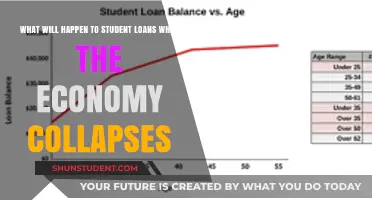

The issue of student debt has become a pressing concern for millions of individuals and families worldwide, as the cost of higher education continues to rise, leaving many graduates burdened with substantial financial obligations. With outstanding student loan balances reaching unprecedented levels, there is growing uncertainty about what the future holds for those struggling to repay their debts. As policymakers, educators, and borrowers grapple with this complex problem, questions arise regarding potential solutions, such as debt forgiveness, refinancing options, or reforms to the higher education system. The fate of student debt will not only impact individual financial well-being but also have far-reaching consequences for the economy, social mobility, and the overall accessibility of higher education.

Explore related products

What You'll Learn

- Potential Loan Forgiveness Programs: Government initiatives to cancel or reduce student debt for eligible borrowers

- Interest Rate Changes: Possible adjustments to student loan interest rates affecting repayment amounts

- Income-Driven Repayment Plans: Expanded options for lower monthly payments based on income levels

- Bankruptcy Discharge Reforms: Easier processes to discharge student debt through bankruptcy filings

- Private vs. Federal Debt: Differing outcomes for federally held loans versus private lenders' policies

![]()

Potential Loan Forgiveness Programs: Government initiatives to cancel or reduce student debt for eligible borrowers

The burden of student debt has reached unprecedented levels, with millions of borrowers struggling to repay their loans. In response, governments are exploring initiatives to cancel or reduce this debt for eligible individuals. These programs, often referred to as loan forgiveness, aim to alleviate financial strain and stimulate economic growth. One prominent example is the Public Service Loan Forgiveness (PSLF) program in the United States, which offers tax-free forgiveness after 10 years of qualifying payments for those working in public service roles. However, the complexity of eligibility criteria and administrative hurdles have limited its effectiveness, highlighting the need for more streamlined and inclusive solutions.

To address these challenges, policymakers are considering targeted forgiveness programs based on income, profession, or demographic factors. For instance, proposals to forgive up to $10,000 or $50,000 in student debt for borrowers earning below a certain threshold have gained traction. Such measures could disproportionately benefit low-income individuals and communities of color, who are often burdened with higher debt-to-income ratios. Additionally, sector-specific forgiveness programs, such as those for teachers, healthcare workers, or STEM professionals, could incentivize careers in critical fields while reducing financial barriers. These initiatives require careful design to ensure fairness and avoid unintended consequences, such as moral hazard or inflationary pressures.

Implementing loan forgiveness programs also raises questions about funding and long-term sustainability. One approach is to reallocate existing education budgets or impose targeted taxes on high-income earners or financial institutions. Another strategy involves tying forgiveness to economic contributions, such as requiring recipients to work in underserved areas or invest in local communities. For example, Canada’s Repayment Assistance Plan adjusts loan payments based on income and forgives remaining debt after a set period for those who cannot repay. Such models demonstrate how forgiveness can be structured to balance relief with fiscal responsibility.

Critics argue that broad-based forgiveness could be perceived as unfair to those who have already repaid their loans or chose not to pursue higher education. To mitigate this, programs could include partial forgiveness options or phased implementation. For instance, borrowers could receive incremental forgiveness for each year of qualifying employment or community service. Transparency in eligibility criteria and clear communication of benefits are essential to build public trust and ensure equitable access. Borrowers should also be educated on how to navigate these programs, as evidenced by the low uptake of existing initiatives due to lack of awareness or confusion.

Ultimately, the success of loan forgiveness programs hinges on their ability to address systemic issues in higher education financing. While immediate relief is crucial, sustainable solutions must also focus on reducing tuition costs, increasing grants, and improving financial literacy. Governments must strike a balance between providing relief to current borrowers and preventing future debt accumulation. By combining forgiveness with broader reforms, policymakers can create a more equitable and accessible education system, empowering individuals to pursue their aspirations without the shadow of overwhelming debt.

Did Obama Pass a Law to Forgive Student Loans?

You may want to see also

Explore related products

![]()

Interest Rate Changes: Possible adjustments to student loan interest rates affecting repayment amounts

Student loan interest rates are a pivotal factor in determining the total cost of education debt. Even minor fluctuations can significantly alter monthly payments and long-term financial obligations. For instance, a 1% increase on a $30,000 loan at a 5% interest rate over 10 years adds approximately $1,500 to the total repayment amount. Understanding how interest rates may change—whether due to federal policy, economic conditions, or refinancing options—is essential for borrowers to plan effectively.

