The ongoing freeze on federal student loan payments, interest, and collections, implemented as part of pandemic relief measures, has provided significant financial breathing room for millions of borrowers. However, as the pause is set to expire, many are left wondering: when will the student loan freeze end? The current extension, announced by the U.S. Department of Education, is scheduled to conclude on a specific date, after which borrowers will need to resume payments. This impending deadline has sparked concerns about financial preparedness, loan forgiveness programs, and the broader implications for the economy. As borrowers await further guidance, staying informed about potential updates and planning for repayment is crucial to navigating this transition smoothly.

Explore related products

What You'll Learn

- Current Freeze End Date: Official deadline for the student loan payment freeze to expire

- Potential Extensions: Possibility of further delays beyond the announced freeze end date

- Government Announcements: Updates from officials regarding the freeze’s termination timeline

- Impact on Borrowers: How the freeze’s end affects repayment plans and financial obligations

- Post-Freeze Policies: New rules or programs expected after the freeze concludes

![]()

Current Freeze End Date: Official deadline for the student loan payment freeze to expire

The student loan payment freeze, a lifeline for millions during the pandemic, is set to expire on August 31, 2022, as announced by the U.S. Department of Education. This date marks the end of a moratorium that has paused federal student loan payments, waived interest, and halted collections on defaulted loans since March 2020. Borrowers have grown accustomed to this financial reprieve, but the clock is ticking toward a return to regular repayment obligations. Understanding this deadline is crucial for anyone with federal student loans, as it directly impacts budgeting, financial planning, and long-term debt management strategies.

Analyzing the implications of this end date reveals both challenges and opportunities. For many, the freeze has provided a buffer to save money, pay down other debts, or simply stabilize finances during economic uncertainty. However, resuming payments could strain budgets, especially for those who have not worked consistently during the pandemic. The Department of Education has urged borrowers to prepare by updating contact information, reviewing repayment plans, and exploring options like income-driven repayment or loan consolidation. Ignoring this deadline could lead to missed payments, accruing interest, and potential damage to credit scores.

From a practical standpoint, borrowers should take immediate steps to ensure a smooth transition. First, log into your loan servicer’s website to confirm your current balance, interest rate, and monthly payment amount. Second, consider enrolling in autopay to secure a 0.25% interest rate reduction and avoid late payments. Third, if your financial situation has changed, explore deferment, forbearance, or income-driven repayment plans before the freeze ends. Proactive planning can mitigate the shock of resuming payments and help maintain financial stability.

Comparatively, this freeze end date stands out as a critical juncture in the broader student loan landscape. Unlike previous extensions, this deadline appears firm, with no immediate indications of further postponement. This contrasts with the multiple extensions granted throughout the pandemic, which often left borrowers in limbo. The August 31 deadline underscores the need for borrowers to act decisively, as reliance on another extension could lead to unpreparedness and financial hardship.

In conclusion, the August 31, 2022, deadline for the student loan payment freeze to expire is a pivotal moment for borrowers. It demands attention, preparation, and strategic planning to navigate the transition back to repayment. By understanding the specifics of this deadline and taking proactive steps, borrowers can minimize stress and set themselves up for financial success in the post-freeze era.

Unlock Automatic Student Loan Forgiveness: Eligibility and Steps to Qualify

You may want to see also

Explore related products

![]()

Potential Extensions: Possibility of further delays beyond the announced freeze end date

The student loan freeze, initially slated to end in September 2023, has already seen multiple extensions due to economic uncertainties and political maneuvering. This pattern raises a critical question: could further delays be on the horizon? Historical precedent suggests that when financial relief measures are tied to broader economic recovery, their expiration dates often become flexible. For instance, the CARES Act’s forbearance provisions were extended three times as unemployment rates and inflation persisted. If current economic indicators—such as stagnant wage growth or rising living costs—fail to improve, policymakers may face pressure to prolong the freeze again, especially in an election year.

