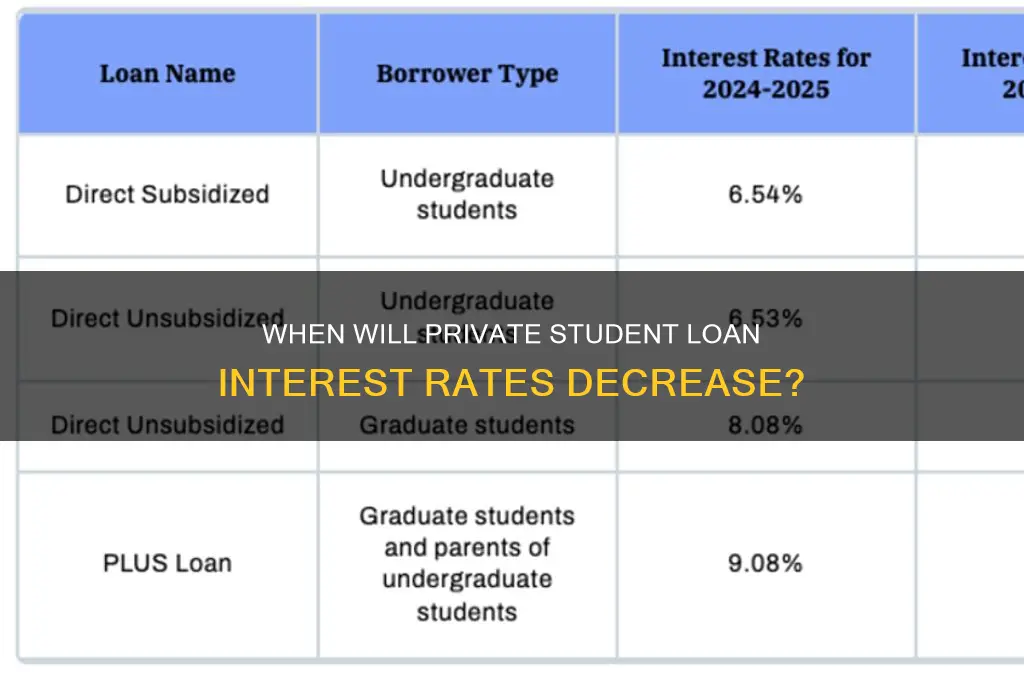

Private student loan interest rates are influenced by broader economic factors, including the Federal Reserve’s monetary policy, inflation, and market conditions. As of now, rates remain elevated due to persistent inflation and higher benchmark interest rates set by the Fed. However, economists predict that as inflation continues to ease and the Fed begins to lower rates, private student loan interest rates could follow suit. Borrowers should monitor economic indicators and consider refinancing options when rates decline, though timing remains uncertain and dependent on the pace of economic stabilization.

| Characteristics | Values |

|---|---|

| Current Trend (as of October 2023) | Private student loan interest rates remain high due to Federal Reserve rate hikes. |

| Federal Reserve Influence | Private loan rates are tied to benchmark rates (e.g., SOFR, LIBOR), which follow Fed actions. |

| Next Fed Meeting | November 2023 (potential pause or cut depends on inflation data). |

| Projected Rate Cut Timeline | Mid-to-late 2024, if inflation stabilizes and Fed begins easing rates. |

| Market Expectations | Economists predict 1-2 rate cuts in 2024, lowering benchmark rates. |

| Impact on Private Loans | Variable-rate loans may decrease; fixed rates depend on lender policies and market conditions. |

| Economic Factors | Inflation, unemployment, and GDP growth will drive Fed decisions. |

| Lender Competition | Increased competition among lenders could lower rates independently of Fed actions. |

| Refinancing Opportunities | Borrowers may see better refinancing options in 2024 if rates decline. |

| Historical Context | Rates peaked in 2023 due to aggressive Fed hikes; gradual decline expected post-2024. |

Explore related products

What You'll Learn

![]()

Economic Factors Influencing Rates

Private student loan interest rates are intricately tied to broader economic conditions, making them a barometer of financial health and market expectations. One of the most significant factors is the Federal Reserve’s monetary policy. When the Fed raises benchmark interest rates to combat inflation, private lenders often follow suit, increasing borrowing costs for students. Conversely, during periods of economic downturn or deflationary pressure, the Fed may lower rates, creating a ripple effect that could reduce private student loan interest rates. For instance, the Fed’s rate cuts during the 2020 pandemic temporarily eased borrowing costs, though private loan rates remained higher than federal alternatives due to perceived risk.