Consider the historical context: federal student loan interest rates are tied to the 10-year Treasury note and adjusted annually. In 2023, undergraduate loans carried a 5.5% rate, while graduate loans were at 7.05%. However, these rates are not static. Economic shifts, such as inflation or recession, can prompt the Federal Reserve to adjust interest rates, indirectly impacting student loans. For example, a rising federal funds rate often leads to higher borrowing costs across the board, including for student loans. Borrowers must monitor these trends to anticipate changes in their repayment obligations.

Refinancing offers a proactive strategy to mitigate the impact of rising interest rates. Private lenders often provide lower rates to borrowers with strong credit histories or stable incomes. For example, refinancing a $40,000 loan from a 7% federal rate to a 4% private rate could save over $5,000 in interest payments over 10 years. However, this option comes with caveats: federal loans offer protections like income-driven repayment plans and loan forgiveness programs, which are forfeited upon refinancing. Borrowers must weigh the immediate savings against long-term benefits.

Income-driven repayment (IDR) plans provide another layer of protection against interest rate volatility. These plans cap monthly payments at a percentage of discretionary income, typically 10-20%, and forgive remaining balances after 20-25 years. For borrowers with high debt-to-income ratios, IDR plans can offset the burden of rising interest rates by ensuring payments remain manageable. For instance, a borrower earning $40,000 annually with $50,000 in debt at 6% interest might see payments reduced from $555 to $200 per month under an IDR plan.

In conclusion, interest rate changes demand proactive management of student debt. Borrowers should regularly review their loan terms, monitor economic indicators, and explore refinancing or IDR plans to minimize financial strain. By staying informed and strategic, individuals can navigate interest rate fluctuations with greater confidence and control over their repayment journey.

When Can You Apply for Student Loan Forgiveness: A Guide

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans: Expanded options for lower monthly payments based on income levels

The burden of student debt often feels insurmountable, especially for graduates entering the workforce with entry-level salaries. Income-Driven Repayment (IDR) plans offer a lifeline by capping monthly payments at a percentage of discretionary income, typically 10-20%. This means if you earn $30,000 annually, your payment might be as low as $150 per month, compared to the standard $300+ under a 10-year repayment plan.

Consider the case of Sarah, a social worker earning $45,000. Under a standard plan, her monthly payment would be around $500. With an IDR plan, it drops to $250, freeing up $250 monthly for essentials or savings. This flexibility is crucial for borrowers in low-paying but essential fields like education, healthcare, and social services.

However, IDR plans aren’t a one-size-fits-all solution. They extend repayment terms to 20-25 years, potentially increasing total interest paid. For instance, a $30,000 loan at 5% interest could accrue an additional $10,000 in interest over 25 years. Additionally, any remaining balance after the term is forgiven but may be taxed as income, creating a future financial obligation.

To maximize IDR benefits, borrowers should annually recertify their income to ensure payments reflect current earnings. For married borrowers, filing taxes separately can lower the income used to calculate payments, though this may have other tax implications. Tools like the Federal Student Aid Repayment Estimator can help model scenarios and choose the best plan.

In conclusion, IDR plans provide critical relief for borrowers with limited incomes, but they require careful planning. By understanding the trade-offs and leveraging available tools, borrowers can navigate student debt more sustainably, aligning payments with their financial reality.

Exploring Off-Campus Living: Where Do Johns Hopkins Students Reside?

You may want to see also

Explore related products

$12.95 $22.99

![]()

Bankruptcy Discharge Reforms: Easier processes to discharge student debt through bankruptcy filings

Student debt has become an insurmountable burden for millions, with many turning to bankruptcy as a last resort—only to find it largely ineffective. Current laws make discharging student loans through bankruptcy extremely difficult, requiring debtors to prove "undue hardship," a vague and rarely met standard. However, proposed reforms aim to streamline this process, offering a glimmer of hope for those trapped in financial despair. By redefining the criteria and simplifying the legal framework, these changes could provide a realistic path to relief for borrowers who have exhausted all other options.

Consider the case of a 35-year-old teacher with $120,000 in student loans, earning $45,000 annually. Despite consistent payments, the interest accrual outpaces her ability to reduce the principal. Under current bankruptcy laws, her chances of discharge are slim. Reforms could introduce a standardized "means test" similar to Chapter 7 filings, evaluating income, expenses, and loan repayment history to determine eligibility. This objective approach would replace the subjective "undue hardship" standard, making the process fairer and more predictable.

