Understanding your minimum payment on a student loan is crucial for managing your finances effectively. The minimum payment is the smallest amount you’re required to pay each month to keep your loan in good standing, but it’s important to note that paying only the minimum can extend the life of your loan and increase the total interest paid over time. Factors influencing your minimum payment include the type of loan (federal or private), the interest rate, the repayment plan you’ve chosen, and the total loan balance. Federal loans often offer income-driven repayment plans that adjust the minimum payment based on your earnings, while private loans typically have fixed or standard repayment terms. Calculating your minimum payment early helps you budget accordingly and explore strategies to pay off your debt faster, potentially saving you money in the long run.

Explore related products

What You'll Learn

![]()

Understanding Minimum Payment Calculation

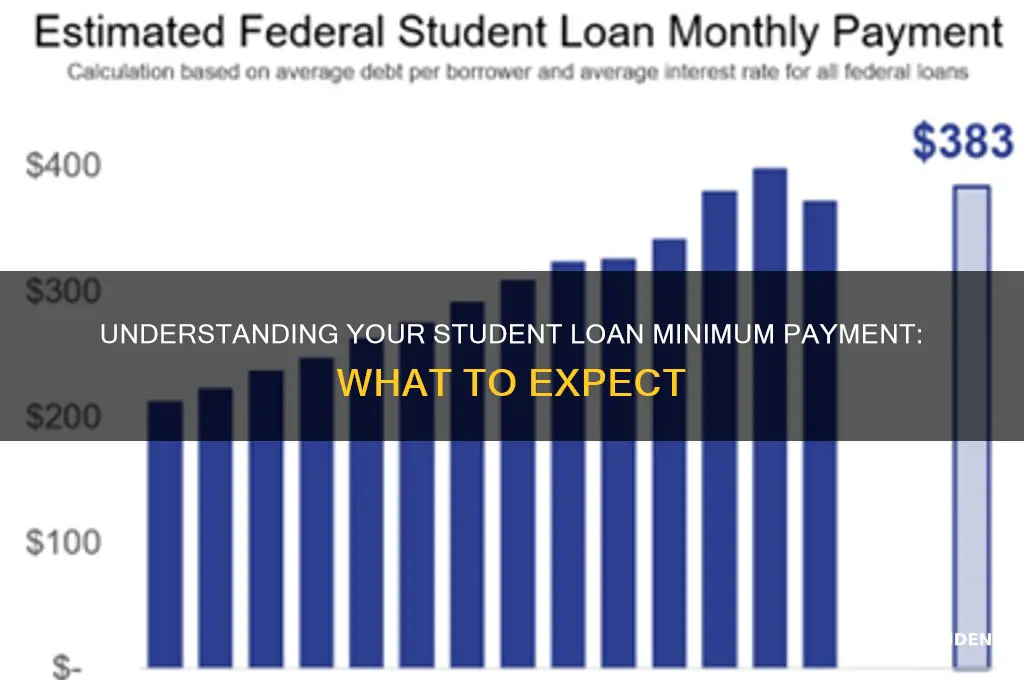

Minimum payments on student loans are not arbitrary; they are calculated using specific formulas that vary by loan type and lender. For federal student loans, the standard repayment plan typically sets the minimum payment at a fixed amount designed to ensure the loan is paid off within 10 years. This often results in a payment equal to $50 or the total interest accrued monthly, whichever is higher. Private student loans, however, may use different methods, such as a percentage of the principal balance or a flat percentage of the monthly income, depending on the lender’s terms. Understanding these formulas is the first step to managing your payments effectively.

For income-driven repayment plans, the calculation becomes more personalized. These plans, such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE), base the minimum payment on a percentage of your discretionary income, typically 10% to 20%. Discretionary income is defined as the amount of your income above 150% of the poverty line for your family size and state. For example, if your annual income is $40,000 and you’re single in a state with a poverty line of $13,590, your discretionary income would be $40,000 - $20,385 (150% of $13,590), or $19,615. A 10% payment on this amount would be approximately $163 per month. This method ensures payments remain affordable relative to your earnings.

