Navigating the complexities of student loans can be overwhelming, especially when it comes to understanding where to find information about your loan interest. Student loan interest is a crucial aspect of your repayment plan, as it directly impacts the total amount you’ll owe over time. To locate details about your student loan interest, start by logging into your loan servicer’s website or portal, where you can typically view your current interest rate, loan balance, and payment history. If you’re unsure who your loan servicer is, check your most recent loan statement or visit the National Student Loan Data System (NSLDS) for federal loans. Additionally, your original loan agreement or promissory note will outline the interest terms. For private loans, contact your lender directly. Understanding where to find this information is the first step toward managing your student loan debt effectively.

| Characteristics | Values |

|---|---|

| Source of Information | Federal Student Aid (FSA) website, Loan Servicer's Website, Tax Documents |

| Federal Loan Interest Details | Available on StudentAid.gov under "My Loan Information" |

| Private Loan Interest Details | Check loan servicer's website or contact the lender directly |

| Tax Documents | Form 1098-E (Student Loan Interest Statement) sent by lender/servicer |

| Interest Rate Type | Fixed or Variable (depends on loan type) |

| Interest Accrual Period | Daily, monthly, or annually (varies by loan) |

| Interest Capitalization | Occurs when unpaid interest is added to the loan principal |

| Repayment Plans Impact | Income-driven plans may affect interest accrual and capitalization |

| Loan Forgiveness Programs | Public Service Loan Forgiveness (PSLF) may include interest benefits |

| Latest Data Availability | Updated annually or upon request from loan servicer |

| Contact for Assistance | Federal Student Aid: 1-800-4-FED-AID, Loan Servicer's Customer Support |

Explore related products

What You'll Learn

- Federal vs. Private Loans: Identify loan type to locate interest info

- Loan Servicer Websites: Check servicer portals for interest details

- Tax Documents: Review Form 1098-E for interest paid

- Loan Statements: Monthly statements often list accrued interest

- StudentAid.gov: Federal loan interest info available on this site

![]()

Federal vs. Private Loans: Identify loan type to locate interest info

When trying to locate your student loan interest information, the first step is to identify whether your loans are federal or private, as the process for finding this information differs significantly between the two. Federal student loans are funded by the U.S. Department of Education and come with standardized terms, while private student loans are offered by banks, credit unions, or other financial institutions and have terms that vary by lender. Understanding the type of loan you have is crucial, as federal loans typically provide access to interest information through government-managed platforms, whereas private loans require you to contact your specific lender.

For federal student loans, the most direct way to find your interest information is by logging into the Federal Student Aid (FSA) website at studentaid.gov. After signing in with your FSA ID, navigate to the "My Aid" section, where you can view details about your loans, including interest rates, balances, and loan servicers. Additionally, federal loan borrowers can access their interest information through their loan servicer’s website, such as Great Lakes, Nelnet, or FedLoan Servicing. Each servicer provides an online portal where you can review your loan details, including the interest rate applied to each loan. If you’re unsure which servicer handles your loans, the FSA website will provide that information.

In contrast, private student loans require a different approach. Since private loans are not managed by a centralized system, you’ll need to contact your lender directly to obtain interest information. Start by reviewing your loan agreement or monthly statements, which should list the lender’s name and contact details. Most private lenders offer online account access, where you can log in to view your loan terms, including the interest rate. If you’re unable to find this information online, reach out to your lender’s customer service team via phone or email. They can provide a breakdown of your loan details, including the interest rate and any applicable fees.

Another key difference between federal and private loans is how interest is handled. Federal loans often have fixed interest rates set by Congress, and some may offer benefits like interest subsidies or deferment options. Private loans, however, may have variable interest rates that fluctuate over time, depending on market conditions. Understanding these differences can help you better interpret the interest information you find. For federal loans, the interest rate is typically listed clearly in your loan agreement or online portal. For private loans, you may need to review your loan terms more closely to understand how interest accrues and is calculated.

If you’re still unsure about the type of loan you have, there are a few ways to verify. For federal loans, check the National Student Loan Data System (NSLDS) at nslds.ed.gov, which provides a comprehensive list of all your federal student loans. For private loans, review your financial records, including loan agreements, emails, or statements from the lender. If you took out loans through a school’s financial aid office, they may also have records indicating whether the loans were federal or private. Once you’ve confirmed the loan type, follow the appropriate steps to locate your interest information.

In summary, identifying whether your student loans are federal or private is the first step in finding your interest information. Federal loan borrowers can access this data through the FSA website or their loan servicer’s portal, while private loan borrowers must contact their lender directly. Understanding the differences between these loan types and knowing where to look will save you time and ensure you have the accurate information needed to manage your student loan obligations effectively.

When Does Direct PLUS Student Loan Interest Start Accruing?

