Navigating the complexities of student loan repayment can be overwhelming, and many borrowers wonder if a tax offset could defer their student loans. A tax offset occurs when the government withholds a portion of your tax refund to repay outstanding federal student loans in default. While this process doesn’t directly defer your loans, understanding how it works is crucial. Deferment, on the other hand, temporarily pauses your loan payments under specific conditions, such as returning to school or experiencing economic hardship. If your loans are in default, a tax offset may accelerate repayment, but it doesn’t provide the same relief as deferment. Exploring options like loan rehabilitation or consolidation might be more effective in managing your debt and avoiding tax offsets altogether.

| Characteristics | Values |

|---|---|

| Tax Offset Impact on Student Loans | A tax offset (treasury offset) can intercept federal tax refunds to repay defaulted student loans. |

| Deferment Eligibility | Tax offsets do not directly defer student loans; deferment requires separate application through loan servicer. |

| Loan Status | Applies only to defaulted federal student loans (Direct, FFEL, Perkins). |

| Notification | Borrowers receive a notice from the U.S. Department of Education before offset occurs. |

| Prevention Options | Rehabilitation, consolidation, or repayment agreement can stop tax offsets. |

| Refund Impact | Entire or partial tax refund may be withheld to pay toward defaulted loan balance. |

| State Tax Refunds | Some states may also offset state tax refunds for defaulted student loans. |

| Timeline | Offsets typically occur during tax season (January–April) after default status is confirmed. |

| Appeal Process | Borrowers can dispute offsets if they believe an error occurred (e.g., incorrect loan status). |

| Current Data (2023) | Over 1 million borrowers annually face tax offsets due to defaulted student loans. |

Explore related products

What You'll Learn

![]()

Eligibility for Tax Offsets

Tax offsets, often misunderstood as a direct means to defer student loans, actually operate within a distinct financial framework. Eligibility for these offsets hinges on specific criteria set by tax authorities, not student loan providers. To qualify, individuals must meet income thresholds, claim eligible deductions, and sometimes satisfy residency or citizenship requirements. For instance, in Australia, the Low and Middle Income Tax Offset (LMITO) applies to taxpayers earning up to $126,000 annually, while in the U.S., the American Opportunity Tax Credit (AOTC) requires enrollment in an eligible educational institution and a modified adjusted gross income (MAGI) below $90,000 for single filers. Understanding these parameters is crucial, as tax offsets reduce taxable income or directly lower tax liability, but they do not directly interact with student loan repayment schedules.

A critical aspect of eligibility is the timing and documentation required. Tax offsets are typically claimed during the annual tax filing process, meaning borrowers must wait until the end of the tax year to benefit. For those in financial hardship, this delay underscores the importance of proactive planning. Keeping detailed records of income, expenses, and loan payments is essential. For example, the U.S. student loan interest deduction allows up to $2,500 in interest payments to be deducted, but only if the borrower’s MAGI falls below $85,000 (single filers). Similarly, in Canada, the Tuition Tax Credit requires proof of tuition fees paid, which must be claimed within the year they were incurred or carried forward to future years. Missteps in documentation can result in ineligibility, making precision a non-negotiable requirement.

Finally, while tax offsets do not directly defer student loans, strategic use of these benefits can alleviate financial strain. Borrowers should assess their eligibility annually, as criteria may change due to shifts in income, marital status, or tax laws. For instance, the expiration of temporary programs like the LMITO in Australia or the pause on student loan payments in the U.S. during the COVID-19 pandemic highlights the need for adaptability. Pairing tax offsets with other financial strategies, such as loan consolidation or refinancing, can create a more sustainable repayment plan. Ultimately, eligibility for tax offsets is a tool in the financial toolkit—one that requires careful navigation but can yield significant relief when leveraged correctly.

Can Great Lakes Student Loans Be Forgiven? Eligibility Explained

You may want to see also

Explore related products

![]()

Impact on Loan Repayments

A tax offset can significantly alter the trajectory of your student loan repayments, but understanding its mechanics is crucial. When the IRS applies a tax offset, they intercept your tax refund to cover defaulted student loan debt. This means instead of receiving a refund, that money goes directly toward your loan balance. For borrowers in default, this can be both a relief—reducing the principal—and a setback, as it depletes expected funds. The impact is immediate: your loan balance decreases, but your cash flow takes a hit, potentially disrupting short-term financial plans.

