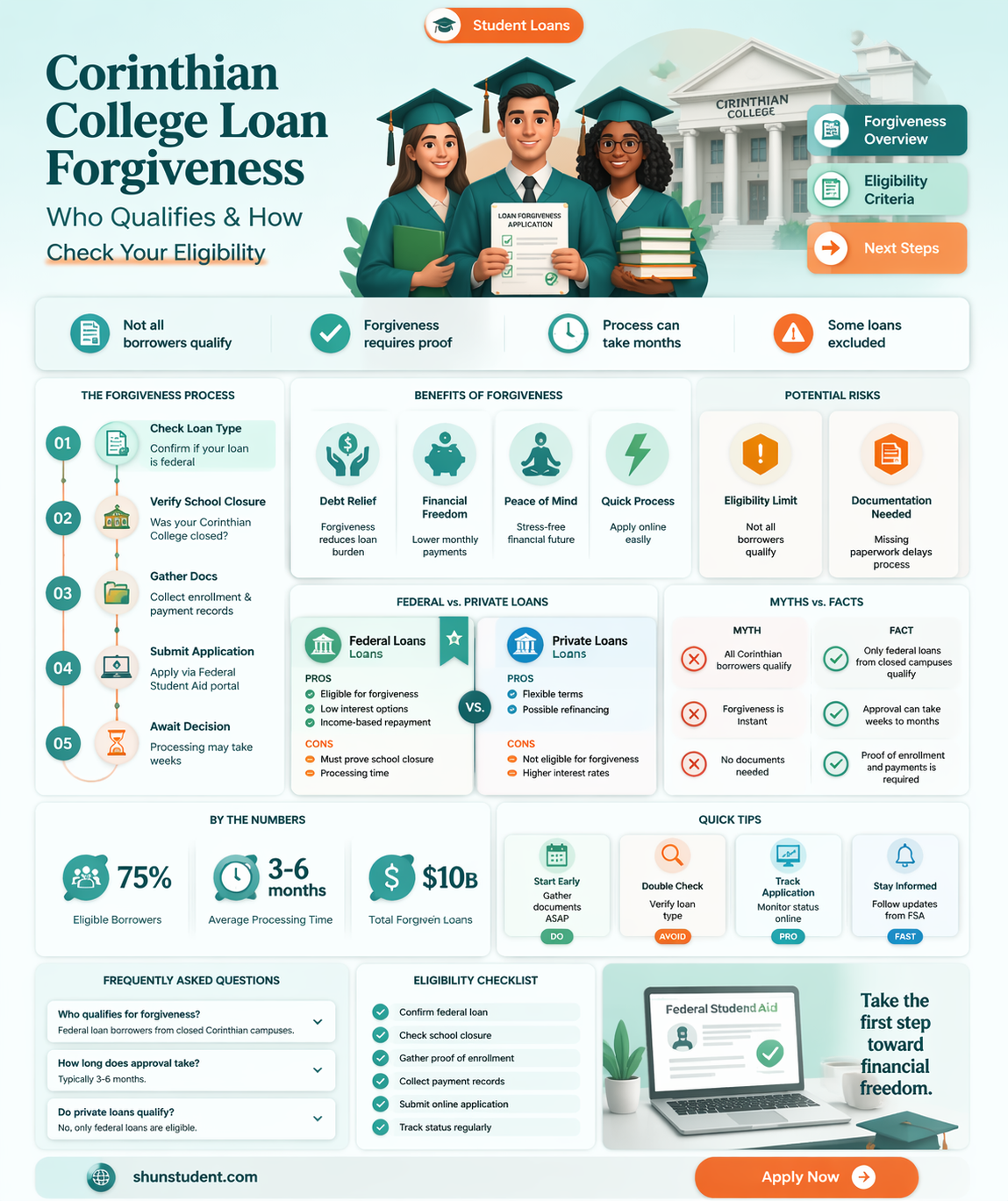

The question of whether all Corinthian College student loans are being forgiven has gained significant attention in recent years, particularly following the collapse of the for-profit institution in 2015. Corinthian Colleges, which operated under brands like Everest, Heald, and WyoTech, faced widespread allegations of fraudulent practices, including misleading students about job placement rates and the value of their degrees. In response, the U.S. Department of Education has implemented targeted loan forgiveness programs, such as the Borrower Defense to Repayment rule, to assist students who were defrauded. While thousands of former Corinthian students have had their loans discharged, the process has been criticized for its slow pace and limited scope, leaving many borrowers still awaiting relief. As of now, not all Corinthian College student loans have been forgiven, and ongoing efforts continue to address the remaining cases and advocate for broader solutions.

