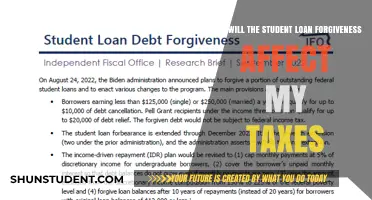

The topic of when the one-time student loan forgiveness will occur has been a pressing concern for millions of borrowers, especially following recent announcements and policy changes. In August 2022, the Biden administration unveiled a plan to forgive up to $20,000 in federal student loan debt for eligible borrowers, marking a significant step toward addressing the growing student debt crisis. However, the initiative faced legal challenges, leading to delays and uncertainty. As of now, borrowers are eagerly awaiting updates on when the forgiveness process will resume, with many hoping for clarity on timelines and eligibility criteria. The outcome of ongoing court cases and potential legislative actions will play a crucial role in determining when and how this one-time relief will be implemented.

Explore related products

What You'll Learn

- Eligibility Criteria: Who qualifies for one-time student loan forgiveness under current or proposed programs

- Forgiveness Timeline: When will borrowers receive notification and relief for their eligible loans

- Loan Types Covered: Which federal or private loans are included in one-time forgiveness plans

- Application Process: Steps borrowers need to take to apply for one-time loan forgiveness

- Impact on Credit: How will one-time loan forgiveness affect borrowers’ credit scores and reports

![]()

Eligibility Criteria: Who qualifies for one-time student loan forgiveness under current or proposed programs?

The eligibility criteria for one-time student loan forgiveness programs are often complex and vary depending on the specific initiative. Understanding these criteria is crucial for borrowers seeking relief, as it determines who can access this potentially life-changing benefit.

Current Programs: Targeted Relief for Specific Groups

Existing one-time forgiveness programs typically target specific borrower profiles. For instance, the Public Service Loan Forgiveness (PSLF) program requires borrowers to work full-time for a qualifying employer in the public sector or a non-profit organization for at least 10 years while making 120 qualifying payments. This program is designed to incentivize careers in public service. Similarly, the Teacher Loan Forgiveness program offers up to $17,500 in forgiveness for teachers who work in low-income schools for five consecutive years. These programs demonstrate a focus on rewarding borrowers who contribute to specific societal needs.

Proposed Expansions: Broader Reach, Stricter Conditions?

Proposed one-time forgiveness programs often aim for broader reach but may come with stricter eligibility requirements. Some proposals suggest income-based thresholds, capping forgiveness amounts for borrowers earning above a certain level. Others propose targeting borrowers with specific loan types, such as those with high-interest private loans or those who attended predatory for-profit institutions. These proposals reflect a desire to address systemic issues within the student loan landscape while ensuring responsible use of taxpayer funds.

Key Considerations: Documentation and Timelines

Regardless of the program, meticulous documentation is essential. Borrowers must maintain records of employment, loan payments, and other relevant information to prove eligibility. Additionally, understanding application deadlines and processing times is crucial, as these can vary significantly. Missing a deadline or failing to provide required documentation can result in disqualification.

Staying Informed: A Dynamic Landscape

The landscape of student loan forgiveness is constantly evolving. Borrowers should stay informed about new programs, changes to existing ones, and potential legislative developments. Utilizing resources from the Department of Education, reputable financial advisors, and advocacy groups can help borrowers navigate the complexities of eligibility criteria and maximize their chances of qualifying for one-time student loan forgiveness.

Can Bankruptcy Discharge Federal Student Loans? What You Need to Know

You may want to see also

Explore related products

![]()

Forgiveness Timeline: When will borrowers receive notification and relief for their eligible loans?

The Biden administration’s one-time student loan forgiveness program has left borrowers eagerly awaiting clarity on when they’ll receive notification and relief. While the program aims to discharge up to $20,000 in debt for eligible borrowers, the timeline remains uncertain due to ongoing legal challenges. As of late 2023, the Supreme Court’s ruling struck down the program, but the Department of Education continues to explore alternative pathways to provide relief. Borrowers should monitor official updates from Federal Student Aid (FSA) and prepare necessary documentation to act swiftly if the program resumes.

