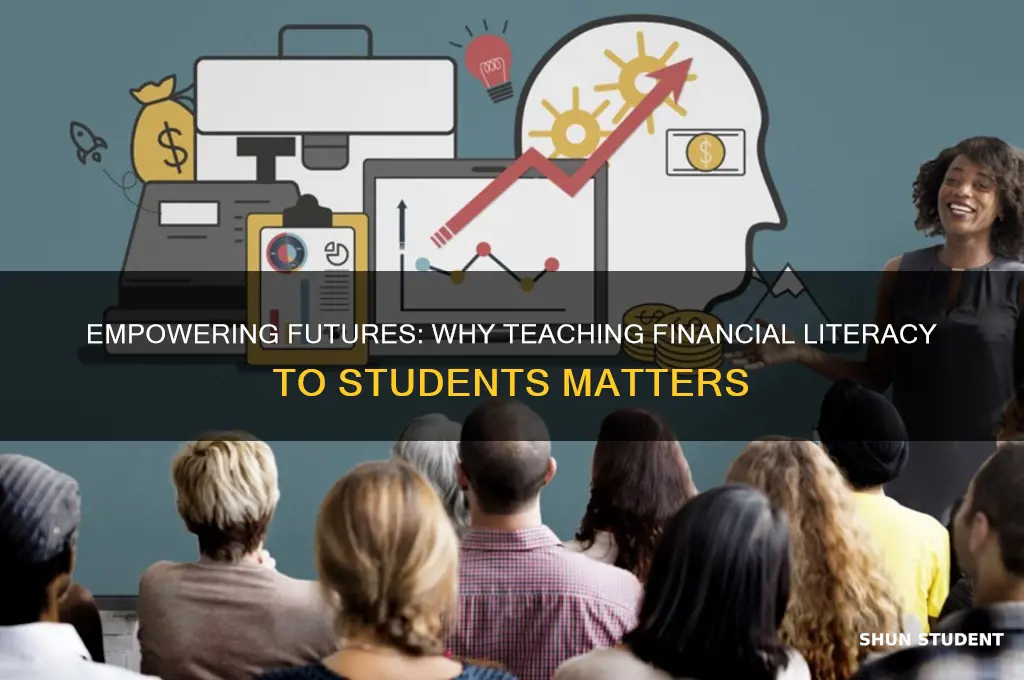

Teaching financial literacy to students is essential because it equips them with the knowledge and skills needed to make informed decisions about money, which can have a lifelong impact on their financial well-being. By integrating financial education into school curricula, students learn critical concepts such as budgeting, saving, investing, and managing debt, fostering a foundation for financial independence and stability. Early exposure to these principles helps young people avoid common pitfalls like overspending or accumulating debt, while also encouraging habits like saving for emergencies and planning for long-term goals like retirement. Moreover, financial literacy empowers students to navigate an increasingly complex economic landscape, reducing financial stress and increasing their ability to achieve personal and professional success. Ultimately, investing in financial education for students not only benefits individuals but also contributes to a more financially resilient society.

| Characteristics | Values |

|---|---|

| Improved Financial Decision-Making | 70% of students who receive financial education report making better financial decisions (Source: National Endowment for Financial Education, 2023) |

| Increased Savings and Investment | Financially literate students are 2x more likely to save and invest for the future (Source: Council for Economic Education, 2022) |

| Reduced Debt and Financial Stress | Students with financial education have 30% less credit card debt and report lower financial stress levels (Source: Jump$tart Coalition, 2021) |

| Enhanced Employability and Earnings | Financially literate individuals earn 10-15% more on average and have better job prospects (Source: OECD, 2020) |

| Better Budgeting and Money Management | 80% of students who learn financial literacy report improved budgeting skills (Source: H&R Block Budget Challenge, 2023) |

| Increased Financial Confidence | Financially educated students are 40% more confident in their ability to manage money (Source: FINRA Investor Education Foundation, 2022) |

| Reduced Risk of Financial Fraud | Students with financial education are 50% less likely to fall victim to financial scams (Source: Federal Trade Commission, 2021) |

| Improved Long-Term Financial Planning | Financially literate individuals are 2.5x more likely to plan for retirement and have adequate savings (Source: Employee Benefit Research Institute, 2020) |

| Positive Impact on Overall Well-being | Financial literacy is linked to improved mental and physical health, with a 20% reduction in stress-related illnesses (Source: Journal of Financial Therapy, 2021) |

| Intergenerational Benefits | Financially educated students are more likely to pass on good financial habits to their children, breaking the cycle of poverty (Source: Brookings Institution, 2022) |

