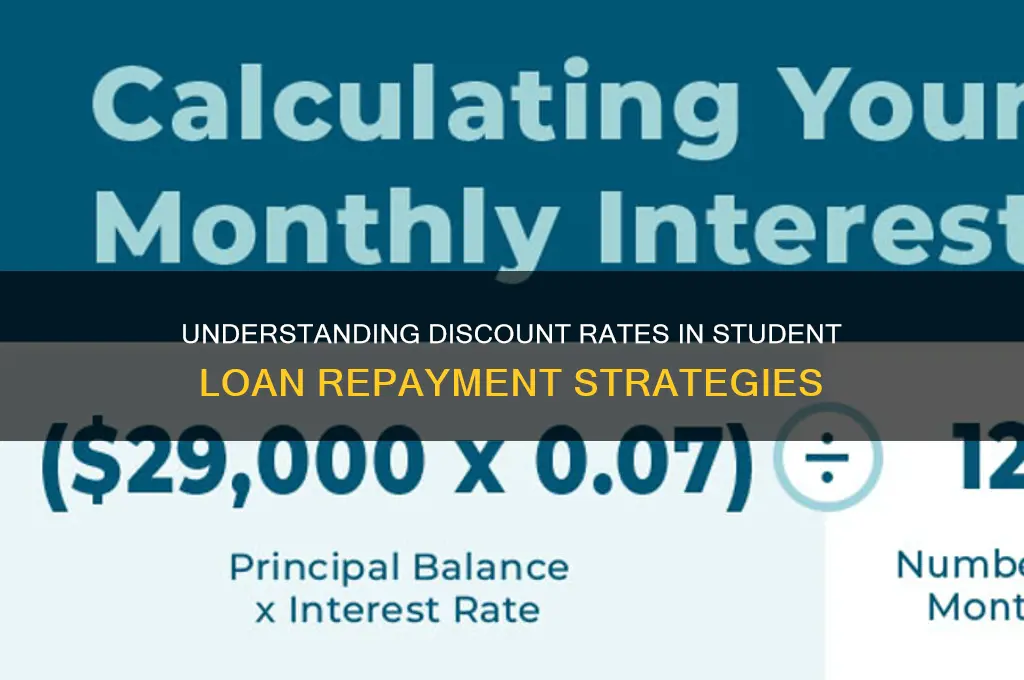

Student loans, a critical financial tool for many pursuing higher education, often involve complex calculations to determine their long-term cost and value. One key concept in this analysis is the discount rate, which is used to estimate the present value of future loan payments. The discount rate reflects the time value of money, accounting for factors such as inflation, interest rates, and opportunity costs. When considering whether student loans utilize a discount rate, it’s important to understand that lenders and borrowers alike rely on this metric to assess the loan’s affordability and return on investment in education. For borrowers, a higher discount rate can make future payments appear less burdensome in present terms, while for lenders, it helps in pricing loans to ensure profitability. Thus, the discount rate plays a pivotal role in shaping the economics of student loans and the decisions surrounding them.

Explore related products

What You'll Learn

![]()

Understanding Discount Rate in Student Loans

The concept of a discount rate is an essential aspect of finance, and its application in the context of student loans is worth exploring. When considering whether student loans utilize a discount rate, it's important to understand the role this financial mechanism plays. In simple terms, a discount rate is the interest rate used to calculate the present value of future cash flows. In the realm of student loans, this concept becomes particularly relevant when assessing the long-term financial implications for borrowers.

In the United States, the federal student loan system often employs a discount rate to determine the present value of future loan repayments. This is especially true for income-driven repayment plans, where the borrower's monthly payments are adjusted based on their income and family size. The discount rate, in this case, is used to estimate the current worth of those future payments, taking into account the time value of money. By applying a discount rate, lenders can assess the potential risk and value of the loan, ensuring that the repayment structure is fair and sustainable for both parties.