Analyzing the current landscape, the forgiveness timeline hinges on legislative and judicial developments. If Congress passes new legislation or the administration revises its approach, notifications could begin within 60 to 90 days of approval. Borrowers would likely receive emails or letters from their loan servicers outlining eligibility and next steps. Relief, in the form of balance adjustments, could follow within 30 to 60 days after notification. However, this timeline assumes no further legal delays, which remain a significant variable.

For borrowers, proactive steps can streamline the process once forgiveness resumes. Ensure your contact information is updated with your loan servicer and FSA to avoid missing critical notifications. Review your loan balances and payment histories to confirm eligibility, particularly if you’ve made payments during administrative forbearance. Additionally, consider enrolling in income-driven repayment plans or Public Service Loan Forgiveness (PSLF) as backup options while awaiting broader relief.

Comparatively, the timeline for student loan forgiveness differs from other debt relief programs. For instance, PSLF requires 120 qualifying payments, while income-driven plans take 20–25 years. The one-time forgiveness program, however, promises immediate relief for eligible borrowers, making its timeline uniquely urgent. Unlike gradual repayment plans, this program’s success depends on swift government action and borrower readiness.

In conclusion, while the exact timeline for one-time student loan forgiveness remains uncertain, borrowers can prepare by staying informed and organized. Regularly check FSA’s website and subscribe to updates from reputable sources. By understanding the potential timeline and taking proactive steps, borrowers can position themselves to receive relief as soon as it becomes available. Patience and preparedness will be key in navigating this evolving landscape.

Can You Buy Beer with a Student ID? Reddit's Take

You may want to see also

Explore related products

![]()

Loan Types Covered: Which federal or private loans are included in one-time forgiveness plans?

Federal student loan forgiveness programs, particularly one-time initiatives, are not a one-size-fits-all solution. Understanding which loans qualify is crucial for borrowers navigating these opportunities. The landscape of eligible loans varies depending on the specific forgiveness program.

Direct Loans Dominate: The majority of one-time forgiveness programs, such as the Public Service Loan Forgiveness (PSLF) and the recently announced limited waiver, primarily target Direct Loans. This includes Direct Subsidized and Unsubsidized Loans, Direct PLUS Loans (for both graduate students and parents), and Direct Consolidation Loans. These loans, issued directly by the federal government, are the backbone of most forgiveness initiatives.

FFEL and Perkins Loans: A Path to Inclusion: Federal Family Education Loans (FFEL) and Perkins Loans, older loan types often held by private lenders, were historically excluded from many forgiveness programs. However, recent policy changes, like the limited PSLF waiver, have opened a temporary window for these borrowers. Consolidating FFEL and Perkins Loans into a Direct Consolidation Loan is the key to unlocking forgiveness eligibility. This process essentially converts ineligible loans into a qualifying Direct Loan, paving the way for potential debt relief.

Private Loans: Largely Left Out: Unfortunately, private student loans, issued by banks, credit unions, and other financial institutions, are typically excluded from federal forgiveness programs. These loans operate under different terms and conditions, and forgiveness is rarely an option. Borrowers with private loans should explore alternative strategies like refinancing for lower interest rates or negotiating with lenders for more manageable repayment plans.

The Takeaway: Understanding loan type eligibility is the first step towards leveraging one-time forgiveness opportunities. While Direct Loans are the primary beneficiaries, recent policy shifts have created pathways for FFEL and Perkins Loan holders to participate. Private loan borrowers, however, must seek alternative solutions outside the realm of federal forgiveness programs.

Will Private Student Loans Ever Be Forgiven? Exploring Possibilities and Updates

You may want to see also

Explore related products

![]()

Application Process: Steps borrowers need to take to apply for one-time loan forgiveness

The application process for one-time student loan forgiveness is a critical pathway for eligible borrowers seeking financial relief. While the specifics may vary depending on the program, a structured approach ensures clarity and maximizes the chances of approval. Here’s a step-by-step guide tailored to help borrowers navigate this process effectively.

Step 1: Verify Eligibility

Before initiating the application, borrowers must confirm their eligibility for one-time loan forgiveness. This typically involves checking criteria such as loan type (federal vs. private), repayment plan, employment status, and income level. For instance, programs like Public Service Loan Forgiveness (PSLF) require 120 qualifying payments and employment in a public service role. Use official government resources or loan servicer portals to assess eligibility accurately. Ignoring this step can lead to unnecessary effort and potential rejection.