Explore related products

What You'll Learn

- Early Financial Habits: Teaches saving, budgeting, and investing habits from a young age

- Debt Prevention: Helps students avoid pitfalls like credit card debt and loans

- Economic Empowerment: Equips students to make informed financial decisions independently

- Long-Term Wealth: Builds foundation for retirement planning and financial security

- Reduced Stress: Financial knowledge lowers anxiety related to money management

![]()

Early Financial Habits: Teaches saving, budgeting, and investing habits from a young age

Children as young as three can grasp basic financial concepts, according to research from the University of Cambridge. By age seven, many habits—financial or otherwise—begin to solidify. This critical window presents an opportunity to instill saving, budgeting, and investing habits that can shape a lifetime of financial well-being. Start by introducing the concept of delayed gratification through simple activities like saving a portion of their allowance for a desired toy. For instance, a five-year-old can use a clear jar to visually track progress, fostering both patience and goal-setting skills.

Teaching budgeting to young students doesn’t require complex spreadsheets. Instead, use tangible tools like envelopes or piggy banks labeled “Save,” “Spend,” and “Share.” Allocate a child’s weekly allowance (e.g., $5) into these categories: $2 for spending, $2 for saving, and $1 for donating. This hands-on approach not only demystifies budgeting but also encourages empathy and generosity. For older kids (ages 8–12), introduce apps like Greenlight or GoHenry, which allow them to manage digital money while parents monitor and guide their decisions.

Investing may seem advanced, but simplified lessons can begin as early as age 10. Start with the concept of “making money work for you” by explaining how compound interest grows savings over time. Use real-world examples: if a 10-year-old invests $100 at a 5% annual return, it could grow to over $430 by age 30. Introduce low-risk options like index funds or custodial accounts (e.g., UGMA/UTMA) to make investing tangible. Even small, consistent contributions—like $10 monthly—can teach the value of long-term thinking.

Early financial education isn’t just about knowledge; it’s about behavior. A study by the University of Wisconsin found that children who received financial education were 20% more likely to save regularly as adults. However, avoid overwhelming young learners with jargon or complex scenarios. Instead, embed lessons in everyday activities: compare prices at the grocery store, discuss family financial decisions, or play games like The Game of Life or Monopoly to simulate real-world choices. Consistency is key—regular, age-appropriate conversations ensure these habits stick.

The ultimate goal is to empower students to make informed decisions independently. By age 15, they should understand basic investing, budgeting for irregular income (like part-time jobs), and the impact of debt. Encourage them to set short- and long-term financial goals, such as saving for a bike or college. Early financial habits not only reduce future stress but also build confidence in navigating an increasingly complex economic landscape. Start small, stay consistent, and watch these habits grow into lifelong financial resilience.

Dancing Through Duty: How Dance Fosters Responsibility in Students

You may want to see also

Explore related products

$19.2 $35

![]()

Debt Prevention: Helps students avoid pitfalls like credit card debt and loans

Credit card debt and student loans can trap young adults in cycles of financial stress, often before they’ve established stable careers. Teaching debt prevention equips students with the foresight to recognize predatory lending practices, such as high-interest credit cards marketed on college campuses. For instance, a study by the Consumer Financial Protection Bureau found that students who received financial literacy training were 30% less likely to default on loans. By understanding the long-term consequences of compounding interest—how a $1,000 credit card balance at 20% APR can balloon to over $1,200 in just one year—students can make informed decisions to avoid these pitfalls.

To effectively teach debt prevention, educators should incorporate real-world scenarios into lessons. For example, simulate a credit card offer with hidden fees and penalties, then guide students through calculating the true cost. Pair this with case studies of peers who’ve fallen into debt traps, emphasizing how small, impulsive purchases can accumulate. For high schoolers, introduce the concept of a "debt-to-income ratio" and explain how exceeding 30% can harm credit scores. For college students, focus on federal vs. private loans, highlighting the lower interest rates and flexible repayment plans of federal options.

