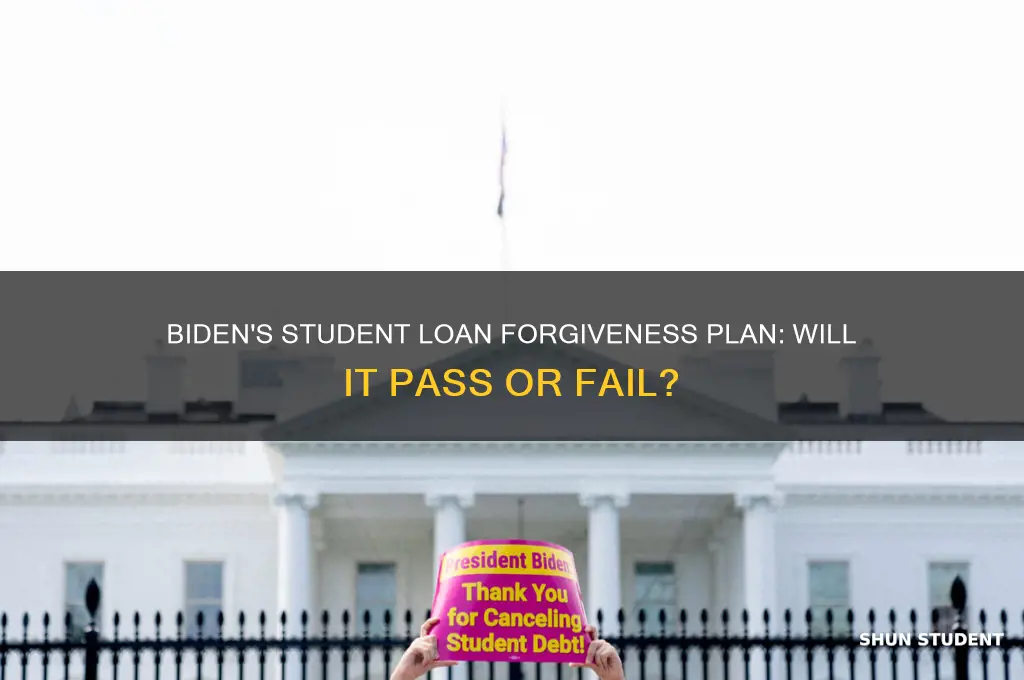

The question of whether President Biden's student loan forgiveness plan will go through remains a highly debated and closely watched issue, as it faces significant legal, political, and logistical challenges. Announced in 2022, the plan aimed to provide up to $20,000 in debt relief for millions of borrowers, but it has been mired in lawsuits and opposition from Republican lawmakers and conservative groups. The Supreme Court’s decision in June 2023 struck down the initial program, citing a lack of congressional authorization. Since then, the Biden administration has pursued alternative pathways, including targeted relief through existing programs like income-driven repayment plans and Public Service Loan Forgiveness, while also exploring new legal avenues. Despite these efforts, the fate of widespread student loan forgiveness remains uncertain, leaving borrowers in limbo and fueling ongoing discussions about the broader implications for higher education financing and economic equity.

| Characteristics | Values |

|---|---|

| Current Status | As of October 2023, Biden's student loan forgiveness plan is on hold due to legal challenges. The Supreme Court struck down the plan in June 2023. |

| Original Plan Scope | Up to $20,000 in forgiveness for Pell Grant recipients and $10,000 for non-Pell Grant borrowers earning under $125,000 (individual) or $250,000 (married). |

| Legal Challenges | The plan faced lawsuits from Republican-led states and conservative groups, arguing it exceeded presidential authority. |

| Supreme Court Ruling | The Court ruled 6-3 against the plan, stating it required congressional approval under the HEROES Act. |

| Alternative Efforts | The Biden administration is exploring other avenues, such as income-driven repayment (IDR) reforms and targeted loan cancellations for specific groups. |

| Payment Restart | Student loan payments resumed in October 2023 after a three-year pause during the pandemic. |

| Public Opinion | Mixed reactions, with supporters praising debt relief and critics arguing it burdens taxpayers and inflates inflation. |

| Congressional Action | No significant bipartisan legislation has passed to replace or revive the forgiveness plan. |

| Future Prospects | Uncertain, as the administration focuses on smaller-scale relief measures and IDR improvements. |

Explore related products

$14.99 $14.99

What You'll Learn

- Eligibility Criteria: Who qualifies for Biden's student loan forgiveness plan

- Loan Amounts: How much debt will be forgiven under the plan

- Legal Challenges: Potential lawsuits and court rulings affecting implementation

- Application Process: Steps borrowers need to take to receive forgiveness

- Impact on Budget: How the plan affects federal spending and taxpayers

![]()

Eligibility Criteria: Who qualifies for Biden's student loan forgiveness plan?

