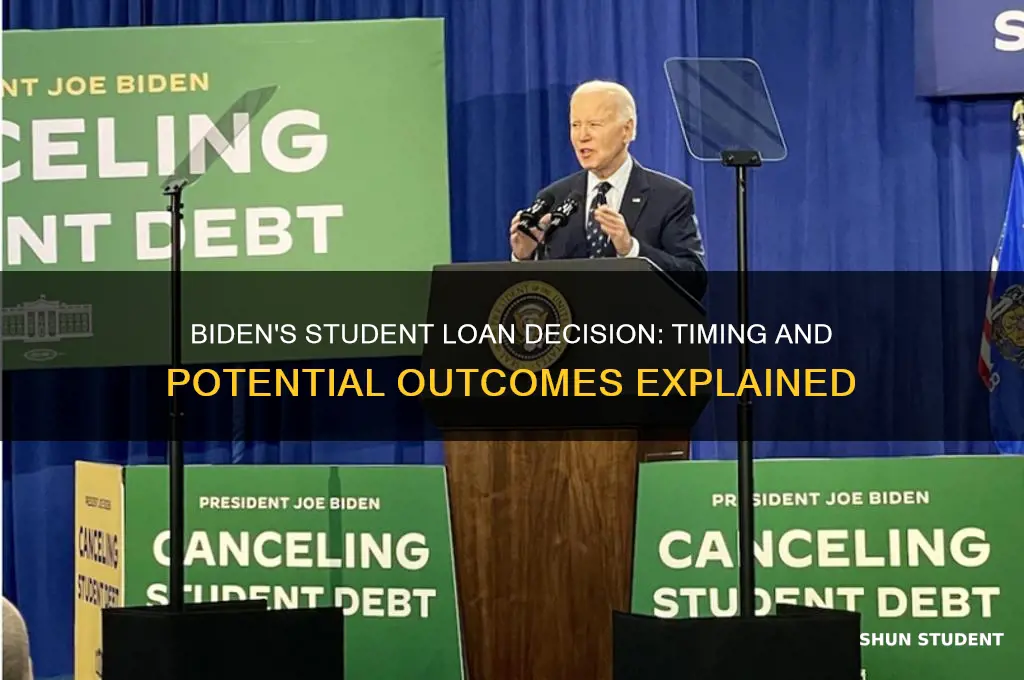

The question of when President Biden will make a decision regarding student loans has been a pressing concern for millions of Americans burdened by educational debt. With the pause on federal student loan payments set to expire, borrowers are eagerly awaiting clarity on potential loan forgiveness, payment resumption, or further extensions. Biden’s administration has faced mounting pressure from advocacy groups, lawmakers, and borrowers themselves to address the $1.7 trillion student debt crisis, which has become a significant economic and political issue. While the White House has hinted at possible actions, including targeted debt relief or income-driven repayment reforms, a definitive timeline remains uncertain. As the August 2023 deadline approaches, the decision will have far-reaching implications for individual financial stability and the broader economy, leaving many anxiously awaiting Biden’s next move.

| Characteristics | Values |

|---|---|

| Current Status | Biden administration has not announced a specific decision date. |

| Recent Updates | Ongoing legal challenges and Supreme Court involvement. |

| Key Factors Influencing Decision | Legal battles, economic conditions, political considerations. |

| Potential Timeline | Uncertain; dependent on court rulings and legislative actions. |

| Loan Payment Restart | Payments remain paused until further notice or court resolution. |

| Debt Forgiveness Plan | Original plan blocked by courts; alternative plans under consideration. |

| Public Statements | Biden has expressed commitment to providing relief but no firm timeline. |

| Congressional Role | Limited direct action; focus on legal and administrative pathways. |

| Impact on Borrowers | Continued uncertainty for millions of student loan holders. |

| Latest News (as of October 2023) | Supreme Court’s June 2023 ruling struck down Biden’s initial forgiveness plan. |

Explore related products

$14.99 $14.99

What You'll Learn

- Forgiveness Plan Timeline: When will Biden announce the final decision on student loan forgiveness

- Eligibility Criteria: Who qualifies for loan forgiveness under Biden’s plan

- Amount of Forgiveness: How much debt will be forgiven per borrower

- Legal Challenges: Potential lawsuits delaying Biden’s student loan decision

- Payment Restart Date: When will student loan payments resume after forgiveness

![]()

Forgiveness Plan Timeline: When will Biden announce the final decision on student loan forgiveness?

