The topic of forgiving student debt has become a pressing issue in recent years, as millions of individuals struggle to repay their loans, often facing financial hardship and limited opportunities for economic mobility. With the cost of higher education skyrocketing, many students have been forced to take on substantial debt to pursue their academic goals, only to find themselves burdened by repayments that can last for decades. As a result, policymakers, educators, and advocates have begun to question the sustainability of this system and explore potential solutions, including widespread student debt forgiveness. By examining the reasons behind this growing movement, we can gain a deeper understanding of the economic, social, and moral implications of student debt and the potential benefits of alleviating this burden for individuals and society as a whole.

Explore related products

What You'll Learn

- Economic Stimulus: Debt relief boosts spending, aiding economic recovery and growth

- Racial Wealth Gap: Forgiveness addresses disparities in Black and Brown communities

- Education Accessibility: Reduces barriers, encouraging more students to pursue higher education

- Mental Health Impact: Alleviates stress and anxiety for millions of borrowers

- Political Strategy: Aims to gain voter support and address systemic inequality

![]()

Economic Stimulus: Debt relief boosts spending, aiding economic recovery and growth

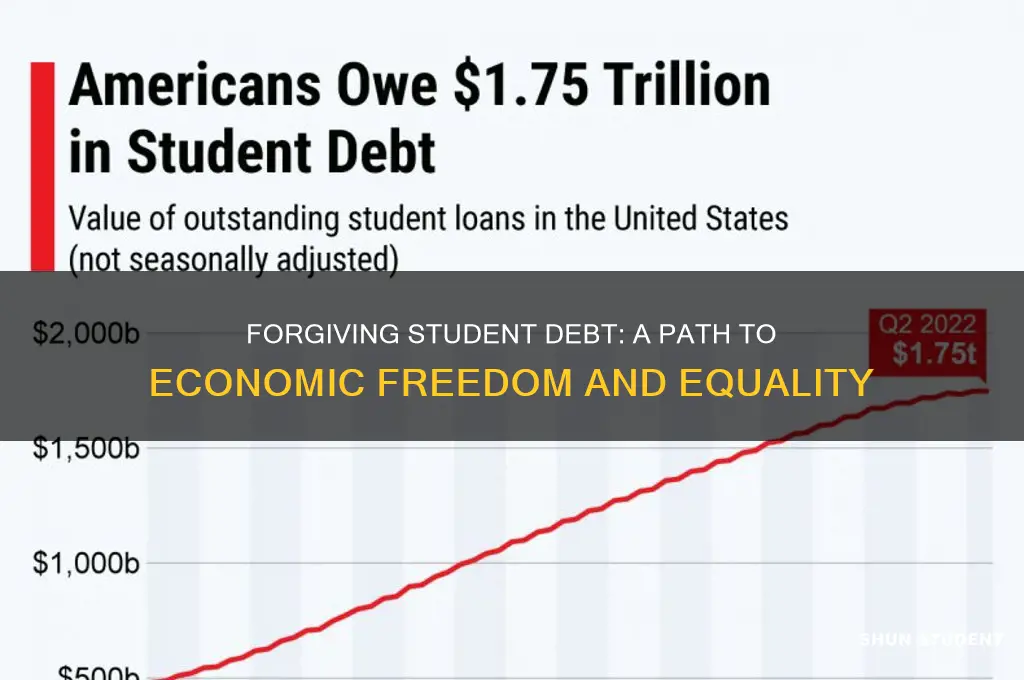

Student debt relief isn't just about easing individual burdens; it's a strategic economic lever. When burdened with debt, individuals prioritize repayment over discretionary spending, stifling economic activity. Forgiving student debt injects disposable income directly into the hands of millions, particularly younger adults with higher propensity to spend. This isn't theoretical – a 2021 study by the Roosevelt Institute estimated that canceling $50,000 in student debt per borrower could boost GDP by $86 billion to $108 billion annually over the next decade.

Discover If You Qualify for Student Loan Forgiveness: A Guide

You may want to see also

Explore related products

![]()

Racial Wealth Gap: Forgiveness addresses disparities in Black and Brown communities

The racial wealth gap in the United States is a stark reminder of systemic inequalities, with Black and Brown families holding a fraction of the wealth of their white counterparts. According to the Federal Reserve, the median wealth of white families is nearly ten times that of Black families and eight times that of Hispanic families. Student debt forgiveness emerges as a targeted intervention to address this disparity, as Black and Brown borrowers are disproportionately burdened by higher education loans. For example, 83% of Black bachelor’s degree recipients graduate with debt, compared to 69% of white graduates, and their average debt is nearly $7,400 higher just four years after graduation. This disparity is compounded by lower family wealth, limiting the ability to repay loans without sacrificing other financial priorities.

