Navigating the complexities of student loan forgiveness can be overwhelming, especially when trying to determine when your $10,000 student loan might be forgiven. The timeline for loan forgiveness depends on various factors, including the type of loan, repayment plan, and eligibility for specific forgiveness programs such as Public Service Loan Forgiveness (PSLF) or income-driven repayment plans. For instance, under PSLF, borrowers may qualify for forgiveness after 120 qualifying payments, typically around 10 years, while income-driven plans can offer forgiveness after 20-25 years of payments. Understanding your loan terms, exploring available programs, and staying informed about policy changes are crucial steps in determining when your $10,000 student loan might be forgiven.

| Characteristics | Values |

|---|---|

| Eligibility | Borrowers with federal student loans earning below $125,000 (individuals) or $250,000 (married couples) annually. |

| Loan Type | Federal student loans held by the U.S. Department of Education. |

| Forgiveness Amount | Up to $10,000 in forgiveness. |

| Additional Forgiveness for Pell Grant Recipients | Up to $20,000 in forgiveness. |

| Application Process | Automatic for most borrowers if income data is available; otherwise, apply via a form (released by the Department of Education). |

| Deadline to Apply | December 31, 2023 (extended deadline). |

| Loan Status | Loans must be in repayment, grace period, deferment, or forbearance. |

| Excluded Loans | Private student loans and some federally owned FFELP loans not held by the Department of Education. |

| Tax Implications | Forgiveness is tax-free at the federal level. |

| Impact on Credit Score | No negative impact on credit score. |

| Current Status | Program is active but subject to legal challenges. |

| Updates | Borrowers should monitor the Department of Education’s website for updates. |

Explore related products

What You'll Learn

![]()

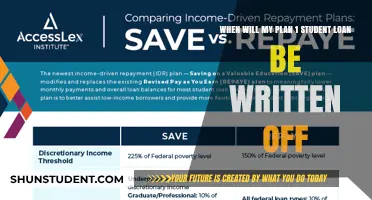

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans are a lifeline for borrowers juggling federal student loans, particularly those with high debt relative to their income. These plans cap monthly payments at a percentage of discretionary income—typically 10% to 20%, depending on the plan—and recalculate payments annually based on updated income and family size. For example, if you earn $40,000 annually and have a family of two, your payment under the Revised Pay As You Earn (REPAYE) plan would be roughly $200 per month, compared to the standard $1000+ payment on a $10,000 loan. This flexibility ensures payments remain manageable, even during periods of low earnings.

The real game-changer with IDR plans is their pathway to loan forgiveness. After 20 to 25 years of qualifying payments, any remaining balance is forgiven, though borrowers may owe taxes on the forgiven amount. For instance, if you’re on the Income-Based Repayment (IBR) plan and consistently make payments for 25 years, your $10,000 loan could be wiped clean, even if only a fraction was repaid. However, this timeline shortens for certain borrowers under recent policy changes. For example, the 2023 IDR Account Adjustment allows borrowers to receive credit toward forgiveness for months spent in any repayment status, including forbearance or deferment, potentially shaving years off their timeline.

Choosing the right IDR plan requires careful consideration. REPAYE, for instance, is ideal for borrowers expecting income growth, as it caps payments at 10% of discretionary income but doesn’t limit interest accrual. In contrast, Pay As You Earn (PAYE) limits payments to 10% and caps interest, making it better for those with steady, lower incomes. Married borrowers should also weigh filing taxes separately to exclude their spouse’s income from payment calculations, though this may not always be financially advantageous.

One critical caveat: IDR plans aren’t a one-size-fits-all solution. They’re best for borrowers with high debt-to-income ratios or those pursuing public service. For example, a teacher with $50,000 in loans and a $35,000 salary would benefit far more than a software engineer with the same debt but a $90,000 salary. Additionally, private loans aren’t eligible for IDR plans, and enrolling in one may extend the repayment period, increasing total interest paid unless forgiveness is achieved.

To maximize IDR benefits, borrowers should annually recertify their income and family size promptly to avoid payment spikes. Tools like the Federal Student Aid Loan Simulator can help estimate payments and forgiveness timelines under different plans. For those nearing the 20- to 25-year mark, tracking payment counts via the loan servicer’s portal is crucial, as errors in counting qualifying payments are common. With strategic planning, IDR plans can transform a $10,000 loan from a burden into a manageable, forgivable obligation.

