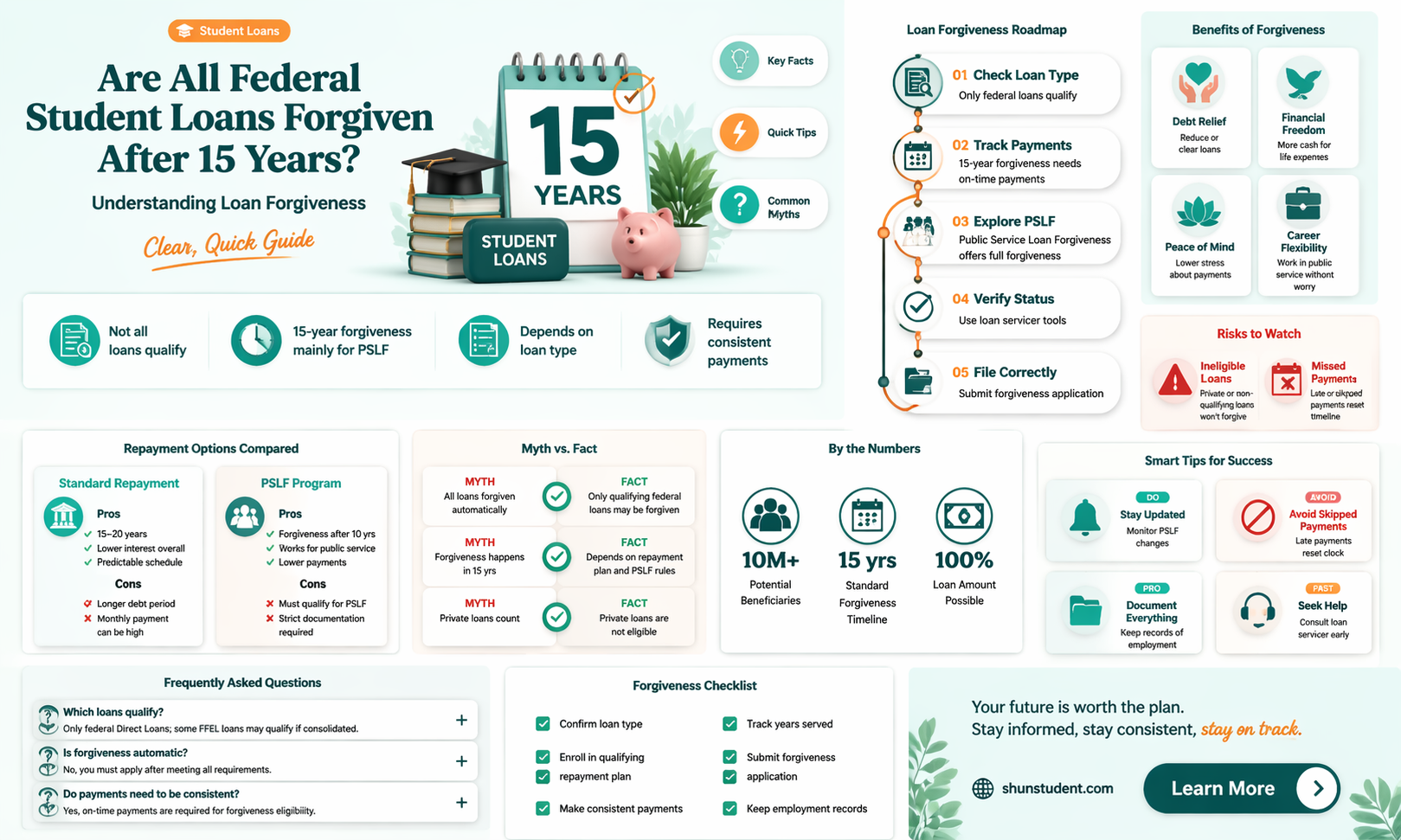

The question of whether all federal student loans are forgiven after 15 years is a common one, often tied to the Public Service Loan Forgiveness (PSLF) program and income-driven repayment (IDR) plans. While it’s true that certain federal loan borrowers may qualify for forgiveness after 15 years under IDR plans like Revised Pay As You Earn (REPAYE) or Income-Based Repayment (IBR), this is not automatic for all borrowers. PSLF, for instance, forgives loans after 10 years of qualifying payments for those working in public service, but the 15-year forgiveness under IDR plans typically applies to borrowers with remaining balances after making consistent payments for that period. Eligibility depends on factors like the repayment plan, loan type, and payment history, making it essential for borrowers to understand their specific terms and requirements.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness After 15 Years | Only applies to borrowers enrolled in the Income-Driven Repayment (IDR) plans. |

| Loan Types Covered | Direct Loans (Subsidized, Unsubsidized, PLUS, Consolidation). |

| Forgiveness Condition | Remaining balance forgiven after 15 years of qualifying payments. |

| Payment Qualification | Payments must be made under an IDR plan (e.g., IBR, PAYE, REPAYE). |

| Tax Implications | Forgiven amount may be taxable as income (check current tax laws). |

| Other Forgiveness Programs | Separate from Public Service Loan Forgiveness (PSLF), which requires 10 years of qualifying payments. |

| Private Loans Eligibility | Not eligible; only federal student loans qualify. |

| Latest Update (as of 2023) | No changes to the 15-year forgiveness rule under IDR plans. |

| Impact of Payment Pause (2020-2023) | Paused payments during COVID-19 count toward IDR forgiveness. |

| Application Requirement | No separate application; forgiveness is automatic after 15 years of qualifying payments. |

Explore related products

What You'll Learn

- Income-Driven Repayment Plans: Forgiveness eligibility after 15 years under specific income-driven repayment plans

- Public Service Loan Forgiveness: 10-year forgiveness for public service workers, not 15 years

- Loan Type Matters: Only Direct Loans qualify for 15-year forgiveness under income-driven plans