Analyzing the mechanics of this issue reveals how student debt exacerbates racial wealth inequality. Black and Brown borrowers are more likely to attend underfunded institutions, rely on riskier loans, and face higher default rates due to systemic barriers in employment and wage gaps. For instance, a Brookings Institution study found that the typical Black borrower still owes 95% of their loan balance 20 years after starting college, compared to 60% for white borrowers. Debt forgiveness, particularly when paired with income-driven repayment plans, can disrupt this cycle by freeing up income for wealth-building activities like homeownership, entrepreneurship, or retirement savings—areas where Black and Brown families lag significantly.

To implement effective debt forgiveness with racial equity in mind, policymakers must consider targeted approaches. Universal forgiveness, while beneficial, may not sufficiently address the scale of disparity. Instead, proposals like forgiving up to $50,000 in debt for borrowers in low-income communities or those attending historically Black colleges and universities (HBCUs) could have a more direct impact. Additionally, pairing forgiveness with investments in affordable higher education and workforce development programs can create long-term pathways to financial stability for marginalized communities. Caution must be taken, however, to avoid creating administrative hurdles that disproportionately exclude Black and Brown borrowers from accessing relief.

Persuasively, the moral and economic case for addressing the racial wealth gap through student debt forgiveness is clear. Every dollar forgiven for a Black or Brown borrower is a step toward rectifying decades of discriminatory policies, from redlining to predatory lending. Economically, reducing debt burdens in these communities can stimulate local economies, increase tax revenues, and reduce reliance on public assistance programs. Critics argue that forgiveness is a temporary fix, but it is a necessary first step in a broader strategy to dismantle systemic barriers. Without it, the wealth gap will continue to widen, perpetuating cycles of poverty and limiting social mobility for generations to come.

Descriptively, imagine a Black family in the Southeast, where the legacy of Jim Crow laws still shadows economic opportunities. The parents, both burdened by student debt, struggle to save for their children’s education or invest in a home. Debt forgiveness could transform their reality, allowing them to build equity through homeownership or start a small business. Multiply this scenario across millions of families, and the potential for generational wealth creation becomes evident. Forgiveness is not just about erasing numbers on a balance sheet; it’s about unlocking doors that have been systematically closed to Black and Brown communities for centuries.

Peace Corps Service: A Path to Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Education Accessibility: Reduces barriers, encouraging more students to pursue higher education

Student debt forgiveness isn’t just about alleviating financial strain—it’s a strategic move to dismantle barriers that prevent millions from accessing higher education. Consider this: in 2023, the average student loan debt in the U.S. exceeded $37,000, a burden that disproportionately affects low-income and minority students. For many, this debt looms as an insurmountable obstacle, deterring them from even applying to college. By forgiving student debt, we reset the playing field, signaling that education is a right, not a privilege. This shift encourages individuals who might have been discouraged by financial risks to pursue degrees, fostering a more inclusive and educated society.

To understand the impact, imagine a high school senior from a low-income family. Despite qualifying for a full scholarship, they’re told their expected family contribution is $5,000—an impossible sum. Fear of loans drives them to forgo college altogether. Now, with debt forgiveness policies in place, this student sees a future where education isn’t synonymous with lifelong debt. They enroll, knowing that systemic support exists to cushion financial risks. Multiply this scenario by millions, and you see how debt forgiveness acts as a catalyst, transforming higher education from an exclusive club into an accessible pathway for all.

Critics argue that debt forgiveness benefits only those who’ve already attended college, but its ripple effects extend far beyond current borrowers. When debt is forgiven, institutions are pressured to reevaluate tuition costs and funding models, making education more affordable for future students. For instance, colleges might invest in need-based grants or cap tuition increases, knowing that excessive debt undermines their long-term sustainability. This systemic change reduces barriers at the entry point, ensuring that the next generation faces fewer financial hurdles when considering higher education.

Practical steps can amplify this impact. Pairing debt forgiveness with initiatives like income-driven repayment plans or tuition-free community college creates a comprehensive support system. For example, a student could attend community college debt-free, transfer to a four-year institution with reduced tuition, and graduate with minimal debt. Add in loan forgiveness programs for public service or STEM fields, and you incentivize students to pursue careers that benefit society. These layered approaches ensure accessibility isn’t just theoretical—it’s actionable, tangible, and sustainable.

Ultimately, forgiving student debt isn’t an act of charity; it’s an investment in a more equitable future. By reducing financial barriers, we empower individuals to pursue education without the shadow of debt looming over them. This, in turn, drives innovation, strengthens the workforce, and uplifts communities. Education accessibility isn’t just a moral imperative—it’s a strategic one. When we remove barriers, we don’t just change lives; we transform societies.

