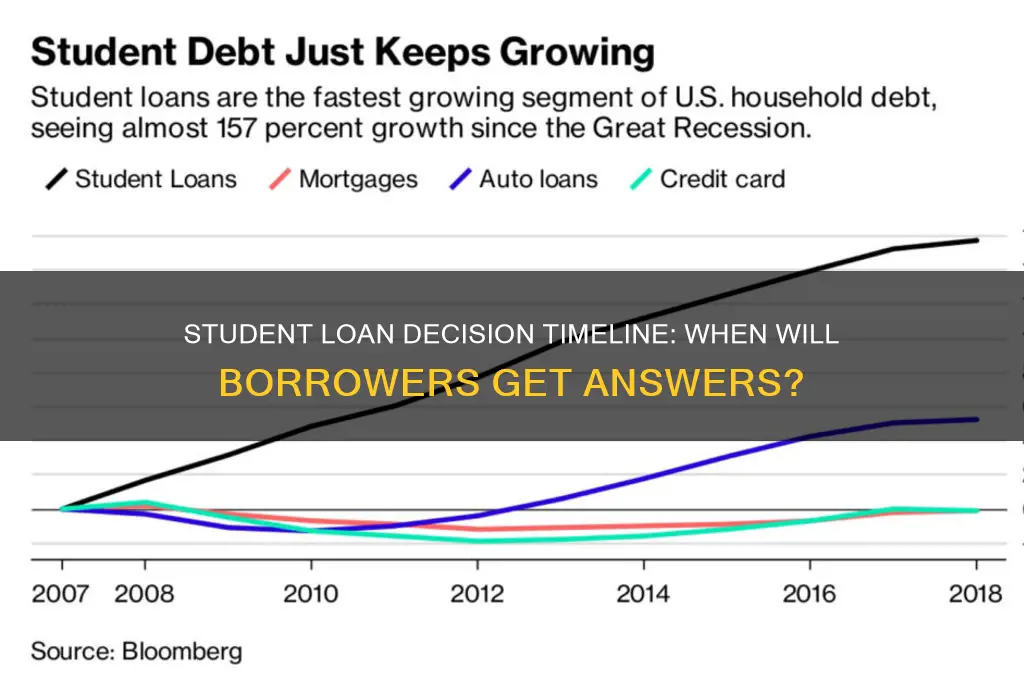

The question of when a decision will be made on student loans has become a pressing concern for millions of borrowers, as the ongoing debate over loan forgiveness, repayment plans, and interest rates continues to unfold. With the Biden administration’s previous attempts at widespread loan forgiveness stalled in legal battles and the temporary pause on loan payments set to expire, borrowers are eagerly awaiting clarity on their financial futures. Key factors influencing the timeline include court rulings, legislative actions, and potential executive orders, leaving many to speculate whether relief will come in the form of partial forgiveness, extended payment pauses, or revised repayment terms. As the 2024 election approaches, political pressures and economic considerations further complicate the decision-making process, leaving borrowers in a state of uncertainty and anticipation.

| Characteristics | Values |

|---|---|

| Current Status | No official decision date announced as of October 2023. |

| Recent Updates | Supreme Court struck down Biden's student loan forgiveness plan in June 2023. |

| Pending Actions | Department of Education exploring alternative pathways for loan relief. |

| Potential Timeline | Unclear; dependent on legislative or administrative actions. |

| Key Factors Influencing Decision | Legal challenges, political climate, and economic considerations. |

| Impact on Borrowers | Millions of borrowers awaiting clarity on loan repayment or forgiveness. |

| Next Steps | Borrowers advised to monitor official updates from the Department of Education. |

| Loan Payments Status | Payments resumed in October 2023 after pandemic-related pause ended. |

| Public Sentiment | Mixed reactions, with calls for broader relief and concerns about debt burden. |

| Legislative Efforts | Ongoing discussions in Congress but no concrete bills passed yet. |

Explore related products

What You'll Learn

![]()

Timeline for Loan Forgiveness Announcement

The Biden administration’s student loan forgiveness plan has been mired in legal challenges, leaving millions of borrowers in limbo. While the Supreme Court struck down the initial $400 billion debt cancellation proposal in June 2023, the Department of Education has continued to explore alternative pathways to provide relief. Borrowers eagerly await a definitive timeline for an announcement, but the process remains complex and dependent on legislative and judicial outcomes.

