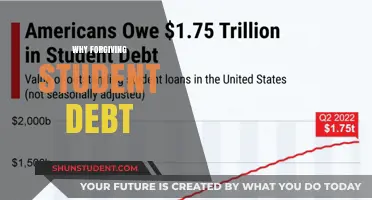

The Supreme Court's decision to block President Biden's student loan forgiveness program has sparked widespread debate and concern, as it directly impacts millions of borrowers seeking financial relief. The Court's ruling, which halted the implementation of the plan, was based on legal challenges arguing that the administration overstepped its authority under the HEROES Act and that the program lacked proper congressional approval. Critics of the decision argue that it undermines efforts to address the growing student debt crisis, which burdens over 40 million Americans with a collective $1.7 trillion in loans. Proponents, however, contend that the program raises constitutional and fiscal concerns, emphasizing the need for legislative action rather than executive intervention. The ruling has left borrowers in limbo, highlighting the complex intersection of law, politics, and economic policy in addressing one of the nation's most pressing financial issues.

| Characteristics | Values |

|---|---|

| Legal Basis | The Supreme Court ruled that the Biden administration overstepped its authority under the HEROES Act, which allows loan modifications but not mass forgiveness without explicit congressional approval. |

| Separation of Powers | The Court emphasized that large-scale debt forgiveness is a legislative function, not an executive action, requiring congressional authorization. |

| Economic Impact | Concerns about the $400 billion cost of the program and its potential impact on federal spending and taxpayer burden. |

| Plaintiffs' Standing | The Court upheld the standing of Republican-led states (Missouri, Arkansas) and loan servicers who argued they would be financially harmed. |

| Statutory Interpretation | The HEROES Act was interpreted narrowly, limiting the Education Secretary's power to waive student loans beyond modest adjustments. |

| Political Divide | The decision reflects a 6-3 conservative majority ruling against a key Democratic policy initiative. |

| Precedent for Executive Action | The ruling sets a precedent limiting executive branch authority in implementing sweeping financial policies without congressional backing. |

| Impact on Borrowers | Approximately 40 million borrowers were affected, with $430 billion in potential debt relief blocked. |

| Future of Student Loan Policy | The decision shifts the focus back to Congress for any broad student loan forgiveness measures. |

| Public Reaction | Mixed reactions, with critics arguing it harms low-income borrowers and supporters praising adherence to constitutional limits. |

Explore related products

What You'll Learn

- Legal Authority: Does the Biden administration have the power to forgive student loans without Congress

- Standing Issue: Are plaintiffs in lawsuits against forgiveness legally harmed to challenge it

- Separation of Powers: Is loan forgiveness an overreach of executive authority

- Economic Impact: How does blocking forgiveness affect borrowers and the economy

- Political Motives: Are Supreme Court decisions influenced by partisan politics

![]()

Legal Authority: Does the Biden administration have the power to forgive student loans without Congress?

The Biden administration's plan to forgive up to $20,000 in student loan debt per borrower hinges on a critical question: does the executive branch possess the legal authority to act unilaterally, without congressional approval? This issue lies at the heart of the Supreme Court's recent decision to block the initiative. The administration's argument rests on the HEROES Act of 2003, which grants the Secretary of Education the power to "waive or modify" student loan provisions during national emergencies. The COVID-19 pandemic, they contend, constitutes such an emergency, justifying broad debt relief. However, opponents argue this interpretation stretches the law's intent, which was designed to provide targeted assistance to military personnel and those directly impacted by disasters, not to implement sweeping policy changes.

To understand the legal debate, consider the HEROES Act's original purpose. Enacted after the September 11 attacks, it aimed to protect service members from financial hardship while deployed. The law allows for adjustments like interest rate reductions or payment deferments, but its scope is limited. The Biden administration's plan, by contrast, involves canceling principal balances for millions of borrowers, a move critics view as legislative overreach. This raises a fundamental question: can an executive agency redefine the terms of a statute to achieve policy goals Congress never explicitly authorized?

A comparative analysis of past executive actions provides insight. During the Obama administration, the Department of Education used the HEROES Act to create income-driven repayment plans, a more modest exercise of authority. In contrast, the current proposal resembles legislative action, traditionally the domain of Congress. The Supreme Court’s conservative majority has signaled skepticism toward expansive interpretations of executive power, particularly when they reshape economic policy without clear statutory basis. This judicial perspective aligns with the principle of separation of powers, which requires Congress to authorize significant spending initiatives.