You may want to see also

Explore related products

![]()

Loan Servicer Websites: Check servicer portals for interest details

If you're looking to find your student loan interest, one of the most direct and reliable methods is to check the website of your loan servicer. Loan servicers are companies that manage the billing and other services of your federal or private student loans. They maintain detailed records of your loan account, including interest accrual and payment history. By logging into your account on their portal, you can access up-to-date information about your loan interest. This method is particularly useful because it provides real-time data and allows you to track changes over time.

To begin, identify your loan servicer. For federal student loans, you can find this information by logging into your account on the Federal Student Aid website (studentaid.gov). Once you know your servicer, visit their official website and log in to your account using your credentials. Most servicer portals have a dashboard or account summary page that displays key details, such as your current loan balance, interest rate, and any interest that has accrued since your last payment. Look for sections labeled "Loan Details," "Account Summary," or "Interest Information" to find the specific interest data you need.

If you’re having trouble locating the interest information, don’t hesitate to explore the portal’s navigation menu. Many servicer websites have dedicated sections for loan management, where you can view statements, payment history, and interest breakdowns. Some portals even offer tools to calculate how extra payments can reduce the total interest paid over the life of the loan. For example, FedLoan Servicing, Great Lakes, and Nelnet—common federal loan servicers—provide detailed interest summaries and resources to help borrowers understand their loans better.

For private student loans, the process is similar. Log in to your loan servicer’s website, which may be a bank or financial institution like Sallie Mae or Discover Student Loans. Private loan servicers often provide comprehensive account information, including interest rates, accrual details, and payment allocation. If the interest information isn’t immediately visible, check the "Account Overview" or "Loan Activity" sections. Some private servicers also offer customer support via chat or phone to assist you in finding the specific details you need.

Lastly, if you have multiple loans serviced by different companies, you’ll need to check each servicer’s portal individually. While this may require a bit more effort, it ensures you have a complete picture of your total student loan interest. Regularly reviewing your loan servicer’s website not only helps you stay informed about your interest accrual but also allows you to monitor your overall loan health and make informed decisions about repayment strategies.

When Unpaid Student Loan Interest Capitalizes: A Crucial Timeline Explained

You may want to see also

Explore related products

![]()

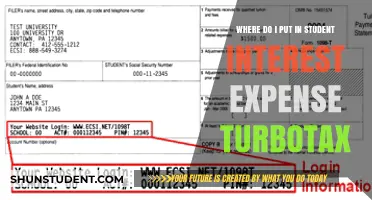

Tax Documents: Review Form 1098-E for interest paid

When it comes to finding information about the interest paid on your student loans, one of the most crucial tax documents to review is Form 1098-E. This form is specifically designed to report the amount of interest you’ve paid on qualified student loans during the tax year. Lenders are required to send this form to borrowers if they have paid at least $600 in interest over the year. If you’re unsure where to find your student loan interest, Form 1098-E is the primary document you should look for. It provides a clear and detailed breakdown of the interest paid, which is essential for claiming the student loan interest deduction on your tax return.

To locate Form 1098-E, start by checking your email or physical mailbox in January or February, as lenders typically send this form by the end of January. If you haven’t received it by mid-February, log into your student loan servicer’s online portal. Most servicers provide digital copies of tax documents, including Form 1098-E, in your account dashboard. Look for a section labeled "Tax Information," "Documents," or "Statements." If you’re still unable to find it, contact your loan servicer directly to request a copy. It’s important to ensure you have this form before filing your taxes, as it contains the exact amount of interest paid, which is necessary for accurate tax reporting.

Once you have Form 1098-E in hand, review it carefully. The form includes your name, address, and taxpayer identification number, as well as the lender’s information. The most critical detail is Box 1, which shows the total amount of interest paid during the tax year. This is the number you’ll need to report on your tax return if you’re eligible for the student loan interest deduction. Double-check that the information on the form matches your records to avoid any discrepancies. If you notice any errors, contact your loan servicer immediately to request a corrected form.

It’s worth noting that not all student loans qualify for the interest deduction, and there are income limits and other eligibility criteria. However, Form 1098-E is still essential for understanding your financial situation and potential tax benefits. Even if you don’t qualify for the deduction, keeping this form for your records is a good practice. It serves as proof of the interest paid and can be useful for future financial planning or audits.

In summary, if you’re wondering where to find your student loan interest, Form 1098-E is the key document. It provides the exact amount of interest paid, which is crucial for tax purposes. Make it a priority to obtain and review this form each year, either through your loan servicer’s portal or by requesting a copy directly. By doing so, you’ll ensure accurate tax filing and maximize any potential deductions related to your student loan interest.

Understanding the Student Loan Interest Deduction on Your 1040 Form

You may want to see also

Explore related products

$6.99

![]()

Loan Statements: Monthly statements often list accrued interest

If you're looking to find information about your student loan interest, one of the most straightforward places to start is with your loan statements. Loan statements, typically sent monthly by your loan servicer, are a treasure trove of information about your loan, including the accrued interest. These statements are designed to provide a clear and detailed breakdown of your loan activity, making them an essential tool for understanding how interest is affecting your overall debt. When you receive your monthly statement, whether in the mail or via email, take the time to review it carefully. The statement will usually include a section that explicitly lists the accrued interest for that billing cycle. This figure represents the interest that has accumulated on your loan balance since the last statement.