Consider the scenario of a borrower with a $10,000 tax refund and $30,000 in defaulted student loans. If the IRS offsets the entire refund, the loan balance drops to $20,000, but the borrower loses access to $10,000 they may have relied on for emergencies or other expenses. This highlights a critical trade-off: while the offset reduces debt, it does so at the cost of liquidity. Borrowers must weigh the long-term benefit of a lower loan balance against the immediate financial strain.

To mitigate the impact, proactive steps are essential. First, contact your loan servicer to explore rehabilitation programs, which can remove your loan from default status and prevent future offsets. Second, adjust your tax withholdings to reduce the size of your refund, minimizing the amount available for offset. For example, if you typically receive a $5,000 refund, reducing withholdings could lower it to $1,000, limiting the offset’s reach. Third, create a budget that accounts for the potential loss of your refund, ensuring you have alternative funds for emergencies.

Comparatively, borrowers in non-default status face a different dynamic. Tax offsets only apply to defaulted loans, so those in repayment plans or forbearance are not at risk. However, understanding this distinction is vital, as it underscores the importance of maintaining good standing with your loans. For instance, enrolling in an income-driven repayment plan can lower monthly payments and prevent default, thereby safeguarding your tax refund.

In conclusion, a tax offset’s impact on loan repayments is twofold: it reduces your debt but strains your finances. By understanding this mechanism and taking proactive measures—such as loan rehabilitation, adjusting withholdings, and budgeting—borrowers can navigate this challenge more effectively. The key is to balance the long-term goal of debt reduction with the immediate need for financial stability.

Understanding the Student Loan Forgiveness Debate: Key Issues and Names

You may want to see also

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71OcM906MLL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![TurboTax Premier Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71ofxs16-9L._AC_UL320_.jpg)

![TurboTax Home & Business Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71-jbdrZxVL._AC_UL320_.jpg)

![]()

Tax Offset vs. Loan Deferment

Tax offsets and loan deferments serve distinct purposes in managing student loan debt, yet borrowers often conflate the two. A tax offset occurs when the government withholds your tax refund to repay defaulted student loans, a punitive measure for delinquency. In contrast, loan deferment is a temporary pause on payments granted under specific conditions, such as economic hardship or enrollment in school. Understanding these differences is crucial, as one is a consequence of default, while the other is a proactive tool for financial relief.

Consider this scenario: You’ve recently lost your job and are struggling to make student loan payments. Applying for a deferment could halt payments for up to three years, depending on the type of loan and eligibility criteria. For federal loans, deferment may even suspend interest accrual on subsidized loans, preventing your balance from growing. However, if you ignore payments and default, the government may intercept your tax refund through a tax offset, leaving you with no refund and a still-growing debt. The choice between proactive deferment and reactive offset hinges on timely action and understanding your options.

From a strategic standpoint, deferment is a preventive measure, while a tax offset is a corrective one. Deferment requires documentation and approval, such as proof of unemployment or enrollment in school, and it’s not automatic. Tax offsets, however, are triggered by default, typically after nine months of missed payments on federal loans. Borrowers under 25 or over 50 may face unique challenges; younger individuals might qualify for deferment due to continued education, while older borrowers may struggle with limited deferment options and higher stakes in default.

Practical tips for navigating these options include monitoring your loan status regularly to avoid default and applying for deferment before payments become unmanageable. For instance, if you’re returning to school, submit your deferment request promptly to ensure coverage from the first day of classes. If you’re at risk of default, contact your loan servicer to explore repayment plans or forbearance as alternatives. Remember, a tax offset can’t be reversed once initiated, so addressing delinquency early is key.

In conclusion, while both tax offsets and loan deferments impact student loan management, they operate on opposite ends of the financial spectrum. Deferment offers a structured pause, preserving financial stability, whereas a tax offset is a forced repayment method with long-term consequences. By recognizing these distinctions and acting proactively, borrowers can safeguard their finances and avoid the pitfalls of default.