A persuasive argument for debt prevention education lies in its long-term societal benefits. When students avoid debt, they’re less likely to delay major life milestones like homeownership or starting a family. Consider this: the average student loan debt in the U.S. is $37,000, with monthly payments averaging $400. By teaching students to prioritize needs over wants—like choosing a used car over a leased luxury vehicle—they can redirect funds toward savings or investments. Schools can reinforce this by partnering with financial institutions to offer workshops on budgeting apps or low-interest student accounts.

Comparatively, countries like Australia and Canada have integrated financial literacy into their curricula, resulting in lower youth debt rates. In Australia, students as young as 12 learn about compound interest and loan amortization, skills that translate into cautious borrowing habits. Contrast this with the U.S., where only 17 states require high school students to take a personal finance course. By adopting a comparative approach, educators can advocate for policy changes while tailoring lessons to address local economic challenges, such as high living costs in urban areas.

Finally, debt prevention education must be actionable and age-appropriate. For middle schoolers, start with basic budgeting and the concept of "paying yourself first" by saving 10% of allowances. High schoolers should practice reading credit reports and understanding credit scores, while college students need guidance on navigating loan agreements and repayment strategies. Encourage students to track expenses for a month using apps like Mint or YNAB, then analyze where unnecessary spending could lead to debt. By making financial literacy practical and engaging, students not only avoid debt but also build a foundation for lifelong financial health.

Pennsylvania Student Teaching Hours: Requirements and Expectations Explained

You may want to see also

Explore related products

![]()

Economic Empowerment: Equips students to make informed financial decisions independently

Financial literacy isn’t just about balancing a checkbook—it’s about equipping students with the tools to navigate a complex economic landscape. By teaching them how to budget, save, and invest, we empower them to make decisions that align with their long-term goals. For instance, a high school student who understands compound interest might start saving $50 a month at age 18, potentially amassing over $100,000 by age 65, even with modest returns. This simple act of early financial education can transform their economic trajectory.

Consider the contrast between two young adults: one who received financial education and another who didn’t. The former is likely to avoid predatory loans, negotiate better salaries, and invest wisely, while the latter may struggle with debt and financial insecurity. Studies show that students who participate in financial literacy programs are 20% more likely to save regularly and 15% less likely to max out credit cards. These statistics underscore the tangible benefits of equipping students with financial knowledge early on.

To implement this effectively, schools should integrate financial literacy into existing curricula, starting as early as middle school. For example, math classes can incorporate budgeting exercises, and social studies lessons can explore the history of economic systems. Practical tips include using real-life scenarios, such as calculating the true cost of a car loan or comparing rental vs. buying decisions. Teachers can also encourage students to track their own spending for a month, fostering self-awareness and accountability.

However, teaching financial literacy isn’t without challenges. Educators must avoid one-size-fits-all approaches, as students come from diverse socioeconomic backgrounds. Tailoring lessons to address specific needs—like explaining how to build credit for those with limited access to banking—ensures inclusivity. Additionally, schools should partner with financial institutions or nonprofits to provide hands-on experiences, such as mock stock market competitions or savings account simulations.

Ultimately, economic empowerment through financial literacy is about more than just money—it’s about freedom. When students understand how to manage their finances, they gain the confidence to pursue their aspirations without being constrained by debt or ignorance. By investing in their financial education today, we prepare them to build a secure and prosperous future tomorrow.

The Power of Teachers: Shaping Minds, Inspiring Futures, and Transforming Lives

You may want to see also

Explore related products

![]()

Long-Term Wealth: Builds foundation for retirement planning and financial security

Financial literacy education in schools isn't just about balancing checkbooks or understanding credit scores. It's about planting the seeds of long-term financial security, a concept often overlooked until it's too late. By introducing students to the power of compound interest, the importance of consistent saving, and the realities of inflation, we empower them to build a future where retirement isn't a looming financial crisis but a planned, comfortable phase of life.

Imagine a 25-year-old who, thanks to early financial education, starts contributing $200 monthly to a retirement account with a 7% annual return. By age 65, they'd have amassed over $500,000, even without increasing contributions. This simple act, made possible by understanding the time value of money, highlights the transformative power of early financial literacy.