Critics argue that easing bankruptcy discharge for student debt could incentivize strategic defaults, burdening taxpayers who fund federal loan programs. However, data from countries with more flexible discharge policies, such as Canada, show that abuse is minimal. Instead, these reforms primarily benefit borrowers in genuine distress, such as those with disabilities, low-income earners, or victims of predatory lending practices. Implementing safeguards, like a mandatory waiting period or credit counseling, could further mitigate risks while ensuring relief for those who need it most.

For borrowers considering this route, practical steps include consulting a bankruptcy attorney specializing in student debt cases and gathering comprehensive financial documentation. While bankruptcy remains a serious decision with long-term credit implications, reforms could make it a viable option for those with no other way out. As legislative discussions progress, staying informed about policy changes and advocating for borrower-friendly measures will be crucial. Easier bankruptcy discharge processes could redefine the student debt crisis, offering not just financial relief but also a chance to rebuild lives.

Transferring from USAFA: Colleges Welcoming Academy Cadets for Completion

You may want to see also

Explore related products

![]()

Private vs. Federal Debt: Differing outcomes for federally held loans versus private lenders' policies

The fate of student debt hinges largely on whether it’s held by the federal government or private lenders. Federal loans, backed by the Department of Education, offer borrowers a suite of protections and repayment options that private loans rarely match. For instance, federal loan holders can enroll in income-driven repayment (IDR) plans, which cap monthly payments at a percentage of discretionary income, or pursue Public Service Loan Forgiveness (PSLF) after 10 years of qualifying payments. Private lenders, however, operate under no such obligations. Their terms are often rigid, with fewer forbearance options and higher interest rates, leaving borrowers with less flexibility during financial hardship.

Consider the impact of recent policy changes. Federal student loan borrowers have benefited from pauses in payments and interest accrual during the COVID-19 pandemic, with some even seeing partial debt cancellation. Private lenders, unbound by federal directives, offered little to no relief during this period. This disparity highlights a critical difference: federal loans are subject to legislative and executive actions, while private loans are governed by contracts that prioritize lender profitability. For borrowers, this means federal debt is more likely to be influenced by broader economic or political shifts, whereas private debt remains static and unforgiving.

For those strategizing debt repayment, understanding these differences is crucial. Federal loans allow for consolidation, which can simplify multiple payments into one and potentially lower interest rates. Private loans, on the other hand, often require refinancing, which may offer lower rates but typically requires a strong credit score or cosigner. Additionally, federal loans can be discharged in cases of borrower death or total disability, whereas private lenders may still pursue repayment from estates or cosigners. These nuances underscore the importance of prioritizing federal loan repayment strategies while aggressively negotiating terms with private lenders.

A practical tip for borrowers: if you hold both federal and private debt, allocate extra funds to pay down private loans first. Their higher interest rates and lack of protections make them the costlier burden. Meanwhile, take full advantage of federal programs like IDR or PSLF to manage federal debt sustainably. For example, a borrower with $30,000 in private loans at 8% interest and $50,000 in federal loans at 5% interest should focus on eliminating the private debt first, even if it means making minimum payments on the federal loans temporarily.

In conclusion, the distinction between private and federal student debt is not just semantic—it’s structural. Federal loans offer a safety net, with repayment plans and forgiveness programs designed to accommodate varying financial circumstances. Private loans, by contrast, are a high-stakes gamble, with fewer safeguards and greater financial risk. Borrowers must navigate these differences strategically, leveraging federal protections while minimizing the impact of private debt. As student debt policies continue to evolve, this awareness will remain a cornerstone of effective financial planning.

Understanding Student Loan Forgiveness: Payments Required for Debt Relief

You may want to see also

Frequently asked questions

As of now, there is no guarantee that all student debt will be forgiven entirely. While some targeted forgiveness programs exist, widespread cancellation depends on legislative and policy changes, which remain uncertain.

If you can’t afford payments, options include income-driven repayment plans, deferment, forbearance, or loan consolidation. In extreme cases, bankruptcy may discharge student debt, though it’s rare and requires proving undue hardship.

Certain professions, like public service, healthcare, or teaching, may qualify for loan forgiveness programs (e.g., Public Service Loan Forgiveness). However, eligibility criteria are strict, and not all borrowers will qualify.