- Payment Requirements: Must make 180 qualifying payments under an income-driven plan

- Tax Implications: Forgiven amounts may be taxable as income in some cases

![]()

Income-Driven Repayment Plans: Forgiveness eligibility after 15 years under specific income-driven repayment plans

Not all federal student loans are forgiven after 15 years, but certain income-driven repayment (IDR) plans offer this possibility. Specifically, the Revised Pay As You Earn (REPAYE) Plan and the Pay As You Earn (PAYE) Plan allow for loan forgiveness after 240 qualifying payments, or 20 years. However, for borrowers with undergraduate loans only, this timeline shortens to 15 years under the REPAYE Plan, introduced in 2023. This adjustment underscores the importance of understanding the nuances of IDR plans to maximize forgiveness potential.

To qualify for forgiveness after 15 years under the REPAYE Plan, borrowers must meet strict criteria. First, all loans must be Direct Loans, and only undergraduate loan balances qualify for the 15-year timeline. Graduate loan balances revert to the standard 20-year forgiveness period. Second, borrowers must make 180 qualifying payments while enrolled in REPAYE before the plan’s 2023 update. Payments made under other IDR plans, such as Income-Based Repayment (IBR) or Income-Contingent Repayment (ICR), do not count toward the 15-year threshold unless consolidated into a Direct Loan. This highlights the need to consolidate older loans, like Federal Family Education Loans (FFEL), into the Direct Loan program to qualify.

The calculation of monthly payments under REPAYE further complicates eligibility. Payments are set at 10% of discretionary income, defined as the difference between adjusted gross income (AGI) and 150% of the federal poverty guideline for the borrower’s family size. For example, a single borrower earning $40,000 annually in a state with a poverty guideline of $14,580 would have discretionary income of $25,420. Their monthly payment would be approximately $212, with any remaining balance forgiven after 180 payments (15 years). However, borrowers must recertify income and family size annually to maintain eligibility, as changes in income can adjust payment amounts.