| Characteristics | Values |

|---|---|

| Eligibility for Loan Forgiveness | Not all Corinthian College students are eligible for loan forgiveness. |

| Qualifying Schools | Students who attended Corinthian Colleges, Heald College, or Wyotech. |

| Closure Date Requirement | Students enrolled when the school closed or within 120 days prior. |

| Loan Types Covered | Federal student loans (Direct Loans, FFEL, Perkins Loans). |

| Private Loans | Private student loans are not eligible for forgiveness. |

| Application Process | Automatic discharge for eligible students; no application required. |

| Tax Implications | Loan forgiveness is tax-free under the American Rescue Plan Act (2021). |

| Current Status (as of 2023) | Over $5.8 billion in loans forgiven for 580,000 former Corinthian students. |

| Ongoing Litigation | Some cases still pending for additional relief or expanded eligibility. |

| Department of Education Oversight | Managed by the U.S. Department of Education’s Borrower Defense program. |

| Additional Support | Eligible students may receive refunds for prior payments made on loans. |

Explore related products

What You'll Learn

![]()

Eligibility criteria for Corinthian student loan forgiveness

The U.S. Department of Education has implemented specific eligibility criteria for Corinthian Colleges student loan forgiveness, offering relief to thousands of borrowers who were misled by the now-defunct for-profit institution. Understanding these criteria is crucial for former Corinthian students seeking to have their loans discharged. The process is not automatic; borrowers must take proactive steps to determine their eligibility and apply for forgiveness.

Step 1: Attendance at a Corinthian School

To qualify, borrowers must have attended a Corinthian-owned institution, including Everest, Heald, or WyoTech. The school must have closed while the borrower was enrolled or shortly after their withdrawal. For those who attended a school that remained open, eligibility hinges on proof of misrepresentation by Corinthian, such as false job placement rates or accreditation claims.

Step 2: Loan Type and Enrollment Period

Only federal student loans, such as Direct Loans, are eligible for forgiveness. Private loans are excluded. Borrowers who attended Corinthian between 2010 and its closure in 2015 are most likely to qualify, as this period aligns with documented fraudulent practices by the institution.

Step 3: Proof of Misrepresentation

Borrowers must demonstrate that Corinthian misled them about job prospects, program accreditation, or transferability of credits. This can include marketing materials, enrollment agreements, or personal testimony. The Department of Education has streamlined this process through group discharges for certain campuses, eliminating the need for individual attestation in some cases.

Caution: Avoid Scams

Borrowers should beware of third-party companies charging fees to assist with loan forgiveness applications. The process is free, and official applications are submitted directly through the Federal Student Aid website.

Eligible borrowers should apply promptly, as deadlines for certain forgiveness programs may apply. The Corinthian Colleges loan forgiveness initiative represents a significant opportunity for relief, but it requires understanding and action to secure its benefits.

Forbearance Impact: How It Influences Student Loan Forgiveness Eligibility

You may want to see also

Explore related products

![]()

Process to apply for loan discharge

The process to apply for loan discharge, particularly in the context of Corinthian Colleges, involves several critical steps that borrowers must navigate carefully. First, determine your eligibility. If you attended a Corinthian College, including Everest, Heald, or WyoTech, and believe you were defrauded or misled, you may qualify for borrower defense to repayment. This federal program allows students to seek discharge if their school violated certain laws. Not all Corinthian students automatically qualify, so understanding the specific criteria is essential.

Once eligibility is confirmed, gather supporting documentation. This includes enrollment records, loan statements, and any evidence of the school’s misconduct, such as misleading job placement rates or false advertising. The U.S. Department of Education’s Federal Student Aid website provides a borrower defense application form, which requires detailed explanations of how the school deceived you. Be precise and thorough; incomplete applications often delay processing.

Submitting the application is the next step. Applications can be filed online or by mail, but digital submission is faster and more trackable. After submission, the Department of Education reviews the claim, which can take several months. During this period, borrowers may request forbearance to pause loan payments without penalty. It’s crucial to monitor the status of your application and respond promptly to any requests for additional information.

A common pitfall is assuming approval is guaranteed. While many Corinthian students have received discharges, each case is evaluated individually. If denied, borrowers can appeal the decision, providing new evidence or clarifying existing claims. Staying informed about policy updates, such as those announced by the Biden administration in recent years, can also improve your chances of success.

