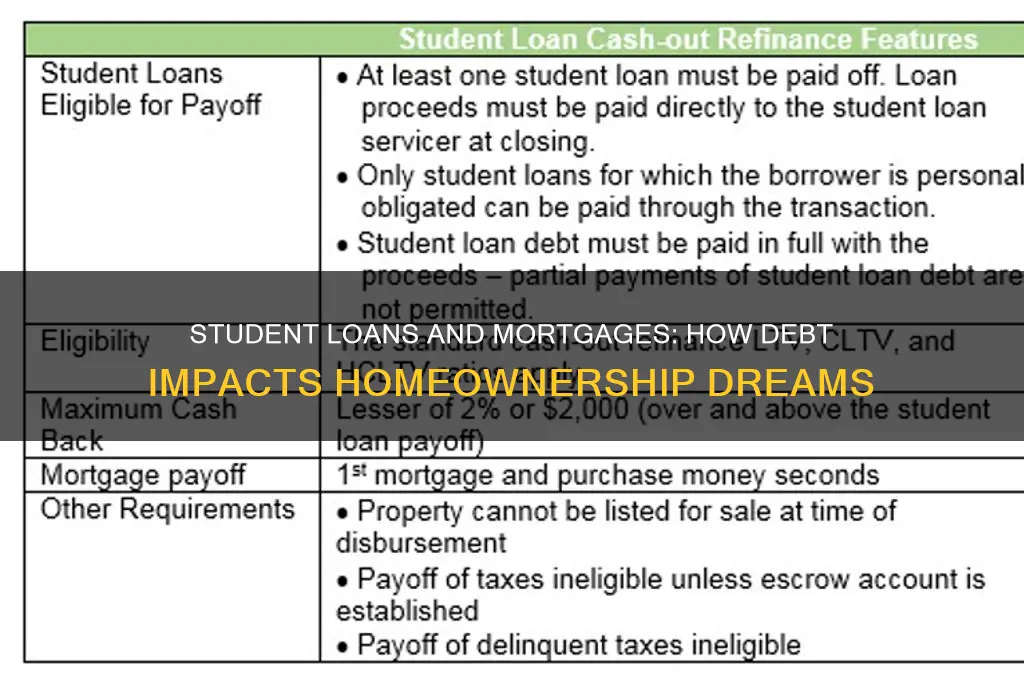

Navigating the intersection of student loans and mortgage eligibility can be complex for many individuals. Student loans, being a significant financial commitment, can impact a borrower’s debt-to-income ratio, credit score, and overall financial health, all of which are critical factors lenders consider when approving a mortgage. While having student loans does not automatically disqualify someone from obtaining a mortgage, it can influence the terms and interest rates offered. Lenders assess how well borrowers manage their existing debt, including student loans, to gauge their ability to take on additional financial responsibilities. Understanding how student loans affect mortgage eligibility requires a careful examination of one’s financial situation, including payment history, loan balances, and strategies to minimize debt burden. By proactively managing student loans and maintaining a strong credit profile, borrowers can improve their chances of securing a mortgage on favorable terms.

Explore related products

What You'll Learn

![]()

Debt-to-Income Ratio Impact

Your debt-to-income ratio (DTI) is a critical metric lenders use to assess your mortgage eligibility, and student loans can significantly skew this balance. This ratio compares your monthly debt payments to your gross monthly income, expressed as a percentage. For instance, if your monthly student loan payment is $300, credit card minimums total $100, and your income is $4,000, your DTI is 10% (($300 + $100) / $4,000). Lenders typically prefer a DTI below 36%, though some may accept up to 43% for qualified borrowers. Student loans, especially those with high balances or long repayment terms, can inflate this ratio, potentially disqualifying you from certain mortgage programs or increasing your interest rate.

Consider the scenario of a recent graduate with $50,000 in student debt on a standard 10-year repayment plan. Their monthly payment might be around $500. If their income is $5,000 monthly, this single debt alone pushes their DTI to 10%. Add other obligations like a car loan or credit card debt, and the ratio climbs further. Lenders view a higher DTI as a risk indicator, as it suggests less disposable income to handle mortgage payments. To mitigate this, borrowers can explore income-driven repayment plans, which lower monthly payments by extending the loan term, thereby reducing the immediate DTI impact. However, this strategy increases total interest paid over time, so it’s a trade-off.

