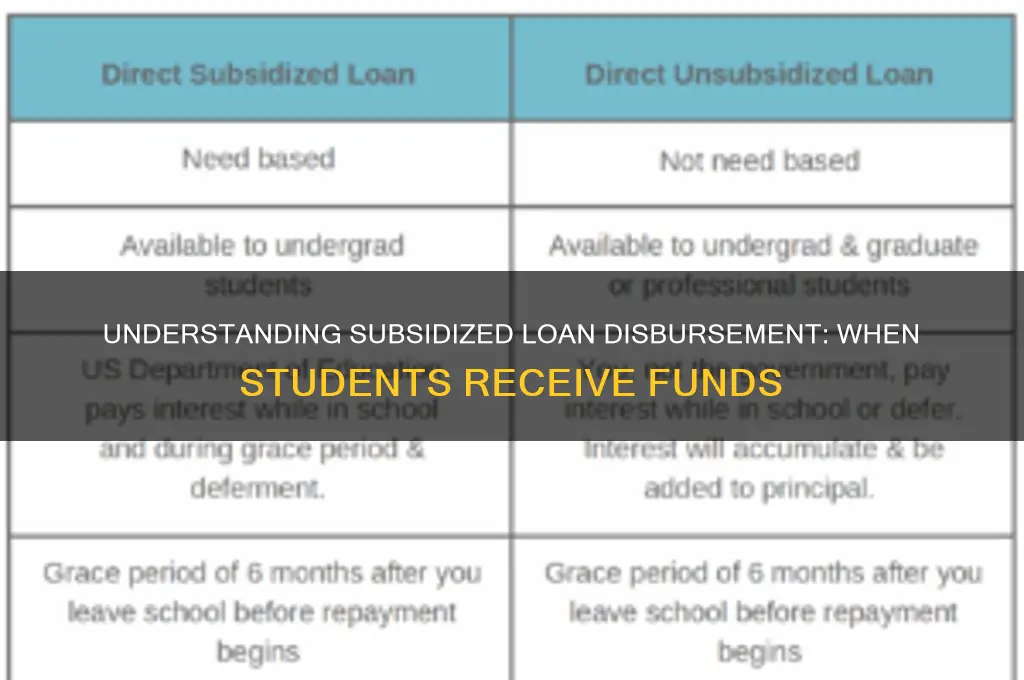

Subsidized loans are a form of federal student aid designed to help undergraduate students with demonstrated financial need cover tuition and other educational expenses. One key feature of subsidized loans is that the government pays the interest on the loan while the student is enrolled in school at least half-time, during the grace period after leaving school, and during any approved deferment periods. This means the loan balance does not increase during these times. A student typically receives a portion of their subsidized loan at the beginning of each semester or term, disbursed directly to their school to cover tuition, fees, and other eligible expenses. Any remaining funds are then released to the student for other educational costs, such as books or living expenses. The timing and amount of disbursement depend on the school’s policies and the student’s enrollment status.

| Characteristics | Values |

|---|---|

| Disbursement Timing | Typically at the beginning of each academic term (e.g., fall, spring). |

| First-Time Borrowers | May have a 30-day delay in receiving the first disbursement. |

| Enrollment Status | Must be enrolled at least half-time in an eligible program. |

| Loan Period Coverage | Disbursed in equal amounts over the loan period (e.g., one academic year). |

| School Certification | Funds are released after the school certifies enrollment and eligibility. |

| Direct Deposit or Check | Funds are sent directly to the school, which then applies them to tuition, fees, and other costs, with any remainder refunded to the student. |

| Subsidized Loan Benefit | Government pays interest while student is in school, during grace period, and deferment periods. |

| Annual and Aggregate Limits | Subject to annual and aggregate borrowing limits based on year in school and dependency status. |

| Notification Requirement | Students must be notified by the school about the loan disbursement dates and amounts. |

| Prerequisites | Completion of the FAFSA, entrance counseling, and a Master Promissory Note (MPN). |

Explore related products

What You'll Learn

- Eligibility Criteria: Meeting academic and enrollment requirements for loan disbursement

- Disbursement Schedule: Timing of loan release by the school

- Enrollment Status: Must be enrolled at least half-time

- Loan Limits: Annual and aggregate borrowing caps affecting disbursement

- First Disbursement Rules: Additional steps for first-time borrowers

![]()

Eligibility Criteria: Meeting academic and enrollment requirements for loan disbursement

To receive a portion of their subsidized loan, students must first navigate a stringent set of eligibility criteria tied to academic performance and enrollment status. These requirements are not merely bureaucratic hurdles but essential safeguards ensuring federal funds support students actively progressing toward their degrees. At the core, maintaining Satisfactory Academic Progress (SAP) is non-negotiable. This typically involves achieving a cumulative GPA of at least 2.0 (though institutions may set higher standards) and completing 67% of attempted courses. Falling below these benchmarks can trigger a warning, probation, or outright suspension of aid, delaying or halting loan disbursements.

