When filing your taxes, you may be eligible to claim the student loan interest deduction, which can help reduce your taxable income. This deduction is entered on Schedule 1 (Form 1040), specifically on line 20. To qualify, you must have paid interest on a qualified student loan during the tax year, and your income must fall below certain thresholds. The deduction can be claimed without itemizing deductions, making it accessible to a broader range of taxpayers. It’s important to gather Form 1098-E, which lenders provide to report the interest paid, to ensure accurate reporting on your tax return.

| Characteristics | Values |

|---|---|

| Tax Form Location | IRS Form 1040, Schedule 1 (Additional Income and Adjustments to Income) |

| Line Number | Line 20 (Student loan interest deduction) |

| Deduction Limit | Up to $2,500 per year (as of 2023) |

| Eligibility Requirement | Must have paid interest on a qualified student loan during the tax year |

| Income Phaseout Range (Single) | $75,000 to $90,000 (as of 2023) |

| Income Phaseout Range (Married Filing Jointly) | $150,000 to $180,000 (as of 2023) |

| Qualified Loans | Loans taken for qualified higher education expenses (e.g., tuition, fees, room, and board) |

| Documentation Needed | Form 1098-E (Student Loan Interest Statement) from the lender |

| Claiming Without Form 1098-E | Possible if interest paid is $600 or less (self-reporting required) |

| Tax Year Applicability | Applies to the tax year in which the interest was paid |

| Carryforward Option | No carryforward of unused deduction amounts |

| E-Filing Availability | Available through most tax software and IRS Free File |

| Updated IRS Guidance | Refer to IRS Publication 970 (Tax Benefits for Education) for details |

Explore related products

What You'll Learn

- IRS Form 1040: Locate Schedule 1, Line 21, to claim the student loan interest deduction

- Eligibility Criteria: Ensure your loan qualifies and your income meets IRS limits for deduction

- Deduction Limits: Maximum deduction is $2,500 annually, phased out at higher incomes

- Documentation Needed: Gather Form 1098-E from your lender to report interest paid

- Filing Status Impact: Deduction availability varies based on married filing jointly/separately status

![]()

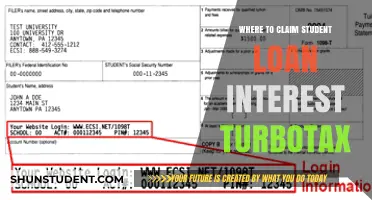

IRS Form 1040: Locate Schedule 1, Line 21, to claim the student loan interest deduction

When filing your federal tax return, claiming the student loan interest deduction can help reduce your taxable income, potentially lowering your tax liability. To claim this deduction, you’ll need to locate Schedule 1, Line 21, of IRS Form 1040. This line is specifically designated for reporting deductible student loan interest. Here’s a step-by-step guide to help you navigate the process.

First, ensure you have IRS Form 1040 and its associated schedules ready. Form 1040 is the primary tax return form used by individuals to report income, claim deductions, and calculate taxes owed or refunded. If you’re eligible for the student loan interest deduction, you’ll need to complete Schedule 1, which is an additional form used to report certain types of income and adjustments to income. Schedule 1 is attached to Form 1040 and includes Line 21, where the student loan interest deduction is entered.

To locate Schedule 1, begin by filling out the main sections of Form 1040, such as your personal information, filing status, and dependents. Once you reach the section titled "Additional Income and Adjustments to Income," you’ll find the instructions to attach Schedule 1. On Schedule 1, look for Part I: Additional Income, and then proceed to Part II: Adjustments to Income. Line 21 in Part II is labeled "Student loan interest deduction." This is where you’ll enter the amount of deductible interest you paid on qualified student loans during the tax year.

Before entering the amount on Line 21, ensure you meet the eligibility criteria for the deduction. The interest must have been paid on a qualified student loan used for higher education expenses, and your income must fall within the phase-out limits set by the IRS. Once you’ve confirmed eligibility, gather your Form 1098-E, which lenders provide to borrowers who paid at least $600 in student loan interest during the year. This form will show the exact amount you can deduct.