One critical aspect often overlooked is how interest capitalization affects minimum payments. When unpaid interest is added to the principal balance—a process known as capitalization—it increases the total amount on which future interest accrues. For instance, if you have a $30,000 loan with a 5% interest rate and defer payments for a year, approximately $1,500 in interest will capitalize, bringing your balance to $31,500. This higher balance means your minimum payments will be recalculated based on the new total, potentially increasing your monthly obligation. Avoiding capitalization by paying at least the accruing interest during deferment periods can save you money in the long run.

To estimate your minimum payment accurately, use online calculators provided by lenders or the Department of Education. These tools require inputs such as your loan balance, interest rate, and repayment plan. For example, a $25,000 loan at 6% interest on a standard 10-year plan would result in a minimum payment of around $280 per month. However, switching to an income-driven plan could lower this amount significantly if your income is modest. Always verify the calculation with your loan servicer to ensure accuracy, as errors can lead to unexpected increases in payments or penalties.

Finally, consider strategies to manage minimum payments effectively. If you’re on a tight budget, prioritize paying at least the minimum to avoid delinquency or default. However, if possible, pay more than the minimum to reduce the principal faster and save on interest. For instance, adding $50 to a $200 monthly payment on a $20,000 loan at 7% interest could save you over $1,500 in interest and shorten the repayment term by more than a year. Additionally, explore options like loan consolidation or refinancing to lower your interest rate, which can reduce both your minimum payment and overall cost. Proactive management of your payments ensures financial stability and minimizes long-term debt burden.

Can You Buy Beer with a Student ID? Reddit's Take

You may want to see also

Explore related products

![]()

Impact of Interest Rates on Payments

Interest rates are the silent architects of your student loan repayment journey, shaping not just the total cost but also the monthly burden you’ll carry. A seemingly small difference in interest rates can balloon into thousands of dollars over the life of your loan. For instance, a $30,000 loan at 4% interest paid over 10 years results in total payments of $33,570, while the same loan at 7% jumps to $39,184. That’s a difference of $5,614, or roughly $47 per month—enough to cover a gym membership or a weekly grocery run. Understanding this dynamic is the first step in predicting your minimum payment and strategizing to minimize long-term costs.

Consider the mechanics: interest accrues daily on most student loans, meaning the longer you take to pay, the more interest compounds. For federal loans, the minimum payment is typically calculated as a percentage of your total debt, often starting at $50 per month. However, this baseline can increase if your interest accrual outpaces your payments, as is common with income-driven repayment plans. Private loans, on the other hand, often have fixed minimum payments based on a 10- or 15-year amortization schedule, but higher interest rates can inflate these amounts significantly. For example, a 5% rate might yield a $283 monthly payment on a $20,000 loan, while an 8% rate could push it to $328.

To mitigate the impact of interest rates, focus on two strategies: paying more than the minimum and refinancing when possible. Paying extra each month reduces the principal faster, shrinking the base on which interest is calculated. Even $20 extra per month can save hundreds in interest over time. Refinancing, meanwhile, allows you to replace your current loan with a new one at a lower rate, but proceed with caution—federal loans offer protections like income-driven repayment and forgiveness programs that private refinanced loans do not. Use online calculators to model scenarios and determine if refinancing is worth the trade-offs.

Finally, stay vigilant about rate fluctuations, especially if you have variable-rate loans. Federal student loans have fixed rates, but private loans may adjust periodically based on market conditions. A 2% increase in a variable rate can add $40–$50 to your monthly payment on a $20,000 loan. Monitor economic indicators like the Prime Rate or LIBOR, and consider switching to a fixed-rate loan if rates are expected to rise. Proactive management of interest rates isn’t just about lowering payments—it’s about reclaiming control over your financial future.

