The topic of student loan forgiveness in the UK has garnered significant attention, particularly as many graduates grapple with mounting debt and the long-term financial implications of their higher education. With rising tuition fees and living costs, there is growing pressure on the government to address the issue and provide relief to borrowers. While the UK’s student loan system differs from other countries, with repayments tied to income and loans written off after a certain period, many are calling for more immediate solutions, such as partial or full forgiveness, especially in light of economic challenges like inflation and the cost of living crisis. Discussions around when and how student loans might be forgiven in the UK remain a key focus for policymakers, students, and graduates alike.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Based on repayment plan (Plan 1, Plan 2, Plan 4, or Postgraduate Loan) |

| Plan 1 Forgiveness Age | 65 years old |

| Plan 2 & Plan 4 Forgiveness Age | 30 years from the April after graduation |

| Postgraduate Loan Forgiveness Age | 30 years from the April after the first repayment was due |

| Income Threshold (Plan 1) | £20,195 per year (2023/24 tax year) |

| Income Threshold (Plan 2 & Plan 4) | £27,295 per year (2023/24 tax year) |

| Interest Rates (Plan 1) | RPI (Retail Price Index) or 1.5%, whichever is lower |

| Interest Rates (Plan 2 & Plan 4) | RPI + up to 3%, depending on income |

| Repayment Rate | 9% of income above the threshold |

| Automatic Forgiveness | Yes, after the specified period if not fully repaid |

| Early Repayment Option | Yes, but no penalty for early repayment |

| Impact on Credit Score | Student loans do not appear on credit reports in the UK |

| Latest Policy Changes (2023) | No major changes; thresholds and terms remain consistent |

| Source of Information | UK Government Student Finance Website |

Explore related products

What You'll Learn

![]()

Eligibility criteria for UK student loan forgiveness programs

The UK's student loan system operates on a unique income-contingent repayment model, meaning forgiveness isn't a straightforward process. Instead, loans are written off after a certain period, typically 30 years from the April after you graduate or leave your course. This automatic forgiveness is a key feature, but it's not the only path to debt relief. Understanding the eligibility criteria for loan forgiveness programs is crucial for borrowers seeking to navigate this complex landscape.

