Federal student loans typically begin accruing interest as soon as the loan is disbursed, though the timing can vary depending on the type of loan. For Direct Subsidized Loans, the government covers the interest while the borrower is in school at least half-time, during the grace period after leaving school (usually six months), and during eligible deferment periods. In contrast, Direct Unsubsidized Loans and PLUS Loans accrue interest immediately upon disbursement, regardless of the borrower's enrollment status, meaning borrowers are responsible for paying the interest or allowing it to capitalize, which increases the total loan balance. Understanding when interest accrues is crucial for managing student loan debt effectively and minimizing long-term costs.

| Characteristics | Values |

|---|---|

| Direct Subsidized Loans (Undergrad) | No interest accrues while in school, during grace period, or deferment. |

| Direct Unsubsidized Loans | Interest accrues immediately after disbursement, including during school, grace period, and deferment. |

| Direct PLUS Loans | Interest accrues immediately after disbursement, including during all periods. |

| Perkins Loans | No interest accrues while in school, during grace period, or deferment. |

| Grace Period | Typically 6 months after leaving school for most loans (except PLUS Loans). |

| Deferment | Interest may or may not accrue depending on loan type (e.g., subsidized vs. unsubsidized). |

| Forbearance | Interest accrues on all loan types during forbearance. |

| Income-Driven Repayment Plans | Interest may accrue depending on loan type and payment amount. |

| Loan Consolidation | Interest accrues based on the new consolidated loan terms. |

| Latest Update | As of October 2023, these rules remain consistent with federal student loan policies. |

Explore related products

What You'll Learn

- Subsidized vs. Unsubsidized Loans: Subsidized loans don’t accrue interest while in school; unsubsidized loans do

- Grace Period Interest: Interest accrues on unsubsidized loans during the 6-month grace period after graduation

- Deferment Interest: Interest accrues on unsubsidized loans during deferment periods unless paid by the borrower

- Forbearance Interest: Interest accrues on all loan types during forbearance and must be paid eventually

- In-School Interest: Interest accrues on unsubsidized loans while enrolled, even if payments are deferred

![]()

Subsidized vs. Unsubsidized Loans: Subsidized loans don’t accrue interest while in school; unsubsidized loans do