For borrowers, understanding the discount rate is crucial as it directly impacts the overall cost of their education. When a student takes out a loan, the discount rate influences the calculation of the loan's interest, which, in turn, affects the total amount to be repaid. A higher discount rate means that future repayments are considered less valuable in the present, potentially leading to higher interest charges. This is why it's essential for students and their families to comprehend how discount rates are applied and how they can impact the long-term financial commitment of a student loan.

Furthermore, the use of discount rates in student loans can also be seen in the context of loan consolidation or refinancing. When borrowers opt to consolidate multiple loans or refinance their existing loan, financial institutions may use a discount rate to determine the new loan's terms. This process involves assessing the present value of the remaining repayments on the original loan(s) and then offering a new loan with potentially more favorable terms. Borrowers should be aware that the discount rate applied in such scenarios can significantly impact the overall savings or benefits of consolidating or refinancing their student debt.

In summary, the discount rate is a critical component in the financial structure of student loans. It allows lenders to evaluate the present value of future repayments, ensuring a balanced approach to lending. For borrowers, understanding this concept is key to making informed decisions about their education financing. By grasping how discount rates influence interest calculations and loan terms, students can better navigate the complexities of student loans and potentially make more financially advantageous choices. This knowledge empowers borrowers to ask the right questions and seek the most suitable loan options for their unique circumstances.

Unlock Savings: Understanding Converse's Student Discount Benefits & Eligibility

You may want to see also

Explore related products

![]()

Impact of Discount Rate on Loan Repayments

The discount rate plays a crucial role in determining the present value of future loan repayments, and its impact on student loans is particularly significant. When student loans are issued, the lender must estimate the future cash flows from repayments and discount them back to the present using an appropriate discount rate. This rate reflects the time value of money and the risk associated with the loan. A higher discount rate reduces the present value of future repayments, meaning the lender may offer a smaller loan amount or charge a higher interest rate to compensate for the perceived risk. Conversely, a lower discount rate increases the present value of future repayments, potentially allowing for larger loan amounts or lower interest rates.

For borrowers, the discount rate indirectly affects the cost of their student loans. If the discount rate used by lenders is high, borrowers may face higher interest rates or more stringent repayment terms. This is because lenders need to ensure that the present value of future repayments covers their costs and provides a reasonable return on investment. In this scenario, borrowers might end up paying more over the life of the loan, increasing the overall financial burden of their education. Understanding the discount rate used by lenders can help borrowers anticipate the potential costs and plan their finances accordingly.

The choice of discount rate also influences the affordability of student loans for different demographic groups. For instance, if lenders apply a higher discount rate to loans for students from lower-income backgrounds or those pursuing degrees with uncertain job prospects, these borrowers may receive less favorable terms. This can exacerbate existing inequalities in access to education, as students from disadvantaged backgrounds may struggle to secure affordable financing. Policymakers and financial institutions must consider the social implications of discount rate selection to ensure that student loans remain accessible and equitable.

Moreover, changes in the discount rate over time can impact existing student loans, particularly those with variable interest rates. If the discount rate rises, borrowers with variable-rate loans may see their monthly repayments increase, putting additional strain on their budgets. This volatility underscores the importance of borrowers understanding the terms of their loans and considering options like fixed-rate loans or refinancing when the discount rate is low. Financial literacy and proactive management of loan terms are essential for mitigating the impact of discount rate fluctuations.

In summary, the discount rate has a profound impact on student loan repayments by shaping the present value of future cash flows, influencing borrowing costs, and affecting loan accessibility. Borrowers must be aware of how lenders determine and apply discount rates to make informed decisions about their education financing. Policymakers and lenders, on the other hand, should strive to use discount rates that balance financial sustainability with the need to support equitable access to higher education. By understanding and addressing the implications of the discount rate, all stakeholders can work toward creating a more fair and efficient student loan system.

