The debate over canceling student debt has sparked significant discussion about its potential economic impacts, particularly whether such a policy could exacerbate inflation. Proponents argue that forgiving student loans would alleviate financial burdens on millions of Americans, boosting consumer spending and stimulating economic growth. However, critics warn that injecting large sums of money into the economy through debt cancellation could increase demand without a corresponding rise in supply, potentially driving up prices and contributing to inflation. Additionally, concerns arise about the fairness of the policy and its long-term effects on government spending and borrowing. As policymakers weigh these considerations, the question remains: could canceling student debt unintentionally fuel inflationary pressures in an already fragile economic environment?

| Characteristics | Values |

|---|---|

| Economic Impact | Canceling student debt could increase inflation by boosting consumer spending. |

| Amount of Debt Cancellation | Proposals range from $10,000 to $50,000 per borrower, totaling $1.7 trillion in federal student loans. |

| Inflationary Pressure | Estimates suggest a potential 0.1-0.3 percentage point increase in inflation over 1-2 years. |

| Timing of Impact | Inflationary effects would likely be temporary, concentrated in the short term. |

| Offsetting Factors | Increased tax revenue from higher economic activity could partially offset inflation. |

| Targeted vs. Universal Cancellation | Targeted cancellation (e.g., income-based) may have a smaller inflationary impact than universal cancellation. |

| Monetary Policy Response | The Federal Reserve could raise interest rates to counteract inflationary pressures. |

| Long-Term Economic Effects | Debt cancellation could improve long-term economic growth by increasing household wealth and reducing defaults. |

| Political and Social Considerations | Public opinion is divided, with arguments for fairness and economic stimulus versus concerns about inflation and moral hazard. |

| Latest Data (as of October 2023) | Inflation remains a concern, with the Federal Reserve closely monitoring fiscal policies like debt cancellation. |

Explore related products

What You'll Learn

- Impact on Consumer Spending: Higher disposable income may boost spending, driving demand and prices

- Effect on Labor Market: Debt relief could reduce worker urgency, potentially easing wage inflation pressures

- Government Spending Role: Increased federal spending might add to inflationary pressures in the economy

- Wealth Inequality Factor: Targeted relief may mitigate inflation by aiding lower-income households disproportionately

- Long-Term Economic Effects: Debt cancellation could stimulate growth, but risks overheating the economy

![]()

Impact on Consumer Spending: Higher disposable income may boost spending, driving demand and prices

Canceling student debt would inject billions into the economy by freeing up monthly cash flow for millions of borrowers. This sudden increase in disposable income could spark a spending spree, as individuals redirect funds previously allocated to loan payments toward goods and services. Imagine a 30-year-old earning $60,000 annually, burdened by $300 monthly student loan payments. Debt cancellation would effectively grant them a 6% raise, potentially fueling purchases like travel, electronics, or even a down payment on a home.

Multiply this scenario across millions, and the cumulative effect on consumer spending becomes significant.

However, this spending surge could have unintended consequences. Increased demand for goods and services, particularly in sectors with limited supply elasticity, could lead to price hikes. For instance, a rush to purchase homes in a tight housing market would likely drive up prices, benefiting sellers but potentially pricing out first-time buyers. Similarly, increased demand for travel could lead to higher airfares and hotel rates. This phenomenon, known as demand-pull inflation, occurs when aggregate demand exceeds aggregate supply, pushing prices upward.

While debt cancellation aims to alleviate financial strain, it could inadvertently contribute to the very inflation it seeks to avoid.

The magnitude of this inflationary pressure depends on several factors. The total amount of debt forgiven plays a crucial role. A targeted approach, focusing on low-income borrowers or those with high debt burdens, would likely have a smaller impact on overall spending compared to a blanket cancellation. Additionally, the state of the economy at the time of cancellation matters. In a recession, increased spending could stimulate economic growth without triggering significant inflation. Conversely, in a booming economy already facing supply chain constraints, the additional demand could exacerbate inflationary pressures.

Policymakers must carefully consider these factors to ensure debt cancellation achieves its intended goals without unintended economic consequences.

Mitigating potential inflationary effects requires a multi-pronged approach. Pairing debt cancellation with measures to increase supply, such as investments in housing construction or infrastructure, could help absorb the increased demand without driving up prices. Additionally, implementing targeted tax increases on higher-income earners could help offset the stimulative effect of debt cancellation. Finally, clear communication from policymakers about the potential risks and benefits of debt cancellation is essential for managing expectations and preventing panic-driven spending or hoarding behavior. By carefully considering these factors and implementing complementary policies, debt cancellation can be a tool for economic empowerment without fueling inflation.

