Navigating the complexities of student loan forgiveness can be overwhelming, leaving many borrowers wondering when they can expect their debt to be forgiven. The timeline for student loan forgiveness varies depending on the type of loan, repayment plan, and forgiveness program you qualify for. For instance, Public Service Loan Forgiveness (PSLF) typically requires 120 qualifying payments, which can take around 10 years, while income-driven repayment (IDR) plans may offer forgiveness after 20-25 years of payments. Additionally, recent policy changes and temporary relief measures, such as those introduced during the COVID-19 pandemic, can impact forgiveness timelines. Understanding your specific loan terms, staying informed about updates, and proactively managing your repayment strategy are crucial steps in determining when you can expect your student loan to be forgiven.

Explore related products

What You'll Learn

![]()

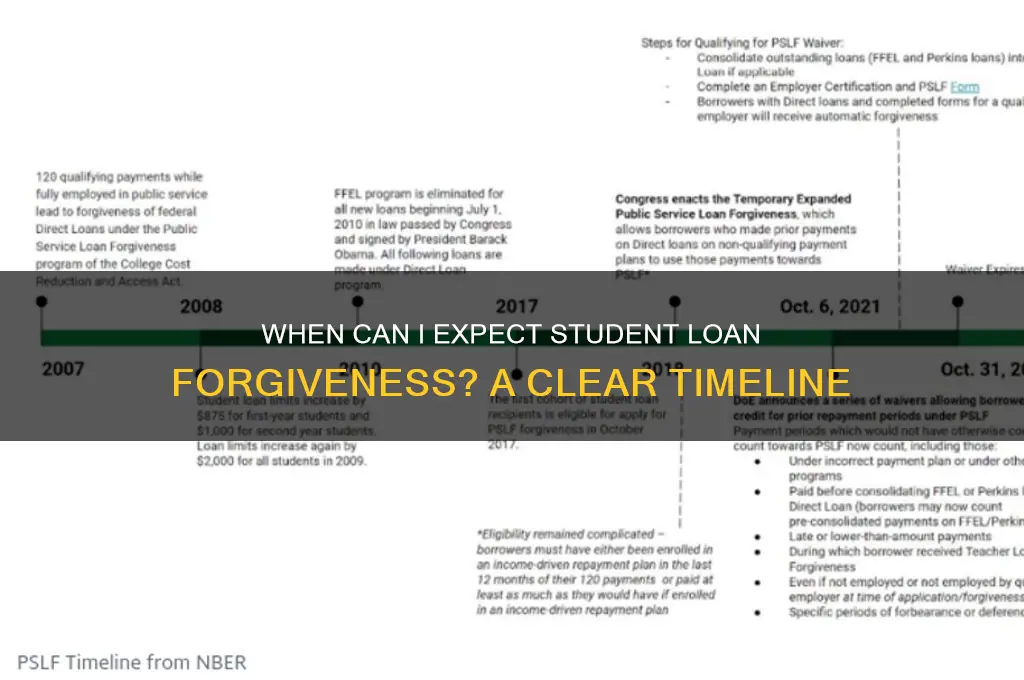

Public Service Loan Forgiveness (PSLF) Requirements

Public Service Loan Forgiveness (PSLF) offers a pathway to debt relief for those committed to a career in public service, but it’s not automatic. To qualify, you must meet specific requirements that go beyond simply working in the public sector. First, your employment must be with a qualifying employer, such as a government organization, 501(c)(3) nonprofit, or other eligible entities. Second, you need the right type of federal student loans—Direct Loans are eligible, while Federal Family Education Loans (FFEL) and Perkins Loans are not, unless consolidated into a Direct Loan. These foundational criteria are non-negotiable, but they’re just the starting point.

Once you’ve confirmed eligibility, the clock begins ticking on your 120 qualifying payments. These payments must be made under an income-driven repayment plan or the standard 10-year plan, and they must be made in full, on time, and while employed full-time by a qualifying employer. Partial payments or those made during periods of deferment or forbearance do not count. Tracking these payments is critical, as errors in payment counts are common. The Department of Education’s PSLF Help Tool can assist in determining employer eligibility and consolidating loans if necessary.