Practically, the stakes are immense. If the Supreme Court upholds the administration’s authority, it could set a precedent for future executive actions on debt relief or other financial matters. Conversely, a ruling against the administration would reinforce congressional primacy in fiscal policy, limiting the executive branch’s ability to act unilaterally. For borrowers, the outcome determines whether billions in debt will be erased or remain a financial burden. To navigate this uncertainty, individuals should continue making payments if possible, monitor legal developments, and explore alternative relief options like income-driven plans or public service loan forgiveness.

In conclusion, the legal authority debate centers on the boundaries of executive power and the limits of statutory interpretation. The Biden administration’s reliance on the HEROES Act represents a bold but contested use of existing law. As the Supreme Court weighs this issue, the decision will shape not only student loan policy but also the balance of power between the executive and legislative branches. For now, borrowers must remain informed and prepared for either outcome.

Massachusetts Tax Rules: Student Loan Forgiveness Explained

You may want to see also

Explore related products

![]()

Standing Issue: Are plaintiffs in lawsuits against forgiveness legally harmed to challenge it?

The Supreme Court's decision to block student loan forgiveness hinges critically on the legal doctrine of standing, a threshold question that determines whether plaintiffs have the right to bring their case to court. At its core, standing requires plaintiffs to demonstrate they have suffered a concrete and particularized injury directly caused by the challenged action and likely to be redressed by a favorable ruling. In the context of student loan forgiveness, the plaintiffs—often states, servicers, or individuals—must prove they are legally harmed by the forgiveness program. This is no trivial task, as the injury cannot be speculative or generalized; it must be tangible and specific to the plaintiff. For instance, a state might argue financial harm due to reduced tax revenue from forgiven loans, but such claims often face scrutiny for lacking direct causation or measurable impact.

Consider the case of *Biden v. Nebraska*, where several states challenged the student loan forgiveness plan. The states argued that the forgiveness program would harm them by reducing revenue from student loan servicers operating within their borders. However, the Court questioned whether this harm was sufficiently concrete and particularized. The states’ injury relied on a chain of assumptions: that servicers would lose revenue, that this loss would translate to reduced state income, and that the states had a legal interest in this revenue stream. Such attenuated harm often fails the standing test, as it lacks the immediacy and directness required by law. This highlights a critical challenge for plaintiffs: proving a clear, legally cognizable injury rather than relying on hypothetical or indirect consequences.

From a practical standpoint, plaintiffs seeking to establish standing must focus on tangible, measurable harms. For example, a loan servicer might argue that forgiveness disrupts its contractual rights to collect payments, a claim rooted in specific financial losses. Similarly, an individual plaintiff could assert that the program unfairly benefits others at their expense, though this argument often struggles to meet the particularized injury requirement. To strengthen their case, plaintiffs should provide detailed evidence of harm, such as financial statements, contractual obligations, or statutory provisions directly linking the forgiveness program to their injury. Without such specificity, their claims risk being dismissed as generalized grievances, insufficient to confer standing.

Comparatively, cases where standing is successfully established often involve plaintiffs with direct, identifiable stakes. For instance, in environmental lawsuits, plaintiffs typically demonstrate harm by showing how pollution directly affects their property or health. In contrast, student loan forgiveness cases often involve more abstract harms, such as economic ripple effects or perceived unfairness. This distinction underscores why standing remains a formidable hurdle in these cases. Plaintiffs must bridge the gap between policy disagreement and legal injury, a task that requires precision and a deep understanding of the standing doctrine’s nuances.

Ultimately, the standing issue in student loan forgiveness lawsuits serves as a reminder of the judiciary’s role in limiting access to the courts to those with genuine, legally cognizable disputes. For plaintiffs, the key takeaway is clear: success depends on demonstrating a concrete, particularized injury directly tied to the forgiveness program. Without this, their challenges are likely to falter at the courthouse steps, leaving the broader policy debate to other branches of government. This legal barrier underscores the complexity of using the courts to challenge executive actions, particularly in cases where the alleged harm is diffuse or indirect.