Another critical economic factor is the yield on Treasury bonds, which serves as a benchmark for many lending products, including private student loans. When Treasury yields rise, lenders typically adjust their rates upward to maintain profit margins. This relationship is particularly evident in variable-rate loans, where interest rates fluctuate with market conditions. Borrowers with variable-rate loans should monitor Treasury yields closely, as even small changes can significantly impact monthly payments. For example, a 1% increase in the 10-year Treasury yield could translate to hundreds of dollars in additional interest over the life of a loan.

The health of the labor market also plays a subtle yet influential role in private student loan rates. A strong job market with rising wages can reduce the perceived risk of default, encouraging lenders to offer lower rates. Conversely, high unemployment or underemployment rates may lead lenders to increase rates to offset potential losses. During the Great Recession, for instance, private student loan rates climbed as lenders grew cautious about borrowers’ ability to repay. Prospective borrowers can use labor market indicators, such as unemployment rates and wage growth, as informal gauges of future rate trends.

Finally, inflation expectations shape lender behavior in setting private student loan rates. When inflation is expected to rise, lenders factor in the eroding value of future repayments, often raising rates to preserve real returns. Borrowers can track inflation forecasts from institutions like the Federal Reserve or the Bureau of Labor Statistics to anticipate rate movements. For example, if inflation is projected to exceed 3% annually, lenders may preemptively increase rates by 0.5% to 1% to protect their margins. Understanding these economic indicators empowers borrowers to time their loan applications strategically, potentially locking in lower rates during favorable conditions.

Student Loan Forgiveness Applications: When and How to Apply

You may want to see also

Explore related products

![]()

Federal Reserve Policy Impact

The Federal Reserve's monetary policy decisions are a critical factor in determining when private student loan interest rates might decrease. As the central banking system of the United States, the Fed's primary tools for influencing the economy include adjusting the federal funds rate, which is the interest rate at which banks lend to each other overnight. When the Fed lowers this rate, it typically leads to a reduction in borrowing costs across the economy, including private student loans.

Understanding the Mechanism

When the Federal Reserve cuts interest rates, it aims to stimulate economic activity by making borrowing cheaper. For private student loan lenders, this means their cost of funds decreases, allowing them to offer lower interest rates to borrowers. However, the extent to which these reductions are passed on depends on market competition, lender profit margins, and the overall economic environment. For instance, during the COVID-19 pandemic, the Fed slashed rates to near zero, yet private student loan rates remained relatively high due to perceived borrower risk and administrative costs.

Timing and Economic Indicators

Borrowers should monitor key economic indicators that influence Fed policy, such as inflation rates, unemployment data, and GDP growth. Historically, the Fed lowers rates during economic downturns or periods of low inflation to encourage spending and investment. For example, in 2020, the Fed’s aggressive rate cuts were a response to the pandemic-induced recession. Conversely, during inflationary periods, like in 2022, the Fed raises rates to cool the economy, which can delay reductions in private student loan interest rates.

Practical Tips for Borrowers

To maximize the benefits of potential rate decreases, borrowers should consider refinancing existing private student loans when the Fed lowers rates. Refinancing allows borrowers to replace their current loan with a new one at a lower interest rate, potentially saving thousands of dollars over the loan term. Additionally, maintaining a strong credit profile and shopping around for competitive offers can further enhance savings. Tools like rate comparison websites and financial advisors can help borrowers navigate these opportunities effectively.

Long-Term Outlook

While the Federal Reserve’s actions are a significant driver of private student loan rates, they are not the sole determinant. Market conditions, lender policies, and legislative changes also play crucial roles. For instance, federal student loan rates are set by Congress and are not directly tied to the Fed’s decisions. Borrowers should stay informed about broader financial trends and consider diversifying their debt management strategies, such as exploring income-driven repayment plans or pursuing loan forgiveness programs where applicable. By understanding the interplay between Fed policy and private loan rates, borrowers can make more informed decisions about when and how to secure lower interest rates.

