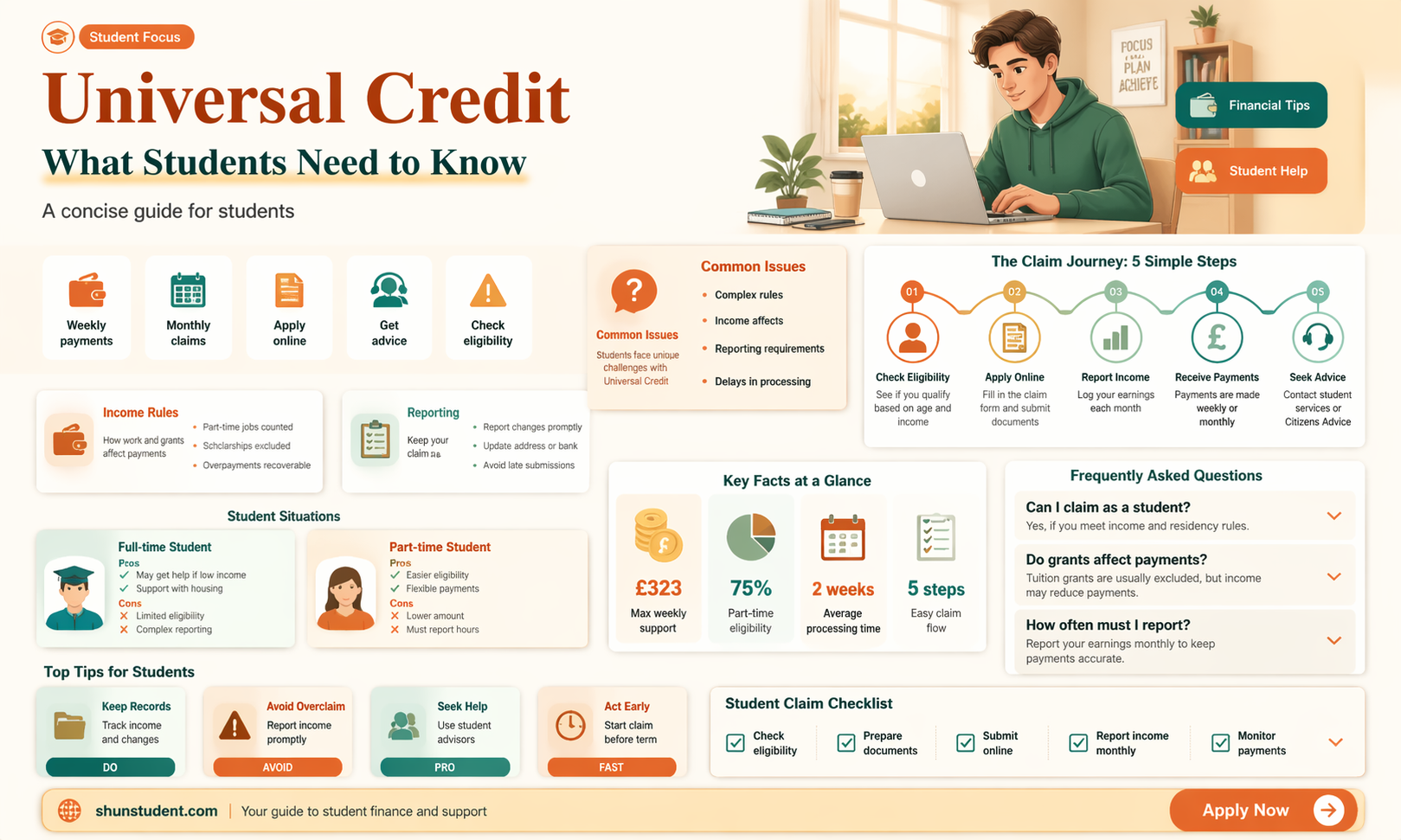

Universal Credit is a monthly payment from the government to help with living costs. You may be able to claim it if you are on a low income or need help with living costs. Usually, full-time students are not eligible for Universal Credit, but there are exceptions. For example, if you are aged 21 or under, in full-time non-advanced education, and do not have parental support, you may be eligible. Similarly, if you are a full-time student with a disability and have been assessed as having a limited capability for work, you may be eligible for Universal Credit. If you are a part-time student and available for work, you may also be eligible. The amount of Universal Credit you receive may be affected by your student income, such as loans and grants.

