If you're considering Public Service Loan Forgiveness (PSLF) as a strategy to manage your student loan debt, one common question is whether it can lower your monthly payments. While PSLF itself doesn't directly reduce your monthly payments, enrolling in an income-driven repayment (IDR) plan, which is often a requirement for PSLF eligibility, can significantly lower your monthly payments. IDR plans cap your payments at a percentage of your discretionary income, making them more manageable, especially for those in public service careers with lower salaries. Over time, PSLF offers the added benefit of forgiving the remaining balance of your loans after 120 qualifying payments, providing long-term financial relief rather than immediate payment reduction.

Explore related products

What You'll Learn

![]()

Income-Driven Repayment Plans

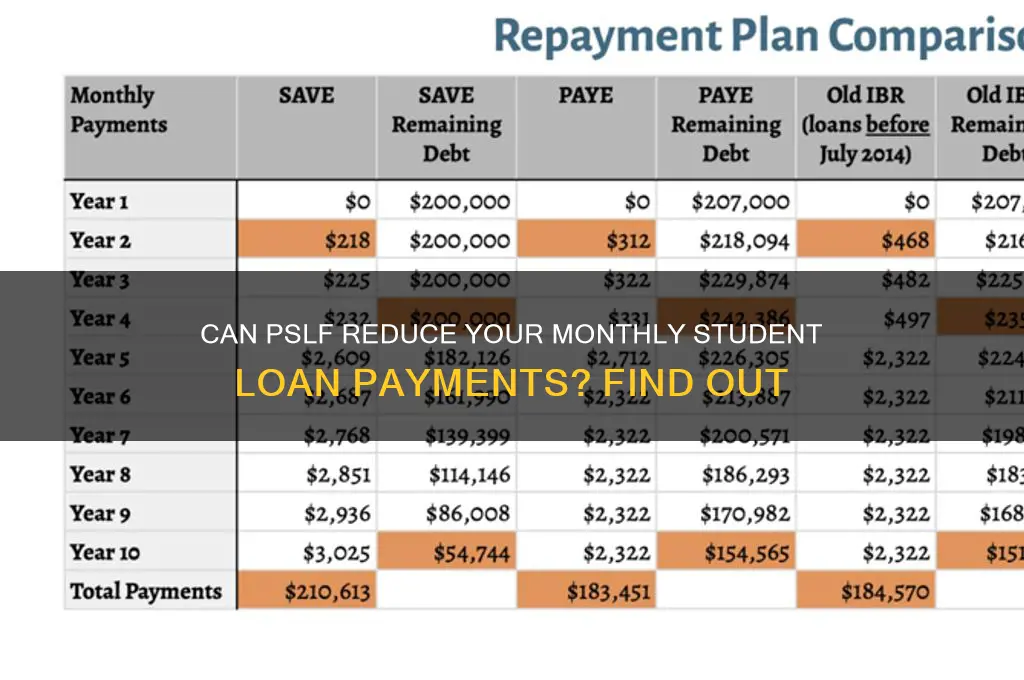

Income-driven repayment (IDR) plans are a lifeline for borrowers juggling federal student loans, particularly those with modest incomes or high debt loads. These plans recalibrate monthly payments based on your discretionary income and family size, often reducing them to as little as $0 if your earnings are low enough. For instance, under the Revised Pay As You Earn (REPAYE) plan, payments are capped at 10% of discretionary income, calculated as the difference between your adjusted gross income and 150% of the federal poverty guideline for your family size. This structure ensures payments remain manageable relative to your financial situation, a stark contrast to standard 10-year repayment plans that prioritize speed over affordability.

Consider the case of a borrower earning $40,000 annually with $60,000 in student loans. Under a standard plan, their monthly payment would be approximately $611. However, on an IDR plan like REPAYE, their payment could drop to around $200—or even $0 if their income falls below the poverty guideline. This reduction not only eases immediate financial strain but also aligns payments with long-term earning potential, especially for those in public service or lower-paying fields. However, it’s critical to note that lower payments often extend the repayment term, meaning more interest accrues over time.

