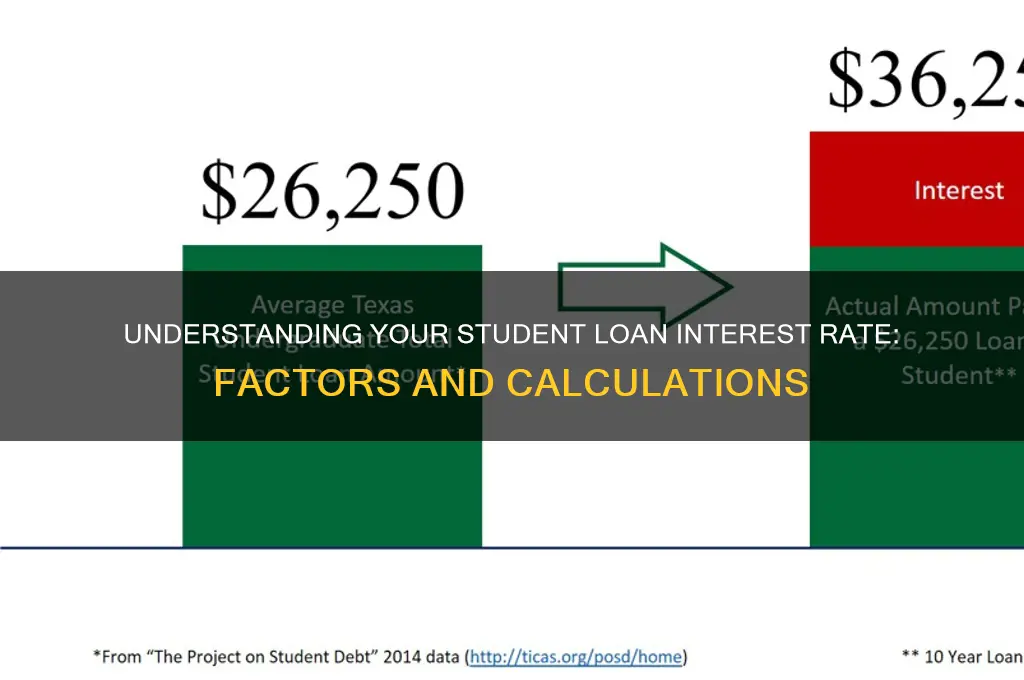

Understanding what your interest rate will be for a student loan is crucial, as it directly impacts the total cost of borrowing and your monthly payments. Interest rates on student loans can vary widely depending on factors such as the type of loan (federal or private), your credit score, the lender, and current market conditions. Federal student loans typically offer fixed rates set by the government, while private loans may have variable rates that fluctuate over time. Additionally, your financial situation, cosigner involvement, and repayment plan choice can influence the rate you qualify for. Researching and comparing options, as well as exploring potential discounts or incentives, can help you secure the most favorable interest rate for your student loan.

Explore related products

What You'll Learn

![]()

Federal vs. Private Rates

Federal student loan interest rates are set by Congress and remain fixed for the life of the loan, offering borrowers predictability. For the 2023-2024 academic year, undergraduate Direct Subsidized and Unsubsidized Loans carry a rate of 5.5%, while graduate Unsubsidized Loans are at 7.05%. These rates, though not the lowest historically, are generally lower than private loans and come with borrower protections like income-driven repayment plans and loan forgiveness options. For instance, if you borrow $30,000 at 5.5%, your monthly payment on a standard 10-year plan would be approximately $326, with total interest paid around $9,120.

Private student loan rates, in contrast, are determined by lenders and fluctuate based on market conditions and your creditworthiness. As of 2023, variable rates range from 4.99% to 14.99%, while fixed rates span from 5.29% to 14.99%. Unlike federal loans, these rates can change over time, especially with variable-rate loans. For example, a borrower with excellent credit might secure a 5.29% fixed rate, but someone with fair credit could face rates nearing 12%. A $30,000 loan at 12% would result in a monthly payment of $408 on a 10-year plan, with total interest exceeding $19,000—nearly double that of a federal loan.