Step 2: Gather Required Documentation

Once eligibility is confirmed, compile all necessary documents. Common requirements include proof of employment, payment history, tax returns, and loan account details. For income-driven repayment plans, recent pay stubs or benefit award letters may be needed. Organize these documents digitally or physically to streamline the application process. Missing or incomplete documentation is a frequent cause of delays, so double-check the program’s checklist.

Step 3: Complete the Application Form

Most forgiveness programs require a formal application, often available online through the Department of Education or loan servicer websites. Fill out the form meticulously, ensuring all fields are accurate and complete. Errors, such as incorrect loan numbers or misspelled names, can result in processing delays or denials. If unsure about any section, contact the loan servicer or a financial advisor for clarification.

Step 4: Submit and Follow Up

After submitting the application, retain a copy for your records and note the confirmation number or receipt. Follow up with the loan servicer within 30 days to confirm receipt and inquire about the processing timeline. Some programs may require additional steps, such as recertifying income or updating employment information. Stay proactive and monitor your loan account for updates.

Cautions and Practical Tips

Beware of scams promising expedited forgiveness for a fee—legitimate applications are free. Avoid procrastination, as processing times can be lengthy, especially during high-volume periods. Keep all communication with loan servicers documented, and consider setting reminders for follow-ups. Finally, explore complementary relief options, such as temporary forbearance or deferment, if financial hardship persists during the application process.

By following these steps and staying vigilant, borrowers can navigate the one-time loan forgiveness application process with confidence and increase their chances of achieving much-needed financial relief.

Should You Apply for Student Loan Forgiveness During Beta Launch?

You may want to see also

Explore related products

![]()

Impact on Credit: How will one-time loan forgiveness affect borrowers’ credit scores and reports?

The one-time student loan forgiveness program, while offering significant financial relief, raises questions about its impact on borrowers' credit profiles. Understanding these effects is crucial for anyone anticipating or benefiting from such forgiveness.

Here's a breakdown of how this initiative could influence credit scores and reports:

Direct Impact on Credit Reports: Loan forgiveness will likely result in the removal of the forgiven loan balance from your credit report. This means the loan will no longer be listed as an outstanding debt, potentially improving your overall credit utilization ratio – a key factor in credit scoring. A lower utilization ratio generally indicates responsible credit management and can boost your score.

Potential Score Fluctuations: While the removal of debt is positive, credit scores are complex algorithms. Initially, your score might experience a slight dip due to the closure of an established credit account. However, this effect is usually temporary, and the long-term benefit of reduced debt outweighs this minor fluctuation.

Long-Term Credit Health: The most significant impact of one-time loan forgiveness is the alleviation of a substantial financial burden. This can lead to improved financial stability, allowing borrowers to focus on other financial goals, make timely payments on remaining debts, and potentially build a stronger credit history over time.

Monitoring Your Credit: After loan forgiveness, it's essential to monitor your credit report closely. Ensure the forgiven loan is accurately reflected as "paid in full" or "forgiven." Any discrepancies should be promptly disputed with the credit bureaus to maintain the accuracy of your credit profile.

DIY Guide to Student Loan Forgiveness for Professors: Step-by-Step

You may want to see also

Frequently asked questions

The timeline for one-time student loan forgiveness depends on the specific program or policy announced by the government. For example, the Biden administration's 2022 forgiveness plan began processing applications in late 2022, but implementation was delayed due to legal challenges. Always check official government sources for the latest updates.

Eligibility criteria vary by program. For the 2022 federal forgiveness plan, borrowers earning under $125,000 (individuals) or $250,000 (married couples) were eligible for up to $10,000 in forgiveness, with an additional $10,000 for Pell Grant recipients. Always review the specific requirements for the program in question.

The application process typically involves submitting an online form through the Department of Education's website or your loan servicer. For the 2022 program, borrowers had to complete a simple application, but the process may differ for future initiatives. Follow official instructions provided by the government.

In most cases, borrowers need to apply for forgiveness unless they are already enrolled in income-driven repayment plans or have their income data on file. Some borrowers may receive automatic forgiveness if their eligibility is confirmed through existing data. Check with your loan servicer or the Department of Education for details.

If your application is denied, you can appeal the decision by providing additional documentation or correcting errors. The appeals process varies by program, so follow the instructions provided in the denial notice. Legal challenges or changes in policy may also impact the outcome, so stay informed through official channels.