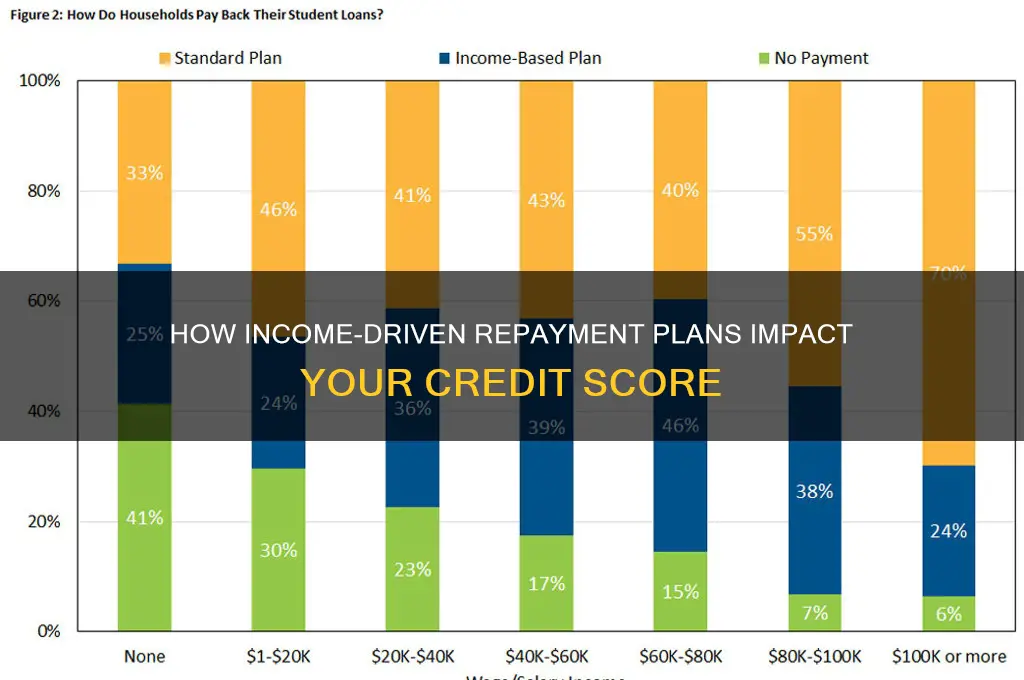

An Income-Driven Repayment (IDR) plan for student loans can impact your credit, but the effects are generally minimal and depend on how the plan is managed. IDR plans adjust monthly payments based on your income and family size, often lowering them to more manageable levels, which can help prevent missed payments and defaults that would harm your credit score. However, enrolling in an IDR plan itself does not directly affect your credit, as it is simply a repayment option. Potential concerns arise if the reduced payments cause your loan balance to grow due to unpaid interest, or if there are reporting errors by the loan servicer. Overall, when used responsibly, an IDR plan can support financial stability and indirectly benefit your credit by ensuring consistent, on-time payments.

| Characteristics | Values |

|---|---|

| Impact on Credit Score | Generally, enrolling in an Income-Driven Repayment (IDR) plan does not directly lower your credit score. However, it depends on how the loan is reported to credit bureaus. |

| Payment History Reporting | On-time payments under IDR are reported positively, which can help build or maintain a good credit score. |

| Loan Status Reporting | Loans in IDR may be reported as "current" if payments are made as agreed, even if the payment is lower than standard plans. |

| Potential Negative Impact | If payments under IDR are lower than accruing interest, the loan balance may increase, but this does not directly affect credit score. |

| Credit Utilization | IDR does not impact credit utilization since student loans are installment loans, not revolving credit like credit cards. |

| Credit Mix | Student loans contribute to credit mix, and IDR does not change this aspect of your credit profile. |

| Debt-to-Income Ratio | Lower payments under IDR may improve your debt-to-income ratio, indirectly benefiting creditworthiness for other loans. |

| Loan Forgiveness Impact | Forgiveness under IDR (e.g., after 20-25 years) does not negatively impact credit score; the loan is reported as paid as agreed. |

| Credit Inquiry Impact | Enrolling in IDR does not involve a hard credit inquiry, so it does not affect your credit score. |

| Late Payments Risk | Missing payments under IDR can lead to delinquency, which negatively impacts credit score, just like any other loan. |

| Credit Reporting Accuracy | Ensure your IDR payments are accurately reported to credit bureaus to avoid any negative impact on your credit score. |

| Long-Term Credit Impact | Consistently making payments under IDR can positively impact your credit history over time. |