Repayment Thresholds and Loan Write-Offs: The Foundation of Forgiveness

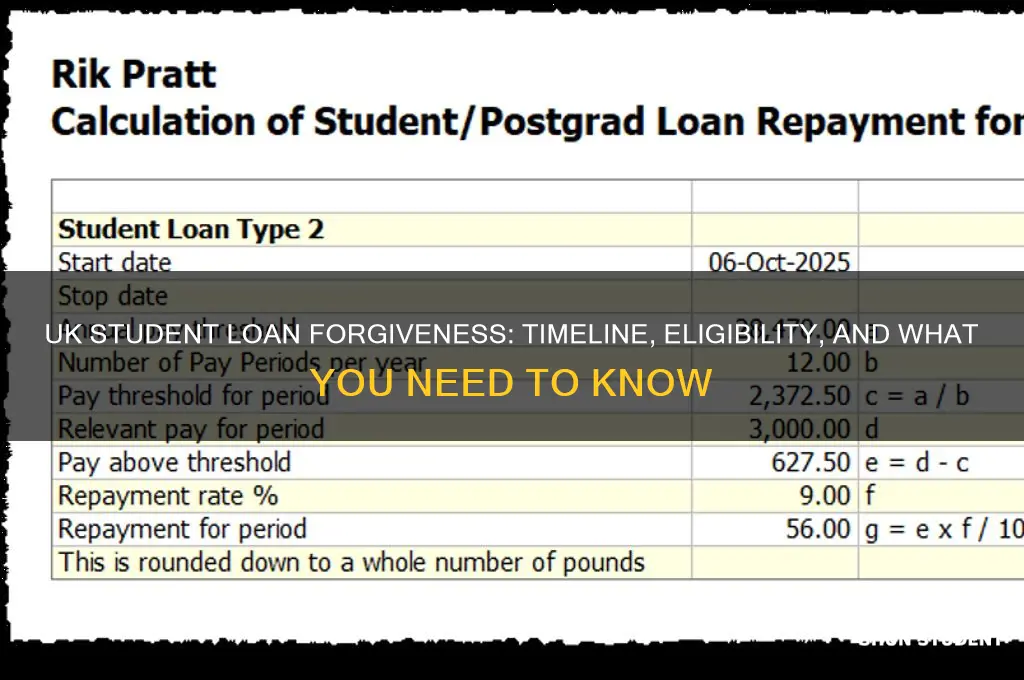

The primary mechanism for student loan forgiveness in the UK is tied to repayment thresholds. As of 2023, if you started your undergraduate course after 1 September 2012 in England or Wales, you'll repay 9% of your income above £27,295 per year. For those who began their studies before this date, the threshold is lower, at £19,895. Crucially, any outstanding balance is written off after 30 years, regardless of how much you've repaid. This system ensures that lower-earning graduates aren't burdened with lifelong debt, providing a safety net for those who may struggle to repay their loans.

Disability and Death: Special Circumstances for Loan Forgiveness

In certain exceptional cases, student loans can be forgiven before the 30-year mark. If a borrower becomes permanently unfit for work due to a disability, they may be eligible for loan cancellation. This requires evidence from a medical professional and an application to the Student Loans Company (SLC). Similarly, if a borrower passes away, their loan is written off, and no repayments are required from their estate. These provisions offer a compassionate approach to debt relief, recognizing the unique challenges faced by individuals in these situations.

Plan 1 vs. Plan 2: Understanding the Differences

It's essential to distinguish between Plan 1 and Plan 2 loans, as they have different repayment thresholds and write-off periods. Plan 1 loans, typically held by those who started their courses before 2012, have a lower repayment threshold and a 25-year write-off period. Plan 2 loans, for post-2012 students, have a higher threshold and a 30-year write-off. Knowing which plan applies to you is critical, as it directly impacts your repayment strategy and potential forgiveness timeline.

Practical Tips for Maximizing Forgiveness Potential

To optimize your chances of loan forgiveness, consider the following strategies:

- Keep track of your repayments: Ensure your employer is deducting the correct amount, and monitor your annual statements from the SLC.

- Update your contact details: Inform the SLC of any changes to your address or circumstances to avoid missing important communications.

- Explore repayment holidays: If you're facing financial hardship, you may be eligible for a temporary repayment break, although interest will still accrue.

- Plan for the long term: Understand that forgiveness is a marathon, not a sprint. Focus on managing your finances effectively to minimize the impact of loan repayments on your overall financial health.

By grasping the intricacies of the UK's student loan forgiveness programs, borrowers can make informed decisions about their repayment strategies. While the system may seem complex, its income-contingent nature and automatic write-off provisions offer a degree of protection for graduates, ensuring that student debt doesn't become an insurmountable burden.

Student Loan Forgiveness: Do You Need to Reapply for Relief?

You may want to see also

Explore related products

![]()

Impact of government policies on loan forgiveness timelines

Government policies in the UK have historically been the linchpin determining when, if ever, student loans are forgiven. The repayment threshold, currently set at £27,295 annually for Plan 2 loans (those taken out after 2012), directly influences how quickly borrowers can clear their debt. When this threshold rises, borrowers retain more income before repayments kick in, delaying forgiveness. Conversely, lowering it accelerates repayments but may strain lower earners. For instance, the 2022 freeze on the threshold amid soaring inflation meant graduates faced higher effective repayment rates, pushing forgiveness further into the future. This policy decision underscores how fiscal adjustments can subtly reshape loan timelines without explicit forgiveness programs.