Finally, approved discharges not only eliminate the loan balance but also refund previous payments and restore creditworthiness. However, discharged loans may be considered taxable income, so consult a tax professional to understand potential liabilities. Navigating this process requires patience and persistence, but for eligible borrowers, it offers a pathway to financial relief from predatory lending practices.

Student Loan Forgiveness: Who Qualified and Got Debt Relief?

You may want to see also

Explore related products

$32.98 $44.99

![]()

Impact of school closure on forgiveness

The closure of Corinthian Colleges in 2015 left thousands of students in limbo, burdened by student loan debt and uncertain futures. For many, the shutdown wasn’t just an educational disruption—it was a financial catastrophe. The U.S. Department of Education recognized the predatory practices of Corinthian, including misleading job placement rates and aggressive recruitment tactics, and launched a process to forgive loans for eligible borrowers. However, the impact of the school’s closure on loan forgiveness wasn’t uniform. Students who attended programs that closed while they were enrolled or shortly after withdrawal were prioritized for automatic discharge under the *Closed School Discharge* policy. Those who attended earlier or transferred credits faced a more complex application process, requiring proof of institutional misconduct to qualify for *Borrower Defense to Repayment*. This disparity highlights how the timing of the closure directly influenced the ease and likelihood of loan forgiveness.

Consider the case of two former Corinthian students: one who withdrew six months before the closure and another who was still enrolled when the doors shut. The latter would automatically qualify for discharge, while the former would need to file a Borrower Defense claim, a process that could take years due to backlogs and legal challenges. This example underscores the critical role of enrollment status at the time of closure in determining forgiveness outcomes. For students who attended years before the shutdown, the burden of proof fell entirely on them, requiring detailed documentation of Corinthian’s misconduct—a daunting task for those who lacked access to records or legal assistance. The closure, therefore, created a tiered system of relief, where proximity to the event dictated the path to forgiveness.

From a procedural standpoint, the closure of Corinthian accelerated the development of loan forgiveness policies but also exposed their limitations. The *Closed School Discharge* process, while straightforward, only applied to a fraction of affected students. The broader *Borrower Defense to Repayment* program, though more inclusive, became overwhelmed by the volume of claims, leading to years-long delays. This bottleneck forced many borrowers to continue making payments on fraudulent loans or face collections, compounding their financial distress. Advocates argue that the closure should have triggered a more comprehensive, automatic forgiveness mechanism for all Corinthian students, given the institution’s systemic fraud. Instead, the piecemeal approach left thousands in bureaucratic limbo, illustrating how school closures can strain existing forgiveness frameworks.

For borrowers navigating this landscape, understanding the interplay between closure timing and forgiveness policies is crucial. If you attended a program that closed while you were enrolled or within 120 days of withdrawal, you’re likely eligible for automatic discharge—apply immediately through your loan servicer. If you attended earlier, gather evidence of Corinthian’s misconduct, such as marketing materials, job placement data, or testimony from instructors, to support your Borrower Defense claim. Organizations like the Student Borrower Protection Center offer free resources and templates to streamline this process. Additionally, stay informed about policy updates; for instance, the Biden administration’s 2021 and 2022 actions expanded approvals for Corinthian borrowers, potentially simplifying your case. The closure of Corinthian serves as a stark reminder that forgiveness isn’t just about policy—it’s about timing, persistence, and advocacy.

Qualifying for Student Loan Forgiveness: Your Guide to $10K Relief

You may want to see also

Explore related products

$12.95 $22.99

$8.34 $17.99

![]()

Role of the Department of Education in forgiveness

The Department of Education's role in student loan forgiveness for Corinthian College attendees is pivotal, acting as both gatekeeper and facilitator. It holds the authority to approve or deny claims under specific programs, such as Borrower Defense to Repayment, which allows borrowers to seek discharge if their school violated state laws. For Corinthian students, this means the Department's interpretation of evidence and its application of regulations directly determine financial relief. Since 2015, the Department has approved over $1.5 billion in loan discharges for Corinthian borrowers, yet thousands of claims remain pending, highlighting the agency's central—and sometimes contentious—position in this process.

To navigate this system, borrowers must submit a Borrower Defense application, detailing how Corinthian misled them. The Department evaluates these claims based on state laws and institutional misconduct records. For instance, Corinthian's false job placement rates and aggressive recruitment tactics have been well-documented, strengthening many claims. However, the Department's backlog and shifting policies under different administrations create uncertainty. Borrowers should include specific evidence, such as enrollment agreements or marketing materials, to bolster their case. The Department's role here is not passive; it actively investigates claims, often in collaboration with state attorneys general, making the quality of evidence critical.