Will Consolidated Student Loans Be Forgiven? Exploring Potential Debt Relief Options

You may want to see also

Explore related products

$14.95 $14.95

![]()

Mental Health Impact: Alleviates stress and anxiety for millions of borrowers

Student debt isn't just a financial burden; it's a mental health crisis. Studies show a direct correlation between student loan debt and increased levels of stress, anxiety, and depression. The constant worry about repayments, the feeling of being trapped, and the inability to plan for the future take a significant toll on borrowers' well-being. For millions, student debt forgiveness isn't just about money, it's about reclaiming mental peace.

Imagine carrying a weight that constantly pulls you down, affecting your sleep, your relationships, and your overall sense of self-worth. That's the reality for many burdened by student loans.

The psychological impact of debt is multifaceted. It triggers a constant state of fight-or-flight, releasing stress hormones like cortisol, which over time, can lead to physical health problems like heart disease and weakened immunity. Anxiety disorders, characterized by excessive worry and fear, are also prevalent among borrowers, manifesting as panic attacks, difficulty concentrating, and avoidance behaviors. Depression, marked by persistent sadness, loss of interest, and feelings of hopelessness, often accompanies the financial strain.

A 2018 study by the Center for Responsible Lending found that student loan borrowers were more likely to experience symptoms of depression and anxiety than those without debt. This isn't surprising considering the long-term nature of student loans, often stretching for decades, creating a sense of perpetual financial servitude.

Forgiving student debt isn't just an economic policy; it's a public health intervention. By lifting this burden, we can significantly improve the mental well-being of millions. Imagine the relief of waking up without the weight of debt crushing your spirit. Imagine the freedom to pursue career paths driven by passion rather than financial necessity. Imagine the ability to plan for a future that includes homeownership, starting a family, or simply saving for retirement without the constant specter of debt looming overhead.

The mental health benefits of student debt forgiveness extend beyond individual borrowers. A healthier population translates to a more productive workforce, reduced healthcare costs, and a more vibrant society. It's an investment in our collective well-being, a step towards a future where financial burdens don't dictate our mental health.

CIA Student Loan Forgiveness: Fact or Fiction? What You Need to Know

You may want to see also

Explore related products

![]()

Political Strategy: Aims to gain voter support and address systemic inequality

Student debt forgiveness has emerged as a potent political strategy, leveraging both immediate voter appeal and long-term systemic change. By canceling debt, policymakers can directly alleviate financial burdens for millions, a move that resonates strongly with younger demographics—a critical voting bloc often disillusioned by traditional politics. For instance, forgiving $10,000 in student debt per borrower could immediately improve credit scores, increase homeownership rates, and stimulate consumer spending, creating a ripple effect across the economy. This approach not only garners support from directly impacted voters but also positions leaders as champions of economic fairness.

However, the strategy’s effectiveness hinges on its ability to address systemic inequality, not just individual relief. Student debt disproportionately burdens low-income and minority communities, perpetuating cycles of poverty. A targeted forgiveness plan—such as canceling debt for borrowers earning below $50,000 annually or those who attended predatory for-profit institutions—could dismantle barriers to wealth accumulation for marginalized groups. Pairing forgiveness with reforms like tuition-free public college or income-driven repayment plans ensures the policy tackles root causes, not just symptoms, of educational inequity.

Critics argue that broad forgiveness benefits higher-income earners disproportionately, diluting its impact on inequality. To counter this, policymakers could cap eligibility based on income thresholds or loan amounts, ensuring resources reach those most in need. For example, limiting forgiveness to borrowers with less than $50,000 in debt or household incomes under $100,000 would focus benefits on lower- and middle-class families. Such precision transforms the policy from a populist gesture into a tool for economic justice, aligning voter appeal with systemic reform.

Implementing student debt forgiveness as a political strategy requires careful messaging and coalition-building. Framing the policy as an investment in the future workforce—rather than a handout—can neutralize opposition. Highlighting success stories, such as nurses or teachers freed from debt to pursue their careers, humanizes the issue and broadens support. Additionally, partnering with grassroots organizations advocating for racial and economic justice amplifies the policy’s reach and credibility. When executed thoughtfully, student debt forgiveness becomes more than a campaign promise—it’s a transformative policy that bridges political expediency with lasting societal change.

Food Stamps and Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

The government is forgiving student debt to alleviate the financial burden on millions of borrowers, stimulate economic growth, and address systemic inequalities exacerbated by student loan debt.

Eligibility for student debt forgiveness varies by program, but typically includes borrowers with federal student loans who meet specific income thresholds, loan types, and repayment histories.

Student debt forgiveness can boost the economy by freeing up disposable income for borrowers, increasing consumer spending, and enabling individuals to invest in homes, businesses, and other financial goals.

While it may seem unfair to some, student debt forgiveness aims to address broader systemic issues and provide relief to those struggling under the weight of debt, which can benefit society as a whole.

Student debt forgiveness is funded through existing government budgets or reallocated funds, so it does not directly result in higher taxes for individuals. However, the long-term fiscal impact depends on how the government manages its finances.