Will Canada Halt Student Visas? Exploring Potential Policy Changes and Impacts

You may want to see also

Explore related products

![]()

Effect on Labor Market: Debt relief could reduce worker urgency, potentially easing wage inflation pressures

Student loan debt often forces individuals into jobs primarily for repayment, distorting labor market dynamics. High debt burdens create a sense of urgency, pushing workers to prioritize income over job fit, career growth, or personal fulfillment. This urgency can lead to a mismatch between skills and roles, reducing productivity and stifling innovation. For instance, a recent graduate with a degree in environmental science might take a high-paying finance job instead of pursuing their field, simply to service their loans. Debt relief could alleviate this pressure, allowing workers to make choices aligned with their skills and passions, potentially enhancing overall labor market efficiency.

Consider the wage inflation angle: when workers are desperate to repay debt, they may accept lower wages or avoid negotiating for better pay, suppressing wage growth. Conversely, debt-free individuals might feel empowered to demand fair compensation, potentially driving wages upward. However, this dynamic is nuanced. If debt relief reduces the urgency to work in any job, it could decrease labor force participation rates, particularly among younger workers. This reduced supply of labor might actually *increase* wage pressures in certain sectors, especially those reliant on entry-level or younger workers. Policymakers must weigh these competing forces carefully.

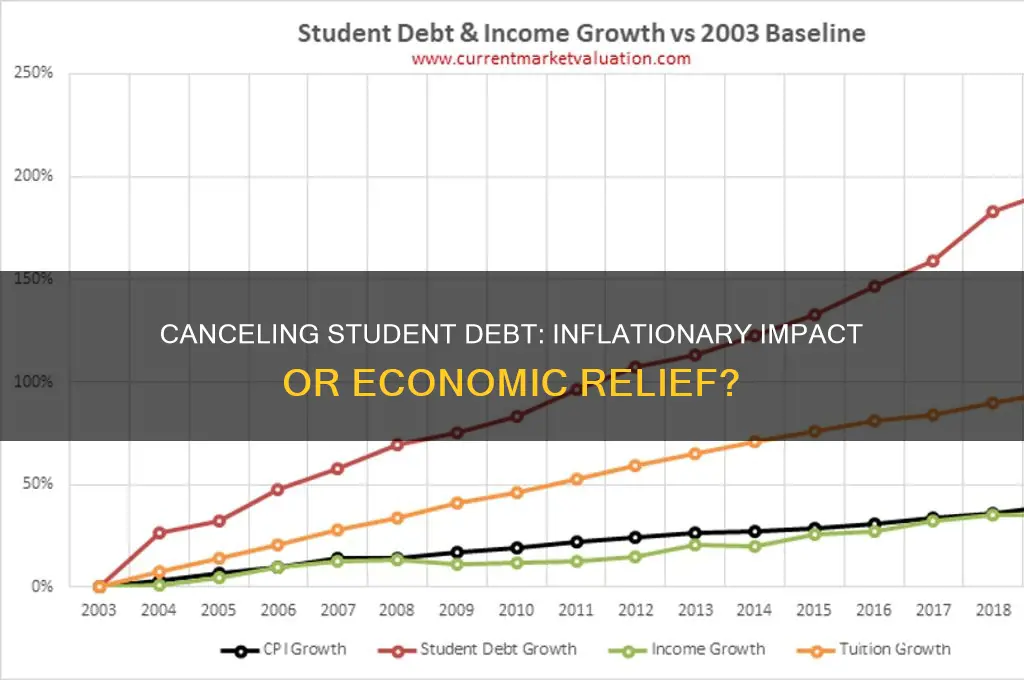

A comparative analysis of countries with and without significant student debt burdens offers insight. In nations like Germany, where higher education is largely tuition-free, labor markets tend to be more flexible, with workers transitioning between jobs and industries more freely. This flexibility can lead to better skill matching and higher productivity, potentially offsetting inflationary pressures. In contrast, the U.S. labor market, burdened by $1.7 trillion in student debt, often sees workers stuck in jobs they dislike, simply to repay loans. Debt relief could bring the U.S. closer to the German model, but the transition period may temporarily exacerbate wage inflation in certain sectors.