One of the most compelling aspects of IDR plans is their synergy with Public Service Loan Forgiveness (PSLF). Borrowers pursuing PSLF must make 120 qualifying payments while working full-time for an eligible employer. IDR plans are the most efficient way to meet this requirement, as they minimize payments while still counting toward forgiveness. For example, a teacher earning $50,000 with $80,000 in loans could see monthly payments drop from $888 on a standard plan to $250 on an IDR plan like Pay As You Earn (PAYE). After 10 years of these lower payments, the remaining balance is forgiven tax-free under PSLF, a benefit that standard plans cannot offer.

However, IDR plans aren’t without pitfalls. Annual recertification is mandatory, requiring borrowers to submit updated income and family size information. Miss this deadline, and you risk being switched to a standard plan with significantly higher payments. Additionally, forgiven balances under IDR plans (outside of PSLF) may be taxed as income, though this provision is currently suspended through 2025. To maximize benefits, borrowers should track payments meticulously, choose the IDR plan best suited to their financial goals, and consider consulting a student loan advisor to navigate complexities.

In summary, income-driven repayment plans are a strategic tool for lowering monthly student loan payments, especially when paired with PSLF. They offer flexibility and long-term relief but demand vigilance in recertification and awareness of potential tax implications. For borrowers seeking to balance affordability with forgiveness, IDR plans are not just an option—they’re often the optimal path forward.

Marriage and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

PSLF Eligibility Requirements

To qualify for Public Service Loan Forgiveness (PSLF), borrowers must meet specific eligibility criteria that go beyond simply working in public service. First, only federal Direct Loans qualify for PSLF, meaning loans like Federal Family Education Loans (FFEL) or Perkins Loans must be consolidated into a Direct Consolidation Loan to be eligible. This consolidation step is critical, as payments made before consolidation do not count toward the required 120 qualifying payments. Borrowers should act promptly to consolidate if their loans are not already in the Direct Loan program.

Second, employment requirements are stringent. Borrowers must work full-time for a qualifying employer, defined as a government organization at any level (federal, state, local), a 501(c)(3) nonprofit, or another type of nonprofit that provides specific public services. Part-time workers can also qualify if they meet their employer’s definition of full-time or work at least 30 hours per week. It’s essential to verify employer eligibility using the PSLF Help Tool, as some nonprofits may not meet the criteria despite their public service focus.

Third, payment requirements are precise. Borrowers must make 120 qualifying payments under an income-driven repayment (IDR) plan, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE). Payments made under the standard 10-year repayment plan do not count unless the payment amount is at least as much as it would be under an IDR plan. Each payment must be made on time, defined as within 15 days of the due date, and for the full amount due. Partial or late payments do not qualify, making it crucial to stay organized and monitor payment history.

Finally, certification and documentation are key to success. Borrowers should submit the Employment Certification Form (ECF) annually or when changing employers to ensure their payments are tracking correctly. This form confirms both employer eligibility and payment qualification. Waiting until the 120 payments are complete to certify employment can lead to unpleasant surprises, such as discovering that an employer or payments did not qualify. Regular certification provides peace of mind and allows borrowers to address issues proactively.

In summary, PSLF eligibility hinges on specific loan types, employment, payment plans, and documentation. By consolidating loans into the Direct Loan program, working for a qualifying employer, enrolling in an IDR plan, and certifying employment regularly, borrowers can maximize their chances of having their loans forgiven after 120 qualifying payments. This structured approach not only ensures compliance with PSLF requirements but also helps lower monthly payments through income-driven plans, making the path to forgiveness more manageable.