To understand the potential timeline, consider the steps involved. First, the administration must finalize a new plan that complies with the Higher Education Act, a process that requires public comment periods and regulatory reviews. This alone could take 6–12 months. Second, any new proposal will likely face immediate legal challenges, adding another 6–18 months of delays. Borrowers should monitor key milestones, such as the release of a draft rule and the conclusion of public comment periods, as these will signal progress.

Comparatively, the timeline for loan forgiveness announcements differs from other policy rollouts. For instance, the Public Service Loan Forgiveness (PSLF) waiver, introduced in 2021, took effect within months due to its narrower scope and existing legal framework. In contrast, broad-based debt cancellation requires navigating constitutional and statutory hurdles, making it a slower process. Borrowers should temper expectations and prepare for a timeline spanning late 2024 to early 2025, barring unexpected breakthroughs.

Practically, borrowers can take proactive steps while awaiting an announcement. First, ensure your contact information is updated with your loan servicer to receive timely updates. Second, explore alternative relief programs like income-driven repayment plans or PSLF, which remain unaffected by the current legal battles. Finally, avoid making extra payments on federal loans until the situation clarifies, as forgiven debt could render those payments unnecessary. Staying informed and prepared will position you to act swiftly once a decision is made.

NC Tax Implications: Will Student Loan Forgiveness Be Taxable?

You may want to see also

Explore related products

![]()

Impact of Political Changes on Decisions

Political shifts often dictate the timeline and nature of decisions regarding student loans, as policy changes are inherently tied to the priorities of the ruling administration. For instance, during election years, incumbent parties may delay decisive actions on student debt to avoid alienating voter blocs, while newly elected officials might expedite reforms to fulfill campaign promises. The 2020 U.S. presidential election exemplifies this: the Biden administration paused federal student loan payments within weeks of taking office, a move directly linked to its platform of addressing educational affordability. Conversely, midterm elections can stall progress, as legislative gridlock becomes more likely when power is divided between parties. Understanding this cyclical pattern allows borrowers to anticipate delays or accelerations in policy changes based on the electoral calendar.

The ideological leanings of political parties play a pivotal role in shaping the substance of student loan decisions, not just their timing. Progressive administrations tend to favor broad-based debt forgiveness or interest rate reductions, as seen in proposals like the $10,000 to $50,000 cancellation plans debated during Biden’s tenure. Conservative governments, however, often prioritize fiscal restraint, advocating for stricter repayment terms or limiting relief to specific demographics, such as low-income borrowers. For example, the Trump administration expanded income-driven repayment plans but resisted calls for widespread forgiveness. Borrowers can strategize by tracking party platforms and aligning financial plans with the likely direction of policy under different political scenarios.

Internationally, political changes in countries like the U.K. and Canada highlight how shifts in leadership can abruptly alter student loan landscapes. In 2012, England raised tuition caps from £3,000 to £9,000 annually, a decision driven by the Conservative-Liberal Democrat coalition’s austerity measures. Conversely, New Zealand’s Labour Party reintroduced free tertiary education for domestic students in 2020, reversing earlier fee increases. These examples underscore the importance of monitoring global political trends, as they provide comparative insights into potential domestic shifts. Borrowers in countries with volatile political climates should diversify repayment strategies, such as exploring international loan consolidation options or currency-hedged savings accounts.