To mitigate risks, policymakers could pair debt relief with targeted workforce development programs. For example, offering incentives for workers to upskill in high-demand fields could ensure that reduced urgency doesn’t translate into labor shortages. Additionally, phasing in debt relief gradually, rather than implementing it all at once, could prevent sudden shocks to the labor market. For individuals, practical steps include reassessing career goals post-relief and investing in continuous learning to remain competitive. While debt relief may ease wage inflation pressures by reducing worker urgency, its success hinges on complementary policies that foster a resilient, adaptive labor market.

Minnesota's Tax Rules: Will Forgiven Student Loans Be Taxable?

You may want to see also

Explore related products

![]()

Government Spending Role: Increased federal spending might add to inflationary pressures in the economy

Canceling student debt, a policy often framed as a financial lifeline for millions, inherently involves a surge in federal spending. When the government forgives debt, it effectively transfers the liability from individuals to the public ledger, injecting billions—potentially trillions—of dollars into the economy. This injection, while intended to alleviate personal financial strain, operates similarly to any large-scale fiscal stimulus: it increases the money supply and boosts aggregate demand. The question then becomes one of scale and timing—how much additional spending can the economy absorb without triggering inflationary pressures?

Consider the mechanics of inflation: when demand outstrips supply, prices rise. Student debt cancellation puts more disposable income in the hands of borrowers, who may then spend it on goods and services. If this spending occurs in sectors already operating near capacity—housing, healthcare, or education, for instance—it could exacerbate existing supply constraints. For example, a 2021 study by the Federal Reserve Bank of New York estimated that canceling $1 trillion in student debt could boost GDP by $86 billion to $108 billion annually over the next decade. While this stimulus could spur economic growth, it also risks overheating sectors where supply is inelastic, leading to price increases.

However, the inflationary impact isn’t automatic or uniform. The effect depends on how borrowers allocate their newfound funds. If a significant portion of the savings is directed toward paying down other debts or saved rather than spent, the demand-side pressure could be muted. Conversely, if borrowers concentrate their spending in high-demand sectors, the inflationary effect could be amplified. Policymakers must therefore weigh the potential benefits of debt cancellation against the risk of unintended consequences, such as widening income inequality or crowding out other government priorities.

To mitigate these risks, a phased approach to debt cancellation could be considered. Instead of a one-time, lump-sum forgiveness, the government could implement gradual reductions tied to economic indicators like inflation rates or unemployment levels. This strategy would allow for real-time adjustments, ensuring that the stimulus doesn’t overwhelm the economy. Additionally, pairing debt cancellation with investments in supply-side measures—such as affordable housing initiatives or workforce training programs—could help balance increased demand with expanded capacity, thereby dampening inflationary pressures.

Ultimately, the role of government spending in canceling student debt is a double-edged sword. While it has the potential to stimulate economic growth and improve financial well-being for millions, it also carries the risk of fueling inflation if not carefully managed. By understanding the interplay between demand and supply, and by adopting targeted, adaptive policies, policymakers can maximize the benefits of debt cancellation while minimizing its inflationary drawbacks. The key lies in striking a balance—a delicate but achievable feat with the right approach.

Does Student Loan Forgiveness Cover Graduate Degrees? Key Facts Explained

You may want to see also

Explore related products

![]()

Wealth Inequality Factor: Targeted relief may mitigate inflation by aiding lower-income households disproportionately

Targeted student debt cancellation could act as a counterbalance to inflationary pressures by addressing the wealth inequality gap. Lower-income households, often burdened by disproportionate debt-to-income ratios, allocate a larger share of their income to debt servicing. For example, a household earning $30,000 annually with $20,000 in student debt spends roughly 20% of its income on loan payments, compared to a $100,000-earning household with the same debt, which spends only 8%. Canceling debt for these lower-income borrowers frees up disposable income, which is more likely to be spent on essential goods and services, stimulating demand in sectors less prone to inflationary spikes, such as groceries or utilities.

Analyzing the mechanics reveals a nuanced relationship between debt relief and inflation. While broad-based cancellation might inject excess liquidity into the economy, targeted relief focuses on households with higher marginal propensities to consume. These households, often in the bottom 40% of income distribution, spend nearly all additional income on immediate needs rather than saving or investing in assets. This spending pattern can boost aggregate demand in non-discretionary sectors, which are less sensitive to price increases, thereby mitigating inflationary pressures compared to untargeted stimulus measures.