One critical difference lies in repayment flexibility. Federal loans offer forbearance, deferment, and income-driven plans that cap payments at a percentage of your income. Private loans rarely provide such options, often requiring immediate repayment after graduation. For instance, if you lose your job, a federal loan might allow you to pause payments, while a private lender may demand continued repayment or charge fees for forbearance. This rigidity can strain borrowers during financial hardship.

When deciding between federal and private loans, consider your long-term financial stability and credit profile. Federal loans are ideal for borrowers with uncertain futures or low credit scores, as they don’t require a credit check (except for PLUS Loans). Private loans, however, might be suitable for borrowers with strong credit and stable incomes who can secure lower rates than federal options. For example, a medical student with a cosigner might obtain a 4.99% private rate, beating the 7.05% federal graduate rate. Always exhaust federal options before turning to private loans, as their protections are unparalleled.

In summary, federal student loans offer lower, fixed rates and robust borrower protections, making them a safer choice for most students. Private loans, while occasionally offering lower rates to well-qualified borrowers, come with higher risks and fewer repayment options. Before committing, use loan calculators to compare total costs and consider your financial resilience. Remember: federal loans are a safety net, while private loans are a gamble—choose wisely.

When Will Student Loan Forgiveness Take Effect: Key Dates Explained

You may want to see also

Explore related products

![]()

Credit Score Impact

Your credit score is a pivotal factor in determining the interest rate on your student loan. Lenders view it as a snapshot of your financial reliability, using it to assess the risk of lending to you. A higher credit score typically translates to lower interest rates because it signals to lenders that you’re a responsible borrower with a history of timely payments and managed debt. Conversely, a lower score may result in higher rates, as lenders compensate for the perceived risk by charging more. For example, a borrower with a credit score above 750 might secure a rate of 3-4%, while someone with a score below 650 could face rates exceeding 8%. This disparity underscores the direct correlation between credit health and borrowing costs.

To mitigate the impact of a lower credit score, consider taking proactive steps to improve it before applying for a student loan. Start by checking your credit report for inaccuracies, as errors can unfairly depress your score. Dispute any discrepancies with the credit bureaus and ensure all accounts are accurately reflected. Next, focus on reducing outstanding debt, particularly credit card balances, as high utilization rates can negatively affect your score. Aim to keep your credit utilization below 30% of your available limit. Additionally, establish a consistent payment history by setting up automatic payments for bills and loans. These actions, while requiring time, can incrementally boost your score and position you for more favorable loan terms.

Another strategy is to explore options that bypass the credit score requirement altogether. Federal student loans, for instance, do not consider credit history when determining eligibility or interest rates. These loans are based on financial need and have fixed rates set by the government, making them a viable option for borrowers with limited or poor credit. However, private student loans almost always factor in credit scores, so if you’re leaning toward this route, consider applying with a cosigner who has a strong credit profile. A cosigner can help you secure a lower interest rate, though it’s crucial to understand that they share equal responsibility for the loan, and missed payments will harm both credit scores.

Finally, it’s essential to recognize the long-term implications of your credit score on student loan interest rates. Even a slight difference in rates can result in thousands of dollars saved or spent over the life of the loan. For instance, a $30,000 loan at 5% interest would accrue approximately $8,000 in interest over 10 years, while the same loan at 7% would cost nearly $12,000 in interest. This highlights the importance of treating your credit score as a financial asset, one that requires ongoing maintenance and strategic management. By prioritizing credit health, you not only improve your chances of securing a lower interest rate but also set the foundation for better financial opportunities in the future.

Biden's Student Loan Forgiveness: Start Date and What You Need to Know

You may want to see also

Explore related products

![]()

Fixed vs. Variable Rates

Interest rates on student loans can significantly impact the total cost of your education, making the choice between fixed and variable rates a critical decision. Understanding the differences is essential for managing your financial future effectively.