Does Trump's Student Loan Forgiveness Include Spouses? Key Details Explained

You may want to see also

![]()

Payment Calculation Methods

Understanding how your monthly student loan payment is calculated under the Public Service Loan Forgiveness (PSLF) program is crucial for financial planning. The primary method used is the Income-Driven Repayment (IDR) plan, which ties your payment to your discretionary income rather than the total loan balance. For instance, the Revised Pay As You Earn (REPAYE) plan caps payments at 10% of your discretionary income, defined as the difference between your adjusted gross income (AGI) and 150% of the federal poverty guideline for your family size. For a single borrower earning $50,000 annually in 2023, the poverty guideline is $14,580, making discretionary income $35,420. Thus, the monthly payment would be approximately $295, significantly lower than standard repayment plans.

Another critical factor in payment calculation is the federal poverty guideline, which varies by family size and state of residence. For example, a family of four in the contiguous U.S. has a 2023 poverty guideline of $30,000, while Alaska’s is $37,500. Borrowers with larger families or lower incomes benefit more from IDR plans because their discretionary income is lower, reducing monthly payments. However, it’s essential to recertify your income and family size annually to ensure accurate calculations. Failure to do so can result in a switch to a standard repayment plan, potentially tripling your monthly payment.

A lesser-known aspect of PSLF payment calculations is the treatment of spousal income. If you file taxes jointly, your spouse’s income is included in the AGI calculation, which can increase your monthly payment. For example, if you earn $40,000 and your spouse earns $60,000, your combined AGI is $100,000. Using the REPAYE plan, discretionary income would be calculated based on this total, potentially raising your payment. To mitigate this, some borrowers file taxes separately, excluding spousal income from the calculation. However, this strategy may disqualify you from certain IDR plans, so consult a tax professional to weigh the pros and cons.

Finally, understanding payment caps is vital for long-term planning. While IDR plans reduce monthly payments, they may not cover accruing interest, leading to balance growth. For instance, if your monthly payment is $200 but interest accrues at $250, your balance increases by $50 monthly. However, under PSLF, any remaining balance after 120 qualifying payments is forgiven, tax-free. This makes IDR plans under PSLF particularly advantageous, as lower payments minimize out-of-pocket costs while maximizing forgiveness potential. To optimize this, prioritize IDR plans like REPAYE or Pay As You Earn (PAYE), which offer the lowest payment caps and most generous forgiveness terms.

Understanding 10-Year Student Loan Forgiveness: A Comprehensive Guide

You may want to see also

![]()

Loan Consolidation Impact

Loan consolidation can significantly alter your monthly student loan payments, but its impact on those pursuing Public Service Loan Forgiveness (PSLF) is nuanced. By combining multiple federal loans into a single Direct Consolidation Loan, borrowers simplify their repayment structure. This move is particularly beneficial for PSLF candidates, as only Direct Loans are eligible for the program. Consolidation ensures all loans fall under the qualifying umbrella, preventing ineligible loans from derailing progress. However, it resets the forgiveness clock, meaning previous qualifying payments no longer count toward the 120 required for PSLF. Borrowers must weigh the trade-off between streamlined management and starting anew.

For those on income-driven repayment (IDR) plans, consolidation can lower monthly payments by recalculating the payment amount based on the new loan balance and family size. This is especially advantageous for PSLF seekers, as IDR plans often result in lower payments, and the forgiven amount after 120 payments is tax-free. For example, a borrower earning $40,000 annually with $100,000 in debt might see payments drop from $800 to $200 per month under an IDR plan post-consolidation. However, this reduction depends on income, family size, and the specific IDR plan chosen. Consolidation also eliminates the need to track multiple payment due dates, reducing the risk of missed payments that could disrupt PSLF eligibility.

A critical caution: consolidating loans in default requires borrowers to rehabilitate them first, which involves making nine on-time payments within ten months. Failure to do so can disqualify the consolidated loan from PSLF. Additionally, consolidating during periods of economic hardship or career transitions can provide immediate financial relief but requires careful planning. For instance, a teacher with $80,000 in FFEL loans could consolidate into a Direct Loan, enroll in an IDR plan, and reduce monthly payments from $700 to $150, making PSLF more attainable. Yet, this strategy demands long-term commitment to public service work.