Will Accrued Student Loan Interest Be Forgiven? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Market Competition Trends

Private student loan interest rates are influenced by market competition, which can drive lenders to offer more favorable terms to attract borrowers. One key trend is the rise of fintech companies and online lenders entering the student loan space. These platforms often leverage technology to streamline the application process, reduce overhead costs, and pass savings onto borrowers in the form of lower interest rates. For example, companies like SoFi and Earnest have gained traction by offering variable rates starting as low as 4.5% APR for well-qualified applicants, compared to traditional banks that may charge upwards of 8-12% APR. This competitive pressure forces established lenders to reevaluate their pricing strategies, potentially leading to broader rate reductions across the market.

Another significant trend is the increasing transparency and comparison tools available to borrowers. Websites like Credible and LendEDU allow students to compare private loan offers from multiple lenders side by side, highlighting interest rates, repayment terms, and fees. This democratization of information empowers borrowers to make informed decisions, incentivizing lenders to compete on price and flexibility. For instance, a borrower with a credit score above 720 might qualify for rates 2-3% lower than average by shopping around, a practice that was less feasible before these platforms existed. As more borrowers utilize these tools, lenders are compelled to lower rates to remain competitive.

However, market competition alone may not be enough to drive rates down significantly without broader economic shifts. The Federal Reserve’s monetary policy plays a critical role, as private student loan rates are often tied to benchmark rates like the LIBOR or SOFR. When the Fed lowers interest rates, lenders’ funding costs decrease, allowing them to offer lower rates to borrowers. For example, during the 2020-2021 period of historically low federal funds rates, some private lenders temporarily reduced their variable rates to as low as 1-2% APR for introductory periods. Borrowers should monitor these macroeconomic trends and consider refinancing when rates are favorable.

A cautionary note: while competition can lead to lower rates, it also introduces risks for borrowers. Some lenders may offer low introductory rates but include variable terms that can increase significantly over time. For example, a loan with a starting rate of 3% APR might adjust to 10% or higher after six months, depending on market conditions. Borrowers should carefully review loan agreements, focusing on the APR cap and repayment terms, to avoid unexpected costs. Additionally, federal student loans often offer fixed rates and borrower protections that private loans lack, making them a safer option for some students despite potentially higher rates.

In conclusion, market competition is a driving force behind the potential reduction of private student loan interest rates, but borrowers must navigate this landscape strategically. By leveraging fintech platforms, comparison tools, and economic trends, students can secure more favorable terms. However, they should remain vigilant about hidden costs and consider the long-term implications of variable rates. As competition intensifies, informed borrowers are best positioned to benefit from downward rate pressures.

Why Didn't I Get Student Loan Forgiveness? Understanding the Reasons

You may want to see also

Explore related products

![]()

Legislative Changes Possibilities

Private student loan interest rates are largely influenced by market conditions, but legislative changes can play a pivotal role in shaping their trajectory. One potential avenue for reducing these rates lies in federal policy reforms that directly target the cost of borrowing. For instance, Congress could introduce legislation capping private student loan interest rates, similar to measures taken in other consumer lending markets. Such a cap would prevent lenders from charging exorbitant rates, especially during periods of economic uncertainty or rising federal interest rates. This approach would require bipartisan support and careful drafting to avoid unintended consequences, such as reduced access to loans for high-risk borrowers.

Another legislative possibility involves incentivizing lenders to lower rates through tax benefits or subsidies. By offering financial incentives to private lenders who reduce interest rates for student borrowers, lawmakers could encourage more competitive pricing. For example, a tiered tax credit system could reward lenders based on the extent to which they lower rates below a certain threshold. This strategy not only benefits borrowers but also aligns with broader economic goals of reducing student debt burdens. However, critics might argue that such subsidies could strain federal budgets, necessitating a balanced approach to ensure fiscal responsibility.

