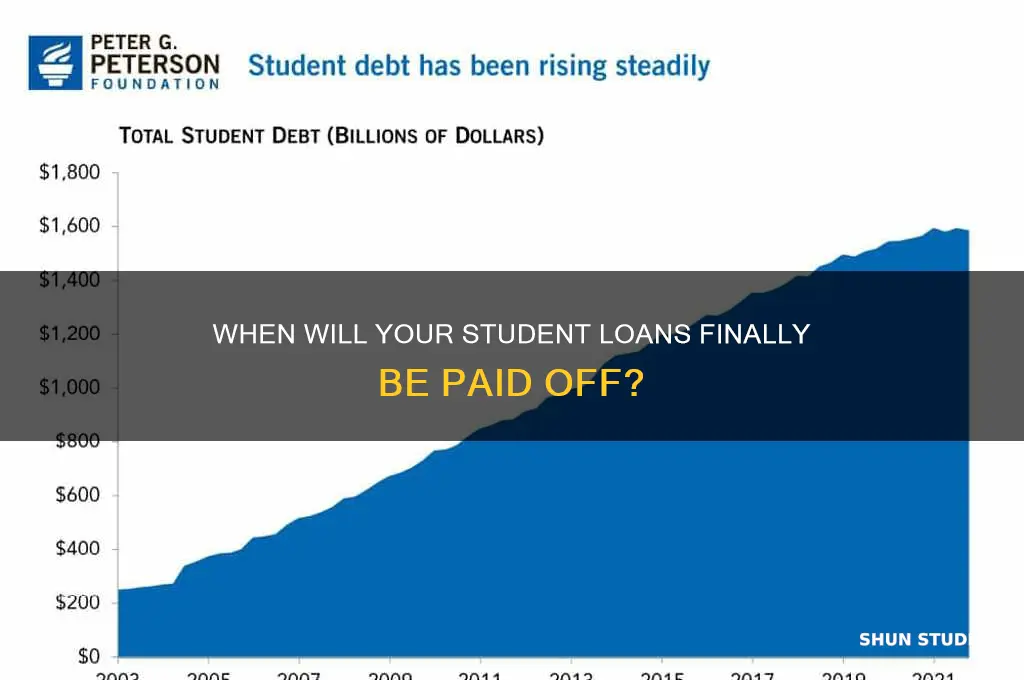

Managing student loan debt is a significant concern for many, and understanding when your loans will be fully paid off is crucial for financial planning. The timeline for paying off student loans depends on various factors, including the total loan amount, interest rates, repayment plan, and monthly payments. By using loan calculators or consulting with financial advisors, borrowers can estimate their payoff year and explore strategies to accelerate repayment, such as making extra payments or refinancing. Knowing when your student loans will be paid off allows you to set realistic financial goals and plan for future milestones like saving for a home or retirement.

| Characteristics | Values |

|---|---|

| Loan Amount | Varies based on individual borrowing (e.g., $30,000, $50,000, etc.) |

| Interest Rate | Typically 3.73% - 7.54% (for federal loans as of 2023-2024) |

| Repayment Plan | Standard (10 years), Graduated, Extended, Income-Driven, etc. |

| Monthly Payment | Calculated based on loan amount, interest rate, and repayment plan |

| Payoff Year | Depends on loan terms; e.g., 10 years for Standard Repayment |

| Early Repayment Options | Extra payments, lump-sum payments, refinancing |

| Loan Forgiveness Programs | Public Service Loan Forgiveness (PSLF), Income-Driven Forgiveness |

| Impact of Deferment/Forbearance | Pauses payments but may extend payoff year due to interest accrual |

| Refinancing Potential | Lower interest rates may shorten payoff timeline |

| Tax Implications | Interest may be tax-deductible; forgiven amounts may be taxable |

| Loan Servicer | Federal loans: FedLoan, MOHELA, etc.; Private loans: Varies |

| Latest Data Source | Federal Student Aid (FSA), Loan Simulator Tools, Lender Websites |

Explore related products

What You'll Learn

- Calculate Monthly Payments: Use loan calculators to estimate monthly payments based on interest rates and terms

- Extra Payments Impact: Learn how additional payments reduce interest and shorten payoff timelines significantly

- Income-Driven Repayment: Explore plans that adjust payments based on income and forgive balances after 20-25 years

- Loan Forgiveness Programs: Research Public Service Loan Forgiveness (PSLF) and other forgiveness options for eligible borrowers