In practice, consolidation’s impact on PSLF hinges on individual circumstances. A borrower with multiple loan servicers might consolidate to avoid administrative confusion, ensuring consistent PSLF tracking. Conversely, someone nearing the 120-payment milestone should avoid consolidation, as it resets progress. Tools like the PSLF Help Tool can clarify eligibility post-consolidation. Ultimately, consolidation is a strategic move—one that lowers monthly payments for many but demands careful consideration of timing and long-term goals. For PSLF seekers, it’s a double-edged sword: simplifying repayment while restarting the forgiveness journey.

Navigating Student Loan Forgiveness: Who Can Guide You to Relief?

You may want to see also

![]()

Forgiveness vs. Lower Payments

Public Service Loan Forgiveness (PSLF) is often touted as a golden ticket for student loan borrowers, but its impact on monthly payments is less straightforward. Unlike income-driven repayment (IDR) plans, which directly lower monthly payments by tying them to income, PSLF does not inherently reduce what you pay each month. Instead, it promises forgiveness of the remaining balance after 120 qualifying payments. This distinction is crucial: PSLF is about long-term relief, not immediate financial ease. Borrowers must weigh the trade-off between lower payments now (via IDR) and the potential for forgiveness later (via PSLF).

To illustrate, consider a borrower with $100,000 in loans earning $50,000 annually. Under the Revised Pay As You Earn (REPAYE) plan, their monthly payment might be around $150. If they pursue PSLF, they’ll continue making these payments for 10 years, totaling $18,000, and then have the remaining balance forgiven. In contrast, staying on REPAYE without PSLF could result in higher total payments over 20–25 years, but with no forgiveness. The key takeaway: PSLF doesn’t lower monthly payments; it shifts the focus to a future payoff.

A common misconception is that PSLF and lower payments are mutually exclusive. In reality, they can work together. Borrowers must enroll in an IDR plan to qualify for PSLF, which means their monthly payments are already reduced based on income. For example, a teacher earning $40,000 might pay $100 monthly under Pay As You Earn (PAYE) while working toward PSLF. The lower payment eases immediate financial strain, while the forgiveness goal provides long-term motivation. This synergy is why PSLF is often recommended for low- to mid-income borrowers in public service.

However, pursuing PSLF isn’t without risks. Missing payments or failing to meet eligibility criteria can derail the entire process. For instance, payments made under the wrong plan (e.g., Standard Repayment) don’t count toward PSLF. Additionally, switching jobs or taking a leave of absence could disrupt qualifying employment. Borrowers must meticulously track payments and submit employment certification forms annually. Those seeking lower payments without the commitment to public service might find IDR plans alone more suitable, albeit without the forgiveness incentive.

Ultimately, the choice between prioritizing forgiveness or lower payments depends on individual circumstances. For borrowers with high debt-to-income ratios, PSLF’s forgiveness can be life-changing, even if monthly payments remain modest. Conversely, those with moderate debt or uncertain public service careers may prefer the flexibility of IDR plans. Practical steps include calculating projected payments under IDR, estimating potential forgiveness, and consulting a loan specialist. By aligning repayment strategy with career goals, borrowers can navigate the PSLF landscape effectively, balancing immediate relief with future financial freedom.

Biden's Student Loan Forgiveness Plan: How It Works and Who Qualifies

You may want to see also

Frequently asked questions

No, enrolling in PSLF does not automatically lower your monthly payment. However, to qualify for PSLF, you must make payments under an income-driven repayment (IDR) plan, which can significantly reduce your monthly payment based on your income and family size.

Yes, switching to an IDR plan is highly recommended if you’re pursuing PSLF. IDR plans cap your monthly payment at a percentage of your discretionary income, often resulting in lower payments compared to standard repayment plans.

Yes, PSLF offers loan forgiveness after 120 qualifying payments, regardless of your monthly payment amount. Even if your payments are low under an IDR plan, PSLF can still eliminate your remaining balance after meeting the program’s requirements.