Consider the interplay between interest rates and loan forgiveness. The Retail Price Index (RPI) plus 3% determines interest rates for Plan 2 loans, often exceeding inflation. While this structure ensures loans retain value for the government, it inflates balances for high earners, delaying the 30-year forgiveness mark. For example, a graduate earning £40,000 with a £50,000 loan could see their balance grow by thousands annually if interest outpaces repayments. Policymakers could cap interest rates or tie them to lower indices, such as the Consumer Price Index (CPI), to prevent ballooning debts and expedite forgiveness for those unlikely to repay in full. Such a shift would require balancing fiscal sustainability with borrower equity.

The political climate also dictates the pace of loan forgiveness. Labour’s 2019 manifesto proposed abolishing tuition fees, which, if implemented, would render forgiveness timelines moot for future students. However, existing borrowers would still be subject to current repayment terms unless a retrospective policy is introduced. Conversely, the Conservative government’s focus on fiscal restraint has prioritized maintaining the loan system’s income-contingent structure. Advocacy groups pushing for broader forgiveness, such as the "Write Off All Student Debt" campaign, highlight how policy inertia perpetuates uncertainty for millions. Borrowers must thus monitor political agendas, as election cycles and shifts in power can abruptly alter forgiveness trajectories.

Finally, the introduction of targeted forgiveness schemes illustrates how policy can directly truncate loan timelines for specific groups. The NHS Student Bursary, for instance, forgives up to £8,000 of debt for healthcare students committing to the NHS post-graduation. Similarly, the Teacher Student Loan Forgiveness program in the U.S. offers parallels for how UK policymakers could structure sector-specific relief. Expanding such schemes to critical sectors like social work or engineering could alleviate debt burdens while addressing workforce shortages. However, these programs require careful design to avoid unintended consequences, such as incentivizing career choices solely for financial relief rather than passion or skill. Borrowers should stay informed about eligibility criteria and application deadlines for such schemes to maximize their chances of early forgiveness.

Iowa Tax Implications: Will Student Loan Forgiveness Be Taxable?

You may want to see also

Explore related products

![]()

Repayment thresholds and forgiveness after 30 years

In the UK, student loan repayment thresholds are a critical factor in determining when and how much borrowers repay, with forgiveness after 30 years offering a safety net for those who may never fully settle their debt. For Plan 2 loans (post-2012), the threshold is currently set at £27,295 annually, meaning repayments only begin once earnings exceed this amount. This system is designed to ensure that repayments are proportional to income, easing the burden on lower earners. However, it also means that higher earners repay more over time, potentially exceeding the original loan amount due to interest accrual.

Analyzing the 30-year forgiveness rule reveals its dual purpose: protecting borrowers from lifelong debt while maintaining the sustainability of the loan system. After 30 years from the April following graduation, any remaining balance is written off, regardless of how much has been repaid. This is particularly beneficial for those in lower-paying careers or with fluctuating incomes, as it caps the financial commitment. For example, a graduate earning £30,000 annually would repay approximately £270 per year, but if their income remains relatively low, a significant portion of their debt could be forgiven after three decades.

To maximize the benefits of this system, borrowers should focus on understanding their repayment terms and thresholds. For instance, ensuring accurate tax filings is crucial, as repayments are calculated based on taxable income. Overpaying slightly above the threshold can also reduce the overall interest accrued, though this strategy may not suit everyone. Additionally, keeping track of annual statements from the Student Loans Company helps borrowers monitor their progress toward the 30-year mark.

Comparatively, the UK’s approach differs from countries like the US, where forgiveness programs often require specific conditions, such as public service or income-driven repayment plans. The UK’s automatic forgiveness after 30 years is more straightforward but less targeted. This simplicity reduces administrative burden but may result in higher earners benefiting disproportionately, as they are more likely to accrue substantial interest before forgiveness.

In conclusion, repayment thresholds and the 30-year forgiveness rule are cornerstone features of the UK student loan system, balancing affordability with long-term financial planning. Borrowers should stay informed about their thresholds, monitor their repayments, and consider their career trajectories to make the most of this structured yet forgiving framework. While not a perfect solution, it provides a clear endpoint for student debt, offering peace of mind to millions of graduates.