President Biden's student loan forgiveness plan has been a topic of intense discussion, with many borrowers eagerly awaiting details on who qualifies. To determine eligibility, it's crucial to understand the specific criteria set forth by the plan. The primary factor is income, with individuals earning less than $125,000 per year or households earning less than $250,000 per year qualifying for relief. This threshold is a key determinant in assessing who will benefit from the proposed forgiveness.

The type of loan held also plays a significant role in eligibility. Federal student loans, including Direct Loans, Perkins Loans, and Federal Family Education Loans (FFEL) held by the Department of Education, are generally covered under the plan. However, privately held FFEL loans and Perkins loans not owned by the Department of Education may not qualify. Borrowers should carefully review their loan types to ensure they meet the necessary criteria.

Another critical aspect is the loan disbursement date. The plan typically covers loans disbursed before a specific cutoff date, often mentioned in official announcements. Loans taken out after this date may not be eligible for forgiveness. It’s essential for borrowers to check their loan disbursement dates against the plan’s guidelines to confirm their eligibility.

For those who meet the income and loan type criteria, the amount of forgiveness varies. The plan often offers up to $10,000 in relief for eligible borrowers, with an additional $10,000 for Pell Grant recipients. This tiered approach aims to provide greater support to borrowers with the highest financial need. Understanding these specifics can help individuals gauge the potential impact of the forgiveness plan on their financial situation.

Lastly, borrowers should stay informed about the application process and any updates to the plan. While the eligibility criteria provide a framework, the actual implementation may involve additional steps, such as submitting an application or providing documentation. Keeping track of official announcements and deadlines is crucial to ensuring a smooth process. By carefully reviewing these criteria and staying proactive, eligible borrowers can maximize their chances of benefiting from President Biden's student loan forgiveness plan.

Candidates Pushing for Student Loan Forgiveness in Upcoming Elections

You may want to see also

Explore related products

![]()

Loan Amounts: How much debt will be forgiven under the plan?

The Biden administration's student loan forgiveness plan has been a topic of intense debate and scrutiny, with many borrowers eagerly awaiting details on how much debt will be forgiven. According to the plan, eligible borrowers can expect to have up to $20,000 of their federal student loan debt canceled, but this amount is contingent on specific criteria. Pell Grant recipients, who typically demonstrate significant financial need, are eligible for the full $20,000, while non-Pell Grant recipients can receive up to $10,000 in forgiveness. This tiered approach aims to provide targeted relief to those most burdened by student debt.

To qualify for this forgiveness, borrowers must meet income thresholds: individuals earning less than $125,000 annually or married couples filing jointly with incomes under $250,000 are eligible. These limits ensure that the relief is directed toward middle- and lower-income borrowers, addressing concerns about fairness and fiscal responsibility. It’s crucial for borrowers to verify their eligibility by reviewing their income from either 2020 or 2021 tax returns, as these years are used to determine qualification.

One practical tip for borrowers is to ensure their contact information is updated with their loan servicers. The Department of Education plans to roll out an application process for forgiveness, and being reachable will streamline the process. Additionally, borrowers should monitor official government websites for updates, as misinformation about the program has been widespread. Understanding the specifics of the plan, such as the $20,000 cap for Pell Grant recipients and the $10,000 cap for others, can help set realistic expectations and avoid confusion.

Comparatively, this plan stands out from previous forgiveness initiatives due to its broad scope and targeted approach. While programs like Public Service Loan Forgiveness (PSLF) require years of qualifying payments, Biden’s plan offers immediate relief based on income and Pell Grant status. However, it’s important to note that private student loans are not eligible for forgiveness under this plan, leaving some borrowers with limited options. For those with both federal and private debt, focusing on paying down private loans while taking advantage of federal forgiveness can be a strategic financial move.