Amazon's Student Loan Forgiveness: Fact or Fiction? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plan Options

Income-driven repayment (IDR) plans adjust your monthly student loan payments based on your income and family size, offering a lifeline if standard payments are out of reach. These plans cap your payment at a percentage of your discretionary income—typically 10% to 20%, depending on the plan. For instance, if your discretionary income is $3,000 per month, your payment under the Revised Pay As You Earn (REPAYE) plan would be $300. This structure ensures payments remain manageable, even if your income fluctuates.

Among the four main IDR plans—Income-Based Repayment (IBR), Pay As You Earn (PAYE), REPAYE, and Income-Contingent Repayment (ICR)—each targets different borrower profiles. IBR and PAYE generally cap payments at 10% of discretionary income, while ICR sets payments at 20% or the amount of a fixed payment over 12 years, whichever is less. REPAYE, on the other hand, caps payments at 10% but includes a provision for unpaid interest to accrue, which can increase your balance over time. Understanding these nuances helps you choose the plan that aligns best with your financial situation.

Eligibility for IDR plans depends on factors like loan type and income level. Federal Direct Loans are typically eligible, but some older loans, like Federal Family Education Loans (FFEL), may require consolidation into a Direct Consolidation Loan to qualify. Additionally, your income must fall below a certain threshold relative to your family size and the federal poverty guideline. For example, if your income is 150% or less of the poverty line, your payment under IBR could be as low as $0, though interest still accrues.

One critical aspect of IDR plans is their forgiveness component. After 20 to 25 years of qualifying payments, any remaining balance is forgiven, though you may owe taxes on the forgiven amount. For instance, if you’re on the PAYE plan and make consistent payments for 20 years, the remaining balance is wiped clean. However, this timeline extends to 25 years for IBR and ICR plans. Strategically choosing an IDR plan can thus provide a long-term path to debt relief, especially if you work in a lower-paying field.

To enroll in an IDR plan, submit an application through your loan servicer, typically including income documentation like tax returns or pay stubs. Annual recertification is required to update your income and family size, ensuring your payment remains accurate. Missing recertification can result in a switch to a standard repayment plan, potentially increasing your monthly payment. Proactively managing your IDR plan—by staying on top of recertification deadlines and monitoring changes to federal regulations—maximizes its benefits and keeps your payments aligned with your financial reality.

Is Student Loan Forgiveness Still Available? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Standard vs. Graduated Repayment Plans

Choosing between a Standard Repayment Plan and a Graduated Repayment Plan hinges on your financial stability and long-term goals. The Standard Plan offers a fixed monthly payment over a 10-year term, ensuring you pay the least interest overall. For instance, if you owe $30,000 at 5% interest, your monthly payment would be approximately $318. This plan is ideal if you can afford consistent, higher payments and want to minimize interest costs. Conversely, the Graduated Plan starts with lower payments that increase every two years, typically over a 10-year term as well. Using the same $30,000 loan example, your initial payment might be around $175, rising to $350 by the final years. This plan suits borrowers expecting income growth, but it results in higher total interest paid—often thousands more than the Standard Plan.

Analyzing these plans reveals trade-offs between immediate affordability and long-term costs. The Graduated Plan’s lower starting payments provide breathing room for recent graduates or those in entry-level positions. However, the escalating payments can become burdensome if your income doesn’t rise as expected. For example, if your salary remains stagnant, a $350 payment in year 10 may feel as tight as a $318 payment would have under the Standard Plan. Conversely, the Standard Plan’s consistency makes budgeting easier but demands financial discipline from the outset. It’s a commitment to paying off debt aggressively, which may limit flexibility for other financial goals like saving or investing.

A persuasive argument for the Standard Plan is its efficiency in debt elimination. By paying more upfront, you reduce the principal balance faster, shrinking the interest accrual. This approach aligns with the principle of "pay yourself first" by freeing up cash flow sooner. On the other hand, the Graduated Plan can feel more forgiving in the short term, allowing you to allocate funds to emergencies or other priorities. However, this flexibility comes at a cost—literally. Over the life of the loan, you could pay 20-30% more in interest with the Graduated Plan compared to the Standard Plan.