Persuasively, the Department’s actions reflect broader policy priorities. Under the Obama administration, it took a proactive stance, establishing a clear pathway for Corinthian borrowers. The Trump administration, however, slowed approvals and proposed stricter eligibility criteria, leaving many in limbo. The Biden administration has since revived efforts, expanding group discharges and streamlining the process. This political ebb and flow underscores the Department’s dual role as both enforcer and advocate. For borrowers, staying informed about policy shifts and engaging with advocacy groups can amplify their chances of approval.

Comparatively, the Department’s handling of Corinthian cases contrasts with its approach to other institutions. While it has prioritized Corinthian due to widespread fraud, borrowers from other schools face higher scrutiny. This disparity highlights the Department’s discretion in defining "misconduct" and its willingness to act on systemic issues. For Corinthian borrowers, this means their claims benefit from a precedent of acknowledged institutional wrongdoing. However, it also underscores the need for continued advocacy to ensure consistent standards across all predatory schools.

Practically, borrowers should monitor the Department’s Federal Student Aid website for updates and deadlines. For instance, the recent expansion of group discharges allows certain Corinthian attendees to receive automatic forgiveness without filing individual claims. Those ineligible for automatic discharge must still submit a Borrower Defense application, ensuring all required documentation is included. Additionally, borrowers should keep records of all communications with loan servicers and the Department. While the process can be lengthy, persistence and attention to detail align with the Department’s criteria for approval, making these steps indispensable for securing relief.

NJ Tax Rules: Student Loan Forgiveness and Your Financial Impact

You may want to see also

Explore related products

$7.99

![]()

Timeline for receiving loan forgiveness approval

The timeline for receiving loan forgiveness approval for Corinthian College students is a critical concern for those burdened by debt from a now-defunct institution. Since 2015, when Corinthian Colleges ceased operations amid allegations of fraud and misconduct, the U.S. Department of Education has implemented several measures to provide relief to affected borrowers. However, the process is not automatic, and understanding the timeline is essential for navigating this complex system.

Steps to Initiate the Forgiveness Process:

- Submit a Borrower Defense to Repayment (BDR) Application: This is the primary pathway for Corinthian College students seeking loan forgiveness. The application requires detailing how the college misled you, such as false job placement rates or accreditation claims.

- Wait for Review: After submission, the Department of Education reviews applications in batches, prioritizing older claims. Processing times have historically ranged from 6 months to several years, depending on application volume and policy changes.

- Receive a Decision: Approved applicants receive full loan discharge, including refunds for amounts already paid. Denials can be appealed, but this extends the timeline further.

Cautions and Delays:

The timeline is unpredictable due to administrative backlogs and policy shifts. For instance, the Biden administration’s 2021 and 2022 actions accelerated approvals for Corinthian students, but thousands of applications remain pending. Additionally, changes in federal leadership or legal challenges can stall progress. Borrowers should continue making payments if required to avoid default, as forgiveness is not guaranteed until officially approved.

Practical Tips for Expediting Approval:

- Gather Evidence: Include detailed documentation of Corinthian’s misleading practices in your BDR application. Admissions materials, marketing claims, and personal correspondence can strengthen your case.

- Stay Informed: Monitor updates from the Department of Education and advocacy groups like the Student Borrower Protection Center.

- Contact Your Loan Servicer: Ensure your account is flagged as pending BDR review to avoid unnecessary collections activity.

While the timeline for Corinthian College loan forgiveness approval remains uncertain, proactive steps can improve your chances of a favorable outcome. Patience, persistence, and staying informed are key as the process unfolds.

Bernie Sanders' Student Loan Forgiveness Plan: What You Need to Know

You may want to see also

Frequently asked questions

Not all Corinthian College student loans are being forgiven, but many former students are eligible for loan forgiveness under specific programs, such as the Closed School Discharge or the Borrower Defense to Repayment program, due to the college's misconduct.

Students who attended Corinthian College while it was under investigation or who were enrolled when it closed may qualify for loan forgiveness. Additionally, those who can prove they were misled by the college about job placement rates or other practices may also be eligible.

To apply, submit an application for Closed School Discharge if the school closed while you were enrolled or within 120 days of withdrawal. Alternatively, file a Borrower Defense to Repayment claim if you were misled by the college. Visit the Federal Student Aid website for detailed instructions and forms.