Another practical tip is to aggressively pay down student loans before applying for a mortgage. Even reducing the balance by $5,000 can lower monthly payments, improving your DTI. For example, paying off $5,000 of a $50,000 loan could reduce the monthly payment from $500 to $475, depending on the interest rate. Additionally, borrowers can increase their income through side gigs or salary negotiations to offset the DTI ratio. Lenders only consider verifiable, consistent income, so ensure any extra earnings are documented for at least two years.

It’s also worth noting that not all student loans are treated equally in DTI calculations. Deferred loans, for instance, may be excluded if they’re in a grace period and won’t come due within 12 months of closing. However, loans in forbearance or income-driven plans are typically factored in based on the actual payment amount, not the standard repayment figure. Understanding these nuances can help borrowers strategize their loan management to optimize their DTI.

Ultimately, while student loans can complicate mortgage approval, proactive management of your DTI can make a significant difference. By reducing debt, increasing income, or restructuring repayment plans, borrowers can position themselves as lower-risk candidates. Remember, lenders don’t just look at the total debt—they assess your ability to manage it alongside a mortgage. A well-planned approach to your DTI can turn a potential obstacle into a manageable step toward homeownership.

Mastering Learning Outcomes: What Students Truly Grasp and Retain

You may want to see also

Explore related products

![NMLS Study Cards: NMLS MLO Test Prep 2025-2026 for the SAFE Mortgage Loan Originator Exam with Practice Test Questions [Full Color Cards]](https://m.media-amazon.com/images/I/61f1NUOp4iL._AC_UY218_.jpg)

![]()

Credit Score Considerations

Your credit score is a numerical snapshot of your financial trustworthiness, and it plays a pivotal role in mortgage approval. Lenders scrutinize this three-digit number to gauge your ability to manage debt responsibly. Student loans, being a significant financial commitment, can either bolster or hinder your credit score depending on how you handle them. Timely payments on your student loans demonstrate reliability, gradually elevating your score. Conversely, missed or late payments can tarnish your credit history, making lenders wary of extending a mortgage. Understanding this dynamic is crucial for anyone navigating the intersection of student debt and homeownership.

Consider the mechanics of credit utilization, a key factor in your credit score. If your student loans are your only form of credit, they heavily influence your credit mix and utilization rate. Aim to keep your overall credit utilization below 30%, as exceeding this threshold can signal financial strain. For instance, if you have a $10,000 credit limit across all accounts and your student loan payments push your utilization to 40%, it may negatively impact your score. Pairing student loans with a credit card used sparingly and paid off monthly can diversify your credit profile and improve your score over time.

Another critical aspect is the length of your credit history. Student loans often span a decade or more, providing a long-term record of financial behavior. Closing other credit accounts while paying off student loans can shorten your credit history, inadvertently lowering your score. To counteract this, keep older accounts open, even if you’re not actively using them. For example, a credit card opened during college can contribute positively to your credit age, provided it’s managed responsibly. This strategy ensures your credit history remains robust while tackling student debt.

Disputing inaccuracies on your credit report is a proactive step often overlooked. Errors, such as misreported payment statuses or incorrect loan amounts, can unfairly depress your score. Regularly review your credit reports from the three major bureaus—Equifax, Experian, and TransUnion—and dispute any discrepancies. For instance, if a student loan payment is marked late despite being paid on time, gather proof and file a dispute. Resolving such issues can yield a quick and significant boost to your credit score, enhancing your mortgage eligibility.

Finally, consider the impact of refinancing student loans on your credit score. Refinancing can lower your interest rate or monthly payments, making debt management easier. However, it involves a hard credit inquiry, which temporarily reduces your score by a few points. Weigh the long-term benefits against the short-term dip. For example, if refinancing saves you $200 monthly, the minor credit score reduction may be a worthwhile trade-off. Strategic refinancing, coupled with consistent financial habits, can position you as a strong mortgage candidate despite carrying student debt.

Can Co-Partnership Affect Your Student Loan Repayment Process?