Am I entitled to Universal Credit as a student?

| Characteristics | Values |

|---|---|

| Full-time student | Not usually eligible for Universal Credit. |

| Full-time student with no student loan/grant | May be eligible for Universal Credit. |

| Full-time student with student loan/grant | May be eligible for Universal Credit, but student income will be taken into account. |

| Full-time student aged 21 or under | May be eligible for Universal Credit if in non-advanced education. |

| Full-time student with limited capability for work | May be eligible for Universal Credit if assessed before starting the course. |

| Full-time student with a partner | May be eligible for Universal Credit if the partner is claiming Universal Credit. |

| Full-time student with a child | May be eligible for Universal Credit. |

| Part-time student | May be eligible for Universal Credit, but must meet other requirements. |

| Low income | May be eligible for Universal Credit. |

| Seeking work | May be eligible for Universal Credit. |

| Student with a disability | May be eligible for Universal Credit, but must have been assessed before starting the course. |

| Student with a mental illness | May be eligible for Universal Credit if it affects work capability. |

| Student receiving Special Support Grant/Loan | May be eligible for Universal Credit, but it will be deducted from the payment. |

| Student receiving Migration Notice | May be eligible for Universal Credit. |

| Student over state pension age with a partner under pension age | May be eligible for Universal Credit. |

| Student in final academic year | May be eligible for Universal Credit after the last day of the course. |

Explore related products

![]()

Full-time students

As a full-time student, you are not usually entitled to Universal Credit. However, there are exceptions to this rule.

If you are a full-time student and are aged 21 or under, in non-advanced education, and do not have parental support, you may be entitled to Universal Credit. Non-advanced education includes any course up to A-Level or its equivalent. If you are in full-time higher education and are a single parent to a child under one, you may also be eligible, as there are no work-related requirements in this case.

You may also be entitled to Universal Credit as a full-time student if you have reached the qualifying age for Pension Credit and live with a partner who is under that age, or if you are disabled and were assessed as having a limited capability for work before starting your course.

If you are a full-time student and receive student income such as a grant or loan for maintenance, you may still be able to claim Universal Credit, but your student income will be taken into account when calculating your benefits.

Out-of-State Students at Lynn University: What's the Count?

You may want to see also

Explore related products

![]()

Part-time students

If you are a part-time student, you may be eligible for Universal Credit if your course does not prevent you from undertaking work-related activities. If you are expected to look for work and be available for work, you must demonstrate that your course will not hinder your ability to fulfil these expectations. In some cases, you may need to agree to leave your course if you receive a job offer. It is important to discuss this with your work coach, who can provide further guidance on your specific circumstances.

Your student income, including loans and grants, can impact the amount of Universal Credit you receive. Loans for maintenance, such as living costs and rent, are considered income and are taken into account when calculating your Universal Credit payment. However, loans for tuition fees and other study costs are excluded from this calculation. For every £1 you are entitled to receive from a maintenance loan, your Universal Credit amount will be reduced by £1. This deduction is based on your student income for the month, minus any expenses.

It is worth noting that if you receive a Special Support Loan or Grant, this will not be deducted from your Universal Credit payment. A Special Support Loan or Grant assists with study costs such as books, equipment, and travel. You may be eligible for this type of support if you are a lone parent or have certain disabilities.

To determine your eligibility for Universal Credit as a part-time student, it is recommended to speak to a welfare benefits officer, who can provide personalised advice based on your specific circumstances.

Thai University Students: Study, Study, Study?

You may want to see also

Explore related products

![]()

Student loans

Generally, as a student, you cannot get Universal Credit if you are studying full-time. However, there are exceptions to this rule. You may be eligible for Universal Credit if you are a student who meets one of the following criteria:

- You are 21 or younger and in full-time non-advanced education. Non-advanced education is any qualification up to A-Level or its equivalent.

- You are responsible for a child.

- You live with your partner, and they are claiming Universal Credit.

- You are old enough to receive a state pension, and the partner you live with is under the state pension age.

- You have a disability or a mental illness and have limited capability for work. You may also qualify for additional benefits such as Personal Independence Payment (PIP), Disability Living Allowance, Child Disability Payment, Attendance Allowance, or Armed Forces Independence Payment.