In conclusion, the Biden student loan forgiveness plan offers substantial relief, with up to $20,000 in debt cancellation for eligible borrowers. By understanding the income thresholds, eligibility criteria, and practical steps to apply, borrowers can maximize their benefits. While the plan is not a one-size-fits-all solution, it represents a significant step toward alleviating the burden of student debt for millions of Americans. Staying informed and proactive will be key to navigating this opportunity effectively.

Understanding Forgivable Student Loans: Eligibility, Benefits, and Repayment Options

You may want to see also

Explore related products

![]()

Legal Challenges: Potential lawsuits and court rulings affecting implementation

The Biden administration's student loan forgiveness plan faces a gauntlet of legal challenges that could determine its fate. Opponents argue the plan oversteps executive authority, violating the Administrative Procedure Act and the separation of powers doctrine. Lawsuits filed by Republican-led states and conservative groups claim the Department of Education lacks the statutory authority to cancel debt on such a massive scale without explicit congressional approval. These cases hinge on interpreting the Higher Education Relief Opportunities for Students (HEROES) Act, which the administration cites as its legal basis. If courts side with challengers, the program could be blocked or significantly scaled back, leaving millions of borrowers in limbo.

Consider the Supreme Court’s role in this legal drama. In *Biden v. Nebraska* (2023), the Court struck down the administration’s initial attempt at broad student loan forgiveness, ruling it exceeded presidential power. This precedent looms large over current litigation. Lower courts must now decide whether the revised plan, which targets specific groups like Pell Grant recipients, passes constitutional muster. Legal experts warn that even minor adjustments may not satisfy skeptical judges, particularly in conservative-leaning circuits. Borrowers should monitor cases like *Missouri v. Biden*, where states argue financial harm from reduced loan servicing revenue, as these could set binding precedents.

A critical factor in these lawsuits is standing—whether plaintiffs have a legal right to sue. Early challenges failed because courts ruled states and individuals lacked demonstrable injury. However, recent filings by loan servicers and state attorneys general have refined their arguments, claiming direct economic harm. For instance, Missouri argues that forgiveness reduces revenue for the Missouri Higher Education Loan Authority (MOHELA), a state entity. If courts accept this logic, it could open the floodgates for more lawsuits, delaying implementation for months or even years. Borrowers should prepare for prolonged uncertainty by continuing regular payments until a final ruling.

Strategically, the administration is narrowing the plan’s scope to bolster its legal defense. By targeting relief to borrowers earning under $125,000 (individuals) or $250,000 (couples), it aims to demonstrate a rational connection to the HEROES Act’s purpose of aiding those affected by national emergencies. However, this approach risks alienating higher-earning borrowers who feel unfairly excluded. Advocates counter that such exclusions are necessary to survive judicial scrutiny, but this trade-off highlights the tension between policy ambition and legal pragmatism. Borrowers should verify their eligibility under these revised criteria to avoid confusion.

Ultimately, the plan’s survival depends on courts’ willingness to defer to executive discretion during crises. The HEROES Act grants the Education Secretary broad authority to “waive or modify” loan provisions during emergencies, but judges may question whether debt cancellation aligns with this mandate. Historical precedent offers little guidance, as no administration has attempted such sweeping relief. Borrowers should stay informed via official channels like studentaid.gov and avoid speculative advice. While the legal battle rages, the program’s future remains uncertain, underscoring the high stakes of this constitutional clash.

Will Student Loans in Collections Qualify for Loan Forgiveness?

You may want to see also

Explore related products

![]()

Application Process: Steps borrowers need to take to receive forgiveness

The Biden administration's student loan forgiveness plan has been a topic of much discussion, with many borrowers eagerly awaiting details on how to apply. For those eligible, the application process is a critical step in securing relief. Here’s a breakdown of what borrowers need to know to navigate this process effectively.

Step 1: Verify Eligibility

Before diving into the application, borrowers must confirm their eligibility. The forgiveness program typically targets federal student loan borrowers earning below specific income thresholds ($125,000 for individuals, $250,000 for married couples filing jointly). Additionally, the type of loan (e.g., Direct Loans, FFELP loans managed by the Department of Education) and repayment plan can affect eligibility. Use the Federal Student Aid website to check your loan type and income status. If you’re unsure, contact your loan servicer for clarification.