Student Loan Forgiveness: Economic Savior or Financial Disaster?

You may want to see also

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71pX8Fh2sNL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![]()

IRS Policies on Student Loans

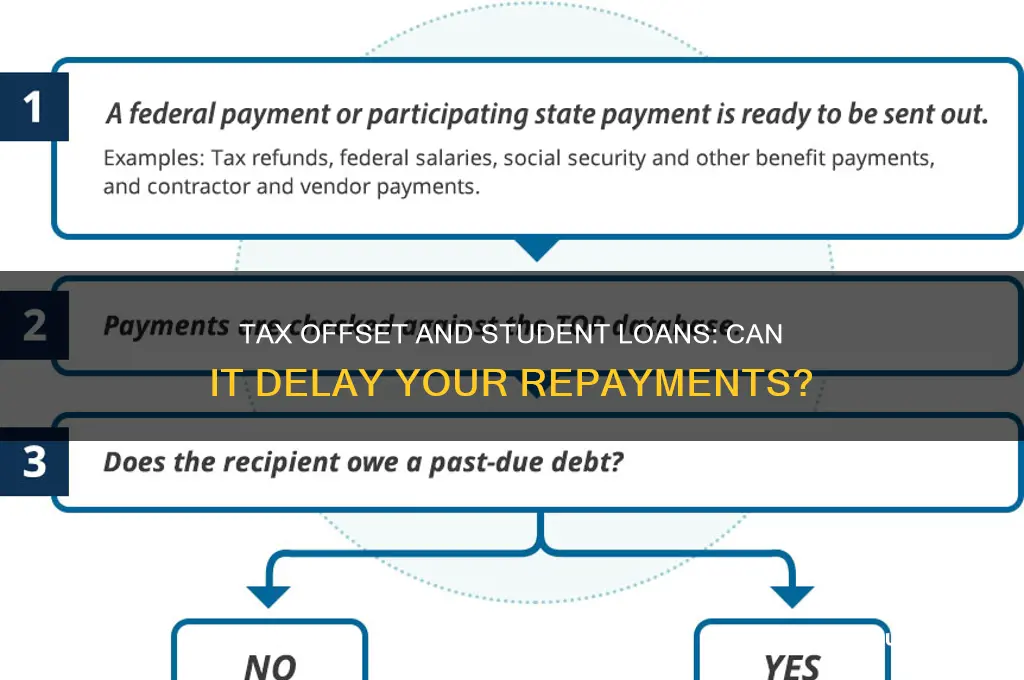

The IRS wields significant power over your student loans through its tax offset program. If you default on federal student loans, the government can intercept your tax refund to repay the debt. This process, known as a tax offset, bypasses the need for court orders or wage garnishment, making it a potent tool for loan recovery. Understanding the IRS's policies is crucial for borrowers navigating financial hardship, as it directly impacts their ability to retain tax refunds and manage loan repayment.

Key to the IRS's approach is the Treasury Offset Program (TOP), which coordinates with various federal agencies to collect delinquent debts. When a borrower defaults on a student loan, the Department of Education notifies the TOP, which then flags the borrower's tax account. Upon filing taxes, any refund due to the borrower is redirected to pay down the outstanding loan balance. This automated process prioritizes government debt repayment over individual financial needs, often catching borrowers off guard.

While tax offsets are a harsh consequence of default, the IRS does provide avenues for relief. Borrowers can request a review of their case if they believe the offset was made in error or if they face severe financial hardship. The IRS may consider factors such as income, expenses, and family size to determine if partial or full relief is warranted. Additionally, borrowers can avoid offsets by consolidating defaulted loans, entering into a rehabilitation agreement, or making satisfactory repayment arrangements with their loan servicer.

A critical aspect of IRS policy is the distinction between federal and private student loans. Tax offsets apply exclusively to federal loans, as private lenders lack the authority to intercept tax refunds. Borrowers with private loans must navigate separate collection processes, which may include lawsuits, wage garnishment, or asset seizure. This distinction underscores the importance of understanding the type of loans you hold and the specific policies governing their repayment.