- Refinancing Options: Consider refinancing to lower interest rates and accelerate payoff timelines effectively

![]()

Calculate Monthly Payments: Use loan calculators to estimate monthly payments based on interest rates and terms

Understanding when your student loans will be paid off starts with knowing how much you’ll pay each month. Loan calculators are your first line of defense against uncertainty, offering clarity by breaking down payments based on interest rates and loan terms. These tools are not just for financial experts; they’re designed for anyone looking to take control of their debt. By inputting your loan amount, interest rate, and repayment term, you can instantly see how much you’ll owe monthly and, more importantly, when you’ll be debt-free. This simple step transforms abstract financial data into actionable insights.

Let’s break it down step-by-step. First, gather your loan details: principal balance, annual interest rate, and loan term in years. Next, find a reliable loan calculator online—many are free and user-friendly. Input your data, and the calculator will generate your monthly payment, total interest paid, and payoff timeline. For example, a $30,000 loan at 6% interest over 10 years would result in a monthly payment of approximately $333. This not only helps you budget but also highlights how higher interest rates or longer terms can significantly increase total costs.

However, not all calculators are created equal. Some offer advanced features like extra payment scenarios, which show how additional monthly contributions can shorten your payoff timeline. For instance, adding $50 to that $333 payment could save you over $2,000 in interest and shave off nearly two years of repayment. Others allow you to compare different repayment plans, such as standard vs. income-driven options. These tools empower you to make informed decisions, ensuring you choose the strategy that aligns with your financial goals.

A word of caution: while calculators provide estimates, they assume consistent interest rates and payments. Variable rates or changes in income can alter your actual timeline. Additionally, some calculators may not account for loan-specific details like origination fees or prepayment penalties. Always double-check assumptions and consider consulting a financial advisor for personalized advice. Despite these limitations, loan calculators remain an indispensable resource for demystifying student loan repayment.

In conclusion, calculating monthly payments is more than a numbers game—it’s a strategic move toward financial freedom. By leveraging loan calculators, you gain transparency into your repayment journey, identify opportunities to save money, and set realistic expectations for when your loans will be paid off. Start today, and take the first step toward a debt-free future.

Candidates' Student Loan Forgiveness Plans: Which Loans Qualify?

You may want to see also

Explore related products

![]()

Extra Payments Impact: Learn how additional payments reduce interest and shorten payoff timelines significantly

Making extra payments on your student loans isn’t just about chipping away at the principal—it’s a strategic move that can save you thousands in interest and shave years off your repayment timeline. For example, if you have a $30,000 loan at 6% interest with a 10-year term, paying an extra $100 per month could reduce your payoff timeline by nearly 3 years and save over $3,000 in interest. This isn’t guesswork; it’s math. Every dollar you pay above the minimum goes directly toward the principal, reducing the balance on which interest accrues.

To maximize this impact, ensure your extra payments are applied correctly. Lenders often allocate payments to interest first, then principal. Contact your loan servicer to specify that additional funds should go toward the principal balance. If you’re juggling multiple loans, focus on the one with the highest interest rate—a strategy known as the avalanche method. This approach minimizes overall interest costs and accelerates debt elimination. For instance, paying off a $10,000 loan at 7% before a $15,000 loan at 5% will yield greater savings, even if the balance is smaller.

The psychological benefits of extra payments are equally compelling. Watching your loan balance drop faster provides tangible motivation, turning a daunting long-term obligation into a manageable, short-term goal. Tools like loan payoff calculators can help visualize progress. Input your loan details, add your extra payment amount, and see the projected payoff date shift dramatically. This clarity can transform student loan repayment from a passive burden into an active, rewarding strategy.

However, balance ambition with practicality. Before committing to extra payments, ensure you’ve built an emergency fund and addressed higher-interest debts like credit cards. Student loans often have lower rates than other debt, so prioritize accordingly. If you’re on an income-driven repayment plan, extra payments may not align with your long-term goals, as forgiveness programs typically require consistent, minimum payments over time. Always weigh your options and consult a financial advisor if needed.

In summary, extra payments aren’t just about paying more—they’re about paying smarter. By targeting the principal and reducing interest, you can transform your repayment timeline from a decade-long slog into a focused, achievable goal. Start small, stay consistent, and watch the years—and dollars—disappear.

Nurse Student Loan Forgiveness: How Effective Is It for Nurses?