One critical caution is the tax implications of loan forgiveness. Under current law, forgiven amounts are treated as taxable income, potentially resulting in a substantial tax bill. For instance, a borrower with $30,000 forgiven after 15 years could face a tax liability of $7,500 if taxed at a 25% rate. To mitigate this, borrowers should plan ahead by setting aside funds or exploring options like the American Rescue Act’s temporary exclusion of student loan forgiveness from taxable income through 2025. Additionally, switching to a plan like IBR, which caps payments at 15% of discretionary income, may reduce monthly payments but extends the forgiveness timeline to 20–25 years, depending on loan type.

In conclusion, while not all federal student loans are forgiven after 15 years, the REPAYE Plan offers this opportunity for undergraduate loan borrowers who meet specific criteria. Success hinges on consolidating eligible loans, maintaining enrollment in REPAYE, and managing tax implications proactively. Borrowers should use tools like the Federal Student Aid Loan Simulator to model repayment scenarios and consult with a financial advisor to align their strategy with long-term financial goals. This targeted approach transforms a complex process into a manageable path toward debt relief.

Military Reserves and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness: 10-year forgiveness for public service workers, not 15 years

A common misconception about federal student loan forgiveness is that all loans are forgiven after 15 years. This is not entirely accurate. While some repayment plans, like Income-Driven Repayment (IDR) plans, offer forgiveness after 20 or 25 years, public service workers have access to a unique program with a significantly shorter timeline: the Public Service Loan Forgiveness (PSLF) program. This program forgives the remaining balance on federal Direct Loans after just 10 years of qualifying payments for those employed full-time in eligible public service jobs.

To qualify for PSLF, borrowers must meet specific criteria. First, they must work full-time for a qualifying employer, which includes government organizations at any level (federal, state, local), non-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code, and some other types of non-profits that provide certain public services. Second, borrowers must make 120 qualifying monthly payments under an eligible repayment plan while employed by a qualifying employer. These payments do not need to be consecutive but must be made after October 1, 2007, and while the borrower is employed full-time in public service.

One critical aspect of PSLF is the type of loans eligible for forgiveness. Only federal Direct Loans qualify for PSLF. If a borrower has Federal Family Education Loans (FFEL) or Perkins Loans, they must consolidate these into a Direct Consolidation Loan to qualify. This step is crucial, as payments made on non-Direct Loans before consolidation do not count toward the 120 required payments. Borrowers should also ensure they are enrolled in an eligible repayment plan, such as an IDR plan, to maximize their chances of having a remaining balance forgiven after 10 years.

To stay on track for PSLF, borrowers should submit the Employment Certification Form (ECF) annually or when they change employers. This form confirms their employment with a qualifying employer and ensures their payments are counted toward the 120 required. Additionally, borrowers can use the PSLF Help Tool provided by the U.S. Department of Education to determine their eligibility, find qualifying employers, and manage their progress. Staying proactive and organized is key to successfully navigating the PSLF program.

In contrast to the 15-year or longer timelines associated with other forgiveness programs, PSLF offers a clear and achievable path to loan forgiveness for public service workers. By understanding the eligibility requirements, consolidating ineligible loans, and staying organized with annual certifications, borrowers can take full advantage of this program. While PSLF may require more specific qualifications than other forgiveness options, its 10-year timeline makes it a valuable opportunity for those committed to a career in public service.

Forgiving Student Loans: Economic Boost or Burden? A Comprehensive Analysis

You may want to see also

Explore related products

![]()

Loan Type Matters: Only Direct Loans qualify for 15-year forgiveness under income-driven plans

Not all federal student loans are created equal when it comes to forgiveness after 15 years. A critical detail often overlooked is that only Direct Loans qualify for this benefit under income-driven repayment (IDR) plans. If you’re enrolled in an IDR plan like Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), or Income-Contingent Repayment (ICR), and you’ve made 15 years of qualifying payments, your remaining balance can be forgiven. However, this perk excludes Federal Family Education Loans (FFEL) and Perkins Loans, even if they’re federal. To check your loan type, log into your account at StudentAid.gov or review your most recent loan statement. If you have non-Direct Loans, consolidating them into a Direct Consolidation Loan is the only way to make them eligible for 15-year forgiveness under IDR plans.

