As the pause on federal student loan payments, implemented during the COVID-19 pandemic, comes to an end, millions of borrowers are eagerly awaiting clarity on when they will need to resume their monthly payments. The U.S. Department of Education has announced that payments will restart in October 2023, following a three-year hiatus that provided financial relief to many during the economic uncertainties of the pandemic. With interest set to accrue again and payments due shortly after, borrowers are advised to review their loan details, explore repayment options, and consider enrolling in income-driven plans or applying for loan forgiveness programs if eligible. This transition period is critical for financial planning, as many face the challenge of reintegrating student loan payments into their budgets after a prolonged break.

| Characteristics | Values |

|---|---|

| Resume Date | October 1, 2023 (Payments resume after the Supreme Court ruling) |

| Interest Accrual Restart | September 1, 2023 (Interest begins accruing again) |

| Fresh Start Initiative | Aims to prevent delinquency for borrowers in default or forbearance |

| Supreme Court Ruling Impact | Struck down Biden’s student loan forgiveness plan in June 2023 |

| Payment Plan Options | Income-Driven Repayment (IDR) plans available for lower monthly costs |

| Loan Forgiveness Programs | Public Service Loan Forgiveness (PSLF) and IDR forgiveness continue |

| Borrower Support | Resources and guidance provided by loan servicers for repayment |

| Grace Period End | No additional grace period; payments resume as scheduled |

| Administrative Forbearance End | October 1, 2023 (COVID-19 payment pause officially ends) |

| Loan Servicer Communication | Borrowers will receive updates and reminders from their servicers |

Explore related products

What You'll Learn

![]()

Payment Restart Date

The Payment Restart Date for federal student loans is a critical piece of information for millions of borrowers. As of the latest updates, payments are set to resume in October 2023, following a prolonged pause due to the COVID-19 pandemic. This date is not arbitrary; it reflects a balance between economic recovery and the financial stability of borrowers. Understanding this timeline is essential for planning, as it marks the end of a significant financial reprieve for many.

Analyzing the implications of this date reveals a layered impact. For borrowers, October 2023 serves as a deadline to reassess budgets, explore repayment plans, and potentially consolidate loans. Lenders and servicers, on the other hand, must prepare for a surge in activity, ensuring systems are robust enough to handle millions of transactions. Economically, the restart of payments could influence consumer spending, as disposable income decreases for a substantial portion of the population. This ripple effect underscores the importance of the Payment Restart Date beyond individual borrowers.

To navigate this transition effectively, borrowers should take proactive steps. First, verify your loan servicer and update contact information to avoid missing critical communications. Second, explore repayment options like income-driven plans, which adjust payments based on earnings. Third, consider making interest-only payments during the final months of the pause to reduce long-term costs. For those in financial hardship, researching deferment or forbearance options is crucial. These actions, taken before the Payment Restart Date, can mitigate stress and financial strain.

Comparatively, the October 2023 restart stands out from previous pauses in its context and preparation. Unlike earlier extensions, this date is accompanied by widespread communication campaigns and resources aimed at borrower readiness. Additionally, the economic landscape has shifted, with inflation and job market dynamics playing a role in how borrowers approach repayment. This unique combination of factors makes the upcoming restart both a challenge and an opportunity for informed financial management.

Practically, the Payment Restart Date should serve as a call to action. Borrowers have a finite window to prepare, and ignoring it could lead to missed payments, increased interest, or credit damage. Start by logging into your loan account to review balances and terms. Next, create a repayment strategy tailored to your financial situation. Finally, mark the date on your calendar and set reminders for the first payment. By treating this deadline with urgency, borrowers can transition smoothly and maintain financial health.

When Will the Student Loan Bubble Burst: A Looming Crisis?