To locate the accrued interest on your loan statement, look for a section labeled "Interest Accrued," "Interest Since Last Statement," or something similar. This amount is typically broken down separately from any payments you’ve made toward the principal balance. Understanding this distinction is crucial because it shows how much of your loan is growing due to interest, even if you’re making regular payments. If you’re having trouble finding this information, don’t hesitate to contact your loan servicer for assistance. They can guide you through the statement and explain how to interpret the interest-related details.

Another important aspect of loan statements is that they often provide a year-to-date summary of accrued interest. This can be particularly useful when tax season approaches, as you may be eligible to deduct a portion of your student loan interest on your federal tax return. By keeping track of this information throughout the year via your monthly statements, you’ll be better prepared to take advantage of this potential tax benefit. Additionally, monitoring the accrued interest over time can help you gauge the effectiveness of any extra payments you’re making toward your loan, as reducing the principal balance directly impacts how much interest accrues.

If you’ve misplaced your paper statements or prefer digital access, most loan servicers offer online portals where you can view and download your monthly statements. Log in to your account on the servicer’s website or mobile app, navigate to the "Statements" or "Documents" section, and locate the most recent statement. These digital versions are typically identical to the paper statements and will include the same detailed information about accrued interest. Some servicers even allow you to set up alerts or notifications when a new statement is available, ensuring you never miss an update on your loan’s interest activity.

Finally, it’s worth noting that if you have multiple student loans, you’ll likely receive a separate statement for each one. Each statement will list the accrued interest specific to that loan, allowing you to track interest across all your debts. This is especially important if your loans have different interest rates or terms, as the accrued interest will vary accordingly. By regularly reviewing these statements, you’ll gain a comprehensive understanding of how interest is impacting your overall student loan burden and can make more informed decisions about repayment strategies.

How to Report Student Loan Interest on Your 1040EZ Form

You may want to see also

Explore related products

![]()

StudentAid.gov: Federal loan interest info available on this site

If you're looking to find information about your student loan interest, StudentAid.gov is a crucial resource for federal loan borrowers. This official U.S. Department of Education website provides comprehensive details about your federal student loans, including interest rates, balances, and repayment options. To access your federal loan interest information, start by logging into your account on StudentAid.gov. Once logged in, navigate to the "My Aid" section, where you’ll find a summary of all your federal loans. Each loan listed will include its current interest rate, which is essential for understanding how much interest accrues over time.

For a more detailed breakdown, click on the individual loan entries in your account. Here, you’ll see specific information about the loan type, disbursement dates, and the fixed or variable interest rate applied. Federal student loans typically have fixed interest rates, meaning they remain the same for the life of the loan. Knowing this rate is critical for budgeting and planning your repayments, as interest directly impacts the total amount you’ll pay back. StudentAid.gov also provides tools to estimate how different repayment plans affect interest accrual, helping you make informed decisions.

If you’re unsure how interest is calculated on your federal loans, StudentAid.gov offers resources to explain the process. Interest on federal loans is generally calculated daily based on your unpaid principal balance. The site includes guides and FAQs to clarify how interest capitalization (when unpaid interest is added to the principal balance) works, especially during periods like deferment or forbearance. Understanding these mechanics can help you minimize the overall cost of your loans.

Another valuable feature of StudentAid.gov is its ability to help you track changes in interest rates. While federal loan interest rates are set by Congress and typically remain fixed, it’s still important to review your loan details periodically. The site allows you to download or print loan statements, which can be useful for record-keeping or when consulting with a financial advisor. Additionally, if you’re considering consolidation or refinancing, StudentAid.gov provides tools to compare how these options might affect your interest rates.

Finally, if you have questions or need assistance, StudentAid.gov offers contact information for loan servicers and support teams. They can help clarify any confusion about your interest rates or repayment terms. By leveraging the resources available on StudentAid.gov, you can take control of your federal student loans and ensure you’re managing your interest effectively. This site is the go-to destination for accurate, up-to-date information on your federal loan interest, making it an indispensable tool for borrowers.

When Does Student Loan Interest Pause: Key Suspension Scenarios Explained

You may want to see also

Frequently asked questions

You can find the interest rate on your federal student loan by logging into your account on the Federal Student Aid website (studentaid.gov) or by checking your loan disclosure statement.

For private student loans, check your loan agreement, log into your lender’s online portal, or contact your loan servicer directly to find interest rate details.

The interest amount is typically listed on your monthly loan statement under sections like "Interest Accrued" or "Interest Paid."

Yes, your student loan interest paid for the year is reported on Form 1098-E, which is sent to you by your loan servicer and can be used for tax deductions.

Use the National Student Loan Data System (NSLDS) for federal loans or check your credit report for private loans to identify all your loans and their interest rates.