The Biden administration's student loan forgiveness plan has been a subject of intense speculation and anticipation, with millions of borrowers eagerly awaiting a definitive timeline. While the administration has made significant strides in addressing the student debt crisis, the exact date of the final decision remains elusive. To understand the potential timeline, it's essential to examine the key milestones and factors influencing the announcement.

Analyzing the Legal Landscape

The Supreme Court’s June 2023 ruling on Biden’s initial $10,000 to $20,000 forgiveness plan struck it down, citing the lack of congressional authorization. Since then, the administration has pursued an alternative path through the Higher Education Act’s compromise and settlement authority. The Department of Education initiated a negotiated rulemaking process in April 2024, a legally required step to craft new regulations. This process, which involves public hearings and stakeholder input, typically takes 6 to 12 months. Given this timeline, a final rule could emerge by late 2024 or early 2025, with an announcement likely preceding implementation by several months.

Political and Practical Considerations

The 2024 election cycle adds a layer of urgency and complexity. Biden’s team is acutely aware of the political stakes, as student loan forgiveness remains a key issue for young and progressive voters. Announcing a decision too close to the election could risk backlash, while delaying it might dampen enthusiasm. Practically, the administration must also navigate the logistical challenges of implementing forgiveness, including updating loan servicer systems and ensuring compliance with the new rules. Borrowers should monitor updates from the Department of Education and prepare documentation, such as income verification, if targeted forgiveness criteria are included.

Comparative Insights from Past Actions

Biden’s previous executive actions on student loans offer clues. The payment pause extensions, for instance, were often announced weeks before expiration dates. Similarly, the final forgiveness decision may follow a pattern of strategic timing, balancing legal readiness with political impact. Notably, the administration has emphasized a phased approach, potentially rolling out forgiveness in stages rather than a single announcement. Borrowers should stay informed through official channels and avoid relying on speculative media reports.

Practical Tips for Borrowers

While awaiting the decision, borrowers can take proactive steps. First, ensure your contact information is updated with your loan servicer to receive timely notifications. Second, explore alternative relief options like income-driven repayment plans or public service loan forgiveness. Finally, avoid making extra payments until the forgiveness terms are clear, as overpayment may not be refundable. By staying informed and prepared, borrowers can maximize their benefits once the plan is finalized.

In summary, while the exact date of Biden’s student loan forgiveness announcement remains uncertain, the legal, political, and practical factors suggest a timeline converging in late 2024 or early 2025. Borrowers should remain vigilant, proactive, and informed to navigate this evolving landscape effectively.

When Will Student Visa Applications Open? Key Dates and Updates

You may want to see also

Explore related products

![]()

Eligibility Criteria: Who qualifies for loan forgiveness under Biden’s plan?

As of the latest updates, President Biden's student loan forgiveness plan has been a subject of intense scrutiny and anticipation. The eligibility criteria are pivotal in determining who benefits from this initiative. To qualify, borrowers must meet specific income thresholds: individuals earning less than $125,000 annually or married couples filing jointly with incomes under $250,000 are eligible. This income-based approach aims to target relief toward those most in need, ensuring that higher earners do not disproportionately benefit from the program.

The type of loans held also plays a critical role in eligibility. Only federal student loans, including Direct Loans, Perkins Loans, and Federal Family Education Loans (FFEL) held by the Department of Education, qualify for forgiveness. Private loans are explicitly excluded, leaving borrowers with such debt to explore alternative relief options. Additionally, the loans must have been disbursed before July 1, 2021, to be considered under the current plan. This cutoff date ensures that the program addresses existing debt rather than incentivizing future borrowing.

Another key factor is the borrower’s repayment status. Those enrolled in income-driven repayment (IDR) plans or the Public Service Loan Forgiveness (PSLF) program may receive additional considerations. For instance, borrowers in IDR plans could see their remaining balances forgiven after 20–25 years of qualifying payments, depending on the plan. Public servants with 10 years of qualifying payments and employment may also benefit from PSLF, which can be combined with Biden’s broader forgiveness plan for maximum relief.