Analyzing the political landscape reveals another layer of potential for extension. Student loan debt is a polarizing issue, with Democrats often advocating for relief and Republicans pushing for fiscal restraint. However, both parties have historically used extensions as a tool to appease voters during times of economic stress. For example, the 2022 midterm elections saw a last-minute extension tied to campaign promises. With the 2024 election cycle approaching, another delay could serve as a strategic move to garner support from younger, debt-burdened voters. Watch for legislative proposals or executive orders in the months leading up to the election as key indicators of this possibility.

From a practical standpoint, borrowers should prepare for both scenarios: the freeze ending as scheduled or being extended. Start by calculating your monthly payments based on your current loan terms and explore income-driven repayment plans or refinancing options if necessary. However, avoid making lump-sum payments toward your principal until the freeze’s fate is clear, as any extension would pause interest accrual again. Instead, allocate those funds to high-interest debt or an emergency savings account. Staying informed through official channels like the Department of Education’s website or trusted financial news sources will ensure you’re not caught off guard.

Comparatively, other countries’ approaches to student debt offer insight into potential long-term solutions. For instance, Germany and Norway provide tuition-free higher education, while Australia uses income-contingent loan systems with no fixed repayment schedules. While such models may not be immediately replicable in the U.S., they highlight alternatives to temporary freezes. If extensions continue without addressing systemic issues, public demand for more permanent reforms could grow, potentially reshaping the debate around student loans entirely.

In conclusion, while the announced end date for the student loan freeze stands, economic and political factors create a plausible case for further delays. Borrowers should remain proactive, balancing preparation for repayment with flexibility should another extension occur. As this issue evolves, it may also catalyze broader conversations about sustainable solutions to the student debt crisis, moving beyond temporary fixes to more enduring policy changes.

How Student Loan Forgiveness Impacts Your Credit Score: What to Know

You may want to see also

Explore related products

![]()

Government Announcements: Updates from officials regarding the freeze’s termination timeline

The student loan freeze, a lifeline for millions during the pandemic, has been extended multiple times, leaving borrowers in a state of uncertainty. Government officials have been tight-lipped about a definitive end date, but recent announcements provide clues. In a press conference last month, the Secretary of Education hinted at a phased approach, suggesting that the freeze might conclude in stages rather than abruptly. This strategy aims to cushion the financial blow for borrowers, many of whom have grown accustomed to the payment pause. While no exact date has been confirmed, the tone of these updates indicates that a decision is imminent, with officials emphasizing the need for a balanced approach that considers both economic recovery and borrower readiness.

Analyzing the pattern of past extensions, it’s evident that the government has been responsive to economic indicators and public sentiment. For instance, the last extension was announced just weeks before the scheduled end date, citing concerns over inflation and job market instability. Borrowers should monitor key economic reports, such as unemployment rates and inflation data, as these will likely influence future decisions. Additionally, staying informed through official channels like the Department of Education’s website or press releases can provide real-time updates. Proactive steps, like recalibrating budgets or exploring repayment plans, could mitigate the impact once the freeze ends.

Persuasively, it’s worth noting that the freeze’s termination is not just a financial issue but a political one. Officials are walking a tightrope between fiscal responsibility and voter satisfaction, particularly with elections on the horizon. Advocacy groups have been vocal, urging lawmakers to either extend the freeze further or implement long-term debt relief measures. Borrowers can amplify their voices by engaging with these groups or contacting their representatives directly. A collective push for clarity and fairness could sway the timeline in favor of those most affected.

Comparatively, the U.S. approach to student loan freezes differs significantly from other countries. For example, Canada implemented a permanent interest-free policy for federal student loans, while the U.K. ties repayment thresholds to income levels. These examples highlight alternative solutions that U.S. officials might consider as they navigate the freeze’s end. Borrowers could benefit from understanding these global models, as they may foreshadow potential policy shifts domestically.

Descriptively, the anticipation surrounding the freeze’s end is palpable, with forums and social media buzzing with speculation. Officials have acknowledged this anxiety, promising transparency in their decision-making process. However, the lack of a concrete date has left many in limbo, juggling financial plans and life decisions. Practical steps, such as enrolling in auto-pay to secure interest rate reductions or exploring loan consolidation, can provide a sense of control. As the government continues to deliberate, borrowers must stay informed, prepared, and engaged to navigate the transition effectively.