You may want to see also

Explore related products

![]()

Loan Repayment Plans

Student loans can significantly impact your ability to secure a mortgage, but the effect largely depends on how you manage your repayment plan. Lenders scrutinize your debt-to-income ratio (DTI), and a high monthly student loan payment can reduce your borrowing power. However, strategic repayment plans can mitigate this. Income-driven repayment (IDR) plans, for example, cap monthly payments at a percentage of your discretionary income, often lowering your DTI and improving mortgage eligibility. Conversely, standard 10-year plans result in higher monthly payments, which may disqualify you from certain loan amounts. Understanding these nuances is crucial for aligning your student loan strategy with your homeownership goals.

Consider the Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE) plans, which limit payments to 10% of discretionary income. These plans can drastically reduce your monthly obligation, making your financial profile more attractive to mortgage lenders. For instance, a borrower earning $50,000 annually with $30,000 in student loans might see payments drop from $300 on a standard plan to $150 on PAYE. This $150 difference could mean qualifying for a larger mortgage. However, these plans often extend repayment terms and may result in capitalized interest, so weigh the long-term costs against immediate mortgage benefits.

If you’re closer to paying off your loans, refinancing could be a better option. Refinancing replaces your existing loans with a private loan at a lower interest rate, potentially reducing both your monthly payment and total repayment amount. For example, refinancing a $40,000 loan from 7% to 4% could save you $50–$100 monthly. This strategy works best for borrowers with stable incomes and good credit scores. However, refinancing federal loans eliminates access to IDR plans and forgiveness programs, so proceed cautiously if job security or public service loan forgiveness is a priority.

For those with multiple loans, consolidation can simplify repayment and lower monthly payments by extending the loan term. Federal Direct Consolidation combines eligible loans into one with a weighted average interest rate, rounded to the nearest eighth of a percent. While this won’t lower your rate significantly, it can reduce payments by stretching the term up to 30 years. For instance, consolidating $50,000 in loans from 10 to 20 years could cut monthly payments in half. However, longer terms mean more interest paid over time, so this strategy is best for borrowers prioritizing short-term cash flow over long-term savings.

Finally, lump-sum payments or aggressive repayment can eliminate student loans faster, freeing up income for mortgage payments. If you have access to extra funds—say, from a bonus or inheritance—applying them to high-interest loans can reduce your DTI quickly. For example, paying off $10,000 of a $30,000 loan at 6% interest could lower your monthly payment by $100. This approach requires discipline and financial flexibility but offers the dual benefit of improving mortgage eligibility and reducing long-term debt burden. Pairing this strategy with a side hustle or budget cuts can accelerate results.

In summary, loan repayment plans are not one-size-fits-all. Income-driven plans offer immediate relief but may extend debt, refinancing provides lower rates at the cost of federal benefits, consolidation simplifies payments but increases interest, and aggressive repayment demands upfront resources. Tailor your approach to your financial situation and homeownership timeline, ensuring your student loan strategy aligns with your mortgage goals.

Empowering Students with Learning Disabilities: Strategies for Inclusive Education

You may want to see also

Explore related products

![]()

Down Payment Challenges

Saving for a down payment is a monumental task for any prospective homebuyer, but for those burdened with student loans, it’s akin to climbing a mountain with a backpack full of bricks. Every dollar allocated to loan repayment is a dollar that can’t be stashed away for a future home. Consider this: the average student loan payment hovers around $400 per month. Over five years, that’s $24,000—a significant chunk of a 20% down payment on a median-priced home. The math is unforgiving, and the psychological toll of watching savings trickle away to debt rather than equity can be demoralizing.

Let’s break it down practically. Suppose you’re a 28-year-old earning $60,000 annually with $30,000 in student debt at 6% interest. Using the 50/30/20 budget rule, you’re already allocating $1,000 monthly to necessities, $600 to discretionary spending, and $1,200 to savings and debt repayment. If $400 of that $1,200 goes to student loans, you’re left with $800 for savings. At this rate, it would take nearly 10 years to save $100,000—a common down payment goal for a $500,000 home. But here’s the kicker: housing prices rise faster than savings accounts grow, often outpacing inflation by 3-5% annually. The longer you wait, the more distant the dream becomes.