Can Forgiven Student Loans Be Reinstated? Understanding the Risks and Rules

You may want to see also

Explore related products

![]()

Separation of Powers: Is loan forgiveness an overreach of executive authority?

The Supreme Court's decision to block President Biden's student loan forgiveness plan hinges on a fundamental principle of American governance: the separation of powers. This doctrine, enshrined in the Constitution, divides federal authority among the legislative, executive, and judicial branches, creating a system of checks and balances. The Court's ruling raises a critical question: does the executive branch, through the Department of Education, have the unilateral authority to cancel hundreds of billions of dollars in student debt without explicit congressional approval?

The Executive's Argument: Broad Interpretations and Emergency Powers

Proponents of the loan forgiveness plan argue that the Higher Education Relief Opportunities for Students (HEROES) Act of 2003 grants the Secretary of Education broad authority to modify student loan terms during national emergencies. They contend that the COVID-19 pandemic constitutes such an emergency, justifying the use of this power to provide economic relief to millions of borrowers. This interpretation emphasizes the executive branch's flexibility in responding to crises, particularly when Congress is perceived as gridlocked or slow to act.

Judicial Scrutiny: Limits on Executive Action

The Supreme Court's majority opinion, however, takes a more restrictive view. The justices argue that the HEROES Act does not provide carte blanche for the executive branch to rewrite federal law. They emphasize that the power to appropriate funds and forgive debts lies primarily with Congress, as outlined in the Constitution's Appropriations Clause. By bypassing Congress, the Court asserts, the executive branch oversteps its constitutional bounds, undermining the separation of powers and setting a dangerous precedent for future unilateral actions.

Practical Implications: Balancing Relief and Responsibility

From a practical standpoint, the Court's decision highlights the tension between providing immediate relief to struggling borrowers and maintaining fiscal responsibility. While loan forgiveness could alleviate financial burdens for millions, it also raises concerns about fairness, economic impact, and the long-term sustainability of federal student loan programs. The ruling underscores the importance of a balanced approach, where executive actions are tempered by legislative oversight and judicial review.

Moving Forward: A Call for Collaborative Solutions

The Supreme Court's block on student loan forgiveness serves as a reminder that addressing complex issues like student debt requires collaboration across branches of government. Rather than relying on broad interpretations of executive authority, policymakers should work together to craft targeted, sustainable solutions. This might include bipartisan legislation that provides relief to specific groups of borrowers, reforms the student loan system to prevent future crises, and ensures accountability in the use of taxpayer funds. By respecting the separation of powers, Congress and the executive branch can develop policies that are both effective and constitutionally sound.

Can All Student Loans Be Forgiven? Exploring the Possibility and Impact

You may want to see also

Explore related products

$14.95 $14.95

![]()

Economic Impact: How does blocking forgiveness affect borrowers and the economy?

The Supreme Court's decision to block student loan forgiveness has immediate and profound economic implications, particularly for the 43 million borrowers holding a combined $1.7 trillion in debt. For individual borrowers, the absence of forgiveness means a return to monthly payments averaging $393, a significant financial burden for those earning median incomes of $46,000 annually. This reallocation of funds from discretionary spending to debt repayment stifles personal financial growth, delaying milestones like homeownership, entrepreneurship, and retirement savings. For instance, a borrower with $30,000 in debt at 5% interest would pay $318 monthly, diverting $3,816 annually from potential investments or savings.

From a macroeconomic perspective, blocking forgiveness dampens consumer spending, a driver of 70% of U.S. GDP. With 1 in 4 borrowers reporting difficulty meeting basic needs, reduced disposable income translates to lower demand for goods and services, particularly in sectors like retail, housing, and healthcare. A Brookings Institution study estimates that widespread forgiveness could inject $100 billion annually into the economy through increased spending. Conversely, the absence of this stimulus risks slowing economic growth, particularly in a post-pandemic recovery marked by inflation and labor market uncertainties.

The racial wealth gap also widens under this decision. Black borrowers, who owe an average of $52,000—50% more than their white peers—face disproportionate hardship. Without forgiveness, their debt-to-income ratios remain unsustainable, perpetuating cycles of financial instability. For example, a Black borrower earning $40,000 annually with $50,000 in debt at 6% interest would allocate 19% of their income to payments, compared to 12% for a white borrower with $30,000 in debt. This disparity undermines economic mobility and exacerbates systemic inequalities.