Unlock Savings: Apple UK Student Discount Guide for Learners

You may want to see also

Explore related products

![]()

How Lenders Determine Discount Rates for Students

When determining discount rates for student loans, lenders employ a multifaceted approach that balances risk, market conditions, and regulatory guidelines. The discount rate, in this context, refers to the interest rate charged on student loans, which is influenced by several key factors. One primary consideration is the borrower’s creditworthiness. Unlike traditional loans, many student loans, especially federal ones, do not require a credit check. However, for private student loans, lenders assess the borrower’s credit history, income, and debt-to-income ratio to gauge repayment likelihood. A higher credit score or a cosigner with strong credit can lead to lower discount rates, as the lender perceives less risk.

Market conditions also play a significant role in setting discount rates for student loans. Lenders often tie their rates to benchmark indices, such as the London Interbank Offered Rate (LIBOR) or the Prime Rate. When these indices fluctuate due to economic factors like inflation or monetary policy changes, student loan rates may adjust accordingly. Additionally, competition among lenders can drive rates down, as institutions vie to attract borrowers with more favorable terms. Federal student loans, on the other hand, are typically set by Congress and are less susceptible to market volatility, offering fixed rates that remain consistent over the life of the loan.

Another critical factor is the type of student loan being offered. Federal student loans, such as Direct Subsidized and Unsubsidized Loans, have discount rates determined by federal legislation and are often lower than private loan rates. These rates are standardized and do not vary based on individual borrower profiles. Private lenders, however, have more flexibility in setting rates and may consider additional factors like the borrower’s field of study, school, and future earning potential. For instance, students pursuing high-income careers may qualify for lower rates compared to those in fields with lower average salaries.

Lenders also account for operational costs and profit margins when determining discount rates. Origination fees, servicing expenses, and default risks are factored into the overall rate structure. Federal loans, for example, include origination fees that are deducted from the loan amount, effectively increasing the borrower’s cost. Private lenders may waive such fees to attract borrowers but compensate by charging higher interest rates. Understanding these cost components helps borrowers evaluate the true expense of their loans beyond the advertised discount rate.

Lastly, government policies and subsidies influence discount rates for student loans. Federal loans benefit from government backing, which reduces lender risk and allows for lower rates. Programs like income-driven repayment plans or loan forgiveness further mitigate risk, enabling lenders to offer more competitive terms. Private lenders, lacking such guarantees, must price their loans to account for higher default probabilities, often resulting in higher discount rates. Borrowers should carefully compare federal and private loan options, considering both the discount rate and the long-term financial implications of each choice.

How to Apply Your Student Discount Code on Boohoo: A Quick Guide

You may want to see also

Explore related products

![]()

Discount Rate vs. Interest Rate in Student Loans

When considering student loans, it's essential to understand the difference between the discount rate and the interest rate, as these terms, though related, serve distinct purposes in the context of borrowing. The interest rate is the most familiar concept to borrowers—it represents the cost of borrowing money, expressed as a percentage of the principal loan amount. For student loans, the interest rate determines how much extra you will pay over the life of the loan. Federal student loans, for instance, have fixed interest rates set by Congress, while private loans may offer variable rates that fluctuate with market conditions. The interest rate directly impacts your monthly payments and the total amount repaid.

On the other hand, the discount rate is a less commonly discussed but equally important concept, particularly in the realm of finance and economics. The discount rate is not a fee paid by the borrower but rather a tool used by lenders, investors, or policymakers to evaluate the present value of future cash flows. In the context of student loans, a discount rate might be used by financial institutions or the government to assess the long-term value of loan repayments. For example, if a student loan is expected to be repaid over 10 years, the discount rate helps determine how much those future payments are worth in today’s dollars, accounting for factors like inflation and opportunity cost.

One key distinction is that the interest rate is directly applied to the borrower’s loan, affecting their repayment obligations, while the discount rate is an internal calculation used by lenders or policymakers to make decisions about lending and risk management. Borrowers do not pay the discount rate; instead, it influences how lenders price loans and assess their profitability. For instance, a higher discount rate might make future loan repayments appear less valuable, potentially leading to stricter lending criteria or higher interest rates for borrowers.