You may want to see also

Explore related products

![]()

Interest Accrual Timeline

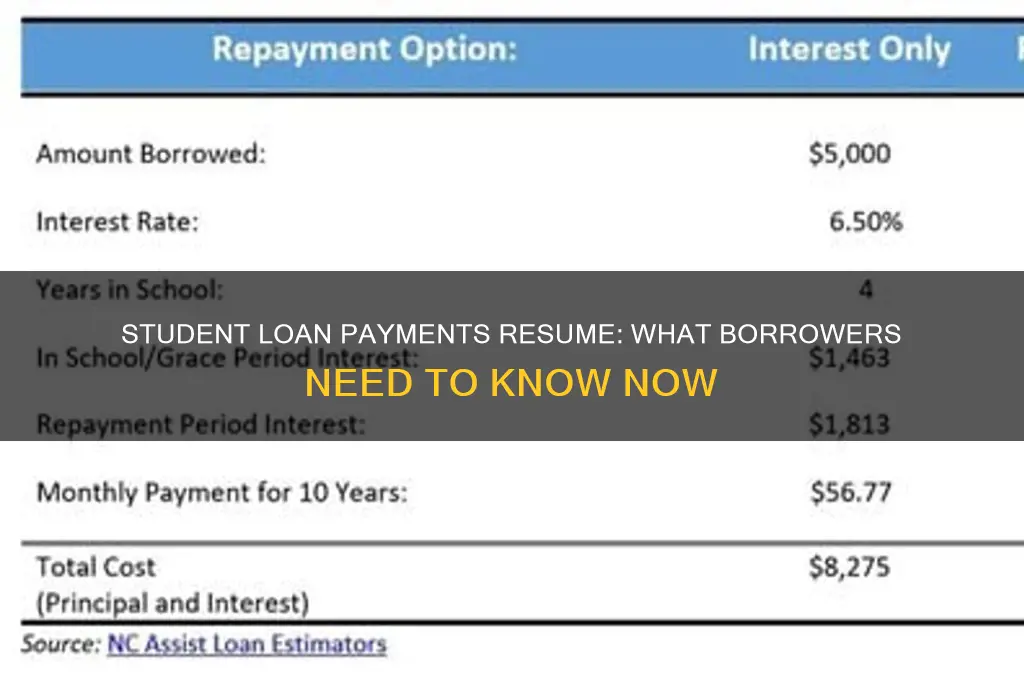

Student loan borrowers often overlook the silent yet significant impact of interest accrual, especially during periods of payment pause. Understanding the timeline of when interest begins to accumulate—and how it compounds over time—is crucial for managing debt effectively. For federal student loans, interest typically starts accruing immediately for unsubsidized loans, while subsidized loans may offer a grace period. Private loans vary widely, with some requiring payments as soon as the loan is disbursed. Knowing this timeline allows borrowers to strategize, such as making interest payments during deferment to prevent capitalization, which adds unpaid interest to the principal balance.

Consider the scenario of a borrower with a $30,000 unsubsidized federal loan at a 5% interest rate. During a 12-month payment pause, interest accrues monthly, totaling $1,500 by the end of the year. If this amount goes unpaid, it capitalizes, increasing the loan balance to $31,500. Over a 10-year repayment term, this capitalization adds approximately $450 to the total interest paid. In contrast, paying the $1,500 during the pause keeps the principal at $30,000, saving the borrower money in the long run. This example underscores the importance of tracking interest accrual timelines to minimize overall debt.

For borrowers nearing the end of a payment pause, proactive steps can mitigate the effects of interest accrual. First, review your loan terms to confirm when interest begins and whether capitalization applies. Second, calculate the total interest that will accrue during the pause using online calculators or simple formulas. Third, allocate funds to cover this amount, even if payments are not required. For instance, setting aside $125 monthly for a year covers the $1,500 interest on a $30,000 loan. Finally, contact your loan servicer to ensure payments are applied correctly, targeting interest before it capitalizes.

Comparing federal and private loans reveals stark differences in interest accrual timelines. Federal loans often provide more flexibility, with options like income-driven repayment plans that can reduce monthly payments and slow interest growth. Private loans, however, may lack such protections, making timely payments critical. For example, a private loan with immediate accrual and no deferment options could see interest compound rapidly, especially if the borrower is unaware of the terms. Borrowers should prioritize understanding these differences to avoid unexpected financial strain.

In conclusion, mastering the interest accrual timeline is a cornerstone of student loan management. By recognizing when interest begins, how it compounds, and the long-term consequences of capitalization, borrowers can take control of their debt. Practical steps, such as calculating accrual amounts and making targeted payments, can save hundreds or even thousands of dollars. Whether federal or private, each loan type demands a tailored approach, emphasizing the need for vigilance and proactive planning as payment resumption looms.