After verifying the amount, transfer it to Schedule 1, Line 21. Once completed, transfer the total from Schedule 1 to Form 1040, Line 10, which adjusts your income. This reduction in income can lower your taxable income, potentially resulting in a smaller tax bill or a larger refund. By carefully following these steps and accurately completing Schedule 1, Line 21, you can successfully claim the student loan interest deduction on your IRS Form 1040.

How to Enter Student Loan Interest in ProSeries: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Eligibility Criteria: Ensure your loan qualifies and your income meets IRS limits for deduction

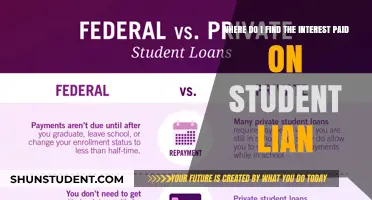

To claim the student loan interest deduction, it’s crucial to first ensure your loan qualifies under IRS guidelines. The loan must have been taken out solely for qualified education expenses, such as tuition, fees, room and board, books, and supplies. Loans from a spouse, relative, or qualified employer plan generally do not qualify. Additionally, the loan must have been used for education provided during an academic period for an eligible student, who was enrolled at least half-time in a program leading to a degree, certificate, or other recognized credential. Consolidation loans also qualify if they were used to refinance eligible student loans.

Next, verify that the student loan interest you paid is eligible for deduction. The interest must have been paid on a qualified education loan during the tax year, and you must be legally obligated to pay the interest. If you’re a parent who took out a loan for your child, the interest is deductible only if you claim the child as a dependent on your tax return. Furthermore, the deduction is reduced or eliminated if the loan was used for any expenses other than qualified education costs. Keep detailed records of your loan payments and interest statements to substantiate your claim.

Your income level plays a significant role in determining eligibility for the student loan interest deduction. The IRS sets annual income limits that phase out the deduction for higher earners. For tax year 2023, the deduction begins to phase out for single filers with modified adjusted gross income (MAGI) above $70,000 and is completely phased out at $85,000. For married couples filing jointly, the phaseout begins at $145,000 and ends at $175,000. If your income exceeds these thresholds, you may not qualify for the full deduction or any deduction at all. Use IRS Form 1040 and Schedule 1 to calculate your MAGI and determine your eligibility.

Another critical eligibility factor is your tax filing status. You cannot claim the student loan interest deduction if you file as “married filing separately.” This restriction is important to note, as it limits the ability of married couples to claim the deduction if they choose to file separate returns. Additionally, you must claim the deduction for the tax year in which the interest was actually paid, not when the loan was taken out. If you prepaid interest in a future year, you must spread the deduction over the life of the loan.

Finally, ensure that you have not claimed other education-related tax benefits for the same expenses. For example, if you claimed the American Opportunity Credit or Lifetime Learning Credit for the same student in the same year, the qualified expenses used for those credits cannot also be used to claim the student loan interest deduction. Carefully review your education expenses and tax credits to avoid double-dipping, as this could result in an IRS audit or denial of your deduction. By meeting these eligibility criteria, you can confidently proceed to claim the student loan interest deduction on your tax return.

How to Report Student Loan Interest on Your 1040EZ Form

You may want to see also

Explore related products

![]()

Deduction Limits: Maximum deduction is $2,500 annually, phased out at higher incomes

When it comes to claiming the student loan interest deduction, understanding the deduction limits is crucial. The maximum deduction allowed is $2,500 per year, which can significantly reduce your taxable income. However, this benefit is not available to everyone, as it phases out for taxpayers with higher incomes. To claim this deduction, you’ll typically enter the information on Schedule 1 (Form 1040) and then transfer the amount to your Form 1040. It’s important to note that this deduction is an above-the-line adjustment, meaning you don’t need to itemize deductions to claim it.

