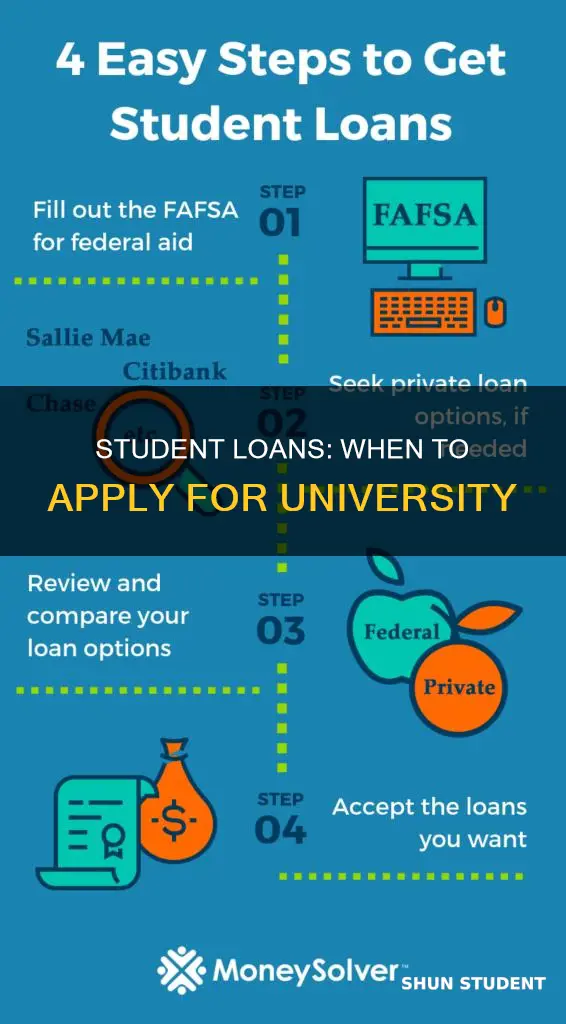

Applying for a student loan can be a daunting task, and it's important to know your options. There are several ways to fund higher education, including grants, scholarships, and work-study programs. Students can also use federal or private student loans to bridge financial gaps. Federal student loans have stricter application deadlines, while private student loans are more flexible, but it's best to apply for either as early as possible.

| Characteristics | Values |

|---|---|

| Who can apply? | Full-time and part-time students who are from or normally live in England |

| How to apply | Apply online for student finance including Tuition Fee Loans, Maintenance Loans and Grants |

| What to include in the application | Basic personal and financial information, and the type of interest rate and repayment plan |

| When to apply | As early as possible, at least 6 weeks before the start of the course |

| Re-application | Required for each year of the course |

| Additional documents | May need to provide extra evidence |

| Application cost | Free |

| Credit check | Required |

| Cosigner | May boost your chances of being approved |

Explore related products

$8.34 $17.99

What You'll Learn

![]()

Federal student loans

After submitting your FAFSA, you will receive a FAFSA Submission Summary, which will give you basic information about your eligibility for federal student aid. This includes grants, scholarships, work-study programs, and loans. To qualify for federal student loans, you must meet certain eligibility requirements, including financial need. Additionally, you must be enrolled at least half-time at a school that participates in the Direct Loan Program and be enrolled in a program that leads to a degree or certificate.

There are two main types of federal student loans: Direct Subsidized Loans and Direct Unsubsidized Loans. Direct Subsidized Loans are available only to undergraduate students who demonstrate financial need. On the other hand, Direct Unsubsidized Loans are available to both undergraduate and graduate or professional degree students, regardless of financial need. PLUS loans are another option that can help cover education expenses up to the cost of attendance, but they do require a credit check.

It's important to note that federal student loans do not require a strong credit history or a cosigner, making them accessible to recent high school graduates. However, for PLUS loans, borrowers with adverse credit history must meet additional requirements to qualify. Overall, federal student loans provide a range of options to help students finance their education, with the added benefit of not needing a perfect financial history.

Jewish Students at Ivy League Universities: What's the Percentage?

You may want to see also

Explore related products

![]()

Private student loans

There are a variety of private student loan options available, and it's important to research which option is best for you. You can use tools provided by student loan comparison sites like Credible and Edvisors to help you find loans that match your criteria. You should generally consider federal student loans first and then take out private loans if you still need money.

Some private student loan lenders include Sallie Mae, Citizens Student Loan, College Ave Student Loans, and ELFI, each offering different loan terms and repayment options. You can apply for a private student loan on the lender's website, and there is usually no cost to apply.

Black Student Enrollment at the University of Kentucky

You may want to see also

Explore related products

![]()

Understanding the differences

There are several differences between applying for a private student loan and a federal student loan. Private student loans are provided by banks or other financial institutions, whereas federal student loans are provided by the government. Private student loans are credit-based, meaning the lender will check your credit rating and other financial information. On the other hand, federal student loans in the UK, such as those provided by Student Finance England, do not require a credit check and are based on eligibility criteria such as household income and where you'll study.