Kansas Tax Rules: Student Loan Forgiveness and Your Financial Impact

You may want to see also

Explore related products

![]()

Repayment Plan Options

Student loan payments are set to resume in October 2023, following a prolonged pause due to the COVID-19 pandemic. As borrowers prepare for this transition, understanding the available repayment plan options is crucial for managing financial obligations effectively. The federal government offers several plans tailored to different financial situations, each with its own eligibility criteria and benefits.

Analytical Perspective: Among the most popular options is the Income-Driven Repayment (IDR) Plan, which caps monthly payments at a percentage of the borrower’s discretionary income. For example, the Revised Pay As You Earn (REPAYE) plan sets payments at 10% of discretionary income, while the Income-Based Repayment (IBR) plan adjusts this to 10% or 15%, depending on when the loans were taken out. These plans are ideal for borrowers with lower incomes relative to their debt, as they can significantly reduce monthly payments. However, it’s important to note that any remaining balance after 20–25 years of qualifying payments may be forgiven, though the forgiven amount could be taxable.

Instructive Approach: For those seeking simplicity and predictability, the Standard Repayment Plan offers a fixed monthly payment over a 10-year term. This plan is best for borrowers who can afford higher payments and want to minimize interest costs over time. Alternatively, the Graduated Repayment Plan starts with lower payments that increase every two years, aligning with the assumption of career progression and higher earnings. Borrowers should assess their long-term financial goals and current income stability before choosing this option.

Comparative Insight: Borrowers with multiple federal loans may benefit from the Consolidation Option, which combines all eligible loans into a single loan with a fixed interest rate based on the weighted average of the original loans. This simplifies repayment by reducing the number of monthly bills. However, consolidating can sometimes reset the clock on forgiveness programs, so it’s essential to weigh the pros and cons carefully. For instance, if a borrower is halfway to Public Service Loan Forgiveness (PSLF), consolidating could restart the 10-year forgiveness timeline.

Persuasive Argument: The Extended Repayment Plan stretches payments over 25 years, lowering monthly costs but increasing overall interest paid. While this plan provides immediate relief, it’s less cost-effective in the long run. Borrowers should consider this option only if they cannot afford payments under other plans and are willing to trade short-term savings for long-term expenses. Additionally, exploring employer-based repayment assistance programs or refinancing with private lenders could offer better terms for those with strong credit histories.

Practical Tips: Before selecting a plan, borrowers should use the Federal Student Aid Loan Simulator to compare estimated monthly payments and total costs. It’s also advisable to recertify income annually for IDR plans to ensure payments remain aligned with financial circumstances. Finally, staying informed about policy changes, such as the one-time account adjustment for IDR forgiveness, can help maximize benefits and avoid pitfalls. With the right plan, resuming student loan payments can be manageable and aligned with long-term financial goals.

When Will Students Receive CARES Act Funding? Updates and Timeline

You may want to see also

Explore related products

![]()

Forbearance Extensions

Student loan forbearance extensions have become a critical lifeline for borrowers navigating financial uncertainty. Since the pandemic-era pause on federal student loan payments ended in October 2023, millions have faced the daunting task of resuming payments. Forbearance extensions offer temporary relief, allowing borrowers to postpone payments without accruing additional interest on subsidized loans. However, this option is not a one-size-fits-all solution. Understanding its mechanics, eligibility criteria, and long-term implications is essential for making informed decisions.

To qualify for a forbearance extension, borrowers must demonstrate financial hardship, such as unemployment, medical expenses, or a significant change in income. Applications typically require documentation, including pay stubs, medical bills, or a letter explaining the hardship. For federal loans, extensions are granted in increments of up to 12 months, with a cumulative maximum of three years. Private loan forbearance terms vary by lender, often with stricter limits and interest capitalization, meaning unpaid interest is added to the principal balance. This can increase the total cost of the loan over time, making it a less attractive option for those with private debt.