The phase-out for the student loan interest deduction begins at specific income thresholds. For single filers, the phase-out starts at a modified adjusted gross income (MAGI) of $70,000 and is completely phased out at $85,000. For married couples filing jointly, the phase-out range is between $140,000 and $170,000. If your income falls within these ranges, your deduction will be reduced proportionally. For example, if you’re a single filer with a MAGI of $80,000, you’ll only be eligible for a partial deduction. Understanding these limits ensures you don’t overclaim or miss out on the benefit entirely.

To calculate your eligible deduction, you’ll need to know the amount of student loan interest you paid during the tax year, which your loan servicer should report on Form 1098-E. If your income is below the phase-out thresholds, you can deduct up to $2,500 of the interest paid. However, if your income exceeds these limits, you’ll need to use the IRS worksheet provided in the instructions for Schedule 1 to determine your reduced deduction amount. This step is essential to ensure accuracy and compliance with IRS rules.

It’s also worth noting that the student loan interest deduction has specific eligibility requirements. The loan must have been taken out for qualified education expenses, such as tuition, fees, and room and board, and the funds must have been used for the taxpayer, their spouse, or dependents. Additionally, the deduction is only available if the taxpayer is legally obligated to pay the interest and is not claimed as a dependent on someone else’s tax return. Meeting these criteria is vital to qualify for the deduction.

Finally, while the $2,500 maximum deduction may seem modest, it can still provide meaningful tax savings, especially for those in the lower phase-out range. For instance, if you’re in the 22% tax bracket, a $2,500 deduction could save you $550 in taxes. To enter this deduction, you’ll report the interest paid on line 21 of Schedule 1 and then transfer the deduction amount to line 15 of Form 1040. Keeping track of your income and interest payments throughout the year will help you maximize this benefit and avoid any surprises during tax season.

When Do Unsub Student Loans Begin Accruing Interest?

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

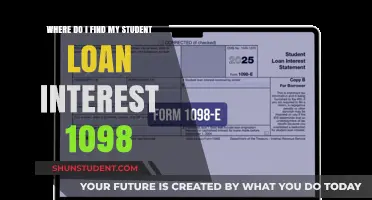

Documentation Needed: Gather Form 1098-E from your lender to report interest paid

When preparing to claim the student loan interest deduction on your tax return, one of the most critical steps is gathering the necessary documentation. The primary document you’ll need is Form 1098-E, which is provided by your student loan lender. This form reports the amount of interest you paid on your student loans during the tax year. Without Form 1098-E, you cannot accurately report the interest paid, as the IRS requires this specific form to verify your deduction. It’s essential to ensure you receive this form from your lender, as it is the official record of your interest payments.

To obtain Form 1098-E, start by checking your mail or email inboxes, as lenders typically send this form to borrowers by January 31st of the following year. If you haven’t received it by early February, log into your student loan account online or contact your lender directly to request a copy. Most lenders provide access to Form 1098-E through their online portals, allowing you to download or view it electronically. Keep in mind that you should only receive this form if you paid at least $600 in student loan interest during the year; otherwise, the lender is not required to send it, though you can still request it.

Once you have Form 1098-E in hand, review it carefully to ensure the information is accurate. The form will include your name, taxpayer identification number, the lender’s name, and the total amount of interest paid during the tax year. If you notice any discrepancies, such as an incorrect interest amount or personal information, contact your lender immediately to request a corrected form. Accurate documentation is crucial, as errors can lead to delays in processing your tax return or potential issues with the IRS.

After verifying the accuracy of Form 1098-E, you’ll need to use the information it provides to complete your tax return. Specifically, the interest amount reported on Form 1098-E is entered on Schedule 1 (Form 1040), Line 21, which is labeled "Student loan interest deduction." This line is where you report the total interest paid on qualified student loans. Ensure you transfer the exact amount from Form 1098-E to avoid calculation errors. If you paid interest to multiple lenders, you should receive a separate Form 1098-E from each one, and you’ll need to add up all the interest amounts to report the total on your tax return.