Practical tips for borrowers include verifying loan types through the Federal Student Aid website and ensuring income documentation is up to date. Borrowers should also monitor updates from the Department of Education, as legal challenges and policy adjustments could alter eligibility criteria. Proactively consolidating FFEL loans into Direct Loans, if necessary, can also ensure qualification for forgiveness. By staying informed and taking these steps, eligible borrowers can maximize their chances of benefiting from Biden’s student loan forgiveness plan.

Student Nurse Loans: Forgiveness Eligibility Explained for Aspiring Nurses

You may want to see also

Explore related products

![]()

Amount of Forgiveness: How much debt will be forgiven per borrower?

The Biden administration's student loan forgiveness plan has been a topic of intense debate and speculation, with borrowers eagerly awaiting details on the amount of debt relief they can expect. While the exact figures remain subject to change, initial proposals suggest a tiered approach based on income and loan type. For instance, individuals earning below $125,000 annually (or $250,000 for married couples) may qualify for up to $10,000 in forgiveness, with an additional $10,000 available for Pell Grant recipients. This structure aims to target relief to those most burdened by debt, particularly low-income borrowers who often struggle with repayment.

Analyzing the proposed amounts, it’s clear that the forgiveness caps are designed to balance fiscal responsibility with meaningful relief. For example, forgiving $10,000 for eligible borrowers could eliminate debt entirely for approximately 15 million individuals, according to estimates from the Department of Education. However, for borrowers with higher balances, such as those in graduate programs or with accrued interest, this amount may only scratch the surface. Critics argue that a one-size-fits-all approach fails to address the disparities in debt levels across different educational paths, while proponents emphasize its potential to provide immediate financial breathing room for millions.

To maximize the impact of forgiveness, borrowers should take proactive steps to ensure eligibility. This includes verifying income levels, confirming Pell Grant status, and consolidating loans if necessary. For instance, borrowers with Federal Family Education Loans (FFEL) not held by the Department of Education may need to consolidate into Direct Loans to qualify. Additionally, staying informed about updates from the Department of Education and avoiding scams promising expedited forgiveness are crucial. Practical tips include setting up notifications for official announcements and keeping detailed records of loan balances and payments.

Comparing Biden’s plan to previous forgiveness programs highlights both its strengths and limitations. For example, the Public Service Loan Forgiveness (PSLF) program offers full debt cancellation after 10 years of qualifying payments but requires a long-term commitment to public service. In contrast, Biden’s proposal provides quicker, albeit partial, relief without such stringent requirements. However, unlike income-driven repayment plans that adjust payments based on earnings, the one-time forgiveness does not address ongoing debt accumulation. This raises questions about the need for systemic reforms to prevent future crises.

Ultimately, the amount of forgiveness per borrower reflects a compromise between political feasibility and the urgent need for relief. While $10,000 or $20,000 may not solve the student debt crisis entirely, it represents a significant step toward alleviating financial strain for millions. Borrowers should remain engaged, advocate for further reforms, and leverage available resources to navigate the complexities of loan forgiveness. As the decision timeline approaches, staying informed and prepared will be key to maximizing the benefits of this historic initiative.

Pennsylvania Student Loan Forgiveness: What Programs Are Available?

You may want to see also

Explore related products

![]()

Legal Challenges: Potential lawsuits delaying Biden’s student loan decision

The Biden administration's student loan forgiveness plan has faced a barrage of legal challenges, creating a complex web of delays and uncertainties. These lawsuits, filed by various groups with differing motivations, threaten to derail the much-anticipated relief for millions of borrowers. Understanding the nature of these legal obstacles is crucial to grasping the timeline for Biden's final decision.

The Legal Landscape: Several lawsuits have emerged, primarily arguing that the administration overstepped its authority in implementing widespread loan forgiveness. One notable case, *Nebraska v. Biden*, challenges the plan on constitutional grounds, claiming it violates the separation of powers. Another lawsuit, filed by the Job Creators Network Foundation, alleges the plan is an abuse of executive power and lacks congressional approval. These cases, currently winding through the court system, have the potential to significantly impact the program's fate.