While forbearance extensions provide immediate relief, they are not a long-term solution. Borrowers should explore alternative options, such as income-driven repayment plans or loan consolidation, which can lower monthly payments and offer pathways to forgiveness. For instance, the Saving on a Valuable Education (SAVE) plan caps payments at 5% of discretionary income for undergraduate loans, compared to 10% under older plans. Additionally, public service workers may qualify for loan forgiveness after 10 years of payments through the Public Service Loan Forgiveness (PSLF) program. Weighing these alternatives against forbearance ensures borrowers address the root cause of their financial strain rather than merely delaying it.

Practical tips for managing forbearance extensions include setting aside funds during the forbearance period to ease the transition when payments resume. Borrowers should also stay informed about policy changes, as extensions may be tied to legislative or administrative actions. For example, the Biden administration’s one-time account adjustment, which counts prior forbearance periods toward forgiveness under income-driven plans, highlights the importance of staying updated. Finally, consulting a financial advisor or loan servicer can provide personalized guidance tailored to individual circumstances.

In conclusion, forbearance extensions serve as a temporary bridge for borrowers facing financial hardship, but they require careful consideration. By understanding eligibility, exploring alternatives, and staying proactive, borrowers can navigate this tool effectively while minimizing long-term financial impact. As student loan payments resume, forbearance extensions remain a valuable, though limited, resource in the broader toolkit for managing educational debt.

Will College Students Receive Stimulus Checks? Eligibility and Updates

You may want to see also

Explore related products

![]()

Loan Forgiveness Updates

As of October 2023, student loan payments are set to resume after a prolonged pause due to the COVID-19 pandemic. With this resumption comes heightened interest in loan forgiveness programs, which have seen significant updates and expansions. One of the most notable changes is the Public Service Loan Forgiveness (PSLF) waiver, which temporarily relaxed rules to allow more borrowers to qualify. This waiver, which expired in October 2022, granted credit for past payments that were previously ineligible, providing a lifeline to public servants burdened by debt. Borrowers who missed this opportunity should review their payment histories and employment certifications to ensure they’re on track for forgiveness under the standard PSLF rules.

Another critical update is the Fresh Start initiative, designed to help defaulted borrowers regain good standing. This program allows defaulted loans to be reinstated without the usual penalties, making it easier for borrowers to qualify for income-driven repayment plans or forgiveness programs. For those in default, taking advantage of Fresh Start is a priority, as it prevents wage garnishments and tax refund interceptions. Borrowers should contact their loan servicers immediately to enroll and explore options like loan consolidation, which can also restart the clock on forgiveness timelines.

The Income-Driven Repayment (IDR) Account Adjustment is another game-changer, particularly for long-term borrowers. This update addresses historical inaccuracies in payment tracking, retroactively crediting borrowers for months spent in forbearance or under certain repayment plans. For example, months in economic hardship deferment now count toward the 20 or 25 years required for IDR forgiveness. Borrowers nearing the forgiveness threshold should review their accounts to ensure all eligible payments are reflected, potentially shaving years off their repayment timeline.

Lastly, the one-time student debt relief program, though currently stalled in courts, remains a topic of interest. While its fate is uncertain, borrowers should stay informed about potential eligibility criteria and application processes. In the meantime, focusing on existing forgiveness programs and repayment strategies is prudent. For instance, teachers working in low-income schools can explore the Teacher Loan Forgiveness program, which offers up to $17,500 in forgiveness after five consecutive years of service. Each program has specific requirements, so borrowers should carefully review eligibility and documentation needs to maximize their chances of success.

In summary, navigating loan forgiveness updates requires proactive steps and attention to detail. Borrowers should leverage tools like the PSLF waiver, Fresh Start, and IDR adjustments while staying informed about emerging programs. By taking advantage of these updates, borrowers can significantly reduce their debt burden and move closer to financial freedom.

Student Loan Forgiveness: Does Household Income Determine Eligibility?

You may want to see also

Frequently asked questions

Student loan payments resumed in October 2023, following the end of the COVID-19 payment pause and forbearance period.

As of now, there are no plans for another extension. The payment pause officially ended in September 2023, and payments resumed in October 2023.

Borrowers who cannot afford payments should explore options like income-driven repayment plans, deferment, or forbearance. Contact your loan servicer to discuss available options.

Yes, interest resumed accruing on student loans as of September 1, 2023, after the pause ended. Borrowers are responsible for payments starting October 2023.