Enrollment status plays an equally critical role. Subsidized loans are disbursed only to students enrolled at least half-time, as defined by their institution. For undergraduates, this often means carrying 6 credit hours per term, while graduate students might need 4–5. Dropping below half-time enrollment—even by a single credit—can disqualify a student from receiving funds. For instance, a student enrolled in 5 credits instead of 6 would not only lose eligibility for that term’s disbursement but also risk capitalizing the loan’s interest, increasing long-term debt.

Institutions also scrutinize the programmatic alignment of a student’s coursework. Credits must apply directly to the student’s declared degree or certificate program. Electives or courses outside the curriculum may not count toward enrollment requirements, inadvertently reducing a student’s credit load below the half-time threshold. For example, a biology major taking three 3-credit biology courses and one 3-credit art history elective would still meet the 6-credit minimum, but only if the art history course is approved as part of their degree plan.

Practical tips for ensuring eligibility include regularly meeting with an academic advisor to confirm course alignment and monitoring enrollment status through the school’s portal, especially during add/drop periods. Students should also familiarize themselves with their institution’s SAP policy, often found in the financial aid handbook. Proactive measures, such as submitting appeals with documented extenuating circumstances (e.g., medical emergencies) if SAP standards are not met, can sometimes reinstate eligibility. Ultimately, staying informed and compliant with these criteria is the student’s responsibility—and the key to unlocking uninterrupted loan disbursements.

Forgiving Student Loan Debt: Economic Boost or Unfair Burden?

You may want to see also

Explore related products

![]()

Disbursement Schedule: Timing of loan release by the school

The disbursement schedule of a subsidized loan is a critical aspect of financial aid, yet it often remains shrouded in confusion for students. Unlike a lump-sum payout, these loans are typically released in installments, following a timeline dictated by the school. This staggered approach serves multiple purposes: it aligns with the academic calendar, ensures funds are available when needed most, and encourages responsible financial management. Understanding this schedule is essential for budgeting and avoiding unnecessary stress.

Schools generally disburse subsidized loans at the beginning of each semester or quarter, coinciding with the start of classes. This timing ensures students have access to funds for tuition, fees, and living expenses from day one. However, the exact dates can vary depending on the institution's policies and the specific loan program. For instance, some schools may release funds a week before classes begin, while others might wait until after the add/drop period to confirm enrollment status.

Several factors influence the disbursement timeline. Federal regulations mandate that schools disburse loan funds within a certain timeframe, typically no earlier than 10 days before the start of the term. Additionally, the school's financial aid office must verify enrollment status and ensure all necessary paperwork is complete. Delays can occur if there are discrepancies in the student's file or if the school is awaiting confirmation of external funding sources.

To navigate the disbursement process smoothly, students should take proactive steps. First, familiarize yourself with your school's specific disbursement schedule, which is usually available on the financial aid website or in the student handbook. Second, ensure all required documents are submitted on time, including loan agreements and verification forms. Finally, monitor your student account regularly to track the status of your disbursement and address any issues promptly.

In conclusion, the disbursement schedule of a subsidized loan is a carefully orchestrated process designed to support students throughout their academic journey. By understanding the timing, factors influencing release, and taking proactive steps, students can effectively manage their finances and focus on their studies. Remember, knowledge is power – and in this case, it can also mean the difference between a smooth semester and a financial scramble.

Can Library Page Jobs Qualify for Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Enrollment Status: Must be enrolled at least half-time

To receive a portion of their subsidized loan, students must maintain at least half-time enrollment status. This requirement is non-negotiable and serves as a safeguard to ensure federal funds are allocated to those actively pursuing their education. Half-time enrollment typically translates to 6 credit hours for undergraduate students per semester, though this may vary by institution. Graduate students often have different thresholds, usually around 4-5 credit hours. Failing to meet this minimum can result in the forfeiture of subsidized loan eligibility, triggering repayment obligations sooner than anticipated.

Consider the scenario of a student who drops from full-time to part-time status mid-semester. If their enrollment falls below half-time, their subsidized loan disbursement may be prorated or halted entirely. This adjustment can create financial strain, as the student may have budgeted for the full loan amount. To avoid such pitfalls, students should consult their academic advisor before making changes to their course load. Additionally, monitoring enrollment status through the school’s student portal can provide real-time updates to prevent unintended consequences.

From a persuasive standpoint, maintaining half-time enrollment is not just a bureaucratic hoop to jump through—it’s a commitment to academic progress. Subsidized loans are designed to support students who are actively working toward their degree, not those who are sporadically attending classes. By staying enrolled at least half-time, students not only retain access to financial aid but also demonstrate dedication to their educational goals. This consistency fosters a sense of accountability and increases the likelihood of timely graduation.