A common pitfall is assuming all public service jobs qualify. For instance, working for a nonprofit hospital might seem like a sure bet, but if the hospital is not a 501(c)(3) organization, it may not meet PSLF criteria. Similarly, political subdivisions of state governments, such as public schools or fire departments, are eligible, but private contractors working for these entities are not. Certifying your employment annually through the PSLF Employment Certification Form helps ensure you’re on track and identifies issues early.

Finally, patience and persistence are key. The PSLF program requires a decade of commitment, and the forgiveness process itself can be bureaucratic. After making 120 qualifying payments, you must submit a PSLF application to receive forgiveness. Approval rates have historically been low due to administrative errors, but recent reforms aim to streamline the process. Staying informed about policy changes and maintaining meticulous records of your payments and employment will maximize your chances of success. PSLF isn’t a quick fix, but for those dedicated to public service, it can be a life-changing opportunity to eliminate student debt.

Navigating Student Loan Forgiveness: A Step-by-Step Complaint Filing Guide

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plan Forgiveness Timeline

Income-driven repayment (IDR) plans offer a lifeline to borrowers by capping monthly payments at a percentage of discretionary income, but the real prize is the promise of loan forgiveness after 20 or 25 years of qualifying payments. However, the timeline isn’t as straightforward as it seems. For instance, if you started repaying under the Revised Pay As You Earn (REPAYE) plan in 2015 at age 25, earning $40,000 annually with a $30,000 loan balance, your forgiveness clock would tick toward 2025—but only if every payment qualifies. Miss a recertification deadline, switch plans, or pause payments, and the clock resets or slows. Understanding this timeline requires precision, as even small missteps can delay forgiveness by years.

To navigate this timeline effectively, borrowers must first choose the right IDR plan. For example, REPAYE forgives after 20 years for undergraduate loans, while Income-Based Repayment (IBR) takes 25 years. If you’re 30 with $50,000 in undergraduate debt and opt for REPAYE, your forgiveness year would be 2038—assuming consistent payments and annual recertification of income. However, if you switch to IBR mid-stream, the timeline extends to 2050. Practical tip: Use the Federal Student Aid Loan Simulator to model scenarios and lock in the plan that aligns with your financial goals.

A critical but often overlooked aspect is the tax implication of forgiveness. Under current law, forgiven amounts are treated as taxable income, which could result in a hefty bill. For instance, if $30,000 is forgiven in 2038, it could push you into a higher tax bracket that year. To mitigate this, consider setting aside 10–15% of your annual savings in a dedicated "forgiveness tax fund." Additionally, stay updated on legislative changes—proposals like the Tax-Free Student Loan Forgiveness Act could eliminate this tax burden, but they’re not yet law.

Finally, borrowers must proactively manage their IDR journey. Recertify income annually without fail; missing this deadline can kick you off the plan and reset the forgiveness clock. For example, a borrower earning $55,000 with $40,000 in graduate loans under Pay As You Earn (PAYE) could lose 12 qualifying months by failing to recertify. Keep detailed records of payments and correspondence with servicers, and consider enrolling in autopay to avoid missed payments. While the path to IDR forgiveness is long, disciplined adherence to these steps can turn a 20- or 25-year timeline into a manageable—and ultimately rewarding—journey.

Canada Student Loan Forgiveness: Years of Residency Requirements Explained

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness Eligibility Criteria

Teachers seeking student loan forgiveness must navigate specific eligibility criteria to qualify for the Teacher Loan Forgiveness Program. This federal initiative offers up to $17,500 in loan forgiveness for eligible educators who teach full-time for five consecutive years in low-income schools. The program is designed to incentivize teaching in underserved communities, but not all teachers or schools qualify. Understanding the criteria is crucial to determining when and if you can expect your student loan to be forgiven.

Eligibility Requirements: A Breakdown

To qualify, teachers must meet three primary criteria. First, you must teach full-time for five complete and consecutive academic years in a designated low-income school or educational service agency. Second, your teaching must occur after the 1997-1998 academic year. Third, you must have at least one direct subsidized or unsubsidized loan from the William D. Ford Federal Direct Loan Program or Federal Family Education Loan (FFEL) Program. Notably, PLUS loans and consolidated loans that repaid PLUS loans are ineligible. Teachers in secondary schools can qualify by teaching subjects like math, science, or special education, while elementary teachers must demonstrate that they taught in a state-defined "high-need" field.