A comparative perspective highlights the inefficiency of untargeted policies. For instance, the 2021 stimulus checks led to a surge in durable goods purchases, contributing to supply chain bottlenecks and price hikes. In contrast, targeted debt cancellation for lower-income borrowers redirects funds toward sectors with stable pricing dynamics, such as food and healthcare. This approach not only alleviates financial strain on vulnerable households but also avoids exacerbating inflation in volatile markets like housing or electronics.

To implement this strategy effectively, policymakers should cap eligibility based on income thresholds, such as households earning below $50,000 annually, and debt-to-income ratios exceeding 1.5. Additionally, pairing debt relief with financial literacy programs can ensure funds are allocated to essential expenses rather than discretionary spending. By focusing on these specifics, targeted relief can serve as a dual-purpose tool: reducing wealth inequality while minimizing inflationary risks through strategic demand stimulation.

Obama Loan Forgiveness: Did Students Receive Reimbursement?

You may want to see also

Explore related products

![]()

Long-Term Economic Effects: Debt cancellation could stimulate growth, but risks overheating the economy

Student debt cancellation has the potential to inject billions of dollars into the economy as borrowers redirect funds from loan payments to consumption or savings. This immediate boost in disposable income could stimulate economic growth, particularly in sectors like retail, housing, and small businesses. For instance, a borrower saving $300 monthly could instead spend it on goods or services, creating a ripple effect of increased demand and production. However, this surge in spending must be carefully managed to avoid overheating the economy, where excessive demand outpaces supply, driving up prices and potentially triggering inflation.

To understand the risks, consider the concept of the "multiplier effect." Every dollar spent by a borrower can generate additional economic activity as businesses reinvest profits, hire more workers, and expand operations. While this is beneficial in a sluggish economy, it becomes problematic when the economy is already near full capacity. For example, if unemployment is low and production resources are fully utilized, increased spending from debt cancellation could lead to bottlenecks, causing prices to rise. Historical examples, such as post-war economic booms, show that rapid increases in demand without corresponding supply growth often result in inflationary pressures.

Mitigating these risks requires a strategic approach. Policymakers could pair debt cancellation with measures to expand supply, such as investing in education, infrastructure, or technology to increase productivity. Additionally, phased implementation—canceling debt in smaller, staggered amounts over time—could prevent a sudden spike in demand. For instance, canceling $10,000 per borrower annually over five years would spread out the economic impact, allowing the supply side to adjust gradually. This approach balances growth stimulation with inflation control, ensuring long-term economic stability.

Critics argue that debt cancellation could disproportionately benefit higher-income individuals, who hold a larger share of student debt, potentially exacerbating inequality. However, targeted cancellation—focusing on low- and middle-income borrowers—could address this concern while still boosting aggregate demand. For example, limiting cancellation to borrowers earning below $75,000 annually would direct funds to those most likely to spend them immediately, maximizing the stimulative effect. Combining such targeting with broader economic policies ensures that debt cancellation fosters inclusive growth without overheating the economy.

In conclusion, while student debt cancellation offers a powerful tool for stimulating economic growth, its implementation must be thoughtful and strategic. By understanding the interplay between demand and supply, policymakers can harness its benefits while minimizing inflationary risks. Practical steps, such as phased implementation and targeted cancellation, provide a roadmap for achieving long-term economic prosperity without destabilizing the economy. This balanced approach ensures that debt cancellation serves as a catalyst for growth rather than a source of economic strain.

Do Mail Carriers Qualify for Federal Student Loan Forgiveness?

You may want to see also

Frequently asked questions

Canceling student debt could have a modest inflationary effect if it increases consumer spending, as borrowers with reduced debt may have more disposable income. However, the impact would depend on the size of the cancellation and how quickly borrowers adjust their spending habits.

The inflationary impact is likely to be small relative to other economic factors. Studies suggest that canceling student debt would increase consumer spending gradually, spreading the effect over time and minimizing a sharp inflationary spike.

Long-term inflation from student debt cancellation is unlikely unless it leads to unsustainable increases in demand or is paired with other inflationary policies. The effect would depend on broader economic conditions and how the cancellation is funded.

Some argue that canceling student debt could reduce inflation by freeing up income for other investments, such as starting businesses or buying homes, which could boost economic productivity. However, this effect is uncertain and would take time to materialize.