A third avenue for legislative intervention is the expansion of income-driven repayment plans to include private student loans. Currently, these plans are primarily available for federal loans, leaving private borrowers with fewer options for managing their debt. By extending such protections, lawmakers could indirectly reduce the perceived risk for private lenders, potentially leading to lower interest rates. This change would require collaboration between federal and state regulators to ensure consistent implementation across jurisdictions. Borrowers would need clear guidance on eligibility and application processes, making public awareness campaigns a critical component of this reform.

Lastly, legislative efforts could focus on increasing transparency and regulation in the private student loan market. Stricter oversight of lending practices, including clearer disclosure requirements and penalties for predatory behavior, could create a fairer environment for borrowers. For instance, mandating that lenders provide personalized interest rate estimates based on creditworthiness could empower students to make more informed decisions. While this approach may not directly lower rates, it could foster market competition and reduce instances of borrowers accepting unfavorable terms out of necessity.

In summary, legislative changes offer a multifaceted approach to reducing private student loan interest rates. From direct rate caps to indirect incentives and regulatory reforms, each strategy presents unique opportunities and challenges. Borrowers, lenders, and policymakers must work together to craft solutions that balance affordability with market sustainability, ensuring that future generations have access to education without being burdened by insurmountable debt.

Student Nurse Loans: Forgiveness Eligibility Explained for Aspiring Nurses

You may want to see also

Explore related products

$8.34 $17.99

![]()

Historical Rate Fluctuations Analysis

Private student loan interest rates have historically been influenced by broader economic trends, particularly the Federal Reserve’s monetary policy and market conditions. A review of the past two decades reveals distinct patterns: during periods of economic expansion, such as the mid-2000s and late 2010s, rates tended to rise as the Fed increased benchmark interest rates to control inflation. Conversely, during recessions or economic downturns, like the 2008 financial crisis and the COVID-19 pandemic, rates dropped sharply as the Fed lowered rates to stimulate the economy. For instance, private student loan rates plummeted from an average of 12% in 2008 to around 6% in 2020, mirroring the Fed’s aggressive rate cuts.

To predict when private student loan rates might decrease, examine the relationship between the Fed’s actions and lender behavior. Lenders typically adjust their rates within 3–6 months of a Fed rate change, but the magnitude of the adjustment varies based on market competition and credit risk. For example, during the 2020 rate cuts, some lenders reduced rates by as much as 2 percentage points, while others maintained higher margins due to economic uncertainty. Borrowers should monitor Fed announcements and track lender responses to identify potential rate decreases.

A comparative analysis of historical rate fluctuations highlights the importance of timing. Refinancing during a rate-lowering cycle can yield significant savings. For instance, a borrower with a $30,000 loan at 8% interest could save over $5,000 in interest payments by refinancing to a 5% rate. However, refinancing is most advantageous for those with strong credit scores (typically 700+), stable income, and a low debt-to-income ratio. Borrowers with weaker financial profiles may not qualify for the lowest rates, even during favorable market conditions.

Practical steps for borrowers include setting up rate alerts from financial platforms like Credible or LendingTree, which notify users of market changes. Additionally, maintaining a healthy credit profile—by paying bills on time, reducing credit card balances, and avoiding new debt—can position borrowers to capitalize on rate decreases when they occur. For those with existing loans, consider a variable-rate option if rates are expected to decline further, but be cautious of potential increases in the future.

In conclusion, historical rate fluctuations demonstrate that private student loan interest rates are deeply tied to macroeconomic conditions and Fed policy. By understanding these patterns and taking proactive steps, borrowers can strategically time refinancing decisions to minimize long-term costs. While predicting exact rate movements remains challenging, staying informed and prepared can provide a significant financial advantage.

Is Navient Student Loan Forgiveness Real? What Borrowers Need to Know

You may want to see also

Frequently asked questions

Private student loan interest rates are influenced by market conditions, primarily the Federal Reserve’s benchmark interest rate and lender competition. Rates may decrease when the Federal Reserve lowers rates or when economic conditions improve, but the timing is unpredictable.

Private student loan rates are tied to the prime rate, creditworthiness of the borrower, and overall economic health. A decline in the prime rate, reduced inflation, or increased competition among lenders could lead to lower rates.

Yes, if private student loan interest rates decrease, you may be able to refinance your loans at a lower rate, provided you meet the lender’s eligibility criteria, such as having a good credit score and stable income.