Practical steps for navigating the impact of political changes include setting up alerts for legislative updates, engaging with advocacy groups like the Student Borrower Protection Center, and maintaining a flexible financial plan. For instance, if a forgiveness program is announced but faces legal challenges, borrowers should continue making payments to avoid capitalization of interest. Similarly, during election seasons, consider overpaying on loans if possible, as future policies might cap deductible interest payments. By treating political cycles as predictable variables, borrowers can minimize uncertainty and maximize control over their financial futures.

Can the Department of Education Forgive Your Student Loans?

You may want to see also

Explore related products

![]()

Key Dates for Borrower Notifications

Borrowers often mark their calendars for key dates related to student loan decisions, but understanding the timeline is only half the battle. Notifications about loan forgiveness, repayment plans, or interest rate changes typically arrive within 30 to 60 days after a major policy announcement. For instance, when the Public Service Loan Forgiveness (PSLF) waiver was introduced in 2021, eligible borrowers received updates via email or postal mail within 45 days of submitting their employment certification form. Missing these notifications can delay action, so ensure your contact information is current with your loan servicer.

Consider the annual timeline for income-driven repayment (IDR) recertification, a critical date for many borrowers. Failure to recertify by the deadline—usually 10 months after your last certification—can result in a payment increase or capitalization of unpaid interest. For example, if your recertification date is October 15, 2024, submitting your updated income information by September 1 ensures uninterrupted enrollment. Pro tip: Set a recurring calendar reminder 60 days before your deadline to avoid last-minute scrambling.

Policy changes often trigger mass notifications, but their timing can be unpredictable. During the COVID-19 payment pause, borrowers received updates every 30 to 45 days via email and their loan servicer’s portal. However, not all borrowers checked these channels regularly, leading to confusion when the pause ended. To stay informed, opt into all communication methods offered by your servicer—email, text, and postal mail—and check your spam folder periodically.

Finally, keep an eye on legislative calendars. Major decisions, like the extension of a repayment pause or the introduction of new forgiveness programs, often align with congressional sessions or election cycles. For instance, announcements about student loan relief have historically peaked in September or October, coinciding with the start of the federal fiscal year. Tracking these patterns can help you anticipate notifications and plan accordingly. Practical advice: Follow reputable education policy journalists or subscribe to updates from organizations like the Department of Education to stay ahead of the curve.

Does Northrop Grumman Qualify for Student Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Role of Federal Agencies in Timing

Federal agencies play a pivotal role in determining the timeline for decisions on student loans, acting as both architects and gatekeepers of policy implementation. The U.S. Department of Education (DOE), for instance, is the primary agency responsible for overseeing federal student loan programs. Its Office of Federal Student Aid (FSA) manages the disbursement, repayment, and forgiveness of loans, making it a central player in any decision-making process. However, the DOE does not operate in isolation. Agencies like the Office of Management and Budget (OMB) review proposed policies for fiscal impact, while the Department of the Treasury assesses economic implications. This interagency collaboration ensures decisions are comprehensive but also introduces layers of review that can extend timelines.

Consider the example of the Public Service Loan Forgiveness (PSLF) program reforms. The DOE announced changes in 2021 to address longstanding issues with the program, but the implementation timeline stretched over several months. This delay was partly due to the need for interagency coordination, including OMB’s review of budgetary implications and the Treasury’s assessment of tax-related consequences. Borrowers awaiting relief faced uncertainty, highlighting how federal agency processes directly influence the timing of student loan decisions. For those tracking future announcements, understanding this bureaucratic workflow is key to managing expectations.

To expedite decisions, federal agencies often follow a structured process that includes rulemaking, public comment periods, and finalization. For instance, when the DOE proposes changes to income-driven repayment plans, it must publish a Notice of Proposed Rulemaking (NPRM) and allow a 30- to 60-day public comment period. This step is mandated by the Administrative Procedure Act and ensures stakeholder input but inherently adds weeks to the timeline. Borrowers can stay informed by monitoring the Federal Register, where such notices are published, and submitting comments to influence outcomes. Pro tip: Set up alerts for specific keywords like “student loans” or “loan forgiveness” on the Federal Register website to stay ahead of updates.