Impact on Timeline: Legal challenges introduce a critical element of unpredictability. Court proceedings can be lengthy, with appeals and potential Supreme Court involvement further extending the process. This means that even if the administration is confident in its legal standing, the mere existence of these lawsuits could delay the implementation of student loan forgiveness for months or even years. Borrowers, eagerly awaiting relief, are left in a state of limbo, unsure of when or if their debts will be reduced.

Strategic Considerations: The Biden administration must navigate this legal minefield carefully. One strategy could be to expedite the legal process by seeking swift rulings and appealing any adverse decisions promptly. However, this approach carries risks, as rushed decisions might not be in the administration's favor. Alternatively, they could opt for a more cautious approach, allowing the legal process to unfold naturally, but this could mean prolonged uncertainty for borrowers.

Borrower Implications: For those burdened by student debt, these legal challenges are more than just abstract legal debates. They represent a tangible obstacle to financial relief. Borrowers should stay informed about the progress of these lawsuits and consider their individual financial situations. While waiting for a resolution, exploring alternative repayment plans or seeking financial counseling might be prudent steps to manage debt effectively.

In the intricate dance between politics and the judiciary, the fate of Biden's student loan decision hangs in the balance. These legal challenges underscore the complexity of implementing sweeping policy changes and highlight the need for a comprehensive understanding of the legal system's role in shaping such decisions. As the court battles continue, borrowers can only wait and hope for a swift and favorable resolution.

When Can College Students Expect a $500 Financial Boost?

You may want to see also

Explore related products

![]()

Payment Restart Date: When will student loan payments resume after forgiveness?

The Biden administration's student loan forgiveness plan has left many borrowers wondering: when will payments resume? The answer is not as straightforward as a single date. The restart hinges on a complex interplay of legal challenges, political maneuvering, and the Supreme Court's decision on the forgiveness program itself.

As of October 2023, payments are scheduled to resume 60 days after the Department of Education is permitted to implement the program, or 60 days after June 30, 2023, whichever comes first. However, this timeline is contingent on the Supreme Court upholding the forgiveness plan. If the Court strikes it down, payments could resume as early as summer 2023.

Borrowers should prepare for a potential restart by reviewing their loan servicer information, updating contact details, and exploring repayment options. The Department of Education's website offers resources to help borrowers understand their options, including income-driven repayment plans that can lower monthly payments based on income and family size.

It's crucial to remember that interest will begin accruing again once payments resume. Borrowers who can afford to make payments before the official restart date can reduce the total amount they owe over the life of the loan. Even small payments can make a difference, especially for those with high-interest loans.

For those facing financial hardship, contacting the loan servicer to discuss options is essential. Deferment or forbearance may be available, but these options should be used sparingly as interest continues to accrue during these periods.

The uncertainty surrounding the payment restart date highlights the need for borrowers to stay informed and proactive. By understanding the potential scenarios and taking steps to prepare, borrowers can navigate the transition back to repayment with greater confidence and financial stability.

Australia's Border Reopening: When Can Indian Students Return?

You may want to see also

Frequently asked questions

As of the latest updates, President Biden has not announced a specific date for a final decision on widespread student loan forgiveness. The administration continues to review options, and any announcement is expected to come before the current payment pause ends.

The extent of student loan forgiveness remains uncertain. Proposals range from $10,000 to $50,000 per borrower, but no final decision has been made. The administration is considering income limits and other eligibility criteria.

Student loan payments are currently paused until August 30, 2023. The Biden administration is expected to make a decision on forgiveness before payments resume, but no guarantees have been made.

If forgiveness is approved, the Department of Education will likely provide guidance on eligibility criteria and application processes. Borrowers should monitor official channels for updates.

If the plan faces legal challenges, implementation could be delayed or altered. The administration has stated it is prepared to defend its actions, but the outcome would depend on court rulings.

![EidolonGreen [China Medicinal Herb] Bidens Tripartita(Bidens Tripartita L./Trifid Bur-marigold/Gui Zhen Cao/鬼针草/귀신침 초) Dried Bulk Herb 3 Oz (88 g)](https://m.media-amazon.com/images/I/61B8U7-NK2S._AC_UL320_.jpg)