Now, let’s pivot to strategy. One underutilized approach is leveraging employer-sponsored programs or government assistance. For instance, the Public Service Loan Forgiveness (PSLF) program can eliminate student debt after 10 years of qualifying payments, freeing up funds for a down payment. Similarly, first-time homebuyer grants or low-down-payment mortgages (e.g., FHA loans requiring as little as 3.5% down) can accelerate the process. However, these options come with trade-offs: FHA loans require mortgage insurance, and PSLF demands a decade of commitment to a qualifying employer. Weighing these pros and cons is critical, as the wrong choice could saddle you with higher long-term costs.

Finally, consider the emotional and behavioral hurdles. Student loan debt fosters a scarcity mindset, making it difficult to envision a future where homeownership is possible. This mindset often leads to paralysis—endless scrolling through Zillow, but no actionable steps. To combat this, reframe the challenge as a marathon, not a sprint. Start with micro-goals: save $500 in three months, then $1,000 in six. Celebrate small victories, like paying off a single loan or hitting a savings milestone. Pair this with a side hustle or skill monetization—freelancing, tutoring, or selling unused items—to accelerate progress. The key is consistency, not perfection. Every dollar saved is a step closer to turning the key in your own front door.

Understanding Income Eligibility for Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Lender Policies on Debt

Lenders scrutinize your debt-to-income ratio (DTI) as a key metric when evaluating mortgage applications. This ratio compares your monthly debt payments to your gross monthly income. For instance, if your monthly student loan payment is $300, credit card payments total $200, and your income is $5,000, your DTI is 10% (calculated as $500 / $5,000). Most lenders prefer a DTI below 36%, though some may accept up to 43% for qualified borrowers. Student loans, being long-term debt, directly impact this ratio, potentially limiting the mortgage amount you qualify for or increasing your interest rate.

Not all student loans are treated equally in lender calculations. Deferred or income-driven repayment plans can complicate matters. Some lenders use 1% of the total student loan balance as a placeholder monthly payment if payments are currently deferred. Others may use the actual payment amount reported on your credit, even if it’s lower due to an income-driven plan. For example, if your $50,000 student loan balance would require a $500 monthly payment under standard terms but your income-driven plan reduces it to $100, some lenders might still factor in the $500, significantly inflating your DTI.

To mitigate the impact of student loans on your mortgage application, consider strategies like refinancing to lower monthly payments or paying down high-interest debt to reduce your DTI. If you’re on an income-driven repayment plan, provide documentation to lenders showing your actual monthly payment, as this could result in a more favorable DTI calculation. Additionally, increasing your income through side gigs or requesting a raise can improve your ratio. For instance, boosting your income from $5,000 to $6,000 while keeping debt payments at $500 lowers your DTI from 10% to 8.3%, making you a stronger candidate.

Lender policies vary widely, so shopping around is crucial. Some lenders specialize in working with borrowers carrying significant student debt, offering more flexible DTI thresholds or alternative underwriting methods. Credit unions, for example, may be more lenient than traditional banks. Similarly, government-backed loans like FHA or VA mortgages often have more forgiving debt requirements compared to conventional loans. Understanding these differences and tailoring your application to the right lender can make the difference between approval and denial.

Unlocking Debt-Free Futures: Jobs Qualifying for Federal Student Loan Forgiveness

You may want to see also

Frequently asked questions

No, having student loans does not automatically disqualify you from getting a mortgage. Lenders consider your overall financial health, including your credit score, debt-to-income ratio (DTI), and payment history.

Student loans increase your monthly debt obligations, which raises your debt-to-income ratio (DTI). Lenders typically prefer a DTI below 43%, so high student loan payments may limit the mortgage amount you qualify for.

Yes, you can still get a mortgage if your student loans are in deferment or forbearance. However, lenders may still factor in the potential future payments when calculating your DTI, depending on the loan type and lender guidelines.

Yes, your credit score can be affected by student loans. Timely payments improve your score, while missed or late payments can lower it. A higher credit score increases your chances of mortgage approval and better interest rates.

Qualifying for a mortgage with high student loan debt is possible but may be challenging. Lenders will assess your ability to manage both debts. Strategies like increasing income, reducing other debts, or exploring loan assistance programs can improve your chances.