You may want to see also

Explore related products

![]()

Income-Driven Repayment: Explore plans that adjust payments based on income and forgive balances after 20-25 years

For borrowers grappling with substantial student loan debt, income-driven repayment (IDR) plans offer a lifeline by aligning monthly payments with earnings. These plans recalibrate obligations annually based on adjusted gross income and family size, ensuring payments remain manageable—typically 10% to 20% of discretionary income. For instance, a single borrower earning $40,000 annually might pay as little as $200 monthly under the Revised Pay As You Earn (REPAYE) plan, compared to the standard $400+ payment on a $30,000 loan balance. This flexibility prevents default and provides breathing room for financial stability.

The true allure of IDR lies in its forgiveness component: after 20 to 25 years of consistent payments, any remaining balance is forgiven. For example, under the Income-Based Repayment (IBR) plan, borrowers with undergraduate loans see forgiveness after 20 years, while those with graduate loans or consolidated balances wait 25 years. However, this benefit comes with a tax caveat: forgiven amounts are typically treated as taxable income, potentially triggering a substantial bill. Proactive planning—such as saving in a tax-advantaged account or consulting a financial advisor—can mitigate this impact.

Choosing the right IDR plan requires careful analysis. REPAYE caps payments at 10% of discretionary income but includes spousal income in calculations, making it less ideal for high-earning dual-income households. Pay As You Earn (PAYE) limits payments to 10% and offers forgiveness after 20 years, but eligibility is restricted to borrowers who took out loans after 2007 and received a disbursement after 2011. Meanwhile, IBR adjusts payments to 10% or 15% of discretionary income based on loan type and date, offering a balance between affordability and forgiveness timelines.

Critics argue that IDR plans prolong debt and accrue interest, often leaving borrowers with larger balances over time. For instance, a borrower paying $200 monthly on a $30,000 loan at 5% interest might see their balance grow to $40,000 after 10 years. However, for those in low-paying professions or with high debt-to-income ratios, the trade-off is often worth it. To maximize benefits, borrowers should recertify income annually, explore Public Service Loan Forgiveness (PSLF) if eligible, and prioritize high-interest debt outside of IDR.

In essence, income-driven repayment plans transform student loans from a financial burden into a manageable obligation, offering a clear endpoint for debt-free living. While not without drawbacks, these plans provide a structured path to forgiveness, making them an indispensable tool for borrowers navigating the complexities of student loan repayment. By understanding plan nuances and planning strategically, borrowers can turn the question of "when will my loans be paid off?" into a solvable equation.

Paramedics and Student Loan Forgiveness: Eligibility and Options Explained

You may want to see also

Explore related products

![]()

Loan Forgiveness Programs: Research Public Service Loan Forgiveness (PSLF) and other forgiveness options for eligible borrowers

For borrowers drowning in student loan debt, the question of when their loans will be paid off can feel overwhelming. Loan forgiveness programs offer a glimmer of hope, potentially shaving years off repayment timelines. One of the most prominent programs is Public Service Loan Forgiveness (PSLF), which promises tax-free forgiveness after 120 qualifying payments for those working full-time in eligible public service jobs. However, navigating PSLF’s stringent requirements—such as having the right loan type (Direct Loans) and repayment plan (income-driven)—can be complex. Borrowers must also submit an Employment Certification Form annually and a final application after 120 payments to ensure compliance. While PSLF is a lifeline for qualifying individuals, it’s not the only option. Other forgiveness programs, like Teacher Loan Forgiveness and Income-Driven Repayment (IDR) forgiveness, cater to specific professions or income levels, each with unique eligibility criteria and timelines.

Consider Teacher Loan Forgiveness, for instance, which offers up to $17,500 in forgiveness for educators teaching full-time for five consecutive years in low-income schools. This program is ideal for teachers in high-need fields like math, science, or special education. However, it requires a different application process and documentation of employment, distinct from PSLF. Alternatively, IDR forgiveness applies to borrowers on income-driven plans like REPAYE or PAYE, offering forgiveness after 20–25 years of payments, depending on the plan. While this option doesn’t require public service, the forgiven amount may be taxed as income, unlike PSLF. Each program demands careful planning—borrowers must track payments, maintain eligibility, and stay informed about policy changes, such as the limited PSLF waiver that temporarily relaxed certain rules in 2022.