In the context of student loans, the question of whether a discount rate is used often arises in discussions about loan affordability and government subsidies. Federal student loans, for example, may be subsidized, meaning the government pays the interest on the loan while the borrower is in school. In such cases, the discount rate could be used to evaluate the cost of these subsidies to the government. However, for borrowers, the primary concern remains the interest rate, as it directly affects their financial burden.

Understanding the difference between these rates is crucial for borrowers navigating student loan options. While the interest rate is a tangible factor that impacts monthly payments and total repayment amounts, the discount rate operates behind the scenes, influencing lending decisions and policy. Borrowers should focus on securing the lowest possible interest rate to minimize costs, while policymakers and lenders use the discount rate to ensure the sustainability of loan programs. By grasping these distinctions, students can make more informed decisions about financing their education.

Disney Plus College Discount: Savings for Students Available?

You may want to see also

Explore related products

$10.17 $16.99

![]()

Effect of Federal Discount Rate on Student Borrowing

The Federal Discount Rate, set by the Federal Reserve, is the interest rate charged to commercial banks and other depository institutions on loans they receive from their regional Federal Reserve Bank’s lending facility. While this rate primarily influences short-term borrowing costs for financial institutions, its effects ripple through the broader economy, including the student loan market. Student loans, particularly federal student loans, are not directly tied to the Federal Discount Rate. Instead, federal student loan interest rates are set by Congress and are based on the 10-year Treasury note yield, plus a fixed markup. However, the Federal Discount Rate can indirectly impact student borrowing by influencing overall economic conditions and market interest rates.

One of the key effects of the Federal Discount Rate on student borrowing is its role in shaping the broader interest rate environment. When the Federal Reserve raises the discount rate, it often leads to higher borrowing costs across the economy, including for private student loans. Private lenders typically adjust their interest rates in response to changes in the federal funds rate and the discount rate, as these rates influence their own cost of funds. As a result, students seeking private loans may face higher interest rates when the Federal Discount Rate increases, making borrowing more expensive. This can discourage some students from taking out private loans or lead them to borrow smaller amounts.

Conversely, when the Federal Reserve lowers the discount rate, it can create a more favorable borrowing environment. Lower rates generally reduce the cost of private student loans, making them more accessible and affordable for students. However, federal student loan rates remain largely unaffected by these changes, as they are determined by legislation rather than market fluctuations. This stability in federal loan rates can provide a buffer for students during periods of rising interest rates, but it also means that federal loan rates may not decrease when the discount rate falls, limiting potential savings for borrowers.

The Federal Discount Rate also impacts student borrowing by influencing economic growth and employment. Higher discount rates can slow economic activity by increasing borrowing costs for businesses and consumers, potentially leading to reduced job opportunities and lower wages. For students, a weaker job market may increase the need for loans to cover educational expenses, as they may have less financial support from family or personal income. Conversely, a lower discount rate can stimulate economic growth, improving job prospects and potentially reducing the reliance on student loans.

In summary, while federal student loans are not directly tied to the Federal Discount Rate, changes in this rate can have significant indirect effects on student borrowing. Higher discount rates tend to increase the cost of private student loans and may exacerbate financial pressures on students in a slower economy. Lower discount rates, on the other hand, can make private loans more affordable and improve economic conditions, potentially reducing the need for borrowing. Understanding these dynamics is crucial for students and policymakers as they navigate the complexities of financing higher education in a fluctuating interest rate environment.

Spotify Student Discount: Eligibility Criteria and Application Guide

You may want to see also

Frequently asked questions

The discount rate is the interest rate used to calculate the present value of future cash flows, such as loan repayments. It reflects the time value of money and the risk associated with the loan.

Yes, lenders often use a discount rate to assess the present value of future loan repayments, which can influence the terms and interest rates offered to borrowers.

A higher discount rate typically leads to higher interest rates on student loans, as lenders account for increased risk and the time value of money when setting repayment terms.

Generally, borrowers cannot directly negotiate the discount rate, as it is determined by lenders based on market conditions, risk assessment, and federal or institutional policies. However, borrowers can shop around for loans with better terms.