The topic of student loan forgiveness has been a contentious issue in American politics, with millions of borrowers eagerly awaiting a resolution. As the burden of student debt continues to weigh heavily on individuals and the economy, the question of whether Congress will vote on a comprehensive forgiveness plan remains a pressing concern. With various proposals and debates circulating, borrowers are left wondering if and when they might receive relief, making the potential congressional vote a highly anticipated event with significant implications for the future of higher education financing.

| Characteristics | Values |

|---|---|

| Current Status | No active legislation in Congress for broad student loan forgiveness. |

| Biden Administration's Efforts | Executive actions (e.g., targeted forgiveness, payment pauses) instead of congressional votes. |

| Legislative Proposals | Past proposals (e.g., $10,000 forgiveness) stalled due to partisan divide. |

| Political Obstacles | Republican opposition, filibuster in Senate, and legal challenges. |

| Public Opinion | Mixed support, with Democrats more likely to favor forgiveness. |

| Legal Challenges | Supreme Court struck down Biden's 2022 mass forgiveness plan in 2023. |

| Alternative Actions | Focus on income-driven repayment plans, Public Service Loan Forgiveness (PSLF), and targeted relief. |

| Future Outlook | Unlikely for broad forgiveness without significant political shifts. |

Explore related products

What You'll Learn

- Eligibility Criteria: Who qualifies for forgiveness under proposed legislation

- Loan Amount Limits: What maximum forgiveness amounts are being considered

- Funding Sources: How will the government pay for loan forgiveness

- Bipartisan Support: Is there enough cross-party agreement to pass a bill

- Timeline for Action: When might Congress vote on forgiveness legislation

![]()

Eligibility Criteria: Who qualifies for forgiveness under proposed legislation?

The eligibility criteria for student loan forgiveness under proposed legislation are a critical aspect of any potential congressional vote, as they determine who benefits and how much relief they receive. While specifics vary across proposals, common themes emerge, focusing on income thresholds, loan types, and repayment histories. For instance, many plans target borrowers earning below a certain income level, such as $125,000 for individuals or $250,000 for married couples, to ensure relief reaches those most in need. Federal loans, including Direct Loans and FFEL Loans, typically qualify, while private loans are often excluded, reflecting the government’s direct oversight of these programs.

Analyzing these criteria reveals a deliberate effort to balance equity and fiscal responsibility. Proposals frequently prioritize borrowers enrolled in income-driven repayment (IDR) plans, which tie monthly payments to earnings, or those with loans outstanding for over a decade, acknowledging the long-term financial strain of student debt. For example, some plans forgive up to $10,000 for eligible borrowers, with an additional $10,000 for Pell Grant recipients, a targeted approach to aid low-income students disproportionately burdened by debt. However, these thresholds are not arbitrary; they reflect data on median incomes and debt-to-income ratios, ensuring relief is both impactful and sustainable.

To navigate these criteria effectively, borrowers should take proactive steps. First, verify loan types through the National Student Loan Data System (NSLDS), as only federal loans qualify under most proposals. Second, update income information with loan servicers to ensure alignment with eligibility thresholds. For those in IDR plans, recertify income annually to maintain eligibility for both the plan and potential forgiveness. Lastly, stay informed about legislative updates, as eligibility criteria can shift with political negotiations. Practical tools like loan simulators can estimate forgiveness amounts based on current proposals, helping borrowers plan financially.

Comparatively, eligibility criteria in student loan forgiveness proposals differ significantly from those in existing programs like Public Service Loan Forgiveness (PSLF). While PSLF requires 120 qualifying payments and full-time employment in public service, broader forgiveness plans often focus on income and loan tenure, making them accessible to a wider population. This expansion reflects a shift from rewarding specific careers to addressing systemic issues in higher education financing. However, critics argue that overly broad criteria could dilute the impact on those most in need, underscoring the need for careful design and targeted implementation.

In conclusion, understanding eligibility criteria is essential for borrowers anticipating student loan forgiveness. By focusing on income thresholds, loan types, and repayment histories, proposed legislation aims to provide relief to those most burdened by debt. Practical steps, such as verifying loan types and staying informed, can help borrowers maximize their chances of qualifying. While the criteria differ from existing programs, they represent a broader effort to address the student debt crisis, balancing equity and fiscal responsibility in a way that could reshape the financial futures of millions.

Can Today's College Students Get Loan Forgiveness? What to Know

You may want to see also

Explore related products

![]()

Loan Amount Limits: What maximum forgiveness amounts are being considered?

The debate over student loan forgiveness has sparked intense discussions about equity, affordability, and fiscal responsibility. One critical aspect of these conversations is the question of loan amount limits: how much debt should be forgiven, and for whom? As Congress weighs its options, several proposals have emerged, each with distinct implications for borrowers and taxpayers. Understanding these limits requires examining both the political landscape and the practical realities of student debt.