Finally, keep Form 1098-E and any other related documentation in your tax records for at least three years. This includes any correspondence with your lender regarding the form or corrections made to it. Proper record-keeping is essential in case the IRS requests additional information or if you need to refer back to your records in the future. By gathering and accurately reporting the information from Form 1098-E, you can confidently claim the student loan interest deduction and maximize your tax savings.

Maximize Your Tax Savings: Understanding Student Loan Interest Deductions

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Filing Status Impact: Deduction availability varies based on married filing jointly/separately status

When filing your taxes, the availability of the student loan interest deduction can be significantly influenced by your filing status, particularly whether you are filing jointly or separately as a married couple. This distinction is crucial because it directly impacts the eligibility criteria and the amount you can deduct. For married couples filing jointly, the student loan interest deduction is generally more straightforward. Both spouses can combine their eligible student loan interest payments, up to the annual limit of $2,500, provided their modified adjusted gross income (MAGI) falls within the specified phase-out range. This joint filing status often maximizes the deduction potential, as it allows the couple to pool their resources and potentially claim a larger deduction.

In contrast, married couples who choose to file separately face stricter limitations. If you and your spouse file separate returns, you are not eligible to claim the student loan interest deduction at all. This rule is designed to prevent couples from double-dipping on deductions and ensures consistency in tax reporting. Therefore, if you anticipate significant student loan interest payments, filing jointly may be more advantageous, assuming your combined income does not exceed the phase-out thresholds. It’s essential to weigh the pros and cons of each filing status, considering both the student loan interest deduction and other tax implications.

The phase-out ranges for the student loan interest deduction also differ based on filing status. For married couples filing jointly, the deduction begins to phase out at a MAGI of $140,000 and is completely eliminated at $170,000. For those filing separately, the phase-out range is significantly lower, starting at $70,000 and ending at $85,000. This disparity underscores the importance of understanding how your filing status affects your eligibility and the potential deduction amount. If your income falls within these ranges, careful planning and consideration of your filing status can help optimize your tax benefits.

Another critical aspect to consider is the treatment of student loan interest when one spouse has loans and the other does not. If you file jointly, the deduction can still be claimed as long as the loan is in the name of either spouse, and the couple meets the income requirements. However, if you file separately, the spouse who did not take out the loan cannot claim the deduction, even if they contributed to the payments. This highlights the importance of coordinating financial decisions with your spouse to ensure you maximize available deductions.

Lastly, it’s worth noting that the decision to file jointly or separately should not be based solely on the student loan interest deduction. Other factors, such as tax credits, deductions, and overall tax liability, must also be considered. Consulting a tax professional can provide personalized guidance tailored to your specific financial situation. When filing your taxes, the student loan interest deduction is entered on Schedule 1 (Form 1040), line 21, regardless of your filing status. However, understanding how your filing status impacts eligibility and deduction limits is key to accurately completing this section and maximizing your tax savings.

Diverse Passions: Exploring the Term for Students with Varied Interests

You may want to see also

Frequently asked questions

You enter the student loan interest deduction on Schedule 1 (Form 1040), Line 20. This line is specifically for reporting deductible student loan interest.

Yes, the student loan interest deduction is an adjustment to income, so you can claim it even if you take the standard deduction. It does not require itemizing deductions.

If your deductible interest exceeds $2,500, you can only claim up to that amount. Any excess cannot be carried over to future tax years.

While not required, Form 1098-E (provided by your loan servicer) is helpful for verifying the amount of interest paid. You can still claim the deduction if you don’t receive this form, but you’ll need to ensure the amount is accurate.

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![[Old Version] TurboTax Deluxe 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/719rCYQpjdL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)