The distinction between loan types isn’t just bureaucratic jargon—it’s a make-or-break factor for forgiveness. For instance, if you’ve been repaying FFEL loans for 10 years under an IDR plan, switching to a Direct Consolidation Loan resets your payment count to zero but opens the door to 15-year forgiveness. This trade-off requires careful consideration, especially since consolidation can also affect interest capitalization and eligibility for other benefits. A practical tip: use the Loan Simulator tool on StudentAid.gov to model how consolidation impacts your long-term repayment strategy before making a decision.

Income-driven plans tie your monthly payment to your earnings, typically capping it at 10-20% of your discretionary income. For borrowers with low incomes relative to their debt, this structure can lead to significantly lower payments—and, eventually, forgiveness. However, the 15-year clock only starts ticking once you’re enrolled in an IDR plan and have a Direct Loan. If you’re unsure whether your payments qualify, contact your loan servicer to confirm they’re counting toward forgiveness. Keep detailed records of your payments, as servicer errors are not uncommon, and having documentation can save you from costly mistakes.

A common misconception is that all federal loans are forgiven after 15 years, regardless of type. This myth persists because Direct Loans dominate the federal loan landscape today, but older borrowers may still hold FFEL or Perkins Loans. For example, a teacher with $50,000 in FFEL loans won’t qualify for 15-year forgiveness unless they consolidate into a Direct Loan. Consolidation isn’t a one-size-fits-all solution, though—it can disqualify Parent PLUS loans from certain IDR plans and may extend repayment terms. Weigh the pros and cons by comparing your current repayment timeline to the consolidated one, factoring in interest and potential tax implications of forgiven amounts.

Finally, while 15-year forgiveness is a lifeline for many, it’s not automatic. You must remain in an IDR plan, recertify your income annually, and ensure your payments are on time. Missing these steps can reset your progress. Additionally, forgiven amounts may be taxed as income, though current law exempts IDR forgiveness through 2025 under the American Rescue Plan. Stay informed about policy changes and consult a tax professional to plan for potential liabilities. Knowing your loan type and understanding the rules isn’t just about qualifying for forgiveness—it’s about maximizing every payment toward a debt-free future.

Unlocking Student Loan Forgiveness for Radiologic Technologists: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Payment Requirements: Must make 180 qualifying payments under an income-driven plan

Not all federal student loans are forgiven after 15 years, but for those enrolled in an income-driven repayment (IDR) plan, the 15-year forgiveness timeline is a critical milestone. To qualify, borrowers must make 180 qualifying payments under one of these plans. This requirement is non-negotiable and demands careful attention to detail. Qualifying payments are those made on time, in full, and under a specific IDR plan—such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE). Partial or late payments do not count, nor do payments made under the Standard Repayment Plan or while the loan is in forbearance or deferment.

To ensure progress toward forgiveness, borrowers should track their qualifying payments meticulously. The Department of Education’s Federal Student Aid website offers tools to monitor payment counts, but it’s wise to keep personal records as well. For example, if switching IDR plans or consolidating loans, the payment count resets, potentially delaying forgiveness. Borrowers should also be aware of the tax implications of loan forgiveness, as forgiven amounts may be considered taxable income unless they qualify for exemptions under the American Rescue Plan Act of 2021.

Income-driven plans adjust monthly payments based on income and family size, making them accessible for low-income borrowers. However, qualifying for forgiveness requires consistent adherence to these plans. For instance, a borrower earning $40,000 annually with $50,000 in loans might pay as little as $100 per month under REPAYE, but missing even one payment could disrupt the 180-payment count. Practical tips include setting up automatic payments to avoid late fees and annually recertifying income and family size to maintain eligibility for the IDR plan.