Consider the Biden administration’s initial proposal, which suggested forgiving up to $10,000 in federal student loans for eligible borrowers, with an additional $10,000 for those who received Pell Grants. This tiered approach aimed to target relief toward lower-income individuals, acknowledging that Pell Grant recipients often face greater financial hardship. However, critics argue that a $10,000 cap is insufficient for borrowers with six-figure debt, particularly those with advanced degrees or those who attended high-cost institutions. This proposal highlights the tension between broad-based relief and targeted assistance, a dilemma Congress must navigate.

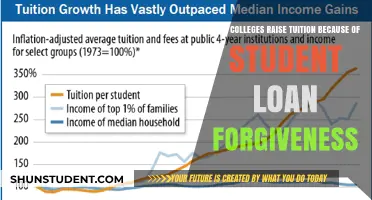

Another perspective emerges when comparing U.S. proposals to international models. In countries like Germany and Norway, tuition is free or heavily subsidized, eliminating the need for large-scale forgiveness programs. By contrast, the U.S. system relies on loans, creating a backlog of debt that now exceeds $1.7 trillion. If Congress were to adopt a higher forgiveness cap—say, $50,000—it could provide substantial relief to millions but would come with a steep price tag, estimated at over $1 trillion. Such a move would require careful consideration of funding sources, potentially including tax increases or budget reallocations.

Practical tips for borrowers awaiting a decision include staying informed about legislative updates and preparing financially for various outcomes. For instance, if a $20,000 forgiveness cap is enacted, borrowers with higher balances should explore income-driven repayment plans or refinancing options to manage remaining debt. Additionally, tracking public sentiment and advocacy efforts can provide insights into which proposals are gaining traction. Websites like the Department of Education’s Federal Student Aid portal offer resources to help borrowers understand their options.

Ultimately, the question of loan amount limits is not just about numbers but about values. Does forgiveness aim to provide a fresh start for all borrowers, or is it a tool for addressing systemic inequalities? Congress’s decision will shape the financial futures of millions, making it imperative to balance ambition with feasibility. As the debate continues, borrowers must remain engaged, advocating for solutions that reflect both their needs and the broader societal impact.

Stafford Loan Forgiveness: Eligibility and Options Explained

You may want to see also

Explore related products

![]()

Funding Sources: How will the government pay for loan forgiveness?

The Biden administration's student loan forgiveness plan, which promises to cancel up to $20,000 in debt for eligible borrowers, has sparked intense debate about its funding sources. With an estimated cost of $400 billion over 30 years, the question of how the government will foot the bill is a critical aspect of the policy's feasibility and long-term impact. The answer lies in a combination of reallocated funds, tax revenue adjustments, and potential economic growth spurred by debt relief.

One proposed funding mechanism involves redirecting money from the Federal Reserve's excess reserves. The Fed, which has accumulated substantial profits from its bond holdings, could transfer a portion of these funds to the Treasury Department. This approach, however, is not without controversy, as it raises concerns about central bank independence and the potential for inflationary pressures. Critics argue that using the Fed's reserves in this manner could undermine its ability to manage monetary policy effectively.

Another strategy is to increase tax revenues by targeting high-income earners and corporations. For instance, implementing a minimum tax rate for large corporations or closing loopholes that benefit the wealthy could generate significant income. Historical data shows that the 1986 Tax Reform Act, which simplified the tax code and broadened the tax base, led to a 9% increase in revenue within the first year. Applying similar principles could help offset the cost of loan forgiveness while addressing income inequality.

A third consideration is the potential economic stimulus that debt relief could provide. Studies suggest that canceling student loans could boost consumer spending, as borrowers would have more disposable income. For example, a 2021 Roosevelt Institute report estimated that canceling $1.4 trillion in student debt could increase GDP by $86 billion to $108 billion annually over the next decade. This growth could, in turn, generate additional tax revenue, partially offsetting the initial cost of the program.

However, relying solely on economic growth is risky, as projections are inherently uncertain. Policymakers must also consider the trade-offs involved, such as the opportunity cost of allocating funds to loan forgiveness rather than other pressing needs like infrastructure or healthcare. Balancing these priorities requires a comprehensive fiscal strategy that ensures long-term sustainability without exacerbating the national debt.

In conclusion, funding student loan forgiveness demands a multifaceted approach that combines reallocated resources, tax reforms, and strategic economic planning. While each option presents challenges, a well-designed policy can mitigate risks and maximize benefits. As Congress deliberates, the key will be to strike a balance that addresses both the immediate needs of borrowers and the broader fiscal health of the nation.

Forgiven Student Loans and Taxes: What You Need to Know

You may want to see also

Explore related products

![]()

Bipartisan Support: Is there enough cross-party agreement to pass a bill?

