The question of whether back interest will be added to student loans is a pressing concern for many borrowers, especially as they navigate the complexities of loan repayment. With the rising cost of education and the significant debt burden faced by students, understanding the intricacies of interest accrual is crucial. Back interest, or capitalized interest, can substantially increase the total amount owed, making it essential for borrowers to be aware of how and when it may be applied to their loans. This issue is further complicated by varying policies across different loan types, such as federal versus private loans, and the impact of deferment or forbearance periods. As such, staying informed about potential changes in legislation and loan terms is vital for managing student debt effectively.

| Characteristics | Values |

|---|---|

| Interest Accrual During Grace Period | Depends on loan type (e.g., subsidized vs. unsubsidized loans). |

| Subsidized Loans | No interest accrues while in school, grace period, or deferment. |

| Unsubsidized Loans | Interest accrues from the date of disbursement, including grace period. |

| Private Student Loans | Interest typically accrues immediately after disbursement. |

| Repayment Plans | Interest may capitalize (added to principal) if unpaid during forbearance or certain plans. |

| Current Interest Rates (2023) | Varies by loan type and disbursement date (e.g., 5.5% for undergraduate subsidized loans). |

| Interest Capitalization | Occurs when unpaid interest is added to the principal balance. |

| Grace Period Length | Typically 6 months after graduation for federal loans. |

| Deferment/Forbearance | Interest may or may not accrue depending on loan type and circumstances. |

| Loan Forgiveness Programs | Interest may be forgiven under certain conditions (e.g., PSLF). |

| Latest Policy Updates (2023) | No major changes to interest accrual policies for federal loans. |

Explore related products

What You'll Learn

![]()

Current Interest Rates on Student Loans

Interest rates on student loans are not static; they fluctuate based on economic conditions and federal policies. As of the latest updates, federal student loan interest rates for the 2023-2024 academic year range from 5.5% for undergraduate Direct Subsidized and Unsubsidized Loans to 8.05% for graduate PLUS Loans. These rates are tied to the 10-year Treasury note yield, plus a fixed margin, reflecting the government’s cost of borrowing. Private student loan rates, however, vary widely—typically between 4% and 13%—depending on creditworthiness and market competition. Understanding these rates is crucial, as they directly impact the total cost of repayment.

For borrowers, the type of loan matters significantly. Federal loans often come with fixed rates, meaning the interest remains constant over the loan’s life. Private loans, on the other hand, may offer variable rates, which can rise or fall with market conditions. For instance, a borrower with a variable-rate private loan at 6% today could see that rate climb to 8% or higher if interest rates increase nationally. This unpredictability underscores the importance of carefully comparing loan options before committing.

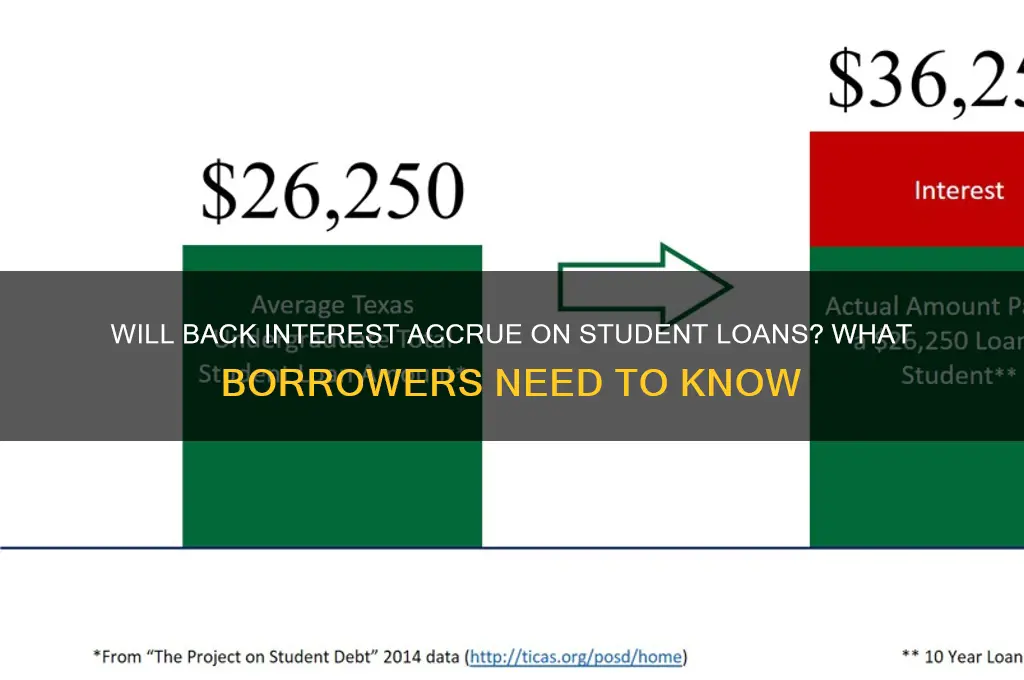

One critical factor often overlooked is the impact of capitalization—when unpaid interest is added to the loan’s principal balance. For federal unsubsidized loans, interest accrues while the borrower is in school, and if not paid, it capitalizes upon entering repayment. This increases the total amount owed, as interest is then calculated on a higher principal. For example, a $10,000 loan with $1,000 in capitalized interest becomes an $11,000 loan, significantly raising the long-term cost. Borrowers can mitigate this by making interest payments while in school, even if they’re not required.