Comparatively, the 180-payment requirement is more stringent than the 10-year forgiveness under Public Service Loan Forgiveness (PSLF), which demands 120 qualifying payments. However, IDR forgiveness is available to all borrowers, not just those in public service. For those juggling multiple loans, consolidating into a Direct Consolidation Loan can simplify repayment but may reset the payment count. Borrowers should weigh this trade-off carefully, as consolidating can extend the timeline to forgiveness but may also lower monthly payments.

In conclusion, the 180-payment requirement under an income-driven plan is a pathway to forgiveness after 15 years, but it demands discipline and strategic planning. Borrowers must stay informed, track payments, and avoid pitfalls like missed payments or plan changes that reset the count. While the process is rigorous, it offers a lifeline for those struggling with federal student loan debt, making it a vital option to explore for long-term financial relief.

Unlocking Debt-Free Future: 25-Year Student Loan Forgiveness Application Guide

You may want to see also

Explore related products

![]()

Tax Implications: Forgiven amounts may be taxable as income in some cases

Forgiven student loan amounts can trigger unexpected tax bills, turning financial relief into a liability if you’re unprepared. The IRS generally treats canceled debt as taxable income, but exceptions exist for federal student loans forgiven under specific programs. For instance, loans discharged through Public Service Loan Forgiveness (PSLF) after 10 years of qualifying payments are tax-free. However, loans forgiven under income-driven repayment plans after 20 or 25 years—not 15—may be taxable unless you qualify for insolvency or bankruptcy exclusions. Understanding these distinctions is critical to avoiding a tax surprise.

To navigate this complexity, consider the timing and type of forgiveness program. For example, if your loans are forgiven under an income-driven plan in 2025, the IRS will send a 1099-C form reporting the forgiven amount as income for that tax year. Suppose you’re in the 22% tax bracket and $30,000 is forgiven; you could owe $6,600 in taxes. To mitigate this, consult a tax professional to explore strategies like adjusting withholdings or making estimated tax payments throughout the year. Proactive planning can prevent a lump-sum tax burden that derails your budget.

Comparing tax treatment across forgiveness programs highlights the importance of program selection. While PSLF offers tax-free forgiveness, income-driven plans like REPAYE or IBR do not. Borrowers pursuing PSLF must make 120 qualifying payments while working full-time for a government or nonprofit employer. In contrast, income-driven plans require 240–300 payments but lack the tax shield. If you’re ineligible for PSLF, consider whether the potential tax liability of income-driven forgiveness outweighs the benefits of lower monthly payments.

Finally, stay informed about legislative changes that could alter the tax landscape. The American Rescue Act of 2021 temporarily made all student loan forgiveness tax-free through 2025, but this provision expires unless extended. Monitor updates from the Department of Education and IRS to ensure compliance. For borrowers nearing forgiveness, timing matters: delaying forgiveness until 2026 could mean paying taxes on the forgiven amount unless new legislation intervenes. Knowledge and strategic timing can transform a tax liability into a manageable financial event.

Unlocking Student Loan Forgiveness: Can You Get Partial Relief?

You may want to see also

Frequently asked questions

No, not all federal student loans are forgiven after 15 years. Only borrowers enrolled in the Public Service Loan Forgiveness (PSLF) program or certain income-driven repayment (IDR) plans may qualify for forgiveness after 15 years, depending on the plan and eligibility criteria.

Federal student loans under income-driven repayment plans like Revised Pay As You Earn (REPAYE) or Income-Based Repayment (IBR) may qualify for forgiveness after 15–25 years, depending on the plan. Additionally, borrowers in the PSLF program can have their loans forgiven after 10 years of qualifying payments.

Not necessarily. For income-driven repayment plans, you must make 15–25 years of qualifying payments, which do not need to be consecutive. For PSLF, you must make 120 qualifying payments (10 years), which do not need to be consecutive but must meet specific criteria, such as working full-time for a qualifying employer.