The Stability of Fixed Rates

Fixed interest rates remain constant throughout the life of the loan, providing predictability in monthly payments. For example, if you secure a 5% fixed rate on a $30,000 loan, your interest payments will remain unchanged, regardless of market fluctuations. This stability is particularly beneficial for borrowers who prefer budgeting without surprises. However, fixed rates often start higher than variable rates, reflecting the lender’s assumption of long-term risk. If you prioritize consistency and are risk-averse, a fixed rate may align better with your financial goals.

The Fluidity of Variable Rates

Variable interest rates, on the other hand, fluctuate based on market indices, such as the London Interbank Offered Rate (LIBOR) or the Prime Rate. Initially, variable rates are typically lower than fixed rates, which can reduce short-term costs. For instance, a variable rate might start at 3% but could rise to 7% or higher if market conditions change. Borrowers who opt for variable rates often do so with the expectation of paying off the loan quickly or refinancing before rates climb. However, this strategy carries risk, especially in a rising interest rate environment.

Scenario Analysis: Fixed vs. Variable

Consider a 10-year repayment period for a $40,000 loan. With a fixed rate of 6%, your total interest paid would be approximately $11,700. If you choose a variable rate starting at 4% but increasing to 8% after 5 years, your total interest could rise to $14,000 or more. This example highlights how variable rates can lead to higher costs if market conditions shift unfavorably. Conversely, if rates remain low or decrease, variable rates could save you money.

Practical Tips for Decision-Making

To decide between fixed and variable rates, assess your financial stability, repayment timeline, and risk tolerance. If you have a steady income and plan to repay the loan within 5–7 years, a variable rate might be advantageous. However, if you’re uncertain about your future earnings or prefer long-term predictability, a fixed rate is safer. Additionally, monitor economic trends and consider refinancing options if you initially choose a variable rate. Tools like loan calculators can help model different scenarios to inform your decision.

Ultimately, the choice between fixed and variable rates depends on your personal financial situation and risk appetite. Fixed rates offer peace of mind, while variable rates provide initial savings with potential long-term risks. By carefully evaluating your circumstances and staying informed about market conditions, you can select the option that best supports your educational investment and financial well-being.

Can Classified Workers Qualify for Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Repayment Plan Effects

Interest rates on student loans are a critical factor in determining the overall cost of borrowing, but the repayment plan you choose can significantly alter how that interest accrues and impacts your financial future. Selecting a repayment plan isn’t just about monthly affordability; it’s about understanding how the structure of your payments interacts with your loan’s interest rate to shape your long-term debt burden. For instance, income-driven repayment plans may lower monthly payments but extend the loan term, allowing more interest to accrue over time. Conversely, standard 10-year plans result in higher monthly payments but minimize total interest paid. This interplay between repayment plan and interest rate demands careful consideration to align with your financial goals.

Consider the graduated repayment plan, which starts with lower payments that increase every two years. While this can provide immediate relief, the escalating payments are designed to pay off the loan within 10 years, similar to a standard plan. However, if your income doesn’t grow at the same rate as your payments, you may struggle later. Meanwhile, the interest continues to accrue based on the principal balance, which decreases more slowly than in a standard plan. This means you could end up paying more in interest over the life of the loan, even though the plan is structured for a 10-year payoff. Understanding this dynamic is crucial for borrowers who anticipate fluctuating income or career changes.

Income-driven repayment plans, such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE), cap monthly payments at a percentage of your discretionary income, typically 10-20%. These plans are particularly beneficial for borrowers with high debt relative to their income. However, the lower payments often don’t cover the full amount of interest accruing monthly, leading to *negative amortization*—where unpaid interest is added to the principal balance. Over time, this can cause the loan balance to grow, even as you make regular payments. For example, a borrower with $50,000 in loans at 5% interest might see their balance increase by $200 monthly if payments only cover $150 of the $210 in accruing interest. While loan forgiveness is available after 20-25 years, the forgiven amount may be taxable, creating a future financial liability.