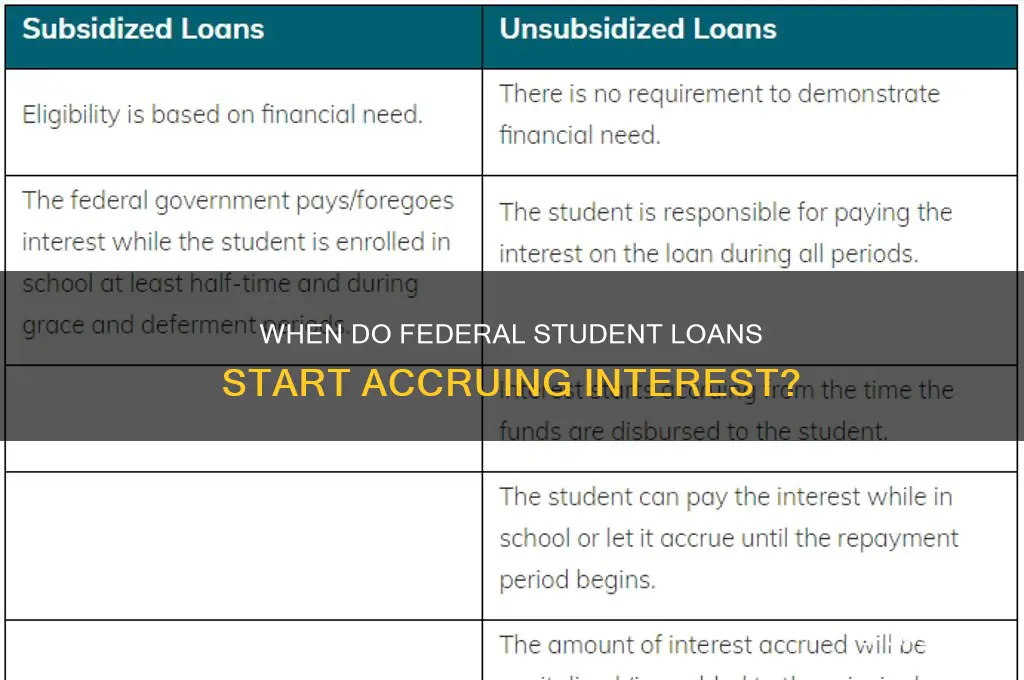

When considering federal student loans, understanding the difference between subsidized and unsubsidized loans is crucial, especially in terms of when interest begins to accrue. Subsidized loans are designed to help students with demonstrated financial need. One of their key benefits is that they do not accrue interest while the borrower is enrolled in school at least half-time, during the grace period after leaving school (typically six months), and during any approved deferment periods. This means the amount you borrow is the amount you will owe when repayment begins, making subsidized loans a more affordable option for eligible students.

In contrast, unsubsidized loans are available to students regardless of financial need, but they come with a significant difference in interest accrual. Unlike subsidized loans, unsubsidized loans begin accruing interest immediately after disbursement, even while the borrower is still in school. This means that if you do not pay the interest as it accrues during your time in school, it will be capitalized (added to the principal balance) and increase the total amount you have to repay. Over time, this can significantly increase the cost of the loan.

The distinction between subsidized and unsubsidized loans directly impacts the total cost of borrowing and the long-term financial burden on the student. For subsidized loans, the government covers the interest during eligible periods, providing a financial cushion for students. However, with unsubsidized loans, the borrower is responsible for all interest that accrues, which can add up quickly if left unpaid. This makes it essential for borrowers to consider their financial situation and repayment strategy when choosing between these loan types.

Another important factor to consider is the eligibility criteria for each loan type. Subsidized loans are need-based, meaning only undergraduate students with demonstrated financial need qualify. Unsubsidized loans, on the other hand, are available to both undergraduate and graduate students, regardless of financial need. This broader eligibility makes unsubsidized loans more accessible but also underscores the importance of understanding their interest accrual terms to avoid unexpected costs.

In summary, the primary difference between subsidized and unsubsidized loans lies in when interest begins to accrue. Subsidized loans do not accrue interest while the borrower is in school, during the grace period, or during deferment, making them a more cost-effective option for eligible students. Conversely, unsubsidized loans start accruing interest immediately after disbursement, which can lead to higher overall costs if the interest is not paid as it accrues. Understanding these differences is essential for making informed decisions about federal student loans and managing student debt effectively.

Unlocking Affordable Education: Best Student Interest Rates Explained

You may want to see also

Explore related products

![]()

Grace Period Interest: Interest accrues on unsubsidized loans during the 6-month grace period after graduation

Federal student loans have specific rules regarding when interest begins to accrue, and understanding these rules is crucial for borrowers to manage their debt effectively. One key aspect is the Grace Period Interest that applies to unsubsidized loans during the 6-month grace period after graduation. Unlike subsidized loans, where the government pays the interest while the borrower is in school or during the grace period, unsubsidized loans begin accruing interest immediately after disbursement. This means that even during the grace period—a 6-month window after graduation, leaving school, or dropping below half-time enrollment—interest continues to accumulate on unsubsidized loans.

During this grace period, borrowers are not required to make payments on their federal student loans, but the accruing interest on unsubsidized loans can lead to higher overall debt if not managed properly. The interest that accrues during this time is typically capitalized, meaning it is added to the principal balance of the loan. This results in borrowers paying interest on a larger amount once repayment begins. For example, if a borrower has a $20,000 unsubsidized loan with a 5% interest rate, approximately $500 in interest will accrue during the 6-month grace period, increasing the total amount owed.

To minimize the impact of grace period interest, borrowers have the option to pay off the accruing interest before it capitalizes. By making interest payments during the grace period, borrowers can prevent their loan balance from growing. This proactive approach can save money in the long run, as it reduces the total amount of interest paid over the life of the loan. Borrowers can contact their loan servicer to set up interest-only payments during this time.

It’s important for borrowers to be aware of the type of federal loans they have, as this determines whether interest accrues during the grace period. While subsidized loans offer a temporary reprieve from interest accrual, unsubsidized loans do not. Borrowers should review their loan agreements or log into their Federal Student Aid account to confirm their loan types. Understanding these distinctions allows borrowers to plan their finances effectively and avoid unexpected increases in their loan balances.