Explore related products

$8.99 $14.99

What You'll Learn

- IDR Basics: Understanding income-driven repayment plans and their impact on credit scores

- Payment History: How consistent, lower payments on IDR affect credit reporting

- Credit Utilization: Potential effects of reduced monthly payments on debt-to-income ratios

- Credit Inquiries: Does enrolling in IDR trigger new credit checks

- Long-Term Impact: How IDR may influence credit over time, including loan forgiveness

![]()

IDR Basics: Understanding income-driven repayment plans and their impact on credit scores

Income-driven repayment (IDR) plans can be a lifeline for borrowers struggling to manage federal student loan payments. These plans adjust monthly payments based on income and family size, often reducing them to a more manageable percentage of discretionary income—typically 10% to 20%. While IDR plans offer immediate financial relief, their impact on credit scores is a common concern. The good news is that enrolling in an IDR plan itself does not directly harm your credit score. Payment history, which makes up 35% of your FICO score, remains intact as long as you make payments on time. However, the reduced payment amount under IDR may not cover accruing interest, leading to loan balance growth over time. This increasing balance does not directly affect your credit score, but it could influence lenders’ perceptions of your debt-to-income ratio when applying for new credit.

One critical aspect of IDR plans is their reporting to credit bureaus. As long as you make payments as agreed, your account will be reported as “current,” which is positive for your credit score. However, if you miss payments or fail to recertify your income annually (a requirement for IDR plans), your loans could revert to a standard repayment plan, potentially leading to delinquency or default. These negative marks can significantly damage your credit score. For example, a single missed payment can drop a good credit score by 50 to 100 points. To avoid this, set reminders for recertification deadlines and consider enrolling in automatic payments to ensure timely submissions.

Comparatively, IDR plans differ from traditional repayment plans in how they handle loan forgiveness. After 20 to 25 years of qualifying payments, any remaining balance is forgiven under IDR. While this forgiveness does not directly impact your credit score, the forgiven amount may be considered taxable income, depending on the year of forgiveness and current tax laws. For instance, under the American Rescue Plan Act of 2021, student loan forgiveness through 2025 is tax-free, but this provision may not be extended. Tax implications aside, the prospect of eventual forgiveness can provide long-term financial stability, indirectly supporting credit health by reducing overall debt burden.

Practical tips for managing IDR and credit include monitoring your credit report annually for inaccuracies and ensuring all payments are reflected correctly. If you’re considering IDR, evaluate your long-term financial goals. For borrowers with low incomes and high loan balances, IDR can be a strategic choice to maintain credit health while pursuing loan forgiveness. Conversely, if your income is expected to rise significantly, you might weigh the benefits of IDR against the potential for interest capitalization. For example, a borrower with $50,000 in loans at 6% interest could see their balance grow by $3,000 annually under a low IDR payment, but this trade-off may be worthwhile for those prioritizing immediate cash flow.

In conclusion, IDR plans do not inherently damage your credit score but require careful management to avoid pitfalls. By staying current on payments, recertifying income on time, and understanding the long-term implications of balance growth and loan forgiveness, borrowers can leverage IDR to maintain or even improve their credit health. While IDR is not a one-size-fits-all solution, it offers a structured path to financial stability for those who qualify, making it a valuable tool in the student loan repayment toolkit.

Can Your Private Student Loan Be Forgiven? Eligibility Explained

You may want to see also

Explore related products

![]()

Payment History: How consistent, lower payments on IDR affect credit reporting

Consistent, lower payments on an Income-Driven Repayment (IDR) plan can shape your credit profile in nuanced ways, primarily through their impact on payment history—the most influential factor in credit scoring. Here’s how: when enrolled in an IDR plan, your monthly payments are recalibrated based on income and family size, often resulting in amounts lower than standard plans. Critically, these reduced payments are still reported as “paid as agreed” to credit bureaus, provided they’re made on time. This means your payment history remains unblemished, a cornerstone of a strong credit score. However, the lower payment amounts themselves don’t inherently boost your credit, as credit scores don’t reward payment size—only consistency and timeliness.

Consider this scenario: a borrower on an IDR plan pays $50 monthly instead of the standard $200. If these $50 payments are made on time, the credit report reflects a flawless payment history, identical to that of a borrower paying the full $200. The key takeaway? Lower payments under IDR don’t penalize your credit score, but they also don’t accelerate its improvement beyond maintaining a clean record. For borrowers with limited income, this structure prevents credit damage from missed payments, offering a protective benefit.