Student Loan Forgiveness: Economic Pitfalls and Long-Term Consequences Explained

You may want to see also

Explore related products

![]()

Impact on Borrowers: How the freeze’s end affects repayment plans and financial obligations

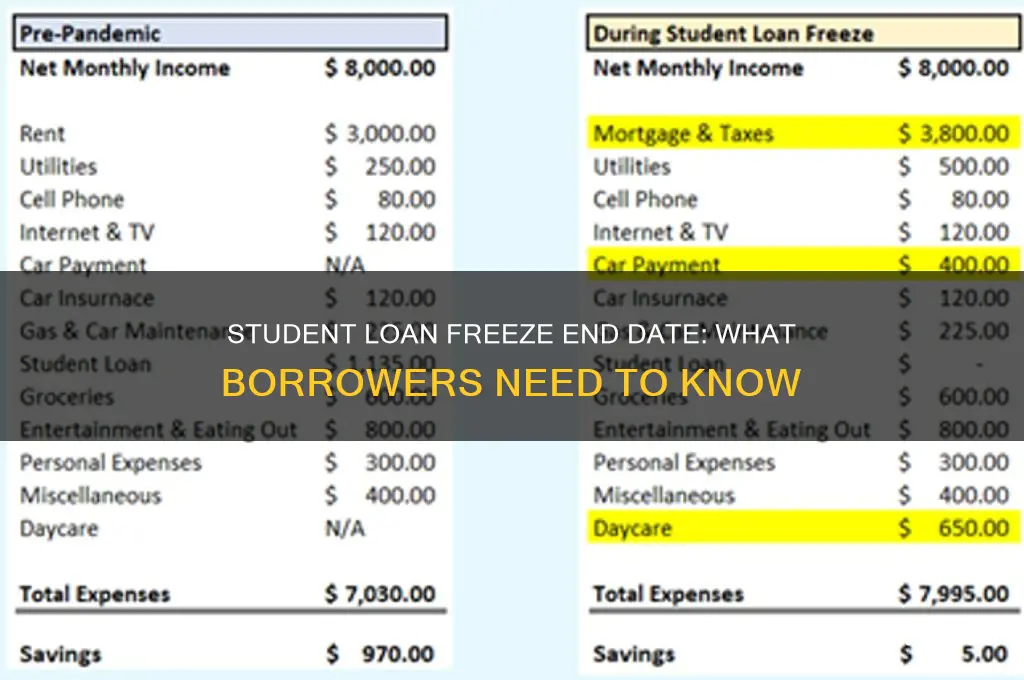

The end of the student loan freeze will trigger a cascade of adjustments for borrowers, forcing many to reevaluate their financial strategies after months of reprieve. For those who used the pause to redirect funds toward savings, investments, or high-interest debt, the resumption of payments will require a recalibration of budgets. Borrowers who treated the freeze as a temporary relief without planning ahead may face immediate cash flow challenges. This shift underscores the importance of proactive financial management, as the transition from zero payments to potentially hundreds of dollars monthly can strain even stable incomes.

Consider the borrower earning $50,000 annually with a $30,000 loan balance at 6% interest. During the freeze, they saved $200 monthly, reducing credit card debt by $5,000. Post-freeze, their $300 monthly payment resumes, shrinking their savings capacity by 50%. Without a revised budget, they risk backsliding into debt. Conversely, a borrower who maintained their payment schedule during the freeze to accelerate loan payoff will face fewer disruptions but may need to adjust if their financial situation has changed. These scenarios highlight the need for tailored strategies based on individual circumstances.

For borrowers on income-driven repayment (IDR) plans, the freeze’s end introduces additional complexities. Recertification of income, typically required annually, was suspended during the pause. As payments resume, many will need to reapply, potentially altering their monthly obligations. For example, a borrower whose income dropped during the pandemic may qualify for a lower payment under IDR, but delays in recertification could lead to temporary overpayment. Conversely, those with increased earnings might face higher payments, necessitating immediate budget adjustments. Navigating these changes requires vigilance and timely communication with loan servicers.