Determining Low-Income Schools: A Practical Tip

One common challenge is confirming whether your school qualifies as low-income. The U.S. Department of Education maintains a directory of eligible schools, updated annually. To check, visit the Teacher Cancellation Low Income Directory (TCLI Directory) and search by state and school name. If your school is listed, it meets the program’s criteria. If not, you may need to explore other forgiveness options like Public Service Loan Forgiveness (PSLF).

Maximizing Forgiveness: A Comparative Analysis

While the Teacher Loan Forgiveness Program caps forgiveness at $17,500, certain teachers can qualify for higher amounts. Secondary math and science teachers, as well as special education teachers, may receive up to $17,500, while other eligible teachers can receive up to $5,000. Compare this to PSLF, which offers full loan forgiveness after 10 years of qualifying payments but requires a longer commitment. For teachers in high-need fields, the Teacher Loan Forgiveness Program provides a faster path to partial relief, making it a strategic choice for those with moderate loan balances.

Application Process: Steps and Cautions

Once eligibility is confirmed, submit the Teacher Loan Forgiveness Application to your loan servicer after completing the five-year teaching requirement. Ensure your school’s chief administrative officer certifies the form. A common mistake is applying before completing the full five years or failing to verify the school’s eligibility. Keep detailed records of your teaching years and school status to avoid delays. Remember, this program does not renew; if you switch schools or take a break, the consecutive years’ count resets.

By understanding these criteria and taking proactive steps, teachers can strategically position themselves to benefit from the Teacher Loan Forgiveness Program, potentially reducing their student loan burden significantly within a relatively short timeframe.

Marjorie Taylor Greene's Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

![]()

Disability Discharge Application Process

For borrowers facing significant health challenges, the Disability Discharge Application Process offers a pathway to student loan forgiveness. This process, while potentially life-changing, requires careful navigation to ensure a successful outcome.

Understanding Eligibility: The Cornerstone of Your Application

First, determine if you meet the stringent eligibility criteria. The Department of Education requires a permanent disability that prevents you from engaging in substantial gainful activity. This means a doctor must certify that your condition is expected to last at least five years or result in death. Veterans may have a streamlined process if they have a service-related disability rated as total and permanent by the VA.

Understanding these criteria is crucial; applying without meeting them will lead to unnecessary delays and disappointment.

Gathering the Necessary Documentation: A Paper Trail of Proof

The application demands a comprehensive medical dossier. This includes a physician's certification form detailing your diagnosis, prognosis, and limitations. Be prepared to provide medical records, test results, and any other documentation supporting your claim. For veterans, a copy of your VA disability rating decision is essential. Remember, the more thorough your documentation, the stronger your case.

Incomplete applications are a common reason for delays, so meticulousness is key.

Navigating the Application Process: A Multi-Step Journey

The application itself is submitted through the Nelnet Total and Permanent Disability Servicer. Be prepared for a multi-step process involving online forms, document uploads, and potentially phone interviews. Patience is paramount; processing times can vary, and you may receive requests for additional information.

Post-Approval Considerations: A New Financial Landscape

Approval brings relief, but it's not without its nuances. For three years following discharge, you must refrain from earning income above the poverty guideline, obtaining new federal student loans, or receiving educational benefits. Understanding these post-discharge conditions is crucial to maintaining your forgiven status.

Proactive Steps for Success:

- Seek Professional Guidance: Consider consulting a disability advocate or attorney specializing in student loan forgiveness. Their expertise can be invaluable in navigating the complexities of the process.

- Stay Organized: Create a dedicated folder for all documentation, both physical and digital. This ensures easy access and prevents crucial documents from getting lost.

- Be Persistent: Don't be discouraged by potential setbacks. If your application is denied, carefully review the reasons and consider appealing the decision.