Student loan forgiveness has become a polarizing issue, with Democrats generally advocating for broad relief and Republicans often expressing skepticism about its fiscal responsibility. However, amidst this divide, certain bipartisan efforts have emerged, suggesting pockets of agreement. For instance, both parties have shown support for targeted forgiveness programs, such as those for public servants or borrowers defrauded by predatory institutions. These examples demonstrate that while comprehensive forgiveness remains contentious, narrower initiatives could garner cross-party backing.

To assess whether there’s enough bipartisan support to pass a bill, consider the legislative process itself. A bill requires 60 votes in the Senate to overcome a filibuster, meaning at least 10 Republicans must join Democrats. Historically, Republicans have opposed large-scale forgiveness, citing concerns about cost and fairness. However, some GOP lawmakers have supported measures like simplifying income-driven repayment plans or expanding Pell Grants, indicating potential areas of compromise. Crafting a bill that addresses these shared priorities could be key to securing the necessary votes.

Persuasion plays a critical role in building bipartisan support. Advocates must frame forgiveness not as a giveaway but as an investment in economic stability. Highlighting data that shows debt relief boosts consumer spending, reduces defaults, and stimulates local economies could appeal to Republicans focused on fiscal growth. Additionally, emphasizing fairness—such as targeting relief to low-income borrowers or those with high debt-to-income ratios—could address GOP concerns about equity. Tailoring the message to align with both parties’ values is essential for fostering agreement.

Comparing student loan forgiveness to other bipartisan successes provides insight. For example, the 2019 passage of the FUTURE Act, which streamlined the FAFSA process, demonstrates that education-related reforms can unite both parties when focused on administrative efficiency and accessibility. Similarly, a forgiveness bill that pairs debt relief with reforms to prevent future borrowing crises—such as capping interest rates or holding colleges accountable for tuition hikes—could attract Republican support. Lessons from these successes suggest that bundling relief with systemic fixes is a viable strategy.

In conclusion, while broad student loan forgiveness faces significant partisan hurdles, targeted initiatives with bipartisan appeal are within reach. By focusing on shared goals like economic growth, fairness, and systemic reform, lawmakers can craft a bill that bridges the divide. Practical steps include prioritizing public service forgiveness, simplifying repayment plans, and pairing relief with accountability measures. With strategic messaging and compromise, Congress could find the common ground needed to pass meaningful legislation.

How to Check Your Student Loan Forgiveness Status: A Quick Guide

You may want to see also

Explore related products

![]()

Timeline for Action: When might Congress vote on forgiveness legislation?

The fate of student loan forgiveness legislation hinges on a complex interplay of political priorities, legislative schedules, and external pressures. While no concrete timeline exists, analyzing congressional rhythms offers clues. Historically, major policy votes cluster around election years, when lawmakers seek to deliver on campaign promises. With the 2024 election looming, the window for action narrows. Expect heightened debate in the first half of 2024, as legislators jockey for position and seek to appeal to voter concerns about education costs.

Several factors could accelerate or delay a vote. A worsening economic outlook might spur urgency, framing forgiveness as a stimulus measure. Conversely, a strong economy could dampen enthusiasm, as lawmakers prioritize other issues. Keep an eye on key committee hearings and markups – these procedural steps are necessary precursors to a full floor vote. The House Education and Workforce Committee and the Senate Health, Education, Labor, and Pensions Committee will be ground zero for drafting and debating any forgiveness bill.

Tracking these committees' schedules provides a real-time pulse on legislative momentum.

Don't underestimate the power of public pressure. Grassroots movements and advocacy campaigns can significantly influence the timeline. A surge in public support, fueled by organized protests, social media campaigns, and targeted lobbying, could force congressional leadership to prioritize forgiveness legislation. Conversely, apathy or division among borrowers could allow other issues to dominate the agenda. Remember, lawmakers are responsive to constituent concerns – make your voice heard through calls, emails, and meetings with representatives.

Ultimately, the timeline for a vote on student loan forgiveness is fluid, shaped by a dynamic interplay of political, economic, and social forces. Stay informed, stay engaged, and be prepared to act when the moment arises.

Can Chase Bank Forgive Your Student Loans? Exploring Options and Myths

You may want to see also

Frequently asked questions

As of now, there is no confirmed schedule for Congress to vote on student loan forgiveness in 2023. Legislative priorities can shift, and any potential vote would depend on bipartisan support or executive actions.

No, Congress cannot pass a student loan forgiveness bill without the President’s approval. The President must sign the bill into law, or Congress would need a two-thirds majority in both chambers to override a presidential veto.

As of the latest updates, there are no active bipartisan proposals in Congress for widespread student loan forgiveness. However, individual lawmakers have introduced bills targeting specific groups or loan amounts.

Congress has the authority to pass legislation that could cancel student loan debt, but it would require bipartisan support or a presidential signature. Alternatively, the Department of Education can implement targeted forgiveness through executive actions under existing laws.