Step 2: Gather Required Documentation

Once eligibility is confirmed, gather necessary documents. This includes proof of income, such as tax returns or pay stubs, and loan account details. The application may also require personal identification, like a Social Security number or driver’s license. Keep these documents organized and readily accessible to streamline the process. For borrowers with complex financial situations, consulting a financial advisor or tax professional can ensure accuracy.

Step 3: Complete the Application

The application itself is expected to be available online through the Department of Education’s website. Borrowers will need to provide detailed information about their loans, income, and personal circumstances. Be thorough and accurate—errors can delay processing. The application may also include a section for borrowers to certify their eligibility under penalty of perjury, so honesty is crucial. If the application is paper-based or requires additional forms, follow instructions carefully and submit all materials by the deadline.

Cautions and Tips

Beware of scams targeting borrowers seeking forgiveness. The government will never charge a fee for loan forgiveness applications. Avoid third-party services promising expedited processing—they are often fraudulent. Instead, rely on official channels like the Federal Student Aid website or your loan servicer for updates. Additionally, keep an eye on your email and mail for notifications about the application’s release and any required follow-up actions.

Navigating the student loan forgiveness application process requires preparation, attention to detail, and vigilance against scams. By verifying eligibility, gathering documents, and completing the application accurately, borrowers can maximize their chances of receiving relief. Stay informed through official sources and take proactive steps to ensure a smooth application experience.

Will Biden's Student Loan Forgiveness Apply Automatically to Borrowers?

You may want to see also

Explore related products

![]()

Impact on Budget: How the plan affects federal spending and taxpayers

Biden's student loan forgiveness plan, if implemented, would inject a substantial one-time expense into the federal budget, estimated at $300 billion to $400 billion. This figure, while significant, pales in comparison to the $1.7 trillion currently outstanding in federal student loans. The plan's impact on annual deficits would depend on the chosen funding mechanism. Direct appropriation from general revenue would immediately widen the deficit, while relying on existing Department of Education funds could involve reallocating resources from other educational programs.

Crucially, the plan's long-term budgetary impact hinges on its ability to stimulate economic growth. Forgiveness could boost disposable income for millions, potentially increasing consumer spending and tax revenue. However, if economic growth fails to materialize, the plan could contribute to a larger national debt burden, requiring future tax increases or spending cuts to address.

Consider the analogy of a household budget. Imagine a family deciding whether to pay off a large credit card debt in one lump sum. While this eliminates future interest payments, it requires a significant upfront expenditure. Similarly, student loan forgiveness presents a trade-off between immediate cost and potential long-term benefits.

Taxpayers, both directly and indirectly, will bear the cost of this plan. Direct taxpayers, particularly those without student loans, may feel a sense of inequity. Indirectly, all taxpayers could face the consequences of a larger national debt, potentially leading to higher interest rates and reduced government spending in other areas.

Ultimately, the budgetary impact of Biden's student loan forgiveness plan is a complex equation. While it offers potential economic benefits, it also carries significant costs. Policymakers must carefully weigh these factors, considering both the immediate financial burden and the long-term implications for taxpayers and the overall economy.

Should You Apply for Student Loan Forgiveness? A Guide

You may want to see also

Frequently asked questions

As of now, the fate of Biden's student loan forgiveness plan is uncertain due to ongoing legal challenges and political opposition. The Supreme Court’s decision in 2023 struck down the initial plan, but the administration is exploring alternative pathways to provide relief.

If the plan is implemented, individuals earning less than $125,000 annually (or $250,000 for married couples) could qualify for up to $10,000 in forgiveness, with an additional $10,000 for Pell Grant recipients. However, eligibility details may change based on the final approved plan.

The timeline is unclear due to legal and legislative hurdles. Borrowers should stay updated through official channels like the Department of Education’s website and prepare for potential changes to repayment plans or relief options.

![EidolonGreen [China Medicinal Herb] Bidens Tripartita(Bidens Tripartita L./Trifid Bur-marigold/Gui Zhen Cao/鬼针草/귀신침 초) Dried Bulk Herb 3 Oz (88 g)](https://m.media-amazon.com/images/I/61B8U7-NK2S._AC_UL320_.jpg)