This isn't just theoretical. Studies show that individuals who receive financial education are more likely to save for retirement, invest wisely, and avoid high-interest debt. They're less likely to rely solely on Social Security, a system facing increasing strain. Teaching students about employer-matched 401(k) plans, Roth IRAs, and the benefits of diversifying investments equips them to navigate the complex world of retirement planning with confidence.

Think of it as building a house. You wouldn't start with the roof; you'd lay a solid foundation first. Financial literacy is that foundation. It's about understanding the building blocks of wealth accumulation: budgeting, saving, investing, and managing risk. Without this foundation, even the most ambitious retirement goals are built on shaky ground.

However, simply providing information isn't enough. We need to make financial literacy engaging and relevant. Incorporate real-life scenarios, simulations, and guest speakers from the financial industry. Encourage students to track their own spending, create mock investment portfolios, and participate in financial literacy competitions. By making it interactive and practical, we ensure the lessons stick.

The benefits extend far beyond individual students. A financially literate population contributes to a more stable economy, reduces reliance on government assistance programs, and fosters a culture of responsible financial decision-making. By investing in financial literacy education today, we're not just preparing students for their future; we're building a more secure future for us all.

Mastering Conversation Skills: Effective Teaching Strategies for Engaging Student Dialogue

You may want to see also

Explore related products

![]()

Reduced Stress: Financial knowledge lowers anxiety related to money management

Financial stress is a silent epidemic, particularly among young adults. Studies show that 73% of Gen Z and Millennials report feeling anxious about their financial situation, with student debt, budgeting, and saving for the future topping the list of worries. This anxiety isn’t just emotional—it spills over into physical health, relationships, and academic performance. Teaching financial literacy directly addresses this issue by equipping students with the tools to manage money confidently, transforming fear into control.

Consider the practical impact of financial knowledge on stress reduction. A student who understands how to create a budget, for example, is less likely to overspend or accumulate debt. This simple skill shifts their mindset from scarcity to strategy. Similarly, knowing how to prioritize expenses—like allocating 50% of income to needs, 30% to wants, and 20% to savings (the 50/30/20 rule)—provides a clear framework that reduces decision-making anxiety. When students see their financial choices as deliberate steps rather than chaotic reactions, stress levels naturally decline.

The benefits extend beyond immediate relief. Financial literacy fosters long-term security, which is a powerful stress buffer. For instance, a 20-year-old who starts investing $100 monthly in a retirement account could accumulate over $200,000 by age 65, assuming a 7% annual return. This knowledge eliminates the panic of “starting too late” and replaces it with a sense of proactive planning. Even small actions, like setting up automatic transfers to a savings account, create a safety net that mitigates financial worry.

Critics might argue that financial education alone can’t solve systemic issues like income inequality or student loan crises. While true, it’s equally undeniable that knowledge empowers individuals to navigate these challenges more effectively. For example, understanding loan terms and interest rates can help students make informed decisions about borrowing, reducing the likelihood of overwhelming debt. Financial literacy doesn’t eliminate external pressures, but it equips students to respond to them with resilience rather than despair.

Incorporating financial literacy into school curricula isn’t just an academic exercise—it’s a mental health intervention. By teaching students how to track expenses, save systematically, and plan for the future, we give them the confidence to face financial challenges head-on. The result? A generation less burdened by money-related stress and more prepared to build stable, fulfilling lives. Start early, stay consistent, and watch as financial knowledge becomes a cornerstone of emotional well-being.

Zoom Classroom Hack: How to Mute Your Teacher as a Student

You may want to see also

Frequently asked questions

Teaching financial literacy equips students with essential skills to manage money, make informed decisions, and build a secure financial future, reducing the risk of debt and financial stress later in life.

Financial literacy education helps students develop habits like budgeting, saving, and investing, which can lead to financial stability, wealth accumulation, and better overall economic well-being as adults.

Teaching financial literacy enhances students' critical thinking and decision-making abilities, enabling them to evaluate risks, avoid scams, and choose financial products that align with their goals and needs.

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61SXdyvdqKL._AC_UL320_.jpg)