The Disability Discharge Application Process, while demanding, offers a vital lifeline for borrowers burdened by student loans and facing significant health challenges. By understanding the eligibility criteria, meticulously gathering documentation, and navigating the process with patience and persistence, individuals can increase their chances of achieving much-needed financial relief.

Do Current Students Qualify for Loan Forgiveness? Key Details Explained

You may want to see also

Explore related products

![]()

Loan Forgiveness for Specific Professions (e.g., healthcare)

Healthcare professionals burdened by student loan debt have access to targeted forgiveness programs designed to alleviate financial strain while addressing workforce shortages in critical areas. The Public Service Loan Forgiveness (PSLF) program, for instance, offers tax-free forgiveness after 120 qualifying payments for those employed full-time by a government or nonprofit organization. For healthcare workers, this includes roles in public hospitals, clinics, and community health centers. However, eligibility hinges on meticulous documentation—each payment must be certified, and loans must be in an income-driven repayment plan. A common pitfall is assuming private employment qualifies; only specific 501(c)(3) organizations and government entities meet the criteria.

Beyond PSLF, the National Health Service Corps (NHSC) Loan Repayment Program provides up to $50,000 in forgiveness for licensed primary care medical, dental, or mental health professionals serving two years in a Health Professional Shortage Area (HPSA). This program is particularly attractive for early-career clinicians, as it offers a substantial reduction in debt in exchange for a relatively short service commitment. For example, a family nurse practitioner working in a rural HPSA could see half their student loans forgiven after just two years, provided they fulfill their contractual obligations. The NHSC also offers state-specific loan repayment programs, which vary in terms of award amounts and service requirements.

For nurses, the Nurse Corps Loan Repayment Program stands out as a profession-specific option. Eligible registered nurses (RNs) or advanced practice registered nurses (APRNs) working in Critical Shortage Facilities (CSFs) or as nursing faculty can receive up to 85% of their unpaid nursing education debt over four years. The program prioritizes applicants serving in areas with the most significant shortages, such as rural or underserved urban communities. A key consideration is the partial forgiveness structure: 60% of debt is forgiven over two years, with an optional third and fourth year for an additional 25%. Applicants must commit to full-time employment, though part-time options are available for faculty positions.

Physicians specializing in high-need fields can explore the National Institutes of Health (NIH) Loan Repayment Programs, which offer up to $50,000 annually in debt repayment for those conducting biomedical or biobehavioral research. This program is unique in that it ties forgiveness to research contributions rather than direct patient care, making it ideal for academically oriented clinicians. Eligibility requires a doctoral degree and a minimum of 20 hours per week dedicated to qualifying research. A notable advantage is the program’s flexibility—recipients can renew their awards annually, provided they continue meeting service requirements.

While these programs offer substantial relief, navigating their complexities requires diligence. Applicants must carefully review eligibility criteria, maintain accurate records, and adhere to service commitments. For instance, failing to recertify income-driven repayment plans annually can disqualify PSLF applicants, while incomplete NHSC applications may result in delayed or denied awards. Prospective beneficiaries should also consider consulting financial advisors or program specialists to optimize their strategy. By aligning career paths with these targeted programs, healthcare professionals can transform overwhelming debt into manageable obligations, fostering both personal financial stability and broader public health impact.

Non-Profit Work and Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

You can expect your student loan to be forgiven after making 120 qualifying payments (10 years) while working full-time for a qualifying public service employer, such as a government or nonprofit organization. Ensure your loans are in an eligible repayment plan and submit the PSLF form to track your progress.

Forgiveness under IDR plans typically occurs after 20–25 years of qualifying payments, depending on the plan. For example, Revised Pay As You Earn (REPAYE) forgives after 20–25 years, while Income-Based Repayment (IBR) forgives after 20–25 years, depending on when you took out the loan.

The timeline for the one-time forgiveness program (up to $20,000 for Pell Grant recipients and $10,000 for others) depends on legal challenges. If approved, eligible borrowers can expect forgiveness within several months after the program resumes, provided they meet income requirements and submit an application.

If you qualify for TPD discharge due to a permanent disability, your loans can be forgiven immediately upon approval. The Department of Education may initiate the process automatically for some borrowers, but you can also apply directly by submitting documentation of your disability.