Comparatively, the half-time enrollment rule distinguishes subsidized loans from other forms of financial aid. For instance, unsubsidized loans and private loans often have more flexible enrollment requirements, but they come with the burden of accruing interest while in school. Subsidized loans, on the other hand, offer interest-free borrowing for eligible students, making the half-time enrollment stipulation a small trade-off for significant savings. Understanding this distinction empowers students to make informed decisions about their financial aid strategy.

Practically speaking, students should plan their academic schedules with the half-time requirement in mind. For those balancing work and school, opting for a mix of daytime and evening classes can help meet the credit hour threshold without overwhelming their schedule. Summer sessions are another strategic option, allowing students to maintain enrollment status year-round and potentially accelerate their degree completion. Proactive planning not only ensures continued access to subsidized loans but also promotes a balanced approach to academic and personal responsibilities.

Will West Virginia Tax Student Loan Forgiveness? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Loan Limits: Annual and aggregate borrowing caps affecting disbursement

Federal student loans are not bottomless pits of funding. Annual and aggregate loan limits act as guardrails, dictating how much a student can borrow each year and over their entire academic career. These caps are designed to prevent students from accumulating unsustainable debt, but they also directly impact when and how much of a subsidized loan a student receives.

Understanding these limits is crucial for financial planning.

Let's break down the specifics. Annual limits vary based on factors like year in school and dependency status. For instance, a dependent undergraduate freshman can borrow up to $5,500 in subsidized and unsubsidized loans combined, with no more than $3,500 subsidized. This means a freshman might receive their subsidized loan disbursement in two installments, one per semester, each capped at $1,750. Aggregate limits, on the other hand, represent the total amount a student can borrow throughout their undergraduate studies. For dependent undergraduates, this cap is $31,000, with no more than $23,000 subsidized.

These limits aren't arbitrary. They reflect a balance between providing access to education and promoting responsible borrowing. Imagine a scenario where a student borrows the maximum subsidized loan each year. By their senior year, they would have reached the aggregate limit, potentially limiting their borrowing options for graduate studies. This highlights the importance of strategic borrowing, considering both immediate needs and long-term financial goals.

Students should view loan limits as a tool for financial planning, not a constraint. By understanding these caps and borrowing responsibly, they can maximize the benefits of subsidized loans while minimizing future debt burdens.

Louisiana's Tax Implications for Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

First Disbursement Rules: Additional steps for first-time borrowers

First-time borrowers often face additional hurdles before receiving their first disbursement of a subsidized loan. Federal regulations require these students to complete Entrance Counseling, a mandatory online session that explains loan terms, repayment options, and financial responsibilities. This step ensures borrowers understand the commitment they’re making, reducing the risk of default. Without completing this counseling, funds remain on hold, delaying access to much-needed financial aid.

Another critical requirement is the Master Promissory Note (MPN), a legal document that outlines the borrower’s promise to repay the loan. First-time borrowers must sign this note electronically, agreeing to its terms and conditions. The MPN remains valid for up to 10 years, covering multiple loans during a student’s academic career. Failure to sign this document halts the disbursement process entirely, leaving students without funds until compliance.

Institutions also enforce a 30-day delay on first disbursements for first-year, first-time borrowers under the Direct Loan program. This rule, mandated by the Department of Education, aims to prevent students from borrowing before confirming their long-term enrollment plans. While frustrating for those in immediate need, this delay encourages thoughtful financial planning and reduces premature borrowing.

Practical tip: Verify your school’s specific disbursement timeline, as it often aligns with the start of classes or after the drop/add period. Some schools disburse funds in two payments per academic year, splitting the loan amount to coincide with semester or quarter starts. Always check your student portal for updates and communicate with the financial aid office to ensure all requirements are met promptly.

In summary, first-time borrowers must navigate Entrance Counseling, the MPN, and potential disbursement delays to access their subsidized loan funds. Proactive completion of these steps ensures timely financial support, allowing students to focus on their academic goals without unnecessary stress.

Why Student Loan Forgiveness is Essential for Economic and Social Equity

You may want to see also

Frequently asked questions

A student will typically receive the first disbursement of their subsidized loan after the school certifies the loan, the borrower completes entrance counseling, and signs the Master Promissory Note (MPN). Disbursement usually occurs at the start of the academic term.

No, subsidized loans are disbursed according to the school’s academic calendar. Funds are generally released no earlier than 10 days before the start of the term, unless the school requests an exception.

Subsidized loans are typically disbursed in at least two installments per academic year, depending on the school’s policies. Each disbursement corresponds to the beginning of each term or semester.

If a student drops below half-time enrollment, their eligibility for subsidized loans ends, and they will no longer receive disbursements. They may also enter the grace period or begin repayment, depending on their enrollment status.