Do You Qualify for Student Debt Forgiveness? Key Eligibility Criteria Explained

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF)

To navigate PSLF effectively, start by confirming your employer’s eligibility using the Federal Student Aid Employer Search Tool. Nonprofits must be tax-exempt under Section 501(c)(3), and government organizations at any level qualify. Next, consolidate any non-Direct Loans into a Direct Consolidation Loan to make them eligible. Once enrolled, track your progress meticulously. Submit the Employment Certification Form annually or whenever you change jobs to ensure each payment counts toward the 120 required. This proactive approach prevents costly mistakes, such as discovering years later that payments were misapplied due to administrative errors.

A common misconception is that PSLF forgives loans after 10 years regardless of the remaining balance. In reality, the program forgives the *remaining* balance after 120 qualifying payments, not the original loan amount. This distinction is vital for borrowers with high balances, as staying in an income-driven plan can significantly reduce monthly payments, making the 10-year commitment more manageable. For example, a borrower earning $50,000 annually with $100,000 in debt might pay as little as $200 monthly under the Revised Pay As You Earn (REPAYE) plan, compared to $1,000 under the Standard plan.

Critics argue that PSLF’s complexity discourages participation, but its benefits far outweigh the administrative burden for eligible borrowers. The program’s forgiveness is tax-free, unlike income-driven plans, which may tax forgiven amounts as income. Additionally, PSLF complements other relief efforts, such as the recent one-time $10,000 forgiveness for federal borrowers. However, these initiatives are temporary, while PSLF remains a permanent option for those in public service. By combining PSLF with strategic repayment planning, borrowers can achieve financial freedom without sacrificing their commitment to serving the public.

Consolidate Student Loans and Unlock Forgiveness: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness Program

Teachers burdened by student loan debt have a powerful ally in the Teacher Loan Forgiveness Program. This federal initiative offers a substantial financial incentive for educators committed to serving in low-income schools.

Eligibility hinges on three key factors: five consecutive, complete academic years of teaching, employment at a designated low-income school, and status as a highly qualified teacher. "Highly qualified" means meeting state standards for licensing, holding a bachelor's degree, and demonstrating subject matter competence.

Those who meet these criteria can receive up to $17,500 in loan forgiveness, a significant chunk of change for most borrowers.

The forgiveness amount varies based on subject area. Secondary school teachers in math, science, or special education are eligible for the full $17,500. Elementary and other secondary teachers can receive up to $5,000. This tiered system acknowledges the critical need for specialized educators in high-demand fields.

Navigating the application process requires attention to detail. Teachers must submit an application after completing their five years of service, along with certification from their school's chief administrative officer. It's crucial to keep meticulous records of employment and qualifications throughout the five-year period.

While the Teacher Loan Forgiveness Program won't erase all student debt, it provides a substantial financial reward for those dedicating themselves to educating students in underserved communities.

Forgiving Student Loans: Economic Impact and Long-Term Consequences Explored

You may want to see also

Explore related products

![]()

Loan Forgiveness After 20-25 Years

For borrowers enrolled in income-driven repayment (IDR) plans, the clock is ticking toward potential loan forgiveness after 20 to 25 years of qualifying payments. This timeline isn’t arbitrary—it’s a lifeline built into federal programs like Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR). Each plan has its own eligibility rules and payment caps tied to discretionary income, but they share a common endgame: forgiveness of any remaining balance after the designated period. For example, REPAYE forgives loans after 20 years for undergraduate borrowers and 25 years for graduate borrowers, while IBR offers forgiveness after 20 or 25 years depending on when the loan was taken out.

Understanding the mechanics of this forgiveness is critical. Qualifying payments include those made under an IDR plan, during periods of economic hardship deferment, or while working in a public service role (though Public Service Loan Forgiveness operates on a separate 10-year timeline). Partial payments, late payments, or payments made under standard repayment plans do not count. Borrowers must recertify their income and family size annually to remain in an IDR plan, ensuring payments stay aligned with their financial situation. Failure to recertify can result in being switched to a standard plan, resetting the forgiveness clock.

A common pitfall is underestimating the tax implications of loan forgiveness. When loans are forgiven after 20–25 years, the IRS may treat the forgiven amount as taxable income, potentially resulting in a hefty bill. However, the American Rescue Plan Act of 2021 temporarily exempts forgiven student loans from federal taxation through 2025. Borrowers should consult a tax professional to plan for potential changes after this deadline. Additionally, some states may still tax forgiven amounts, so state-specific rules must be reviewed.