Yet, there’s a caveat: while IDR payments are reported as “paid as agreed,” some lenders or scoring models might scrutinize the reduced payment amounts when evaluating creditworthiness. For instance, a mortgage lender might question your debt-to-income ratio if your student loan payments appear disproportionately low relative to the principal balance. This doesn’t directly impact your credit score but could influence lending decisions. To mitigate this, borrowers should proactively communicate their IDR status and provide context during loan applications.

Practical tips for maximizing credit health on IDR include setting up autopay to ensure timely payments and periodically reviewing credit reports for inaccuracies. Additionally, if your income increases, consider voluntarily paying more than the IDR amount to reduce principal faster, though this won’t directly affect your credit score. The ultimate goal is to leverage IDR’s flexibility without compromising long-term financial opportunities. By understanding how consistent, lower payments interact with credit reporting, borrowers can navigate IDR plans strategically, preserving credit health while managing student debt sustainably.

Is Student Loan Forgiveness Dead? Analyzing the Future of Debt Relief

You may want to see also

Explore related products

![]()

Credit Utilization: Potential effects of reduced monthly payments on debt-to-income ratios

Reducing monthly payments through an Income-Driven Repayment (IDR) plan can significantly alter your debt-to-income (DTI) ratio, a critical factor in credit utilization. DTI is calculated by dividing your total monthly debt payments by your gross monthly income, expressed as a percentage. For example, if your monthly debt payments are $1,000 and your income is $4,000, your DTI is 25%. Lowering your student loan payments through an IDR plan directly decreases the numerator in this equation, potentially improving your DTI ratio. This improvement can make you appear less risky to lenders, as a lower DTI indicates greater financial flexibility.

However, the impact on credit utilization isn’t solely positive. While reduced payments lower your DTI, they may extend the life of your loan, increasing the total interest paid over time. For instance, switching to an IDR plan might reduce a $500 monthly payment to $200, but extend repayment from 10 to 25 years. This trade-off requires careful consideration, especially if you’re planning to apply for credit soon. Lenders scrutinize both DTI and total debt, so while a lower DTI might help, a higher overall debt balance could offset the benefits.

To maximize the positive effects of reduced payments on your credit utilization, pair IDR adjustments with strategic financial planning. For example, allocate the savings from lower student loan payments toward high-interest debts, such as credit cards. This approach not only improves your DTI but also reduces your overall credit utilization ratio, which should not exceed 30% of your available credit for optimal credit health. Additionally, monitor your credit report regularly to ensure accuracy, as errors can artificially inflate your DTI or credit utilization.

A practical tip for those considering IDR plans is to simulate the impact on your DTI using online calculators. Input your current income, existing debts, and proposed IDR payment to see how the change affects your ratio. For instance, if your DTI drops from 35% to 28% after switching to an IDR plan, this could improve your chances of qualifying for a mortgage or auto loan. Conversely, if the reduction is minimal, weigh the long-term cost of extended repayment against the short-term credit benefits.

In conclusion, reduced monthly payments through an IDR plan can positively influence your DTI ratio, a key component of credit utilization. However, this benefit must be balanced against the potential drawbacks of prolonged debt and increased interest. By strategically managing savings and monitoring credit health, you can leverage IDR plans to enhance your financial profile while minimizing risks. Always assess your unique financial situation before making adjustments to ensure the best possible outcome.

Student Loan Forgiveness: Understanding the 7-Year Myth and Reality

You may want to see also

Explore related products

![]()

Credit Inquiries: Does enrolling in IDR trigger new credit checks?

Enrolling in an Income-Driven Repayment (IDR) plan for your student loans does not typically trigger a new credit check. Unlike applying for a new loan or credit card, which often results in a hard inquiry on your credit report, IDR enrollment is an adjustment to your existing loan terms. This process is administrative in nature and does not require lenders to reassess your creditworthiness. As a result, your credit score remains unaffected by the act of enrolling in an IDR plan itself.

However, it’s important to distinguish between the enrollment process and the broader impact of IDR on your credit. While the enrollment doesn’t generate a new credit inquiry, your payment history under the plan can influence your credit score. For example, if IDR lowers your monthly payments and you consistently make them on time, this positive payment history can strengthen your credit profile. Conversely, if you miss payments or default, your credit score could suffer. The key takeaway is that IDR enrollment itself is neutral regarding credit inquiries, but your behavior post-enrollment matters significantly.