For borrowers seeking to prevent or resolve tax offsets, proactive communication with loan servicers and the IRS is essential. Ignoring notices or delaying action can exacerbate the situation, leading to additional fees and penalties. By staying informed and exploring available options, borrowers can mitigate the impact of IRS policies on their financial stability and work toward resolving their student loan debt.

Massachusetts Tax Implications for Student Loan Forgiveness: What to Know

You may want to see also

Explore related products

![TurboTax Business Desktop Edition 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71iKclcd6ML._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UL320_.jpg)

![]()

Long-Term Financial Implications

A tax offset can temporarily reduce your tax refund or increase your tax liability, but its long-term financial implications on student loans are often misunderstood. While a tax offset may defer student loan payments by intercepting your refund, it does not eliminate the debt. Instead, the offset amount is applied directly to your outstanding loan balance, which can provide temporary relief but also triggers a cascade of financial consequences. For instance, if your $2,500 tax refund is offset, that amount reduces your principal balance, but it doesn’t address the root issue of repayment strategy or future financial planning.

Analyzing the mechanics reveals a critical trade-off. On one hand, a tax offset can force a lump-sum payment toward your student loans, potentially reducing interest accrual over time. For example, a $3,000 offset on a loan with a 6% interest rate could save approximately $180 in interest annually. However, this benefit is often outweighed by the immediate financial strain of losing a refund, especially if you rely on it for emergencies or debt consolidation. Moreover, repeated offsets may signal deeper financial instability, such as consistent default or delinquency, which can damage your credit score and limit future borrowing power.

Instructively, to mitigate long-term harm, consider proactive steps. First, enroll in an income-driven repayment plan to align payments with your earnings, reducing the risk of default. Second, explore tax credit programs like the American Opportunity Tax Credit, which can provide up to $2,500 in refundable credits to offset education expenses. Third, allocate a portion of your income—even as little as $50 monthly—toward student loans to demonstrate good faith and potentially avoid offsets. These actions not only preserve financial flexibility but also position you for long-term stability.

Comparatively, the impact of a tax offset on student loans differs significantly from other debt management strategies. For example, while bankruptcy can discharge certain debts, student loans are rarely eligible, making offsets a more immediate but less permanent solution. Similarly, debt consolidation may lower monthly payments but extends repayment terms, increasing total interest paid. In contrast, a tax offset provides a one-time reduction in principal but does little to address systemic financial challenges. Understanding these distinctions is crucial for crafting a sustainable financial plan.

Descriptively, the long-term financial landscape for those facing tax offsets often includes heightened stress and reduced opportunities. Imagine a scenario where a young professional loses their $1,800 tax refund to an offset, forcing them to delay saving for a home down payment or investing in retirement. Over a decade, this delay could cost tens of thousands in lost compound interest. Additionally, the psychological toll of financial uncertainty can lead to poor decision-making, such as relying on high-interest credit cards to cover shortfalls. These cumulative effects underscore the importance of viewing tax offsets not as a solution but as a symptom of broader financial challenges.

Who to Write to for Student Loan Forgiveness: A Comprehensive Guide

You may want to see also

Frequently asked questions

No, a tax offset does not automatically defer your student loans. A tax offset occurs when the government withholds your tax refund to pay off delinquent federal student loans. It does not affect the status of your loan payments or deferment.

Yes, you can request a deferment or forbearance on your student loans, but it must be approved by your loan servicer. A tax offset does not automatically qualify you for deferment; you must meet specific eligibility criteria.

Resolving a tax offset does not directly prevent your student loans from going into default. To avoid default, you must make consistent payments or apply for deferment, forbearance, or an income-driven repayment plan.

A tax offset itself does not affect your eligibility for deferment programs. However, being in default (which can lead to a tax offset) may limit your options. You’ll need to rehabilitate your loans or consolidate them to regain eligibility for deferment.

![TurboTax Deluxe Online Edition 2025, Federal Tax Return [Activation Code]](https://m.media-amazon.com/images/I/61bFazlntVL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![The Taxes, Accounting, Bookkeeping Bible: [3 in 1] The Most Complete and Updated Guide for the Small Business Owner with Tips and Loopholes to Save Money and Avoid IRS Penalties](https://m.media-amazon.com/images/I/617DYgupSxL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)