Strategic planning can maximize the benefits of this forgiveness pathway. For instance, borrowers with both undergraduate and graduate loans may benefit from consolidating to align their repayment terms. Those nearing the 20–25-year mark should ensure all payments have been accurately tracked by their loan servicer, as errors are common. Tools like the National Student Loan Data System (NSLDS) can help verify payment counts. Finally, staying informed about policy changes—such as the recent IDR Account Adjustment, which retroactively credited certain deferment and forbearance periods toward forgiveness—can accelerate progress toward the finish line.

In summary, loan forgiveness after 20–25 years is a structured yet nuanced process requiring proactive management. By choosing the right IDR plan, maintaining compliance, and anticipating tax consequences, borrowers can navigate this path effectively. While the journey is lengthy, the potential payoff—freedom from tens of thousands in debt—makes it a strategy worth pursuing for those eligible.

Understanding Student Loan Forgiveness: Payments Timeline and Eligibility Criteria

You may want to see also

Explore related products

![]()

Disability or Death Discharge

In the realm of student loan forgiveness, certain life-altering events can expedite the discharge process, offering a glimmer of hope to borrowers facing insurmountable challenges. One such provision is the Disability or Death Discharge, a critical yet often overlooked pathway to relief. This mechanism acknowledges the harsh reality that not all borrowers will be able to fulfill their repayment obligations due to circumstances beyond their control. For those grappling with the question, "When will my 10k student loan be forgiven?" understanding this discharge option could be the key to unlocking financial freedom.

Consider the case of a borrower diagnosed with a permanent disability that renders them unable to work. The Total and Permanent Disability (TPD) Discharge allows federal student loans to be forgiven entirely. To qualify, borrowers must provide documentation from the U.S. Department of Veterans Affairs, the Social Security Administration, or a physician certifying their condition. For Social Security Disability Insurance (SSDI) recipients, the process is streamlined, with the Department of Education automatically initiating a review after three years of payments. However, borrowers on Supplemental Security Income (SSI) must apply manually. This distinction highlights the importance of understanding the nuances of the application process to avoid unnecessary delays.

Equally significant is the Death Discharge, which forgives federal student loans upon the borrower’s passing. This provision ensures that surviving family members are not burdened with the deceased’s educational debt. The process requires submitting a certified copy of the death certificate to the loan servicer. Notably, Parent PLUS loans are also eligible for discharge if the parent borrower or the student on whose behalf the loan was taken passes away. This aspect underscores the program’s inclusivity, addressing a broader spectrum of familial financial responsibilities.

While these discharges offer relief, they are not without potential pitfalls. For instance, TPD discharges may be subject to a three-year monitoring period during which borrowers must meet certain income requirements to avoid reinstatement of the loan. Additionally, forgiven amounts may be considered taxable income, though recent legislation has temporarily waived taxes on TPD discharges through 2025. Borrowers must also be vigilant about private loans, as they typically do not offer similar discharge options, emphasizing the need to review loan terms carefully.

In conclusion, the Disability or Death Discharge serves as a vital safety net within the student loan forgiveness landscape. By familiarizing themselves with the eligibility criteria, application processes, and associated nuances, borrowers can navigate this pathway with greater confidence. For those facing permanent disability or dealing with the loss of a loved one, this provision not only alleviates financial strain but also provides a measure of dignity during challenging times. It is a reminder that, in the face of adversity, there are mechanisms designed to offer relief—one just needs to know where to look.

Did I Apply for Student Loan Forgiveness? Check Your Status Now

You may want to see also

Frequently asked questions

The timing of $10,000 student loan forgiveness depends on the program. For those eligible under the Biden administration’s 2022 plan, forgiveness was expected to begin in late 2022 or early 2023, but legal challenges delayed implementation. Check the Department of Education’s updates for the latest status.

Borrowers with federal student loans earning less than $125,000 (individuals) or $250,000 (married couples) annually qualify for $10,000 in forgiveness. Pell Grant recipients may qualify for up to $20,000. Private loans are not eligible.

Yes, borrowers must submit an application for forgiveness, though the process was paused due to legal challenges. Monitor the Federal Student Aid website for updates on when the application will reopen.

If your loan balance is less than $10,000, the forgiveness will cover the remaining balance, reducing it to $0. It will not provide additional funds or refunds for overpayment.