If you are studying part-time, you may also be eligible for Universal Credit. You will have to meet other Universal Credit requirements.

If you are a student and are eligible for Universal Credit, your student income, such as loans and grants, can affect how much Universal Credit you get. Loans for tuition fees and other costs of study are excluded. Loans for maintenance, such as living costs and rent, are regarded as income and are taken into account when calculating your Universal Credit. The maximum student maintenance loan you are eligible for will be considered, even if you have received a reduced loan because someone has contributed to your living costs.

Postgraduate Master's Loans in England and Wales include maintenance and tuition fees in one payment. When working out your Universal Credit, 30% of the loan is taken into account as student income, while the rest is ignored. Special Support Loans and Grants, which are intended to support you with study equipment and travel, will be deducted from your Universal Credit payment.

Louisiana's Xavier University: Student Population Revealed

You may want to see also

Explore related products

![]()

Student grants

In the UK, there are several funding options available for students who require financial assistance. These include scholarships, grants, bursaries, and loans. While scholarships, bursaries, and grants do not need to be paid back, loans must be repaid.

Grants are a form of financial support offered to students to fund their studies. Students from low-income households are entitled to an increased loan and a maintenance grant, which does not have to be repaid. The precise threshold for qualifying as a low-income household varies depending on the county in the UK. For instance, for the 2009/2010 academic year, students from England and Wales were entitled to a grant of up to £2,906, while students from Scotland and Northern Ireland were entitled to grants of £2,105 and £3,406, respectively.

Maintenance grants help cover living costs, such as accommodation, food, and books. The amount of maintenance grant received depends on the student's household income, with very poor students receiving the full grant and less poor students receiving a partial grant.

In addition to maintenance grants, there are also Special Support grants intended to support students with the cost of study equipment and travel. These grants are deducted from Universal Credit payments.

Students can also apply for scholarships and bursaries, which, like grants, do not need to be repaid. Each scholarship, bursary, and grant has its own terms and conditions, including eligibility criteria and application requirements. These are offered by various providers, including the university itself, external organisations, and individuals.

Overall, students have access to a range of financial support options in the form of grants, scholarships, and bursaries, which can help reduce their reliance on loans and the associated debt.

Marketing Strategies for Students: University Secrets Revealed

You may want to see also

Explore related products

![]()

Student income

Students can claim Universal Credit, a monthly payment from the government to help with living costs, if they are on a low income or out of work. However, full-time students are usually ineligible for Universal Credit. There are, however, some exceptions.

Full-time students

Full-time students can claim Universal Credit if they meet any of the following criteria:

- They are 21 or younger and in full-time non-advanced education (any qualification up to A-Level or equivalent).

- They are responsible for a child.

- They live with a partner who is claiming Universal Credit.

- They are old enough to receive a state pension, and their partner is under the state pension age.

- They have a disability, mental illness, or health condition that has been assessed as having limited their capability for work, and they are receiving Personal Independence Payment (PIP) or other benefits.

- They have received a Migration Notice telling them to move to Universal Credit.

- They are studying in full-time non-advanced education, do not get a student loan or maintenance grant, and are available for work.

Part-time students

Part-time students may be eligible for Universal Credit if they meet the other Universal Credit requirements and are available for work.

Enrollment Figures: Harvard University Student Population

You may want to see also

Frequently asked questions

Students in full-time education are usually ineligible for Universal Credit. However, there are exceptions, including if you:

- Are aged 21 or under, in full-time non-advanced education and have no parental support

- Have reached the qualifying age for Pension Credit and live with a partner who is under that age

- Have received a Migration Notice telling you to move to Universal Credit

- Are disabled, have been assessed as having limited capability for work before starting your course, and are receiving certain benefits

- Are studying in full-time non-advanced education, do not get a student loan or maintenance grant, and are available for work

Student income, including maintenance loans and grants, is taken into account when calculating Universal Credit. For every £1 you’re entitled to get from a maintenance loan, your Universal Credit will be reduced by £1. However, Special Support Loans or Grants are not taken into account.

You can check your eligibility and find information on how to apply for Universal Credit as a student on the Gov.uk website. You can also use a benefits calculator to check what benefits you could get and find out about further education grants.