FBI and Student Loan Forgiveness: Separating Fact from Fiction

You may want to see also

Explore related products

![]()

Forgiveness options for disabled or deceased borrowers

In the UK, disabled borrowers may qualify for student loan forgiveness through the Total and Permanent Disability Discharge (TPDD) scheme. To apply, individuals must provide evidence from a medical professional confirming their inability to work due to a physical or mental impairment expected to last indefinitely. This process requires submitting a formal application to the Student Loans Company (SLC), along with supporting documentation. Approval results in the complete cancellation of outstanding loan balances, offering financial relief to those facing long-term health challenges.

For deceased borrowers, student loans are automatically written off upon death, ensuring surviving family members are not burdened with repayment. The SLC requires a death certificate to process the cancellation, which can be submitted by a relative or executor of the estate. This policy applies to both undergraduate and postgraduate loans, regardless of the borrower’s age or repayment status at the time of death. It’s a straightforward process designed to alleviate additional stress during an already difficult time.

Comparing these two forgiveness options highlights their distinct eligibility criteria and application processes. While the TPDD scheme focuses on the borrower’s medical condition and requires proactive application, the death discharge is automatic and handled posthumously. Both, however, underscore the UK’s commitment to providing compassionate financial solutions for vulnerable borrowers. Understanding these differences ensures individuals or their families can navigate the system effectively.

Practical tips for disabled borrowers include gathering comprehensive medical evidence early and seeking assistance from disability support organizations to streamline the TPDD application. For families of deceased borrowers, promptly notifying the SLC and providing the necessary documentation can expedite the loan cancellation process. Awareness of these options and their requirements empowers borrowers and their loved ones to access the support they need.

Is MA Taxing Student Loan Forgiveness? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Potential changes to loan forgiveness under new legislation

The UK government’s student loan system is under scrutiny, with new legislation potentially reshaping how and when loans are forgiven. One key proposal is adjusting the repayment threshold, currently set at £27,295 annually for Plan 2 loans (those taken out after 2012). Lowering this threshold could mean graduates start repaying sooner but at smaller amounts, delaying forgiveness. Conversely, raising it could accelerate forgiveness for lower earners but reduce overall government recovery. These changes would directly impact the 25-35 age group, who hold the bulk of outstanding debt.

Another legislative focus is the interest rate structure. Currently, interest accrues at RPI + up to 3%, often outpacing repayment rates for lower earners. Proposals to cap or reduce interest rates could prevent debt ballooning over time, particularly for those earning below the repayment threshold. For example, a 28-year-old graduate earning £25,000 annually could see their debt grow by £1,000+ yearly under current rules; a cap could halve this, making forgiveness more attainable within the standard 30-year term.

A third area of reform is the loan forgiveness timeline. Currently, unpaid balances are written off after 30 years for Plan 2 loans. New legislation might shorten this period for specific sectors, such as teachers or nurses, to incentivize public service. Alternatively, extending the term could reduce the fiscal burden on the government but delay relief for borrowers. For instance, a 40-year term would push forgiveness into the mid-60s for recent graduates, potentially overlapping with retirement planning.

Practical tips for borrowers include monitoring legislative updates via the UK Parliament website and student finance bodies. Graduates should also review their repayment plans annually, especially if self-employed or earning variable income, to avoid overpayment. Tools like the Student Loan Repayment Calculator can model how threshold or interest changes might affect individual timelines. Staying informed and proactive could turn potential legislative shifts into opportunities for faster forgiveness.

Unlock Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Frequently asked questions

Student loans in the UK are not typically "forgiven" in the traditional sense. Instead, they are written off after a certain period, usually 30 years after the first repayment was due, depending on the repayment plan and type of loan.

As of now, there are no government plans to forgive student loans en masse before the standard repayment period. However, loans are automatically written off after 30 years (or 25 years for older plans), and some borrowers may qualify for earlier write-offs under specific circumstances, such as disability or death.

Changes to the student loan system, such as adjustments to repayment thresholds or interest rates, may impact how quickly borrowers repay their loans, but they do not typically alter the standard write-off period. Any significant changes to forgiveness policies would require government legislation.