Lastly, borrowers should consider their financial situation and long-term goals when deciding how to handle grace period interest. For those with limited funds, focusing on building an emergency savings or paying off higher-interest debt might take priority. However, if possible, addressing the accruing interest on unsubsidized loans can be a wise investment. By staying informed and taking proactive steps, borrowers can navigate the grace period more confidently and set themselves up for successful loan repayment.

Maximize Tax Savings: Student Loan Interest Deduction Strategies

You may want to see also

Explore related products

![]()

Deferment Interest: Interest accrues on unsubsidized loans during deferment periods unless paid by the borrower

Federal student loans have specific rules regarding when and how interest accrues, and understanding these rules is crucial for borrowers to manage their debt effectively. One key aspect to consider is Deferment Interest, particularly how it applies to unsubsidized loans. Unlike subsidized loans, where the government pays the interest while the borrower is in school or during certain deferment periods, unsubsidized loans accrue interest from the moment the loan is disbursed. This means that even if a borrower is not required to make payments during a deferment period—such as while in school, during military service, or in economic hardship—interest continues to accumulate on unsubsidized loans.

During a deferment period, the borrower has the option to pay the accruing interest on their unsubsidized loans, but it is not mandatory. If the borrower chooses not to pay the interest, it will be added to the principal balance of the loan, a process known as capitalization. Capitalization increases the total amount of the loan, as future interest will be calculated on this new, higher principal balance. This can significantly increase the overall cost of the loan over time, making it more expensive to repay. Therefore, paying the interest during deferment, even if payments are not required, can be a wise financial strategy to minimize long-term debt.

It is important for borrowers to understand the specific terms of their deferment and the type of loans they hold. For instance, while interest accrues on unsubsidized loans during deferment, subsidized loans do not accrue interest during certain deferment periods, such as while the borrower is in school. Borrowers should review their loan agreements or contact their loan servicer to confirm whether their loans are subsidized or unsubsidized and to understand the implications of deferment on their interest accrual. This knowledge can help borrowers make informed decisions about managing their student loan debt.

Another critical point is that not all deferment periods are the same. Some deferments, such as those for economic hardship or unemployment, may have different rules regarding interest accrual depending on the type of loan. For example, while interest always accrues on unsubsidized loans during deferment, certain types of deferments for subsidized loans may still result in interest accrual if the deferment is not related to in-school status. Borrowers should carefully review the terms of their deferment to understand their responsibilities and options regarding interest payments.

Lastly, borrowers should consider the long-term financial impact of allowing interest to accrue and capitalize on their unsubsidized loans during deferment. While deferment provides temporary relief from making payments, the growing loan balance due to unpaid interest can lead to higher monthly payments and increased total repayment amounts once the deferment period ends. Proactively paying the interest during deferment, if possible, can help borrowers avoid capitalization and keep their overall loan costs down. For those unable to pay the interest, it is essential to plan for the increased loan balance and explore repayment strategies that align with their financial situation after the deferment period concludes.

Understanding Unpaid Interest on Student Loans: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Forbearance Interest: Interest accrues on all loan types during forbearance and must be paid eventually

When federal student loans enter a forbearance period, it’s crucial to understand that interest continues to accrue on all loan types, regardless of whether they are subsidized or unsubsidized. Forbearance is a temporary pause or reduction in loan payments granted by the lender, often due to financial hardship, medical issues, or other qualifying circumstances. While forbearance provides immediate relief by allowing borrowers to temporarily stop making payments or pay a reduced amount, it does not stop the interest from accumulating. This means the total cost of the loan increases during the forbearance period, as unpaid interest is typically capitalized (added to the principal balance) once the forbearance ends.

For subsidized federal loans, which normally do not accrue interest while the borrower is in school, during grace periods, or in certain deferment periods, forbearance is a notable exception. Even subsidized loans will accrue interest during forbearance, and this interest must be paid eventually. For unsubsidized loans, which always accrue interest regardless of the repayment status, forbearance simply extends the period during which interest compounds, further increasing the overall debt burden. Borrowers should be aware that allowing interest to capitalize can lead to higher monthly payments and a longer repayment term once the forbearance period concludes.