Finally, the decision impacts labor market dynamics. Burdened by debt, borrowers are less likely to pursue career changes, entrepreneurship, or public service roles, stifling innovation and workforce adaptability. A 2022 survey found that 54% of borrowers would start a business if debt-free, while 45% would switch to more fulfilling but lower-paying jobs. By blocking forgiveness, the Court inadvertently constrains economic dynamism, limiting the potential for growth in high-impact sectors like education, healthcare, and green energy.

In summary, the economic consequences of blocking student loan forgiveness are far-reaching, affecting individual financial health, consumer spending, racial equity, and labor market innovation. Policymakers and stakeholders must consider these ripple effects when evaluating the long-term costs of this decision, as the economy loses not just immediate spending power but also the transformative potential of a debt-free workforce.

Do Federal Student Loans Disappear After Death? Key Facts Explained

You may want to see also

Explore related products

![]()

Political Motives: Are Supreme Court decisions influenced by partisan politics?

The Supreme Court's decision to block President Biden's student loan forgiveness plan has sparked intense debate about the role of partisan politics in judicial rulings. Critics argue that the Court’s conservative majority, appointed by Republican presidents, systematically aligns with GOP policy goals, raising questions about judicial impartiality. This case exemplifies a broader trend where high-stakes decisions appear to reflect ideological leanings rather than legal merit alone.

Consider the legal rationale behind the Court’s ruling: it hinged on the interpretation of the HEROES Act, a statute granting the executive branch limited authority to modify student loans during national emergencies. The majority argued the forgiveness plan exceeded this scope, but dissenters countered that the law allows flexibility in crisis situations, such as the COVID-19 pandemic. This split reveals how statutory interpretation can become a tool for advancing political agendas. For instance, the conservative justices’ narrow reading of the HEROES Act aligns with Republican opposition to broad executive action, while the liberal dissent mirrors Democratic support for expansive relief measures.

To assess whether partisan motives drive these decisions, examine the appointment process. Supreme Court justices are nominated by the president and confirmed by the Senate, both inherently political bodies. Since the 1980s, nominees have increasingly been chosen for their ideological reliability rather than judicial temperament. For example, Justice Amy Coney Barrett’s expedited confirmation weeks before the 2020 election solidified a 6-3 conservative majority, a move widely seen as securing Republican influence on the Court for decades. This politicized selection process naturally raises concerns about justices prioritizing party loyalty over impartial judgment.

However, defenders of the Court argue that justices often rule against their appointing party’s interests, citing examples like Chief Justice John Roberts upholding the Affordable Care Act. Yet, such instances are exceptions rather than the rule. Statistical analyses show a strong correlation between justices’ voting patterns and the party of the president who appointed them, particularly in cases with significant political implications. In the student loan case, the conservative majority’s ruling aligns neatly with Republican critiques of the plan as fiscally irresponsible and legally dubious.

Ultimately, while the Supreme Court claims to operate above the political fray, its decisions in cases like student loan forgiveness suggest otherwise. The interplay between judicial appointments, ideological alignment, and ruling outcomes indicates that partisan politics undeniably shapes the Court’s actions. For those seeking to reform the system, depoliticizing the appointment process or imposing term limits on justices could be practical steps toward restoring public trust in the Court’s impartiality.

Unlock Debt-Free Future: Guide to Student Loan Forgiveness Applications

You may want to see also

Frequently asked questions

The Supreme Court blocked student loan forgiveness based on legal challenges arguing that the Biden administration overstepped its authority under the HEROES Act, which allows loan modifications during national emergencies, and that such broad forgiveness required explicit congressional approval.

The Supreme Court ruled that the Biden administration’s use of the HEROES Act to forgive student loans exceeded the act’s scope, as it was intended for targeted relief, not widespread debt cancellation. The Court also cited the Major Questions Doctrine, requiring clear congressional authorization for significant policy changes.

The plan was challenged by several Republican-led states and conservative groups, who argued that the Biden administration lacked the legal authority to implement such broad forgiveness and that it would harm state tax revenues tied to loan servicers.

While the Supreme Court’s decision blocked the current plan, forgiveness could still occur if Congress passes legislation explicitly authorizing it or if the administration pursues a new legal pathway. However, such actions would likely face political and legal hurdles.