seek safer havens for their money. For students and borrowers, this means that the cost of financing their education is directly tied to the health of the economy.

Consider the impact of inflation, a key economic indicator that influences interest rates. When inflation rises, the purchasing power of money decreases, prompting the Federal Reserve to raise interest rates to curb spending and stabilize prices. For federal student loans, this translates to higher borrowing costs. For instance, during periods of high inflation, a student borrowing $10,000 might face an interest rate of 6% or more, compared to 3-4% in a low-inflation environment. This difference can add thousands of dollars to the total repayment amount over the life of the loan. Borrowers should monitor inflation trends and consider accelerating payments during high-rate periods to minimize long-term costs.

Another critical factor is unemployment rates, which often move inversely with interest rates. During economic recessions, unemployment rises, and the Federal Reserve may lower interest rates to stimulate borrowing and spending. For federal student loans, this could mean lower rates for new borrowers, making education more affordable during tough economic times. However, existing borrowers with fixed-rate loans won’t see a change, while those with variable-rate loans may benefit from reduced monthly payments. Students planning to borrow should time their applications strategically, aiming for periods when economic conditions favor lower rates.

Economic growth also plays a pivotal role in shaping interest rates. A robust economy typically leads to higher interest rates as businesses and consumers compete for loans. For federal student loans, this means borrowers may face steeper costs during economic expansions. However, a strong economy often coincides with higher wages and better job prospects, which can offset the increased borrowing costs. Borrowers should weigh these factors and consider their post-graduation financial outlook when planning for student loans.

Finally, global economic conditions can indirectly influence federal student loan rates. International events, such as trade wars or geopolitical tensions, can affect U.S. Treasury yields, which in turn impact student loan rates. For example, during times of global uncertainty, investors may flock to U.S. Treasury bonds as a safe investment, driving down yields and potentially lowering student loan rates. Borrowers should stay informed about global economic trends and their potential ripple effects on domestic interest rates. By understanding these dynamics, students can make more informed decisions about when and how much to borrow.

Student Loan Forgiveness and 1099-C: What You Need to Know

You may want to see also

Explore related products

![]()

Future Predictions for Federal Loan Rates

Federal student loan interest rates have historically been tied to the 10-year Treasury note yield, with Congress setting fixed rates annually. For the 2023-2024 academic year, undergraduate loans are at 5.5%, graduate loans at 7.05%, and PLUS loans at 8.05%. These rates reflect a significant increase from the previous year, driven by the Federal Reserve’s aggressive rate hikes to combat inflation. Looking ahead, predicting future rates requires analyzing economic indicators, policy shifts, and historical trends.

Economic Indicators and Rate Projections

The Federal Reserve’s monetary policy remains the primary driver of federal loan rates. If inflation continues to moderate, the Fed may pause or reverse rate hikes, potentially stabilizing or lowering Treasury yields. Conversely, persistent inflation or economic uncertainty could keep yields elevated, pushing loan rates higher. Economists predict that if the 10-year Treasury yield remains around 4-5%, federal loan rates for 2024-2025 could hover between 5.5% and 7.5%, depending on the loan type. Borrowers should monitor inflation data, GDP growth, and unemployment rates as key indicators of future rate movements.

Policy Shifts and Legislative Proposals

Congressional action could reshape federal loan rates independently of economic trends. Proposals to cap interest rates or tie them to lower benchmarks, such as the 3-month Treasury bill, have gained traction among lawmakers. For instance, the *Lowering Rates for Student Loans Act* aims to reduce rates by 2-3 percentage points. If such legislation passes, borrowers could see significant savings. However, political gridlock and budget constraints may delay or derail these reforms. Students and families should stay informed about legislative developments and advocate for policies that align with their financial interests.

Practical Tips for Borrowers

Regardless of future rate predictions, borrowers can take proactive steps to manage their debt. Refinancing with private lenders may offer lower rates for those with strong credit, though this forfeits federal protections like income-driven repayment plans. Additionally, enrolling in autopay can secure a 0.25% interest rate reduction on federal loans. For new borrowers, comparing federal and private loan options remains critical, as federal loans offer fixed rates and flexible repayment terms. Finally, prioritizing high-interest debt and exploring loan forgiveness programs can mitigate the impact of rising rates.

Long-Term Outlook and Takeaway

While short-term rate predictions depend on economic and policy factors, the long-term trend suggests federal loan rates will remain volatile. Borrowers should prepare for potential increases by budgeting conservatively and exploring repayment strategies. Policymakers must address the root causes of rising education costs to prevent further strain on borrowers. Ultimately, staying informed and adaptable is key to navigating the evolving landscape of federal student loan rates.

Government Student Loan Forgiveness: What Borrowers Need to Know Now

You may want to see also

Frequently asked questions

The interest rates for federal student loans for the 2023-2024 academic year are 5.5% for undergraduate Direct Subsidized and Unsubsidized Loans, 7.05% for graduate/professional Unsubsidized Loans, and 8.05% for Direct PLUS Loans.

Federal student loan interest rates are determined by Congress and are based on the 10-year Treasury note auction held each May, plus an additional fixed percentage set by law. Rates are adjusted annually for new loans disbursed on or after July 1.

Yes, federal student loan interest rates are updated annually for new loans disbursed between July 1 and June 30 of the following year. Existing loans maintain their original fixed rate for the life of the loan.

No, interest rates vary by loan type. For example, undergraduate Direct Loans typically have lower rates than graduate/professional loans or PLUS Loans.

Interest rates on existing federal student loans are fixed and cannot be lowered unless through refinancing or consolidation. However, certain repayment plans or forgiveness programs (e.g., Public Service Loan Forgiveness) may reduce or eliminate interest over time.