The decision to enter forbearance should not be taken lightly, as the accruing interest can significantly impact long-term financial health. Borrowers are strongly encouraged to explore other options, such as income-driven repayment plans or deferment, which may offer more favorable terms regarding interest accrual. For example, some deferment options allow subsidized loans to remain interest-free, while income-driven plans may reduce monthly payments based on income and family size without capitalizing interest. Forbearance should be considered a last resort when no other alternatives are available.

If forbearance is unavoidable, borrowers can minimize its financial impact by paying the accruing interest during the forbearance period, even if they are not required to make full loan payments. By doing so, they can prevent interest capitalization and keep the loan balance from growing. Lenders often provide estimates of the monthly interest accrual, which borrowers can pay voluntarily to manage their debt more effectively. This proactive approach can save money in the long run and make the transition back to regular payments smoother.

In summary, forbearance interest is a critical aspect of federal student loans that borrowers must understand. Interest accrues on all loan types during forbearance, and this unpaid interest is typically capitalized, increasing the total amount owed. While forbearance offers temporary payment relief, it comes at the cost of higher long-term debt. Borrowers should carefully weigh their options, consider alternatives, and, if possible, pay the accruing interest during forbearance to mitigate its financial consequences. Being informed and proactive can help manage student loan debt more effectively during challenging times.

Understanding Income Limits for Claiming Student Loan Interest Deductions

You may want to see also

Explore related products

$16.53 $22.99

![]()

In-School Interest: Interest accrues on unsubsidized loans while enrolled, even if payments are deferred

Federal student loans come with different terms depending on the type of loan and the borrower's enrollment status. One critical aspect to understand is In-School Interest, particularly how it applies to unsubsidized loans. Unlike subsidized loans, where the government pays the interest while the borrower is enrolled at least half-time, unsubsidized loans begin accruing interest immediately after disbursement, regardless of enrollment status. This means that even if you are actively attending school and not required to make payments, interest is still accumulating on your unsubsidized loans.

The accrual of interest on unsubsidized loans during enrollment can have long-term financial implications. Since payments are typically deferred while in school, many borrowers do not realize that interest is compounding over time. This unpaid interest is often capitalized, meaning it is added to the principal balance of the loan once the grace period ends. As a result, borrowers may graduate with a larger loan balance than they initially borrowed, increasing the total cost of repayment. Understanding this mechanism is crucial for managing student loan debt effectively.

To mitigate the impact of in-school interest, borrowers have the option to make interest payments while still enrolled. Although not mandatory, paying the interest as it accrues can prevent capitalization and keep the overall loan balance in check. This proactive approach can save borrowers hundreds or even thousands of dollars over the life of the loan. Financial aid offices and loan servicers often provide resources to help students estimate their accruing interest and plan for optional payments.

It’s important to note that not all federal loans accrue interest while in school. Subsidized Direct Loans, for example, do not accumulate interest during periods of at least half-time enrollment, grace periods, or deferment. However, unsubsidized Direct Loans, as well as PLUS Loans for graduate students and parents, do accrue interest immediately. Borrowers should carefully review their loan types and terms to understand when and how interest applies to their specific situation.

In summary, In-School Interest on unsubsidized federal student loans is a key factor in the overall cost of borrowing. While payments may be deferred during enrollment, interest continues to accrue and can capitalize, increasing the loan balance. Borrowers can take steps to manage this by making voluntary interest payments while in school. By staying informed and proactive, students can minimize the long-term financial burden of their unsubsidized loans.

Student Loans vs. No-Interest Credit Cards: Which Option is Better?

You may want to see also

Frequently asked questions

Federal student loans typically start accruing interest as soon as the loan is disbursed, except for subsidized Direct Loans, which do not accrue interest while the borrower is in school, during the grace period, or in deferment.

For subsidized Direct Loans, no interest accrues while you are enrolled in school at least half-time. For unsubsidized Direct Loans, interest begins accruing as soon as the loan is disbursed, even while you’re in school.

For subsidized Direct Loans, interest does not accrue during the grace period (usually 6 months after leaving school). For unsubsidized Direct Loans, interest continues to accrue during the grace period.

For subsidized Direct Loans, interest does not accrue during deferment. For unsubsidized Direct Loans, interest accrues during both deferment and forbearance.

The borrower is typically responsible for paying the interest that accrues on unsubsidized loans. For subsidized loans, the government pays the interest while the borrower is in school, during the grace period, and in deferment.