Refinancing is another strategy to manage interest rates, particularly for those with high-interest private loans or federal loans with rates above current market levels. Refinancing replaces existing loans with a new one at a lower rate, potentially saving thousands over the loan term. However, federal loan borrowers should weigh this carefully, as refinancing into a private loan means losing access to income-driven repayment plans, loan forgiveness programs, and other federal protections. For instance, refinancing a 7% federal PLUS Loan to a 5% private loan could save money but would forfeit Public Service Loan Forgiveness eligibility.

In conclusion, navigating current interest rates on student loans requires a proactive approach. Borrowers should monitor federal rate changes annually, compare private loan offers meticulously, and consider strategies like in-school interest payments or refinancing to minimize costs. By staying informed and strategic, borrowers can reduce the financial burden of student debt and set themselves up for more manageable repayment.

Understanding the Sequence of Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Impact of Forbearance on Interest Accrual

Forbearance, a temporary pause or reduction in student loan payments, can be a lifeline for borrowers facing financial hardship. However, it’s crucial to understand that for most federal student loans, interest continues to accrue during forbearance periods. This means the total amount owed grows, even if payments are paused. For example, a borrower with a $30,000 loan at a 6% interest rate could see their balance increase by approximately $150 per month during forbearance, adding $1,800 to their debt over a year. This silent growth of debt underscores the importance of weighing the immediate relief of forbearance against its long-term financial implications.

The impact of interest accrual during forbearance varies depending on the type of loan. For subsidized federal loans, the government covers the interest while the borrower is in school or during certain deferment periods, but not during forbearance. Unsubsidized federal loans and private loans, however, always accrue interest during forbearance, and this unpaid interest is typically capitalized—added to the principal balance—once the forbearance ends. This capitalization can lead to higher monthly payments and increased total repayment costs. For instance, if $1,000 in interest accrues during forbearance and is capitalized, the borrower will then pay interest on that additional $1,000 over the life of the loan.

To mitigate the effects of interest accrual during forbearance, borrowers should explore alternative options if possible. Income-driven repayment plans, which adjust monthly payments based on income and family size, can provide more sustainable relief without the same degree of interest capitalization. Additionally, making interest-only payments during forbearance, even if full payments are paused, can prevent capitalization and keep the loan balance from ballooning. For example, on a $30,000 loan at 6%, paying $150 per month in interest during forbearance would prevent the balance from increasing.

A comparative analysis reveals that forbearance is often less advantageous than other repayment strategies in the long run. While it offers immediate payment relief, the compounding interest can offset its benefits, particularly for borrowers with high loan balances or interest rates. In contrast, deferment—another option for pausing payments—may be interest-free for subsidized loans, making it a more cost-effective choice in some cases. Borrowers should carefully evaluate their financial situation and loan terms to determine the best course of action, potentially consulting a financial advisor or loan servicer for personalized guidance.

In conclusion, while forbearance can provide temporary financial breathing room, its impact on interest accrual and loan capitalization demands careful consideration. Borrowers must weigh the short-term benefits against the long-term costs, exploring alternatives like income-driven plans or interest-only payments to minimize debt growth. Understanding these nuances empowers borrowers to make informed decisions, ensuring that forbearance serves as a tool for financial stability rather than a trap of increasing debt.

Will Student Loans in Collections Qualify for Loan Forgiveness?

You may want to see also

Explore related products

![]()

Subsidized vs. Unsubsidized Loan Interest Rules

Understanding the difference between subsidized and unsubsidized student loans is crucial for managing your financial burden effectively. Subsidized loans, offered to undergraduate students with demonstrated financial need, come with a significant advantage: the government pays the interest on these loans while you’re in school at least half-time, during the grace period after graduation (typically six months), and during any approved deferment periods. This means the amount you owe doesn’t grow during these times, providing a financial cushion as you transition into repayment.

In contrast, unsubsidized loans are available to both undergraduate and graduate students regardless of financial need, but they lack this interest-free grace. Interest begins accruing immediately after the loan is disbursed, even while you’re still in school. If you choose not to pay this interest as it accrues, it will be capitalized—added to the principal balance of your loan—increasing the total amount you’ll owe over time. For example, if you borrow $5,000 with a 4.99% interest rate and defer payments until graduation, the capitalized interest could add hundreds of dollars to your balance.

To minimize the impact of unsubsidized loan interest, consider making interest payments while in school, even if they’re not required. Paying just $25 a month on a $5,000 loan at 4.99% can save you over $700 in capitalized interest by the time you graduate. This proactive approach prevents your debt from snowballing and reduces the overall cost of your education.