Another point to consider is how IDR might indirectly affect your credit utilization ratio. If IDR reduces your monthly payments, you may have more disposable income, which could lead to increased spending or borrowing. If you take on additional debt, such as maxing out credit cards, your credit utilization ratio could rise, negatively impacting your credit score. While this isn’t a direct result of IDR enrollment, it’s a practical consideration for borrowers adjusting their budgets after switching to an IDR plan.

For borrowers concerned about credit inquiries, understanding the distinction between hard and soft inquiries is crucial. Hard inquiries, which occur when you apply for new credit, can temporarily lower your credit score. Soft inquiries, such as checking your own credit report or lenders reviewing your credit for pre-approval offers, do not impact your score. Since IDR enrollment doesn’t involve a hard inquiry, it’s a non-issue in this context. However, staying informed about what does trigger hard inquiries can help you manage your credit more effectively.

In summary, enrolling in an IDR plan does not trigger new credit checks or inquiries. The process is administrative and focuses on adjusting your loan terms based on income, not reassessing your creditworthiness. While this means your credit score won’t be directly affected by enrollment, maintaining timely payments under the plan is essential for preserving or improving your credit. Borrowers should also be mindful of how reduced payments might influence their overall financial habits, ensuring they avoid behaviors that could negatively impact their credit score.

Can Your Work Hours Accelerate Student Loan Forgiveness? Find Out

You may want to see also

Explore related products

![]()

Long-Term Impact: How IDR may influence credit over time, including loan forgiveness

Income-Driven Repayment (IDR) plans can reshape your financial trajectory, but their long-term impact on credit is nuanced. Initially, enrolling in an IDR plan doesn’t inherently damage your credit score. Since payments are reported as "current" as long as you meet the reduced monthly obligation, your payment history—a key credit factor—remains intact. However, the lower payments may extend your loan term, keeping the debt active on your credit report for longer. This extended presence can modestly reduce your credit utilization ratio, a positive factor, but it also delays the "aging off" of the debt, which typically occurs 7–10 years after delinquency or payoff.

Loan forgiveness under IDR plans introduces another layer of complexity. While forgiven amounts aren’t reported as negative on your credit report, the tax implications can indirectly affect your credit. Before 2021, forgiven balances were treated as taxable income, potentially increasing your tax liability. High tax burdens could strain cash flow, leading to missed payments on other debts and harming your credit. However, the American Rescue Act of 2021 temporarily waived taxes on forgiven student loans through 2025, mitigating this risk for now. Still, borrowers should plan for potential tax changes post-2025 to avoid financial strain.

A lesser-known benefit of IDR is its ability to free up monthly cash flow, which can indirectly improve credit health. For example, if your IDR payment drops from $500 to $100 monthly, the extra $400 can be allocated to high-interest credit card debt or savings. Reducing credit card balances improves your credit utilization ratio, while savings provide a buffer against emergencies that might otherwise lead to missed payments. Over time, this strategic reallocation can boost your credit score more than the extended loan term detracts from it.

Finally, the psychological impact of IDR on financial behavior shouldn’t be overlooked. Knowing that a portion of your debt may eventually be forgiven can reduce stress and encourage disciplined financial habits. For instance, a borrower in their 30s on an IDR plan might feel empowered to avoid new high-interest debt, focus on building credit through timely payments, and invest in retirement accounts. Over 20–25 years, these habits can lead to a stronger credit profile than if the borrower had struggled under a standard repayment plan. However, this outcome depends on proactive financial management, not just the IDR structure itself.

In summary, IDR’s long-term credit impact hinges on multiple factors: tax policy changes, cash flow management, and behavioral adjustments. While the extended loan term and potential tax liabilities pose risks, strategic use of freed-up funds and disciplined financial planning can turn IDR into a credit-building tool. Borrowers should monitor tax laws, prioritize high-interest debt reduction, and leverage the psychological relief of IDR to foster long-term credit health.

Is Forgiving Student Loans Fair? Exploring Pros, Cons, and Implications

You may want to see also

Frequently asked questions

Applying for an IDR plan itself does not directly impact your credit score, as it is not reported to credit bureaus as a new loan or credit inquiry. However, if your payments under the IDR plan are lower than the accruing interest, your loan balance may increase, which could indirectly affect your debt-to-income ratio if lenders review it.

Being on an IDR plan will not negatively impact your credit report as long as you make all required payments on time. Late or missed payments, however, will be reported to credit bureaus and can harm your credit score, regardless of the repayment plan.

Enrolling in an IDR plan does not appear on your credit history. Only payment status (e.g., on-time, late, or missed payments) and loan account details are reported to credit bureaus. As long as you adhere to the plan’s terms, your credit history remains unaffected.