The psychological impact of the freeze’s end cannot be overlooked. After prolonged relief, the resumption of payments can induce financial anxiety, particularly for those already struggling with job instability or rising living costs. A practical tip: borrowers should simulate their post-freeze budget now, identifying areas for cuts or additional income. Tools like the Department of Education’s Loan Simulator can help model repayment scenarios. Additionally, exploring refinancing options or consolidating loans could lower interest rates, though federal benefits like IDR eligibility may be lost in the process.

Ultimately, the end of the student loan freeze is not merely a return to the status quo but a critical juncture for borrowers to reassess and fortify their financial health. Proactive steps, such as contacting servicers to confirm payment amounts, revisiting repayment plans, and building a small emergency fund, can mitigate the shock. For those overwhelmed, seeking advice from nonprofit credit counselors can provide clarity. The freeze’s end is inevitable, but its impact on borrowers’ financial obligations doesn’t have to be destabilizing with careful preparation.

Is Student Loan Forgiveness Worth It for Smaller Balances?

You may want to see also

Explore related products

![]()

Post-Freeze Policies: New rules or programs expected after the freeze concludes

The end of the student loan freeze will likely usher in a wave of new policies aimed at addressing the financial strain on borrowers while attempting to balance the needs of lenders and the broader economy. One expected change is the introduction of income-driven repayment (IDR) reforms, which could lower monthly payments for low- to middle-income earners. For instance, the Biden administration has proposed capping IDR payments at 5% of discretionary income, down from the current 10%, a move that could significantly reduce financial burden for millions. Borrowers should prepare by recalculating their expected payments using online tools like the Department of Education’s Loan Simulator to understand their new obligations.

Another anticipated policy shift is the expansion of Public Service Loan Forgiveness (PSLF), which could offer faster pathways to debt relief for those in qualifying public service roles. Currently, borrowers must make 120 qualifying payments, but post-freeze policies might reduce this requirement or broaden the definition of eligible employment. Public servants should gather all employment certification forms now to ensure they can take advantage of any streamlined processes once the new rules are implemented.

A third area of focus will likely be targeted debt cancellation programs, particularly for borrowers with smaller balances or those who have been in repayment for extended periods. For example, a policy forgiving $10,000 in debt for borrowers earning under $125,000 annually could be reintroduced with stricter eligibility criteria. Borrowers should monitor their credit reports and loan servicer communications for updates on how to apply for such programs.

Finally, enhanced borrower protections against predatory lending practices and confusing repayment terms are expected. This could include stricter regulations on private lenders and clearer communication from servicers about repayment options. Borrowers should familiarize themselves with their rights under the Fair Debt Collection Practices Act and document all interactions with loan servicers to ensure compliance with new standards.

In summary, the post-freeze landscape will likely feature a mix of repayment reforms, forgiveness programs, and borrower safeguards. Proactive steps, such as recalculating payments, gathering documentation, and staying informed, will position borrowers to navigate these changes effectively.

Top Japanese Companies Offering Student Sponsorships to Study in Japan

You may want to see also

Frequently asked questions

The end date of the student loan freeze depends on government announcements. As of the latest updates, the freeze is expected to end on September 30, 2024, but this may change based on policy decisions.

Yes, student loan payments will resume the month following the freeze’s end. Borrowers should expect to receive billing statements and prepare to make payments starting October 2024, unless further extensions are announced.

Yes, interest will begin accruing again once the freeze ends. Borrowers should plan for interest to resume on their loans starting October 1, 2024, unless additional relief measures are implemented.

Yes, borrowers can still apply for loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness, before or after the freeze ends. The freeze does not impact eligibility for these programs.

Borrowers should update their contact information with their loan servicer, review their repayment plan options, and explore programs like income-driven repayment or loan consolidation. Creating a budget to accommodate upcoming payments is also recommended.