Another key difference lies in eligibility and borrowing limits. Subsidized loans are need-based, and the amount you can borrow is determined by your school and financial situation, often with lower limits than unsubsidized loans. Unsubsidized loans have higher borrowing limits and are not tied to financial need, making them a more flexible but potentially riskier option if not managed carefully.

In summary, subsidized loans offer a safety net by pausing interest accrual during critical periods, while unsubsidized loans require immediate attention to avoid escalating debt. By understanding these rules and taking proactive steps, such as making interest payments while in school, you can navigate the complexities of student loans more effectively and reduce long-term financial strain.

Disability Forgiveness for Great Lakes Student Loans: What You Need to Know

You may want to see also

Explore related products

$7.99

![]()

Interest Capitalization After Deferment Periods

To minimize the impact of interest capitalization, consider making interest payments during your deferment period, even if they’re not required. For instance, paying $83 monthly on a $20,000 loan at 5% interest would prevent capitalization entirely. If full payments aren’t feasible, even partial payments can reduce the amount capitalized. Another strategy is to explore income-driven repayment plans or loan consolidation, which may offer lower monthly payments or reset deferment terms. For borrowers under 30, starting this practice early can save thousands over the life of the loan, as compounded interest grows exponentially over time.

A comparative analysis reveals that subsidized loans, where the government covers interest during deferment, are far more borrower-friendly than unsubsidized loans. However, subsidized loans are typically limited to undergraduate students with demonstrated financial need. If you have unsubsidized loans, monitor your interest accrual closely, especially during deferment. Tools like loan simulators or calculators can project future balances with and without capitalization, helping you make informed decisions. For instance, a borrower with $30,000 in unsubsidized loans at 6% interest could see their balance increase by $1,800 after a 12-month deferment—a cost that could be halved with proactive payments.

Finally, if you’re nearing the end of a deferment period, review your loan terms and contact your servicer to discuss options. Some servicers offer temporary forbearance or alternative repayment plans to ease the transition. Additionally, consider refinancing if you have a stable income and good credit, as private lenders may offer lower interest rates that reduce long-term costs. While interest capitalization is a built-in feature of many student loans, staying informed and proactive can mitigate its financial burden, ensuring you’re not paying more than necessary.

Great Lakes Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Government Policies on Student Loan Interest Relief

Student loan interest relief has become a critical policy area as governments grapple with the growing burden of educational debt. One key strategy is the implementation of interest-free periods, often during grace periods after graduation or for borrowers in economic hardship. For instance, the U.S. government offers interest-free deferment for subsidized federal loans while borrowers are in school, and some countries, like England, cap interest rates at inflation for certain loan types. These measures aim to provide breathing room for graduates entering the workforce, reducing immediate financial strain and preventing debt from spiraling out of control.

Another approach is income-driven repayment plans, which tie monthly payments to a borrower’s earnings and often include interest subsidies. In the U.S., plans like Pay As You Earn (PAYE) and Revised Pay As You Earn (REPAYE) limit payments to 10% of discretionary income and cover any accrued interest above the monthly payment for subsidized loans. Similarly, Australia’s Higher Education Loan Program (HELP) adjusts repayments based on income and applies a relatively low interest rate indexed to inflation. Such policies ensure that borrowers are not overwhelmed by interest accumulation, particularly during low-earning years.

A more direct form of relief is interest forgiveness or cancellation programs. Canada’s Repayment Assistance Plan (RAP) forgives interest for eligible low-income borrowers, while the U.S. Public Service Loan Forgiveness (PSLF) program waives remaining debt, including accrued interest, after 10 years of qualifying payments. These initiatives incentivize public service careers and provide long-term financial stability for borrowers in critical sectors. However, eligibility criteria and administrative complexities often limit their reach, highlighting the need for streamlined access.

Critically, the effectiveness of these policies depends on their design and implementation. For example, interest-free periods are most impactful when paired with robust job placement programs, ensuring graduates can secure employment before repayment begins. Income-driven plans require clear communication and user-friendly platforms to avoid confusion and underutilization. Policymakers must also address the moral hazard of overborrowing by balancing relief measures with incentives for cost-effective education choices. By refining these strategies, governments can alleviate the student debt crisis while fostering equitable access to higher education.

Student Loan Forgiveness: Types of Loans That Can Be Erased

You may want to see also

Frequently asked questions

During federally authorized repayment pauses, such as those under the CARES Act, interest on eligible federal student loans is temporarily set to 0%, meaning no back interest will accrue.

Back interest policies vary; federal student loans may have interest paused during specific periods, while private student loans typically continue to accrue interest unless otherwise stated by the lender.

For subsidized federal loans, the government pays the interest during deferment, so no back interest is added. For unsubsidized loans and private loans, interest usually accrues and may be capitalized, adding to the principal balance.

If you miss payments, interest will continue to accrue on most loans, and unpaid interest may capitalize, increasing the total amount you owe. This applies to both federal and private student loans unless you qualify for forbearance or deferment.