Comparing these plans requires a realistic assessment of your financial trajectory. If you’re in a high-demand field with clear income growth prospects, the Graduated Plan might align with your career path. For instance, a software engineer starting at $60,000 annually with expected raises to $90,000 within five years could manage the escalating payments comfortably. In contrast, a teacher with a stable but modest salary increase might find the Standard Plan more sustainable, avoiding the stress of rising payments. A practical tip: Use loan calculators to model both scenarios based on your current and projected income, factoring in other expenses like rent, utilities, and savings goals.

Ultimately, the choice between Standard and Graduated Repayment Plans depends on your risk tolerance and financial priorities. If minimizing debt and saving on interest are paramount, the Standard Plan is the clear winner. If cash flow flexibility in the early years is critical, the Graduated Plan offers a viable alternative—but with a higher long-term price tag. Whichever you choose, monitor your progress and adjust as needed. For example, if you start on the Graduated Plan but secure a higher-paying job sooner than expected, consider switching to the Standard Plan to accelerate payoff. Both plans have their place, but the key is aligning your repayment strategy with your unique financial reality.

Abby Lee's Former Students: Will They Return for Season 8?

You may want to see also

Explore related products

![]()

Consequences of Paying Only the Minimum

Paying only the minimum on your student loan may seem like a manageable strategy, but it comes with significant long-term consequences. For instance, a $30,000 loan at a 6% interest rate with a $300 minimum payment could take over 15 years to repay, accruing more than $12,000 in interest. This example illustrates how minimum payments extend repayment timelines, increasing the total cost of the loan dramatically.

From an analytical perspective, the structure of minimum payments prioritizes interest over principal. Typically, a large portion of your early payments goes toward interest rather than reducing the loan balance. For example, on a $20,000 loan at 5%, the first year’s $200 monthly payments would allocate only $600 to principal reduction, while $1,000 goes to interest. This slow principal reduction means you remain in debt longer, limiting financial flexibility for other goals like saving or investing.

Persuasively, consider the opportunity cost of paying only the minimum. If you redirected even $50 extra per month toward a $25,000 loan at 7%, you could save over $3,000 in interest and shave off nearly 4 years of repayment. This extra payment strategy not only reduces the loan’s lifespan but also frees up funds sooner for emergencies, retirement, or other financial priorities.

Comparatively, paying the minimum on student loans versus other debts highlights the unique risks. Unlike credit cards, student loans often have fixed interest rates and longer terms, making them more costly over time. For example, a $10,000 credit card balance at 18% interest paid at the minimum would cost less in total interest than a $30,000 student loan at 6% due to the longer repayment period. This comparison underscores the importance of prioritizing student loan repayment beyond the minimum.

Practically, to mitigate these consequences, start by calculating your loan’s total cost using online calculators. Next, automate extra payments, even if small, to accelerate principal reduction. For federal loans, consider income-driven repayment plans if minimum payments are unmanageable, but be aware these plans often extend repayment terms further. Finally, explore refinancing options if you have a stable income and good credit, as lower interest rates can reduce overall costs. Taking proactive steps now can save thousands and provide financial freedom sooner.

India's Student Suicide Crisis: Urgent Need for Action and Solutions

You may want to see also

Frequently asked questions

The minimum payment on a student loan is typically calculated based on the loan type, balance, interest rate, and repayment plan. For federal loans, it’s often 10-15% of your discretionary income (income-driven plans) or a fixed amount designed to pay off the loan within a standard term (e.g., 10 years). Private loans may use a different formula, often a percentage of the total balance plus interest.

Yes, your minimum payment can change based on factors like changes in your income (for income-driven plans), interest rate adjustments (for variable-rate loans), or switching repayment plans. Recalculations may occur annually for income-driven plans or when you refinance or consolidate your loans.

Making only the minimum payment can extend the life of your loan, resulting in more interest paid over time. For example, on a $30,000 loan at 6% interest, paying only the minimum could double the total repayment amount. It’s generally advisable to pay more than the minimum if possible to save on interest and pay off the loan faster.