Another difference lies in the application process. For private student loans, you can apply directly on the lender's website, and approval can be received within minutes. Private student loans do not have specific deadlines, but it is recommended to apply early to have ample time to compare loan options and find the best one for your needs. In contrast, federal student loans usually have an online application process, and you may need to create a student finance account to apply. The processing time for federal student loans can take up to six weeks, and you may need to provide additional evidence or documentation.

The disbursement process also varies between private and federal student loans. Private lenders typically disburse student loans at the start of the semester, and the funds are sent to the school, which directly applies them to your tuition and fees. Any leftover money is then given to the student for other educational costs. For federal student loans, you will usually receive your maintenance loan directly into your bank account at the start of each term after registering at your university or college.

It is important to note that the differences between private and federal student loans may vary depending on your location and the specific lenders or government programs involved. Additionally, the repayment plans and requirements may differ between private and federal student loans, so it is essential to carefully review the terms and conditions before committing to any loan.

Discover Grand Canyon University's On-Campus Student Population

You may want to see also

Explore related products

$119.5 $179.82

![]()

Application deadlines

Private Student Loans

Private student loans typically do not have specific deadlines. However, it is recommended to apply early, as the application process can take time, and you will want to compare different loan options. Private lenders usually disburse loan funds at the start of the semester, and the funds are sent directly to the school to cover tuition and fees. Any remaining money is then given to the student for other expenses.

Federal or Government Student Loans

The application process and deadlines for federal or government student loans may differ depending on your location and the specific loan program. For example, in England, students can apply for Tuition Fee Loans, Maintenance Loans, and Maintenance Grants online through Student Finance England. The application process can take up to six weeks, and you may need to provide additional evidence or documentation. It is recommended to keep your details, such as household income and bank information, up to date throughout your course, as these changes can affect your loan payments.

University or Institution-Specific Funding

In addition to federal or government loans, you may also explore financial aid opportunities directly from your university or educational institution. Each university may have its own application process and deadlines for financial aid, so be sure to check with your university's financial aid office or website for specific information.

Reapplication and Renewal

Remember that student loans usually need to be reapplied for each year of your course. Keep track of the deadlines for reapplication to ensure continuous funding throughout your studies. Additionally, stay updated with any changes in your eligibility or the loan terms to make informed decisions about your student financing.

Georgian Court University: Student Population Insights

You may want to see also

Explore related products

![]()

Additional fees

When it comes to student loans, there are often additional fees and costs that students and their families need to consider and plan for. These extra expenses can impact the overall cost of education and the loan repayment process. Here are some key points to keep in mind:

Application and Origination Fees

Some lenders may charge fees just for applying for a student loan or for initiating the loan. These fees can vary depending on the lender and the type of loan. It is important to inquire about such fees before applying to avoid unexpected costs.

Interest Rates

Interest rates are a significant component of student loans. The interest is the cost of borrowing money, and it accrues over time. When applying for a student loan, it is essential to understand the interest rate being offered and whether it is fixed or variable. A fixed interest rate remains the same throughout the loan, while a variable interest rate can fluctuate, causing monthly payments to increase or decrease.

Creditworthiness and Cosigners

Obtaining a student loan often requires demonstrating creditworthiness. If a student has a limited credit history, which is common for young individuals, they may need a cosigner. A cosigner, usually a parent or another responsible adult, shares responsibility for the loan and can help secure a lower interest rate. However, it is crucial to remember that the cosigner is equally liable for the loan's repayment.

Loan Refinancing

Refinancing a student loan means replacing the existing loan with a new one, typically from a private lender. This option may be beneficial if you can qualify for a lower interest rate, as it can reduce overall costs. However, refinancing federal loans with a private lender results in losing access to federally sponsored repayment or forgiveness programs. Additionally, a longer-term loan will decrease monthly payments but increase the total interest paid over time.

Additional Costs

Aside from tuition fees, there are other expenses associated with higher education, such as room and board, textbooks, and other living expenses. These costs can vary depending on the location and lifestyle choices. It is essential to factor in these additional costs when planning for student life and understanding the full financial commitment.

When applying for a student loan, it is crucial to carefully review the terms and conditions of the loan, ask questions, and consider all associated fees and expenses. Being well-informed about the financial aspects of your education will help you make more effective decisions and ensure a smoother repayment process in the future.

University of the Cumberlands: Student Population Insights

You may want to see also

Frequently asked questions

It is recommended to apply for federal student loans as early as possible. The Free Application for Federal Student Aid (FAFSA) usually opens on October 1 for the following academic year and closes on June 30.

Private student loans do not have specific deadlines, but it is recommended to apply long before your tuition is due. You can apply for a private student loan at any time, including mid-semester.

The first step is to fill out the FAFSA form, which is typically released on October 1. Once your university of choice has the form, they can review it and determine how much financial aid to offer.

First, fill out an application with your chosen private student loan lender. It can take up to two weeks for the lender to review and approve your application. Then, the lender will work with your school to certify your enrollment status and other details before disbursing the funds.