Persuasively, loan forgiveness programs aren’t just financial tools—they’re career incentives. PSLF, for example, encourages borrowers to pursue public service roles, from nonprofit work to government positions, by offering a clear path to debt freedom. Similarly, Teacher Loan Forgiveness addresses teacher shortages in underserved areas, rewarding those who commit to high-need schools. However, these programs aren’t without pitfalls. Missteps like missing a certification form or switching to an ineligible repayment plan can derail progress. Borrowers must proactively manage their loans, using resources like the Federal Student Aid website or consulting loan servicers to avoid costly errors.

Comparatively, while PSLF offers the fastest route to forgiveness (10 years), it’s the most rigid. IDR forgiveness, though slower, is more accessible but comes with potential tax liabilities. State-specific programs, like loan repayment assistance for healthcare workers in rural areas, provide additional avenues but require relocation or specialization. Borrowers should weigh their career goals, income stability, and tolerance for administrative tasks when choosing a program. For instance, a social worker in a nonprofit might prioritize PSLF, while a mid-career teacher could benefit from Teacher Loan Forgiveness.

Descriptively, imagine a borrower named Sarah, a public defender with $150,000 in Direct Loans. By enrolling in REPAYE and certifying her employment annually, she tracks her PSLF-eligible payments. After 120 months, her remaining balance—approximately $120,000—is forgiven tax-free. Contrast this with Mark, a high school teacher, who receives $17,500 in forgiveness after five years, reducing his $80,000 debt to $62,500. Both examples highlight how tailored strategies can accelerate debt repayment. To maximize these programs, borrowers should consolidate FFEL or Perkins Loans into Direct Loans, choose income-driven plans, and document every payment. The takeaway? Loan forgiveness isn’t automatic—it requires research, discipline, and strategic planning. But for eligible borrowers, it can transform the question from “When will my loans be paid off?” to “How soon can I be debt-free?”

New Student Loan Forgiveness Plan: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Refinancing Options: Consider refinancing to lower interest rates and accelerate payoff timelines effectively

Refinancing student loans can dramatically shift the year you’ll become debt-free by replacing high-interest debt with a more manageable rate. For instance, if you’re currently paying 7% on a $30,000 loan over 10 years, refinancing to 4% could save you over $3,000 in interest and shave off 1-2 years from your repayment timeline. This isn’t just about saving money—it’s about reclaiming time and financial freedom.

To start, assess your eligibility. Lenders typically look for a credit score of 650 or higher, a steady income, and a low debt-to-income ratio. If you’ve built credit since taking out your loans or have a co-signer with strong financials, you’re in a prime position. Use online calculators to compare your current terms with potential refinance offers, factoring in origination fees and repayment periods. For example, a 0.5% origination fee on a $40,000 loan is a small price if it secures a 2% rate reduction.

However, refinancing isn’t without risks. Federal loans come with protections like income-driven repayment plans and loan forgiveness programs, which you’ll forfeit if you refinance with a private lender. If you’re pursuing Public Service Loan Forgiveness or frequently rely on forbearance, refinancing might not be worth the trade-off. Weigh the long-term benefits of lower rates against the loss of federal safeguards before committing.

For those with multiple loans, refinancing can simplify payments by consolidating them into one. Imagine going from juggling four payments at varying rates to a single, lower-interest payment. This not only reduces mental clutter but also makes it easier to track progress toward your payoff year. Just ensure the new loan term doesn’t extend your repayment timeline unless it significantly lowers monthly payments.

Finally, shop around aggressively. Rates and terms vary widely among lenders, and pre-qualifying allows you to compare offers without impacting your credit score. Look for perks like autopay discounts or loyalty bonuses, which can further reduce costs. With strategic refinancing, you could move your projected payoff year from 2030 to 2027—a shift that transforms your financial future.

American Eagle and Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

Use your loan repayment plan details, including the interest rate, monthly payment amount, and remaining balance, to calculate the payoff timeline. Online loan calculators or your loan servicer can assist.

Yes, making extra payments reduces the principal balance faster, shortening the repayment timeline and potentially saving on interest.

Yes, income-driven plans often extend the repayment term (up to 20–25 years) but may offer lower monthly payments and potential loan forgiveness after the term ends.

Refinancing can lower your interest rate or adjust the repayment term, which may shorten or extend the payoff timeline depending on the new terms.

Yes, missed payments can increase the total interest accrued and extend the repayment timeline, delaying the year your loans will be paid off.