Refinancing is another strategy to mitigate the effects of repayment plans on interest rates, but it’s not without risks. Private lenders may offer lower interest rates, especially to borrowers with strong credit histories or high incomes. However, refinancing federal loans means losing access to income-driven plans, forbearance, and forgiveness programs. For example, a borrower refinancing a 6% federal loan to a 4% private loan could save thousands in interest but would no longer qualify for Public Service Loan Forgiveness (PSLF). This trade-off requires a clear understanding of your career trajectory and financial stability. Borrowers in high-earning fields with secure employment may benefit from refinancing, while those in public service or uncertain careers should proceed cautiously.

Ultimately, the repayment plan you choose acts as a lever that amplifies or mitigates the impact of your student loan’s interest rate. To make an informed decision, calculate the total cost of each plan over its full term, not just the monthly payment. Tools like the Department of Education’s Loan Simulator can model different scenarios based on your loan details and income projections. Additionally, consider life events such as marriage, homeownership, or career changes that could affect your ability to manage payments. By treating your repayment plan as a strategic financial tool rather than a default option, you can minimize interest costs and align your student loan management with your broader financial objectives.

When Will Student Loan Payments Appear on My Credit Report?

You may want to see also

Explore related products

![]()

Current Market Trends

Interest rates on student loans are currently experiencing a period of fluctuation, driven by broader economic conditions and policy shifts. As of the latest data, federal student loan interest rates for the 2023-2024 academic year have risen to 5.5% for undergraduate loans, up from 4.99% the previous year. This increase reflects the Federal Reserve’s ongoing efforts to combat inflation through higher interest rates. For private student loans, rates vary widely—typically ranging from 4.5% to 12%—depending on the borrower’s credit score, loan term, and lender policies. Prospective borrowers should monitor these trends closely, as even small rate changes can significantly impact long-term repayment costs.

Analyzing the market reveals a growing preference for fixed-rate loans over variable-rate options. Fixed rates provide stability, locking in a consistent payment amount over the life of the loan, which is particularly appealing in an environment of rising rates. Variable rates, while initially lower, carry the risk of increasing with market fluctuations, potentially leading to higher monthly payments. For instance, a borrower with a $30,000 loan at a 5% fixed rate would pay approximately $318 monthly over 10 years, whereas a variable rate starting at 4% could climb to 7% or higher, increasing payments by $50 or more. Borrowers should weigh their financial stability and risk tolerance before choosing.

Another notable trend is the increasing availability of refinancing options as a strategy to secure lower interest rates. With federal student loan payments resuming after a pandemic-related pause, many borrowers are exploring refinancing to reduce their rates or adjust repayment terms. Private lenders like SoFi, Earnest, and Laurel Road are offering competitive rates as low as 4% for well-qualified borrowers. However, refinancing federal loans into private ones means losing access to income-driven repayment plans and loan forgiveness programs. Borrowers should carefully evaluate whether the potential savings outweigh these trade-offs.

Lastly, income-sharing agreements (ISAs) are emerging as an alternative to traditional student loans, particularly for students in high-earning fields like tech or healthcare. Under an ISA, borrowers agree to pay a percentage of their future income for a set period rather than a fixed monthly payment. While ISAs often lack interest rates entirely, they can be costlier if the borrower’s income exceeds expectations. For example, a borrower might agree to pay 10% of their income for 10 years, which could total more than a traditional loan if their salary grows rapidly. This trend highlights the evolving landscape of student financing and the importance of understanding all available options.

Who Will Guide Student Organizations in Cockreil's Absence?

You may want to see also

Frequently asked questions

Your student loan interest rate is typically determined by factors such as the type of loan (federal or private), your credit score (for private loans), current market conditions, and the loan term. Federal student loan rates are set by Congress and are generally fixed, while private loan rates can vary based on your financial profile.

For federal student loans, interest rates are usually fixed, meaning they remain the same throughout the loan term. However, private student loan rates can be fixed or variable. Variable rates may fluctuate based on market conditions, potentially increasing or decreasing your monthly payments over time.

Yes, you may qualify for a lower interest rate by improving your credit score (for private loans), choosing a shorter repayment term, or refinancing your loan. Additionally, federal loan borrowers may be eligible for interest rate reductions through programs like income-driven repayment plans or by setting up automatic payments.