A comparative analysis of recent student loan decisions reveals that executive actions, such as presidential memoranda, can bypass some of these procedural delays. For example, the Biden administration’s extension of the student loan payment pause in 2022 was implemented swiftly through executive order, sidestepping the lengthy rulemaking process. However, such actions are limited in scope and often require subsequent agency action to formalize changes. This duality underscores the trade-off between speed and durability in federal decision-making. Borrowers should differentiate between temporary measures and permanent policy changes to plan effectively.

In conclusion, the timing of student loan decisions is deeply intertwined with the operational rhythms of federal agencies. While interagency collaboration ensures robust policy outcomes, it also introduces delays that can frustrate borrowers. By understanding these mechanisms—from rulemaking to executive actions—individuals can better navigate the uncertainty surrounding student loan announcements. Practical steps, like monitoring the Federal Register and distinguishing between temporary and permanent measures, empower borrowers to stay informed and proactive.

Understanding Student Debt Forgiveness: Key Facts and Eligibility Criteria

You may want to see also

Explore related products

![]()

Potential Delays and Legal Challenges

The timeline for a decision on student loans is fraught with potential delays, often stemming from the intricate interplay of legislative, judicial, and administrative processes. For instance, the U.S. Department of Education’s implementation of loan forgiveness programs has historically faced setbacks due to bureaucratic hurdles and resource constraints. When a policy change is proposed, it typically requires extensive review, public comment periods, and interagency coordination, each step introducing opportunities for delay. For borrowers awaiting relief, understanding these procedural bottlenecks is crucial for managing expectations.

Legal challenges further complicate the timeline, as lawsuits can halt or significantly slow down the implementation of student loan policies. For example, the Biden administration’s 2022 student loan forgiveness plan was blocked by multiple lawsuits, leading to months of uncertainty for millions of borrowers. Such cases often hinge on questions of executive authority, statutory interpretation, or constitutionality, requiring lengthy judicial proceedings. Borrowers should monitor key court cases, as rulings can either expedite or indefinitely postpone relief measures.

A comparative analysis of past student loan initiatives reveals a pattern: policies with broad eligibility criteria or significant financial implications are more likely to face legal and procedural delays. For instance, the Public Service Loan Forgiveness (PSLF) program, despite being narrower in scope, took years to refine due to administrative complexities. In contrast, smaller-scale programs, like those targeting specific professions or income brackets, have often moved more swiftly. Borrowers can use this insight to assess the potential timeline for current proposals based on their scope and complexity.

To navigate these delays, borrowers should take proactive steps. First, stay informed through official channels like the Department of Education’s Federal Student Aid website, which provides updates on policy changes and legal developments. Second, prepare alternative financial plans, such as budgeting for continued payments or exploring income-driven repayment options. Finally, consider joining advocacy groups or legal watch organizations that track student loan litigation, as collective action can sometimes influence the pace of decision-making. By staying engaged and prepared, borrowers can mitigate the impact of potential delays.

Canceling Student Debt: Economic Boost or Burden? A Critical Analysis

You may want to see also

Frequently asked questions

The timeline for a decision on student loan forgiveness varies depending on government policies and legal processes. As of the latest updates, decisions are typically announced within 6 to 12 months after proposals or lawsuits are filed, but this can change.

Approval times for student loan applications usually range from a few days to several weeks, depending on the lender and the completeness of your application. Federal loans often take longer due to verification processes.

Decisions on student loan interest rates are typically made annually by the federal government, usually in the summer, based on the 10-year Treasury note auction. Private lenders may adjust rates at any time based on market conditions.

Changes to student loan repayment plans are often announced during policy updates or legislative actions. Borrowers are usually notified 30 to 60 days before any changes take effect.

The timeline for decisions on student loan debt cancellation lawsuits depends on the court system and can take several months to years. Borrowers are typically informed via official channels once a ruling is made.